Tesco has now released its final results for the year ending 2015.

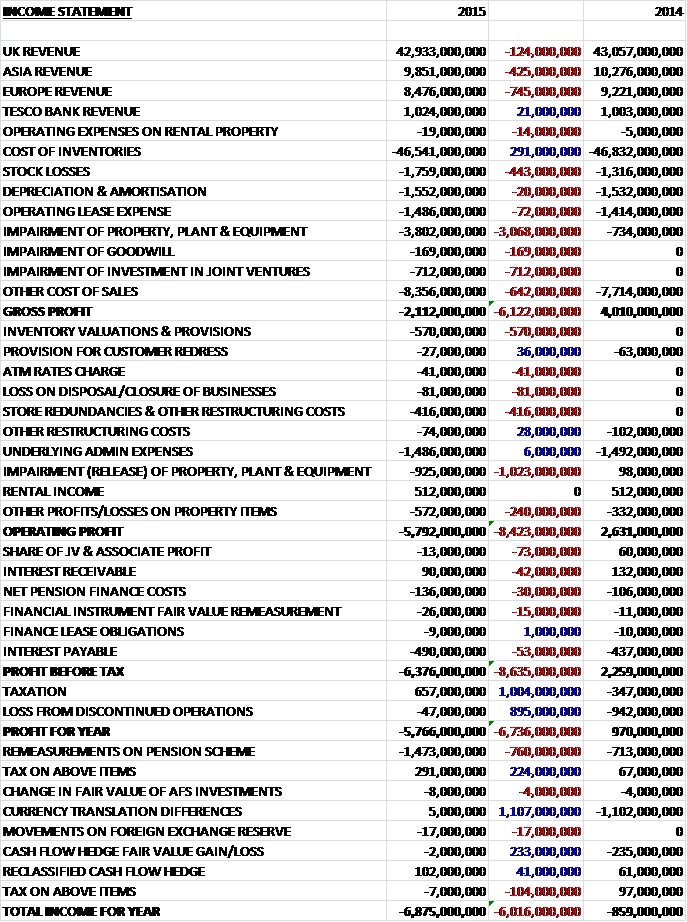

When compared to last year revenues fell considerably as a £21M increase in bank revenue was more than offset by a £745M fall in European sales, a £425M decline in Asia revenue and a £124M decrease in UK revenue. Cost of inventories did fall during the year but this was more than counteracted by a £443M increase in stock losses, smaller increases in depreciation and operating lease expenses, and a growth in other cost of sales. There were also a number of considerable one-off costs which included £3.8BN of impairments to property, plant & equipment; a £712M impairment of joint venture investments and a £169M impairment of goodwill. This all meant that the gross loss came in at £2.112BN, a £6.122BN swing to the negative.

Underlying admin expenses actually fell during the period but this decline was dwarfed once again by some huge one-off costs including a further £925M impairment of tangible assets, a £570M provision against inventory, a £416M charge for store redundancies and restructuring costs and some smaller charges relating to the loss on the closure of a business and an ATM rates charge. We also see a £240M increase in other property costs to give an operating loss of £5.792BN, an astonishing £8.423BN swing to the negative. In addition there was a reduction in the share of associate/joint venture profit, a decline in interest receivable, an increase in pension costs and a £53M growth in interest payable to give a loss before tax of £6.376BN, although this was improved somewhat by the lack of a large loss from discontinued operations and a £657M tax rebate to leave the loss for the year some £6.736BN worse than last year at £5.766BN.

