TT Electronics has now released its interim results for the year ending 2016.

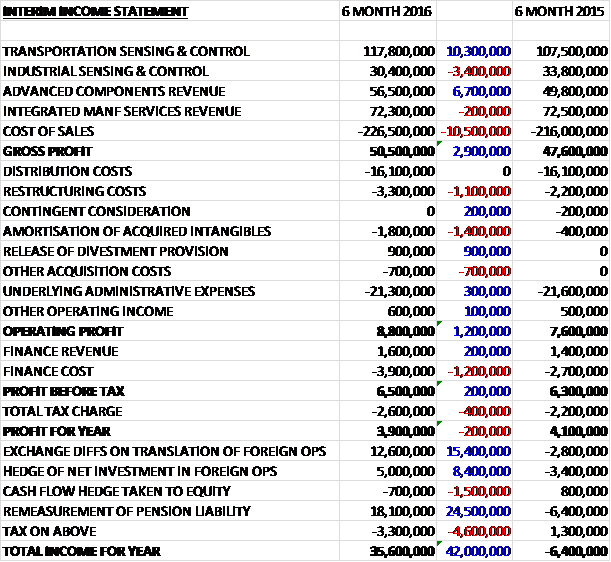

Revenues increased when compared to the first half of last year due to the contribution from Aero Stanrew and favourable currency movements (organic constant currency revenue declined). A £3.4M decline in Industrial Sensing & Control revenue and a £200K fall in Integrated Manufacturing Services revenue was more than offset by a £10.3M growth in Transportation Sensing & Control revenue along with a £6.7M increase in Advanced Component revenue. Cost of sales also grew but gross profit increased by £2.9M. We then see a £1.1M growth in restructuring costs and a £1.4M increase in amortisation of acquired intangibles due to the acquisition although a £900K release of a divestment provision offset a £700K increase in other acquisition costs and after underlying admin expenses saw a modest decline, the operating profit grew by £1.2M. Finance costs increased considerably due to the higher debt levels and tax charges were up £400K which pushes the profit for the period down £200K to £3.9M.

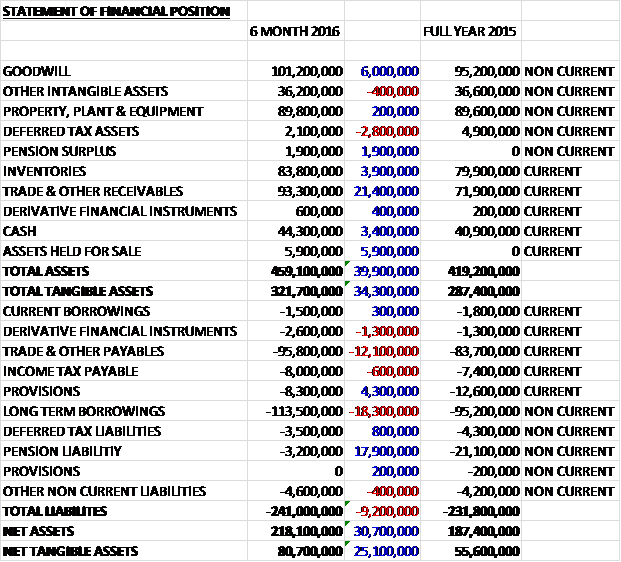

When compared to the end point of last year, total assets increased by £39.9M driven by a £21.4M growth in receivables, a £6M increase in goodwill, a £5.9M growth in assets held for sale, a £3.9M increase in inventories and a £3.4M growth in cash, partially offset by a £2.8M decline in deferred tax assets. Total liabilities also increased during the period as an £18.3M growth in long term borrowings and a £12.1M increase in payables was partially offset by a £17.9M decline in pension liabilities and a £4.5M fall in provisions. The end result was a net tangible asset level of £80.7M, a growth of £25.1M over the past six months.

