TT Electronics has now released its interim results for the year ending 2015.

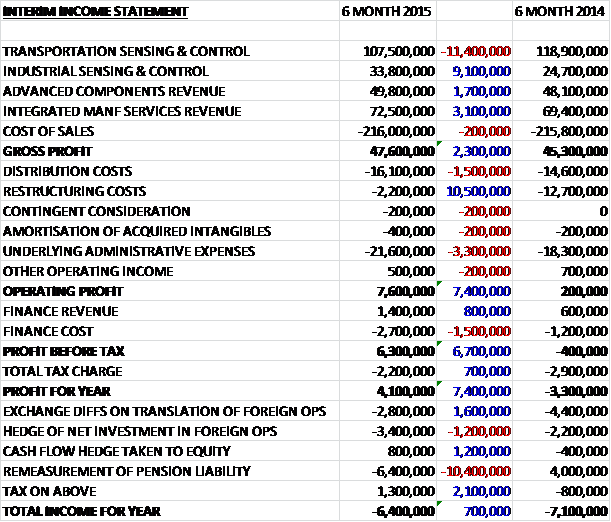

Revenues increased when compared to the first half of last year as an £11.4M decline in transportation revenues was more than offset by a £9.1M increase in industrial revenues, a £3.1M growth in IMS revenues and a £1.7M increase in components revenue. Cost of sales was broadly flat year on year so that gross profit saw a £2.3M increase. Distribution costs increased by £1.5M and underlying admin costs increased by £3.3M but a £10.5M fall in restructuring costs meant that operating profit was £7.4M ahead of last time. An increased finance cost more than made up for a growth in finance revenue and after a reduced tax charge, the profit for the half year was £4.1M, a positive swing of £7.4M year on year.

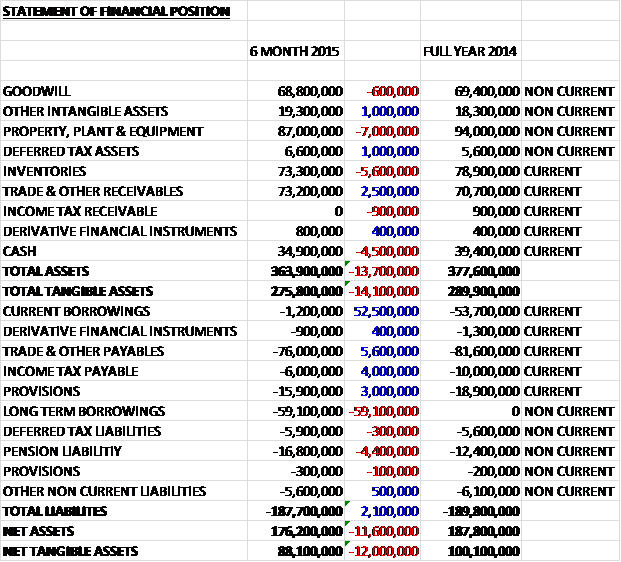

When compared to the end point of last year, total assets fell by £13.7M driven by a £7M fall in property, plant and equipment, a £5.6M decline in inventories and a £4.5M decrease in cash, partially offset by a £2.5M increase in receivables, a £1M growth in deferred tax assets and a £1M increase in other intangible assets. Liabilities also fell during the period as a £5.6M decline in payables, a £4M fall in income tax payable and a £3M decline in provisions was partially offset by a £6.6M increase in borrowings and a £4.4M growth in pension liabilities. The end result is a net tangible asset level of £88.1M, a decline of £12M year on year.

