Tower Resources has now released its final results for the year ending 2014.

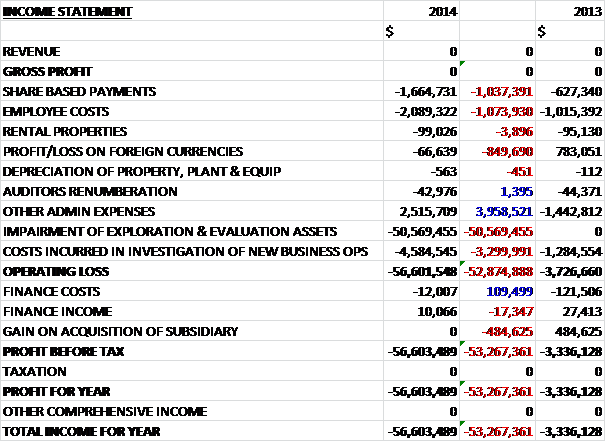

As usual, there are no revenues but we do see a big increase in both share based payments and employee costs. There was also a negative swing to a loss on foreign currencies but these increased costs was counteracted by the “other” admin expenses which relates to the fact that more of these costs were capitalised. There was a $3.3M increase in the costs incurred in the investigation of new business opportunities and a huge $50.6M impairment after the two failed wells in Namibia and Kenya. Finance costs improved considerably but there was a lack of a gain on the acquisition of a subsidiary which occurred last year to give a total loss for the year some $53.3M higher than in 2013 at $56.6M.

When compared to the end of last year, total assets increased by $11.6M, driven by a $25.1M increase in exploration and evaluation assets due to increases in South Africa counteracted by impairments in Namibia and Kenya, partially offset by a $9.5M fall in cash and a $4M decline in goodwill. Liabilities also increased during the period due to a $916K increase in payables to give a net tangible asset level some $10.5M lower at $6.2M for what it’s worth.

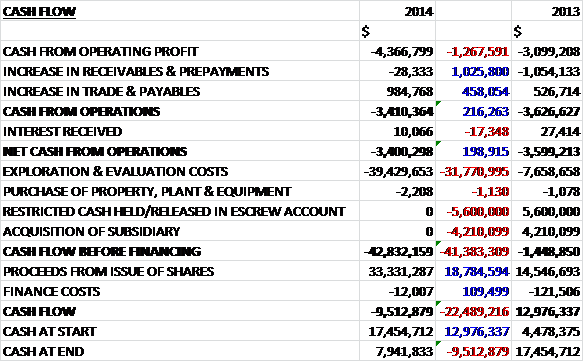

Before movements in working capital, the cash loss increased by $1.3M to $4.4M before a growth in payables gave a net cash outflow from operations of $3.4M, a $216K improvement on last year. The group then spent $39.4M on exploration and evaluation which was partially paid for by proceeds of $33.3M from the issue of shares to give a cash outflow for the year of $9.5M and a cash level of $7.9M at the year-end (which includes some $693K of restricted cash).

The group’s first venture in Cameroon will be the Dissoni offshore block. They were selected as preferred bidder in 2013 and negotiations regarding the production sharing contract have been ongoing since then! They are apparently in the final stages, however, with a conclusion expected in mid-2015. Dissoni lies in the Rio del Rey basin in the Eastern part of the Niger delta where to date over 1 billion bbls have been produced and remaining reserves are estimated at 405 million boe which have come primarily from shallow producing sands at depths of less than 2,000 metres, but there has been very little exploration at deeper depths.

The block has the potential for up to four distinct play systems, including the established producing play in which three discovery wells have already been drilled, which were viewed as non-commercial. The group believes that with better quality seismic, oil reserves can be added to achieve commerciality. The development of a 20 million bbl field should be economically viable and to date some 7 million bbls have been discovered on the block. On signing the agreement, the priority will be the acquisition of 3D seismic in late 2015 or early 2016. The initial exploration period is for three years and the group hopes to be drilling by 2018. Drilling costs in this shallow area would be less than $20M for the shallower targets and a partner will be sought to share the group’s financial commitment and provide additional technical input.

The group became an operator in Zambia upon the acquisition of Rift Petroleum with an 80% interest in blocks 40 and 41. They have now completed all of their initial period commitments in the basin including an extensive programme of geological fieldwork which comprised the evaluation of geophysical data, geochemical analysis and rock sampling to assess the potential for source rock generation and reservoir presence, the results of which indicate that elements for a working petroleum system are present and have been submitted to the Zambian authorities. The three year secondary period has been split into three one year periods with commitments to undertake further field work, airborne gravity and magnetic data acquisition, and a 2D seismic programme. The acreage can be relinquished at the end of each year if results are not good and partners are being sought to fund the work with potential drilling to take place by 2018.