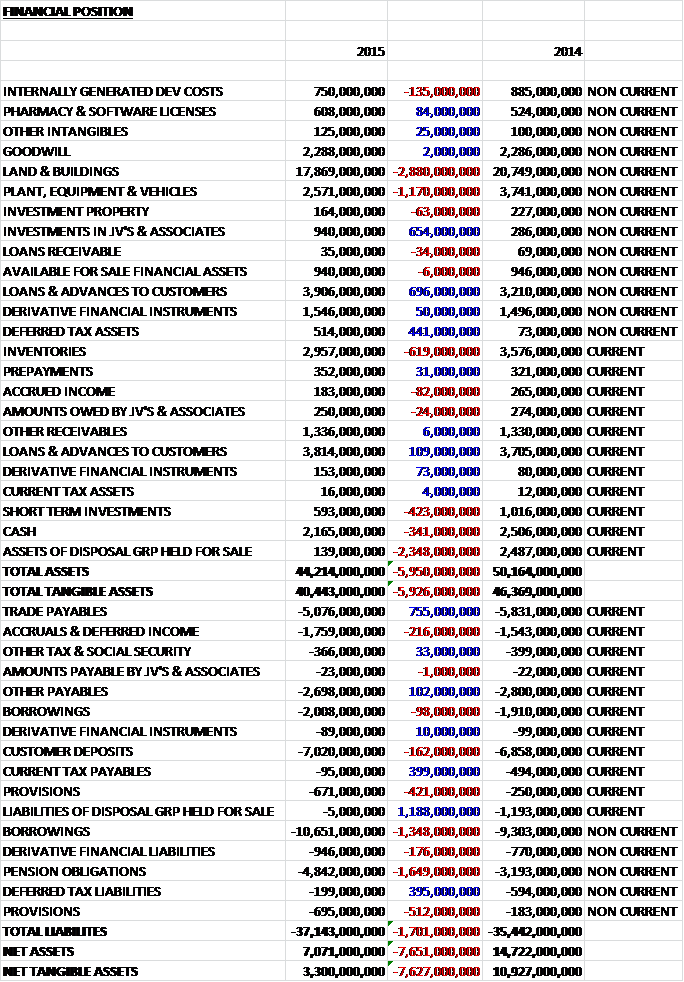

When compared to the end point of last year, total assets crashed by nearly £6BN driven by a £2.88BN fall in the value of land and buildings; a £1.17BN decline in the value of property, plant and equipment; a £2.348BN fall in the assets held for sale, a £619M fall in inventories, a £423M fall in short term investments and a £341M decline in cash levels; only partially offset by a £696M increase in loans to customers, a £654M growth in investments in joint ventures and a £441M increase in deferred tax assets. Conversely we can see that liabilities increased during the period as a £1.188BN decline in liabilities held for sale, a £755M fall in trade payables, a £399M decline in current tax payables and a £395M decrease in deferred tax liabilities were more than offset by a £1.649BN increase in pension obligations, a £1.446BN growth in borrowings and a £933M increase in provisions to give a net tangible asset level of £3.3BN, an incredible £7.627BN crash when compared to last year. It is also worth noting that there is a huge operating lease liability off the balance sheet with a net £14.885BN in non-cancellable leases and when this is considered, this balance sheet does not look very strong at all.