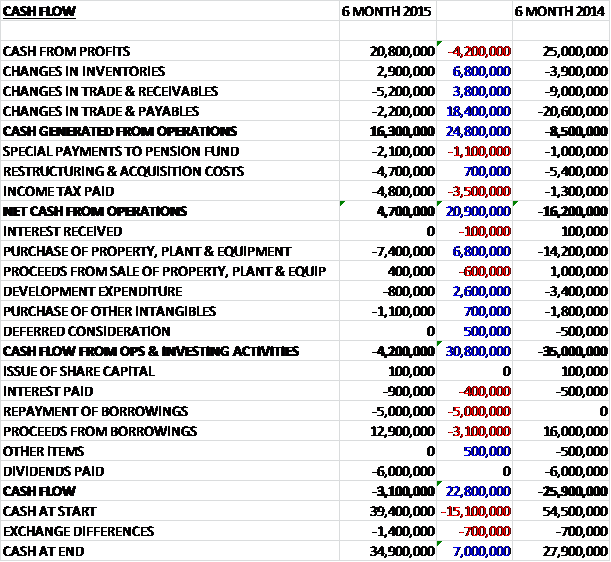

Before movements in working capital, cash profits fell by £4.2M to £20.8M which became £16.3M after a working capital outflow compared to -£8.5M last time after a huge fall in payables in the first half of 2014. After the £2.1M special payment to the pension fund, a £4.7M cash charge relating to restructuring and a similar level of tax, the tax from operations was just £4.7M. This did not cover the £7.4M spent on tangible fixed assets, the £800K spent on development exposure and the £1.1M paid for intangible assets so that before financing there was a £4.2M cash outflow for the half year period. After a net £7.9M increase in borrowings, which covered the £6M paid on dividends, the cash outflow for the period stood at £3.1M to give a cash level of £34.9M at the period-end.

As the group has changed its operating segments slightly, I thought this might be a good opportunity to revisit what they actually do. The Transportation Sensing and Control division develops both sensors and control solutions for automotive OEMs and tier one suppliers including powertrain providers for passenger cars and trucks. The group develops a wide range of products for multiple applications on a vehicle, from power controls, gear position and pedal sensors to fluid and emission sensors, with almost all of them focused on the safety and driver assistance features required by their customers.

The Industrial Sensing and Control division provides products to aid precision, speed of response, reliability and the physical environment. Its position, pressure, temperature, flow and fluid quality sensors are used for critical applications in a range of end markets including industrial automation and process control, medical and aerospace sectors. The Advanced Components division creates specialist, highly engineered electronic components for circuit protection, power management, signal conditioning and connectivity applications in harsh environments. It serves customers in the industrial, aerospace, automotive, defence and medical markets and focuses on creating value by developing innovative electronic solutions to challenging problems on their customers’ electronic circuits or systems.

The IMS division draws on its manufacturing design engineering capabilities, global facilities and world class quality standards to provide complex electronic manufacturing solutions to customers in the aerospace and defence, medical and high technology industrial sectors. The business has broad capabilities ranging from printed circuit board assembly to environmental test and full systems integration. The solutions are focused on low volume, high mix business.

Overall the underlying profit declined by 21% to £10.4M with the reduction relating to a £1.4M increase in R&D expense and £1.9M of contractual price-downs in Transportation Sensing and Control, the £500K non-recurrence of end of life sales in Advanced Components, together with a £2.1M adverse mix impact in IMS. These adverse effects were partially offset by volume growth and cost reductions across the business along with customer requested pull-forward of revenues in advance of a re-sourcing of materials. There was also a £1.2M positive foreign exchange benefit.

The operational improvement plan remains a key area of focus. Of the ten lines planned to be moved from Germany to Romania during 2015, nine have now been transferred, with eight through customer qualification. The focus of the second half of the year is on the transfer of one more line. Six lines are planned for transfer during 2016 and they will continue to evaluate the business case for each line ahead of a final decision to proceed. The transfer of production from Fullerton to Mexicali is expected to be completed in the second half of the year. Overall the operational improvement plan is on track to be completed during the first half of 2017 with full benefits of £5.5M per annum by 2018 – has it all been worth it?