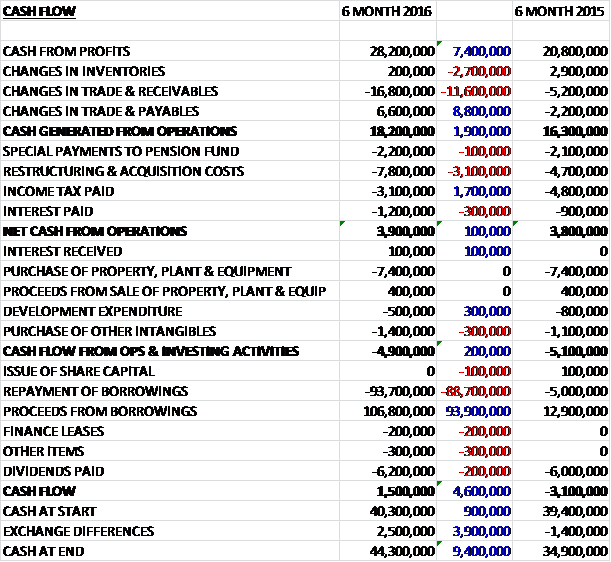

Before movements in working capital, cash profits increased by £7.4M to £28.2M. There was a cash outflow from working capital, apparently related to a very strong 2015 year-end performance, with a large increase in receivables and after £3.1M increase in cash restructuring and acquisition costs and a £1.7 fall in tax payments, the net cash from operations comes in at £3.9M, an increase of just £100K year on year. This was not enough to cover the net £7M spent on property, plant & equipment, the £500K of development costs and £1.4M of other intangible asset costs so there was a cash outflow of £4.9M before financing. The group still paid out £6.2M in dividends so took out more in borrowings to cover all of this which meant that there was a £1.5M cash inflow for the period and a £44.3M cash level at the period-end.

Overall the group’s order book remains sound but the order intake has been mixed across different markets. Strong demand from automotive markets benefited Transportation Sensing and Control and Advanced Components. North American industrial markets remained challenging, however, affecting the performance in Industrial Sensing and Control, Advanced Components and IMS.

The underlying operating profit in the Transportation Sensing and control division was £1.7M, a positive movement of £2.6M year on year on revenues that increased 5%. Organic growth was delivered earlier than anticipated as a result of strong demand in Europe as well as growth in the Chinese market where the business has won new contracts to service the growing domestic demand. The return to profit was supported by the benefits of the Operational Improvement plan as well as ongoing operational efficiencies together with the growth in revenue and a £200K forex benefit.

The division saw continued momentum in China following their strategy to target growth from the sizeable domestic market. They have seen increased production volumes with a large automotive customer for a pedal platform as well as increased volumes for speed sensor crankshaft components. The speed sensor is a redeployment of technology platforms originally developed by the European business. They have also converted two further opportunities for truck pedals into contracts.

They have started to make early progress in the US with their first development order from one of the big three automotive OEMs marking their re-entry into the large US market where they see opportunities to grow market share over the medium term. The development order is for a linear sensor on their SIMPSpad technology for a suspension damper application. These sensors provide car position and speed information using fewer parts than needed before, bringing accuracy, reliability and cost benefits to customer. In France they have won a three year LED project for five different head lamps for a large French OEM.

The underlying operating profit in the Industrial Sensing and Control was £5.5M, a decline of £900K when compared to the first half of last year on revenues that fell 15%. This decline was partly due to last year’s pull forward in demand resulting from a customer request ahead of a change in material supply. North American industrial weakness also had some impact. The profit also suffered from increased R&D expenses although there was a £400K forex benefit to profit.

The group continues with their approach for R&D, targeting industry segments which have an increased requirement for high specification sensors, requiring superior reliability and accuracy such as factory automation and medical equipment. In May, they launched a next generation optical presence and position sensor, Photologic V. The sensor is used in industrial printing and paper handling, factory automation and medical equipment. Collaboration between industrial sensing and control and transportation sensing has resulted in core electronic capabilities from the transportation division being deployed in the launch of a new pressure, TPM, developed in Klingenberg.

The underlying operating profit in the Advanced Components was £4.3M, a growth of £900K when compared to the first half of 2015 on revenues that increased by 11% although excluding the Aero Stanrew contribution there was a 7% organic decline with the base business performance stabilising following the downturn in North American demand experienced in H2 2015. Likewise, the increase in profit was due to the £1.6M contribution from Aero Stanrew and £100K of forex benefits.

The Aero Stanrew business continues to provide components and sub-systems for numerous aerospace and defence programmes where they have single source positions. This includes components for the Joint Strike Fighter programme which has begun to ramp up and volume growth for the Power Distribution Panel, a higher value sub-system designed alongside the customer. The order intake has been strong and is positioning the business well for the growth expected.

The group have seen good progress in their magnetics and connectors offerings, a key area of strategic focus for the division, including wins in the automotive and defence markets. They have also designed a new connector, the Mag-NET, which is being used in demonstration equipment in trials for a large customer in the defence industry.

The underlying operating profit in the Integrated Manufacturing Services division was £2.2M, an increase of £700K year on year on revenue that fell 2% on a constant currency basis as strong demand from China was offset by weakness in North American industrial markets. The increase in profitability was a result of strong cost discipline and ongoing operational efficiency.