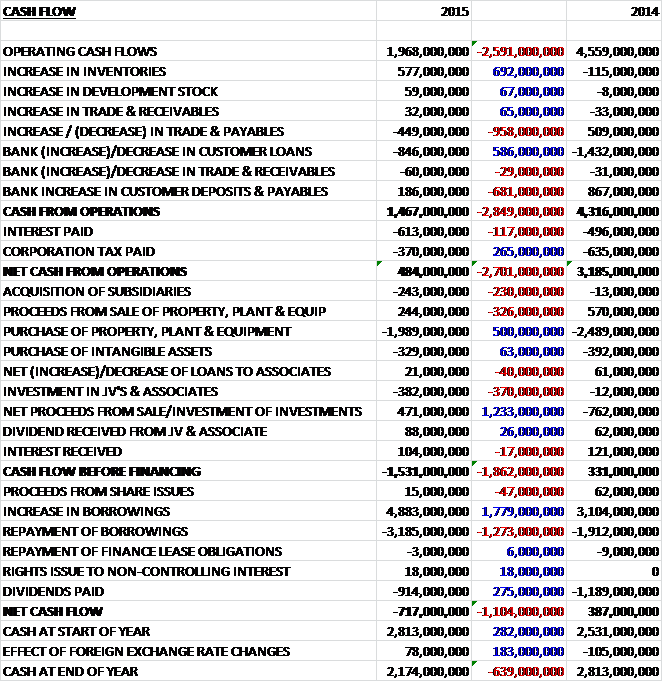

Before movements in working capital, cash profits fell by £2.591BN to £1.968BN before adverse movements in working capital at the bank meant that cash from operations stood at £1.467BN which became just £484M after tax and interest, a decline of £2.7BN when compared to 2014. This was nowhere near enough to pay for the £1.989BN spent on tangible assets and the £329M spent on intangibles but the group did manage to get some £471M from the sale of an investment and £88M in dividends from joint ventures so there was a cash outflow of £1.531BN before financing. There was a net £1.698BN of new borrowings to clear this cash outflow but the payment of 914M in dividends sent the cash flow into negative territory for the year at £717M and at this rate the £2.174BN of cash that the group has will not last much longer despite the suspension of the dividend, although it should be noted that there is some £5BN in headroom from undrawn credit facilities.

The group have been focusing on service, with new staff being hired in customer facing rolls and all head office staff being asked to spend some time working in store; range, with a review taking place across all categories in order to reduce the amount of choice and streamline the range somewhat; availability, which is partly linked to a bloated range, with more space now being given over to the top 1,000 items in store which increases product availability at peak times; and price with both cheaper own brand products and more stable pricing across the board. The board have also identified some £400M worth of cost savings which has led to the closure of 43 unprofitable stores and the cancellation of plans to build a further 49.

The group are also targeting debt and have acknowledged that there is too much. In order to bring this down, a number of decisions have been made, including the cancellation of the final dividend this year, a reduction in capital expenditure to £1BN during the next year, which is about half of that of this year, the replacement of the defined benefit pension scheme and payment of £270M per annum to fund the deficit, and a focus on the leases that contribute to a £1.5BN annual rent bill which has so far resulted in an asset swap with British Land to regain sole ownership of 21 superstores, and finally a review of the peripheral businesses with Blinkbox and Tesco Broadband having been sold or closed and a consultation has begun regarding the future of Dunnhumby.

The changes that the board are making to the group are significant and are likely to result in an increased level of volatility in their performance over the short term. After some of these changes have been made, the group has seen a steady improvement in footfall, transactions and volumes with like for like sales volumes up for the first time in four years but the market is still challenging both overseas and in the UK and many of the changes made will only be felt over the long term. One are that has caused Tesco some embarrassment this year was the commercial income scandal which is now being investigated by the Serious Fraud Office. In order to prevent such a thing happening again, much of the old management have been replaced and there is a focus on cost prices rather than the commercial income received back from suppliers for promoting their products. A new code of business conduct has been introduced to make sure all staff are aware of the issues and to make it easier for staff members to speak up if they suspect some wrongdoing.

It is interesting to see the change in KPIs that are now being used to monitor performance which have been reduced from over 40 to just six. They include customer loyalty as defined by the frequency of shops and average spend, which was down 2.5% this year; the percentage of staff members who would recommend Tesco as a place to work and a place to shop (70% and 77% respectively this year); supplier satisfaction with the company which currently stands at a paltry 58%; group sales, which declined by 1.4% this year; group trading profit which was down some 57.5% this year; and operational cash flow, which fell by nearly 60%. Clearly these have been benchmarked at a low level and customer loyalty seems a bit wishy-washy but I really like the mix of the other five, which suggests the group is really trying to improve some of the core issues surrounding staff, supplier and customer satisfaction as well as the financial performance indicators.

UK trading profit fell by 79% to £467M with sales down 1.7% to £48,231BN and like for like sales down 3.6% which reflects a challenging and deflationary market along with the group’s own underperformance. There has been some recent improvement with Q4 like for like sales falling by just 1%, being driven by positive volumes in response to some of the customer focused initiatives launched in Q3. The full year UK trading margin stood at a wafer thin 1.1%, impacted by lower sales and some of the previously implemented initiatives to reduce price and the reduction in commercial income from suppliers

Asian trading profit fell by 18% to £565M with sales declining by 4.1% which included a 3.2% impact from detrimental foreign exchange movements. In South Korea the impact of the DIDA regulations remained significant whilst in Thailand the recovery in consumer spending was slower than initially expected. The trading performance in Malaysia was impacted by protests against Western owned businesses and a challenging economic environment.

