Tristel have now released their final results for the year ended 2019.

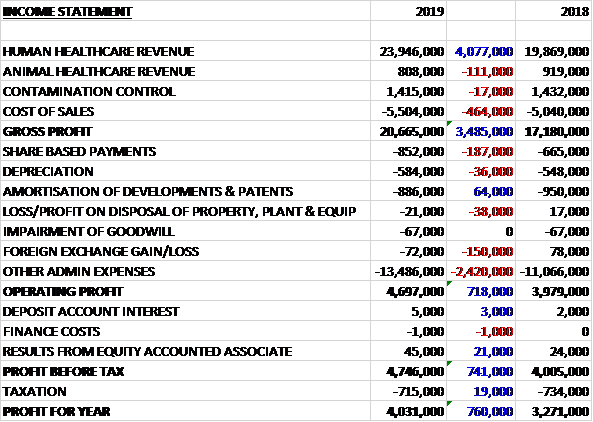

Revenues increased when compared to last year as a £111K decline in animal healthcare revenue was more than offset by a £4.1M growth in human healthcare revenue. Cost of sales also increased somewhat to give a gross profit £3.5M higher. Share based payments increased by £187K, there was a £150K swing to forex losses and other admin expenses were up £2.4M to give an operating profit £718K higher. The profit from the associate increased by £21K and tax charges fell by £19K which meant that the profit for the year came in at £4M, a growth of £760K year on year.

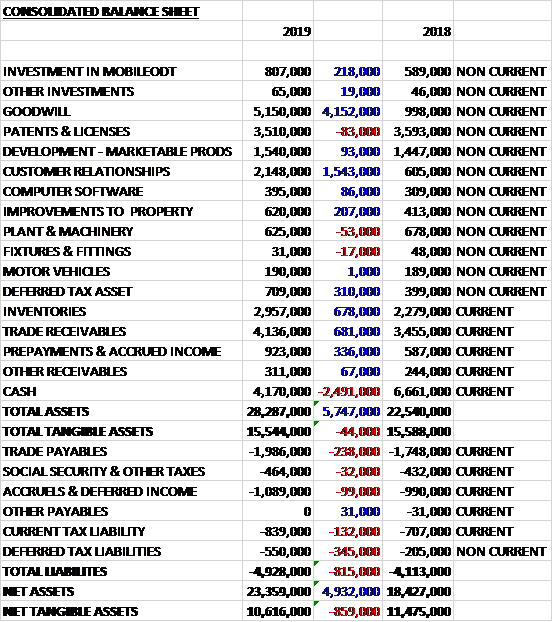

When compared the end point of last year, total assets increased by £5.7M driven by a £4.2M growth in goodwill, a £1.5M increase in customer relationships, a £681K growth in trade revenues and a £678K increase in inventories, partially offset by a £2.5M decrease in cash. Total liabilities also increased in the year due to a £345K growth in deferred tax liabilities and a £238K increase in trade payables. The end result was a net tangible asset level of £10.6M, a decline of £859K year on year.

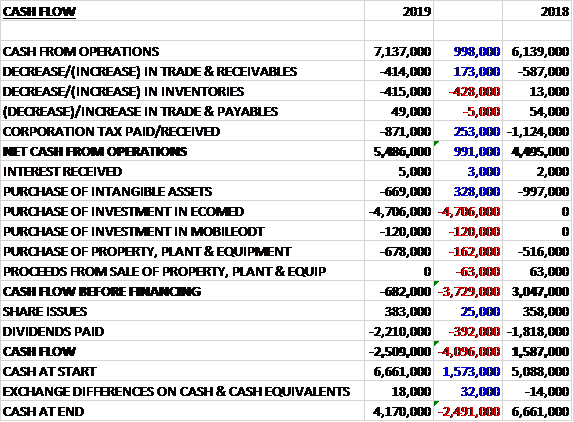

Before movements in working capital, cash profits increased by £998K to £7.1M. There was a cash outflow from working capital, which was broadly the same as last time to give a net cash from operations of £5.5M, a growth of £991K year on year. The group spent £669K on intangible assets, £678K on fixed assets, £120K further invested into MobileODT and £4.7M on Ecomed to give a cash outflow of £682K before financing. They also paid out £2.2M in dividends to give a cash outflow for the year of £2.5M and a cash level of £4.2M at the year-end.

The gross profit in the Human Healthcare sector was £19.2M, a growth of £3.5M year on year. The gross profit in the Animal Healthcare sector was £533K, a decline of £17K when compared to last year. The gross profit in the Contamination Control sector was £922K, flat year on year. Overseas sales grew by 26% and UK sales were up 9% reflecting the differences in market penetration already achieved.

In November 2018 the group acquired their three distributors in Belgium, the Netherlands and France (Ecomed). During the seven and a half month period they were under group ownership, they registered sales of £2.1M which had the effect of increasing group sales by £1.7M. Their direct involvement in the French ultrasound market has been timely with the publication of the new guidelines in the early summer

Whilst no revenues have yet been generated from the US, significant progress has been made to build a commercial platform from which to enter the market. During the year they continued to generate data required for a submission which they intend to make to the FDA to obtain pre-market approval for their foam-based Duo product as a high level disinfectant for medical devices. They have already received approvals from the EPA for Duo. They have entered into a partnership with Parker Labs based in New Jersey by which they have put in place manufacturing capability and a national distribution network.

After the year-end the group acquired 80% of Tristel Italia for £595K which takes their ownership up to 100%.

Going forward, Brexit is yet to occur and has been pushed back, and the board expect the challenges it brings to repeat this year. To forestall any potential disruption to their customers’ supply chain, the group build inventory of all component parts and finished products in the run up to the end of March and encouraged key customers to increase their stock. As Brexit did not take place, they believe that most of their customers’ inventory holdings were then wound down again in the final quarter of the year.

The other significant event relating to Brexit was to move the location of their notified body from BSI’s office in the UK to Amsterdam. They believe this will ensure their ability to CE mark their disinfectants and sell them in Europe irrespective of the outcome of Brexit. Notwithstanding this uncertainty relating to the trading relationship with Europe and the rest of the world, the outlook for the group remains positive.

At the current share price the shares are trading on a PE ratio of 36.5 which falls to 27.6 on next year’s forecast. After a 21% increase in the dividend the shares are yielding 1.7% which increases to 1.9% on next year’s forecast. At The year-end the group had a net cash position of £4.2M compared to £6.7M at the end of last year.

Overall then this has been a decent year for the group. Profits were up, and the operating cash flow improved, although there was no free cash generated after the investment in the distributors. The net tangible asset level deteriorated somewhat. There is not really much to go on as far as trading was concerned, despite Brexit things seem to be ticking along fine. The forward PE of 27.6 and yield of 1.9% looks rather expensive, however, and it is clear that some sales form the US are definitely being priced in.

On the 17th December the group released a trading update. They expect pre-tax profit for the first half of the year to be no less than £2.8M compared to £2.4M last year. This includes a positive contribution from their operations in Belgium, the Netherlands, France and Italy which were all acquired during the past year. They are performing in line with management expectations and the US regulatory approvals project is progressing well.