The underlying operating loss at the Transportation Sensing and Control division was £900K, an adverse movement of £3.2M year on year. The reduction was driven by increased R&D expense together with the impact of lower sales prices, partially offset by productivity improvement and cost reduction. During the period the group displaced an existing tier 1 manufacturer for the supply of an advanced next-generation haptic pedal solution for a global premium automotive OEM. This will see the division shift from being a tier 2 component supplier to being the tier 1 supplier of a complex single box solution that should commence in 2018. The group also launched their AdBlue optical fluid sensor for diesel exhaust systems, a product that overcomes the inherent issues with ultrasonic alternatives.

The underlying operating profit at the Industrial Sensing and Control division was £6.4M, a 49% increase year on year with the operating margin increasing from 17.4% to 18.9%. Excluding the favourable foreign exchange impact of £700K, profits increased by 33%. The acquired Roxpur added £300K to operating profit during the period but the bulk of the increase came from a revenue pull-forward due to a customer request ahead of a change in material supply linked to a key programme, and as a result, profits are expected to be weighted to the first half this year.

Following a lengthy design programme with Delta Electronics, the group received the first production order for their latest optical phase diode array, a critical component used in position sensors, particularly in robotic applications. Deliveries are due to commence in the second half of the year and this order seems to validate the strategy of working with customers who require engineering support to develop sensing solutions for their critical applications. The Roxspur business which was required in the second half of last year is being more fully integrated into the division and they are making steady progress to improve elements of their product range. In the first half of the year, Roxspur secured a new 18 months contract with Tata, their largest customer, for high temperature sensors used in a metal processing application.

The underlying operating profit at the Advanced Components division was £3.4M, an 11% decline year on year with a decline in operating margin from 7.9% to 6.8%. This decline was principally as a result of the absence of the high margin non-recurring orders associated with the US Smithfield facility. During the period, a number of new products were released including a custom inverter module for a major aerospace manufacturer, a custom microcircuit for space use and an AECQ200 approved high temperature moulded inductor for automotive use.

In the market of power modules for aircraft electrification the division was approved for participation in two development projects for “Green Taxi” and helicopter safety programmes, both with major European aerospace manufacturers. The enhanced customer focus and more targeted R&D are also realising benefits. After three years of collaboration, the division won its first major automotive programme from a Chinese manufacturer for the magnetic power components for a fuel saving start/stop function.

The underlying operating profit at the IMS division was £1.5M, a decline of 44% year on year as margins contracted from 3.9% to just 2.1%. Without the benefit of a £400K currency movement, the performance would have been even worse due to an adverse product mix which is expected to reverse substantially in the second half of the year. During the period, the division was chosen by L3 as a partner to support the design and prototyping for a new product to help aircraft operators take advantage of the next generation air transportation system traffic management standards. As well as the mature NADCAP-accredited engineering capabilities at the Ohio facility, IMS was also able to offer NADCAP accreditation in the Suzhou and Rogerstone facilities. The division also benefited dorm a number of customer awards for customer service and the Romanian facility received its TS13485 and ISO9001 certification along with numerous successful customer audits.

The pension scheme remains a bit of a problem, the liability widened to £16.8M compared to £12.4M at the end of last year on assets of £451.1M, so it is quite a sizeable scheme. The group will pay £4.3M this year and £4.5M last year and it is disappointing to see that the deficit widened despite the group paying £2.1M towards the scheme during the period – there is a real problem that this could run away from the company if there is a downturn in the value of the scheme assets in the future.

As mentioned by the chairman in his statement, this is a year of transition but current market conditions remain challenging, especially in Europe, although the order book is apparently solid (probably down slightly as no actual figures are given) and the outlook for the full year is unchanged.

At the period end the group was in a net debt position of £25.4M compared to £14.3M at the end of last year. They also had £48.5M of undrawn committed borrowing facilities and £54.4M of undrawn uncommitted borrowing facilities. After the interim dividend was kept the same (they should probably take a break from dividends in the short term in my view) the shares currently yield 3.6% and this is expected to remain the same next year too.