European trading profit declined by 32% to £164M with sales falling by 8.5% which included a 7.9% adverse foreign exchange effect. Whilst there was some improvement in Q4, the like for like sales performance was mixed over the course of the year with strong competition from discount retailers, particularly in Ireland which saw a like for like sales decline of 6.3%. The profitability of the Central European businesses continued to be under pressure and in Turkey there was a £30M charge relating to the write-off of a fuel debtor. Recent legislative changes in Hungary that mandated store closures on a Sunday and the introduction of a “food supervision fee” will have a material impact to ongoing profitability in that country. The group are looking at restructuring the European business, changing the leadership structure to bring Czech Rep, Hungary, Poland and Slovakia into a single structure which should save in costs and improve buying power.

Tesco bank trading profits remained flat at £194M with revenues up 2.1% due to a strong growth in lending to customers offset by the investment in personal current accounts. The business has extended its range of mortgage and loan products with a current account being launched in June 2014. The motor and home insurance business saw a 3% growth in accounts, having expanded its underwriting providers and implementing digital improvements to enhance the customer experience. Losses from joint ventures and associates were £13M, a decline from the profit of £60M that was recorded last year, driven by the loss from the partnership with China Resources Enterprise which was formed in May 2014.

As can be seen, there has been a huge number of one-off costs and charges this year with over £7BN in total, some £600M of which will result in direct cash outflow. The charges included fixed asset impairment and onerous lease charges of £3.8BN against the trading stores due to the challenging industry conditions with a further impairment charge of £925M relating to impairment of work in progress balances and charges relating to the closure of stores; goodwill and other impairments totalling £878M, which included an impairment of £630M relating to the investment in China Resources Enterprises due to increasing competition from Chinese e-commerce companies, £116M relating to Dobbies and other UK businesses and an impairment of £82M in joint venture investments relating to the slow-down of the roll out of Harris + Hoole and Euphorium sites. There was also a £570M charge to the inventory position due to the adoption of a forward looking provisioning methodology and a £168M impact of a reduction in the level of in-store costs capitalised to inventories was also included; £350M relating to restructuring costs and a £208M cost relating the commercial income adjustment.

During the year the group opened some 1.6M square feet of new space but this was offset by the closure of 1.1M square feet, primarily in Turkey and Hungary. The franchised store network continued to grow, mostly in South Korea with a further 600K square feet being planned for opening this year. At the year end, the estimated market value of fully-owned property fell by £7.6BN to £22.9BN due to a weakening of the UK and Central European property markets but this still represents a surplus of some £2.7BN over the book value and another £700M was added to the value of property portfolio following the post-balance sheet deal with British Land.

During the year the group acquired Sociomantic, a Berlin based provider of digital advertising solutions for £124M which included £38M in deferred cash consideration, generating goodwill of £87M. Going forward, the market is still challenging and the board don’t expect to see this change in the immediate future. Good progress is being made on the improvement initiatives that will deliver significant cost savings during the coming year. The immediate priority will be for these savings to be reinvested in the customer offer (which is basically saying not to expect a dividend any time soon).

There will be no final dividend paid this year with future dividends being considered within the context of the performance of the group, free cash flow generation and level of indebtedness, which refreshingly includes operating lease liabilities, a move that I would love to see adopted at some other companies. This sounds sensible enough to me with no dividend expected next year either. Net debt stood at £8.481BN, an increase of £1.884BN year on year but when compared to the end point of last year but when the pension deficit and operating lease liabilities are added on, the level of total indebtedness increases to an incredible £21.719BN (£3.144BN higher). The shares trade on a rather expensive looking 23.3 on underlying earnings, increasing further to 29 in 2016.