The group’s non-operated interests in the Algoa-Gamtoos and SW Orange basins offshore South Africa also came as part of the Rift acquisition and the operators are New Age Energy and New African Global Energy respectively. On the Algoa-Gamtoos blocks, the processing of 3D seismic data has continued and the first renewal application to the exploration right has been submitted to the South African authorities which is expected to be approved in the second half of 2015 and the group hopes to be in a position to drill by 2017 with a farm out expected before any decision to drill a well. The South West Orange basin is currently held under a Technical Co-operation permit with an application to convert this into a three year exploration right having been submitted. Concerns about the regulatory environment in the country have lessened somewhat by the government’s decision to consult further with the industry.

The group retains a 30% interest in the Repsol operated license 0010 in Walvis Bay, Namibia. During the year, the Welwitschia-1 well targeted five reservoir targets ranging from the Palaeocene-Maastrichtian to the Albian Carbonate sequence at a depth of 3,000m. Only three of these targets were reached and all of these reservoirs were found to be poorly developed. The well was beset by operational difficulties including a delay following the late arrival of the rig, the slumping of a wellhead housing beneath the sea bed which meant the well had to be respudded, and a series of faults with the blow out preventer control system which resulted in suspension for two weeks. The upshot of all this is that the well only reached 2,454 metres with no hydrocarbon finds and with the arrival of the winter season in the South Atlantic, the gross cost of continuing deeper would have been around $40M so the decision was taken to plug and abandon the well. Due to all the delays the well cost much more than anticipated which led to a dispute with Repsol over how much Tower had to pay, which was eventually settled with the group paying $28.3M in total, within the original budget.

The current work programme involves obtaining a fuller understanding of the well results and the implications for the prospectivity of the rest of the license, especially the untested deeper targets including the Albian carbonates with the data from the failed well being tied to the 3D seismic data already obtained. The board still believe that a commercial discovery of oil will happen in Namibia with other international companies planning to drill by 2017. The current strategy is to wait for other operators to begin a fresh drilling campaign in the area before committing to a further well and the Namibian assets have been impaired in the meantime.

In Kenya, after the year end the Bada-1 well was plugged and abandoned as a dry hole. The operator, Lion petroleum, is in discussions with the Kenyan authorities as to how best to complete the evaluation of the remaining prospectivity of Block 2B. One of the other partners, Premier Oil, has given notice to exit the joint venture with Lion and Tower remaining as the sole interested parties. They now wish to fully integrate the well data into geological models to assess the potential in both the Tertiary and Cretaceous areas and a six month license extension to November 2015 has been granted to allow for analysis prior to a decision being made on entering the next exploration phase, although there is not anticipated to be any additional expenditure this year. There is still an injunction preventing physical operations over the bulk of the block, though, with further court hearings expected in Q2 2015 which is a further uncertainty. As a result of the failure, the well costs have been impaired.

The group still holds a 50% interest in the offshore Guelta and Imlili blocks and the onshore Bojador block in Western Sahara. The sovereignty of the territory remains in dispute with Morocco and there is little that can be done to advance exploration of these blocks at the moment. A well was drilled by another company in an area to the north awarded by Morocco but despite finding gas and condensate the discovery was non-commercial, although the find does establish that a working petroleum system exists in the area. In Madagascar, the group continues with discussions with the new government to obtain a license over the previously held area of Block 2102 which are ongoing. In Ethiopia, following a review of an application made by Rift for blocks AB3 and AB6, it was withdrawn. New applications have been made on three other licences and work continues to identify new opportunities but discussions are not being rushed in this low oil price environment.

It is quite interesting to see what the group has actually spent on exploration and evaluation during the year. The most was actually spent in South Africa ($32.3M) with some $29.8M being spent in Namibia, $8.2M in Kenya, $1.3M in Zambia and $35K in Western Sahara. Following impairments in Kenya and Namibia, the capitalised exploration and evaluation assets are $32.3M in South Africa, $1.3M in Zambia and $381K in Western Sahara. As the group does not have any revenue, they need to raise funds by issuing new shares and during the year 550 million were issued that raised $32M. At the end of the year they held about $7.2M in non-restricted cash and it is expected that more funds will have to be raised during the next year to cover working capital needs and committed capital expenditure programmes.

The group does have some exploration expenditure commitments this year with $1.8M still to be paid to fund the remaining Badada-1 well costs in Kenya and a further $741K for extending the PEL0010 license in Namibia which is expiring in August. During the year the group acquired Rift Petroleum, an Isle of Man company with exploration assets in South Africa and Zambia. There were no tangible assets and they paid some $32.2M to acquire the exploration and evaluation assets with 550 million shares. The acquisition gave Tower exposure to a 50% interest in two South African offshore areas.