The Chinese operation benefited from increased demand from an urban rail infrastructure customer in the country and a contract award for vacuum pumps for semiconductors in South Korea. Conversely the US operations are facing continued market headwinds and in the first half a defence project in the region reached the planned end of its cycle which is affecting volumes. In Europe there have been opportunities to collaborate in Romania with the Transportation Sensing and Control division on PCBs.

Following the acquisition of Aero Stanrew in December, the integration process was executed smoothly and is now complete. The business has performed well and early customer indications have reinforced its potential within the group. Opportunities for increased operational collaboration have been identified in addition to a growing pipeline of prospects in both existing TT and Aero Stanrew customers. During the early stages of integration, Aero Stanrew and IMS worked closely together to win a small initial order for test equipment in the aerospace and defence sector. More recently they have identified the opportunity to utilise their existing expertise and operations in Malaysia to build civil aerospace components for one of Aero Stanrew’s customers. Applicable skills for industrial markets are being adapted to meet the more rigorous testing requirements of their aerospace customers.

The group have announced the transfer of their remaining activities from Fullerton to Bedlington in the UK where they are creating a centre of excellence for power hybrid assemblies. The move is ahead of schedule and they will fully exit the Fullerton site in 2017. They have also announced the transfer of the last of their UK thick film production from Corpus Christi to Mexicali, utilising their lower cost capabilities and consolidating thick film production for the region into a single site. Finally they are closing their Basingstoke site, moving operations to Sheffield and engineering skills to Cambridge where a small team will support R&D efforts across three of the divisions.

As usual there was a decent chunk of non-underlying costs. Restructuring costs related to further costs incurred on the Operational Improvement plan initiated in a previous period as well as costs associated with other site restructuring. Acquisition related costs include a credit of £900K relating to the release of a provision established for warranty liabilities arising from a divestment that is no longer required.

The group is monitoring developments following the UK Brexit vote. Within the EU they have operations in Germany, Austria, Romania and the UK and revenues from the bloc accounted for 16.2% of the total. The board believe that the outcome will not have a significant impact on their ability to conduct business into the EU in the short to medium term but they recognise that they are entering a period of uncertainty as the exit process is agreed and they are monitoring political and macro-economic developments closely.

Whilst the uncertain macro-economic environment continues to impact some market segments, the group’s self-help actions are producing tangible benefits. The combination of the underlying business performance and the contribution from Aero Stanrew mean the board are confident of continued progress in 2016.

At the period-end, the net debt position stood at £70.7M compared to £56.1M at the year-end. They have available £54.4M of undrawn facilities and £53.3M of undrawn overdraft. At the current share price the shares are trading on a PE ratio of 21.8, reducing to 14.2 on the full year consensus forecast, although that would exclude the usual non-underling costs. After the interim dividend was kept the same, the shares are yielding 3.9% which remains the same for the full year forecast.

Overall then, this was a bit of a mixed period for the group. Profits declined but this was due to higher tax costs and pre-tax profit was up modestly. Net assets improved but the operating cash flow was broadly flat and no free cash was generated. Although this was not helped by a large increase in receivables and cash profits increased.

Advanced Components saw profit increase but this was due to the contribution from Aero Stanrew and organic profits declined due to weak North American industrial demand, which has now stabilised. Industrial Sensing also suffered from the North American industrial weakness and profits here declined. Advanced Components saw profits rise due to cost cutting and greater efficiencies but it was the Transportation Sensing division that saved the group really with a swing into profitability due to strong demand in Europe and China along with cost cutting.

Things certainly do seem to be improving here but continued US industrial weakness is an issue, as is the inability to make any free cash – although this should improve as the working capital position unwinds. A forward dividend yield of 3.9% is pretty decent but the forward PE of 14.2 is pretty uninspiring. A tricky one this, TTG is looking more attractive than it ever has since I have started covering it.

On the 17th November the group released an update for the first four months of H2. Overall the group has performed well. As expected, revenues have grown on an organic basis. The order book is marginally ahead of last year, before the additional contribution from Aero Stanrew where the order intake continues to be encouraging. They have secured the first contract win as a result of the integration of Aero Stanrew and the group.

Trading results have been favourably impacted by forex movements, increasing revenue and operating profit in the first ten months of the year by about £30M and £2.5M respectively. The cash generation of the business remains on track to see an improved performance in the second half of the year and in addition, the former head office site in Weybridge was sold in September, generating proceeds of about £6M.

Overall the business performance is in line with plans but is being enhanced by the favourable forex movements so the board expect to be ahead of market expectations for the year as a whole.

This seems pretty good actually, albeit mostly not of the group’s own doing.