Overall then this was clearly a terrible year for Tesco, the group made a reported loss with an underlying fall in profits across all regions, a collapse in net asset values and a reduction in operational cash flows with a negative free cash position. There will be further headwinds in Hungary following new regulations there and the board do not seem to expect any let off in the difficult trading conditions in the near term. Having said that, Q4 was certainly less bad than the rest of the year and I do have confidence in the newish CEO to turn things round long term – there is a very refreshing approach, with honest acknowledgement of the operating lease issue and some good looking KPIs which make me think that this juggernaut will be turned round eventually. I see this as long term though, and in the short term I see better opportunities elsewhere so I have sold out here for now.

After recovering at the start of the year, the share price seems to have started a slow descent from the release of these results.

Tesco have now released an update covering trading in Q1 this year. Overall group revenues fell by 1.3% on a like for like basis excluding VAT and Fuel. This represents an improvement over the decline of 1.8% last quarter, itself an improvement from the quarter before. UK like for like sales fell by 1.3% compared to 1.7% last quarter as a result of continued significant deflation driven by the group’s price investments and weakening commodity markets. Following the significant price cuts on branded products made in January, the group have rolled out similar reductions on more than 300 additional products and seen improvements in their pricing against key competitors. The range reviews are progressing well, enabling them to simplify their offer, reducing prices and increasing availability. They have now completed reviews in fifteen categories, reducing the number of lines by 20% which have helped them get record levels of availability.

Like for like sales fell by 4.4% in Ireland, an improvement on the 6.7% decline last quarter but the weakening Euro had a strong impact and sales at actual exchange rates collapsed by 14.7%. The group have made a significant investment in lower prices in Ireland which helped the like for like sales improve somewhat, although performance was still held back by a difficult competitive environment including high levels of competitor couponing. Elsewhere in Europe, like for like sales on a constant currency basis increased by 2.2% but again the weak Euro took its toll and sales fell by 9.4% at actual exchange rates. Both comparisons represent a decline quarter on quarter. There was a strong performance in the Czech Rep and a step up in performance in Slovakia but the introduction of new legislation in Hungary, including enforced Sunday closures, impacted the business. A significant restructure of the individual Central European country leadership teams to one regional team is largely complete, creating substantial synergies.

In Asia, like for like sales fell by 3% on a constant currency basis, an improvement on the 4.7% decline last quarter. This region benefited from currency exchange rates, however, an at actual rates sales increased by 4.3%. The improvement suggests that customers are responding well to the focused price investments made in fresh food and core groceries in the region but external conditions remain challenging with like for like sales declining in the two largest markets of Korea and Thailand. In Malaysia, an improving underlying trend was more than offset by the negative impact of the introduction of a new tax in April.

Sales at the bank increased by just under 1% due to the expansion of their offer in categories such as loans and mortgages and making the product range accessible to more customers but this was offset by reduced interchange income, relating to the introduction of an EU cap which takes full effect within the next year. Overall then, things are certainly still tough for the group and sales are continuing to decline but the slowdown of this fall has got to be a positive and the super tanker does seem to be slowly turning around.

On the 7th September the group announced the proposed sale of the Homeplus business in South Korea. They have entered into a conditional agreement with entities established by a group of investors led by MBK Partners, including the Canadas Pension Plan investment board, Public Sector Pension investment board and Temasek Holdings. The consideration payable represents an enterprise value of £4.24BN and under the terms of the disposal, Tesco will receive just over £4BN in cash with net proceeds of the disposal being £3.351BN.

The business is profitable with an underlying operating profit of £281M last year but the introduction of the distribution industry development act has had a material impact on store opening hours and trading days at Homeplus with an associated impact on profitability. The net cash proceeds of £3.351BN will be used to strengthen the balance sheet by redeeming certain upcoming bond and commercial paper maturities over the course of the next year and a half. It is expected, however, that the disposal will have a dilutive effect on the earnings per share in the current year and will result in an estimate accounting loss of about £150M.

Clearly the group does need to find some cash from somewhere in order to pay its debts as they come due and the South Korean business has been hit by the new opening hours regulation but I think it is a bit of a shame that a business that clearly has a decent long term future has been sacrificed and I am not sure that this is a good move in the long term.