Overall then, this was a transition period for the group and progress seems to be taking some time. Profits did improve year on year but if last year’s higher restructuring costs are taken into account, the underlying profit fell in the first half of this year. Net assets also fell and although operating cash flows did increase, this was entirely due to a huge outflow of working capital last time and underlying cash profits were also lower. The group is not yet generating any free cash so I am not sure I approve of the dividend remaining the same despite the decent cash cushion.

The restructuring seems to be past the hump, although the transition to Mexico should take place in the second half of this year and there are still some lines to move over to Romania. Operationally the Industrial division prevented the situation being even worse but the good performance was due to last year’s acquisition and the pull-forward of an order following a request from a customer, so his is unlikely to do so well in the second half. Elsewhere, the transport division did very poorly, mainly it seems due to higher R&D costs and lower sales prices. The Components division saw profits fall but they were not as drastic as in other divisions and seem to be due to tough comparatives. The IMS division saw a poor product mix, a situation which should reverse in H2.

In conclusion then, I have not really seen enough evidence that things are improving here very quickly and I am a bit disappointed by the falls in underlying profit. We should also be mindful of the pension deficit. So, despite the fact that I actually quite like the company, their products and management I don’t think I will be investing at this time.

The shares have undergone an impressive steady recovery and this does look like a good chart, I am still not convinced though.

On the 17 November the group released a trading update covering the period to the end of October 2015. Overall the group’s performance remains in line with management expectations. For the year to date, revenues have declined by 3% on an organic basis, of which 2% is accounted for by the large non-recurring orders in Industrial Sensing and Control, and Advanced Components delivered last year. General industrial markets have, however, been somewhat weaker during Q3. Whilst the majority of the group’s businesses continues to perform as expected, there has been some impact on the shorter cycle businesses, notably the Advanced Components division, and as a result their order book is marginally lower than in the prior year.

The group have now completed the transfer of ten lines, with nine of them customer qualified. Transfer and qualification of a further two lines is scheduled for H1 2016. The final four lines will remain in Germany, with the transfer of production to Romania now expected to be concluded by the end of the first half of 2016. As a result, they now expect the cost of the programme to be around £25M, about £5M less than originally anticipated and there will be a modest reduction in project benefits. They intend to re-deploy this cash in further cost reduction measures in their shorter cycle industrial market facing businesses. The above actions, together with the group’s enhanced focus on cash flow, mean that they now expect full year net debt to be in the region of £35M.

The transfer of production from Germany to Romania is now expected to be completed a year earlier than anticipated and the group are developing plans to deploy the cash saved in further cost reduction measures. General industrial markets have become weaker in recent months, and the group therefore remain cautious about market conditions. Whilst there has been some softening in the shorter cycle businesses, notably in Advanced Components, this is being offset by earlier realisation of benefits from the operational improvement plan and the outlook for the year is unchanged.

Overall then, there is nothing here that makes me want to buy in just yet. It is clearly possible that the weak industrial markets have further to go and it seems like they are only going to hit targets due to less expenditure on the restructuring which is fortuitous. I will continue to watch here though.

On the 21st December the group announced the acquisition of Aero Stanrew for a consideration of £42.2M. Aero Stanrew is based in Devon and designs and produces electromagnetic components and electronic systems for harsh environments and safety critical applications. The business is focused on the commercial aerospace and defence markets with sole-source positions on key growing platforms. Last year the business reported adjusted EBITDA of £3.2M and gross assets were about £13.6M (although this is pretty meaningless as there could be large liabilities). The acquisition is expected to be immediately earnings enhancing.

The consideration has been settled through a combination of £39.8M in cash from the existing facilities and the issues of 2,576,000 shares to key members of the management team who will remain with the business. I have to say this this doesn’t seem to be that cheap, but without a net asset figure it is hard to confirm this. Also, I am not sure this is the right stage in the group’s recovery for it to be making large acquisitions and given the large debt level now seen here I think the shares are now looking too expensive.