During the year CEO Graeme Thomson managed to pocket a bonus of more than $1M which is interesting as there seems little that was achieved to warrant this and his total pay package increased from $606K to $1.6M which seems really very excessive to me given the fact that Tower have still not managed to find any hydrocarbons.

After the year-end the group announced that the Badada-1 well had not encountered commercial hydrocarbons and was plugged and abandoned. They also announced that the £20M EFF funding facility with Darwin was not being renewed and 15 million shares were issued under contractual arrangement as part payment for services provided in Q4 2014. There are no drills planned for the coming year.

Going forward, the board point out that successful wells are usually achieved with the help of data obtained from unsuccessful ones and they believe that the group is building valuable data sets and relationships in several basins and countries (albeit expensive ones) that will bear fruit in time.

Overall then, this was clearly a disappointing year for Tower as both potentially high impact wells came up dry. The Cameroon license seems to offer something a bit different with a potentially lower risk, lower impact prospect. In Zambia, the group still seems a long way off drilling but South Africa may offer a prospect of something happening in 2017, although the comment about the regulatory environment is a little concerning. Nothing will happen in Namibia for a few years as the group waits it out to see if any other company’s make interesting finds and I am not too sure if Kenya still offers much in the way of prospects after a dry well that let Premier to jump ship and the continued injunction. The coming year should be quiet with no drilling in this low oil price environment but the group will have to raise further funds nonetheless. The shares I still own are as good as worthless so there is not much point selling them at these levels abut there is not much in the short term that makes me want to buy any more.

On the 28th May the group released a statement confirming Premier’s exit from the Kenya prospect which means that Tower now has a 33% interest and the first exploration period has been extended by 6 months by the Kenyan authorities to the end of November which will give the partners enough time to assess the remaining prospectivity of the block.

This chart is a painful one to holders of the share but there does appear to be a vague upwards trend since the decline after the Kenyan well results.

The group have released an update covering current trading and a new placing. The company has placed 2,904,989,747 shares in the capital of the company at a price of 0.19p to raise proceeds of £5.2M. Following admission of the new shares, the company’s share capital will comprise of 6,735,155,777 shares. When added to the current cash balance of $1.8M, the $8M placing will be used as follows: $5.4M in Cameroon, $2.7M in Namibia, $600K in Zambia, $500K on other licenses and $600K on corporate costs.

In Cameroon the group was selected as the preferred bidder for the Thali block, offshore, in September 2013. The Thali PSC has been negotiated and the board expect to be formally awarded a 100% interest in the block imminently. This block is located in the Rio del Rey basin which to date has produced over one million barrels and has remaining reserves estimated at 1,200M boe, primarily from shallower producing sands at depths of less than 2,000 metres. The block has the potential for up to four distinct play systems including the established play in which three discovery wells have already been drilled. These are currently views as being sub-commercial but with better quality seismic the group sees potential to add incremental oil reserves to achieve commerciality. There is also significant potential to develop prospects at deeper levels one better imaging has been achieved.

The existence of infrastructure in adjacent blocks means that the development of a 20 million barrel field has the potential to be economically viable at current oil prices with 7 million barrels already discovered on the block. On signing of the PSC, the company priority will be the acquisition of 3D seismic in early 2016 which will be used alongside older data to allow better resolution of shallow plays alongside imaging of deeper sections. The initial exploration period is for three years and the group expects to be drilling in 2017/2018. The market downturn in the services sector presents the opportunity for the company to leverage lower seismic and drilling costs and a partner will be sought to share their financial commitment and provide additional technical input.

In Namibia the group is currently negotiating substantial new operated acreage positions offshore. The current exploration period of PEL10, however, only extends to August 22nd and all current license obligations have been met. The next period would require a well to be drilled and the group does not consider that to be currently justified. The area remains of interest, though, and there are plans announced by other companies to drill in the country next year and the year after. In South Africa, the group hopes to see a restart of drilling activity by the industry when the proposed legislative framework is clear but in the meantime their work commitments in this area are minimal.

In Zambia, the company has successfully completed all of its initial period commitments and is well positioned for the next exploration phase. The results from the fieldwork are apparently encouraging and indicate that elements for a working petroleum system are present with the potential for both oil and gas generation, Given the excellent surrounding infrastructure and constrained domestic energy market, it is believed that there is a significant gas to power opportunity in the area. The three year secondary period has been split into one year periods with commitments to further fieldwork (being funded by the placing), airborne gravity and magnetic data acquisition and interpretation along with a 2D seismic programme. The acreage can be relinquished at the end of each annual decision point if results are discouraging. The group is looking for partners to accelerate the programme so that prospects could be drilled in 2017/2018.

The directors of the company have agreed to subscribe for 371,500,000 shares at a cost of $1.1M and M&G, an international asset manager, is investing about $3.55M in the placing which will give them an 18% shareholding in the company.