Utilitywise has now released its interim results for the year ending 2015.

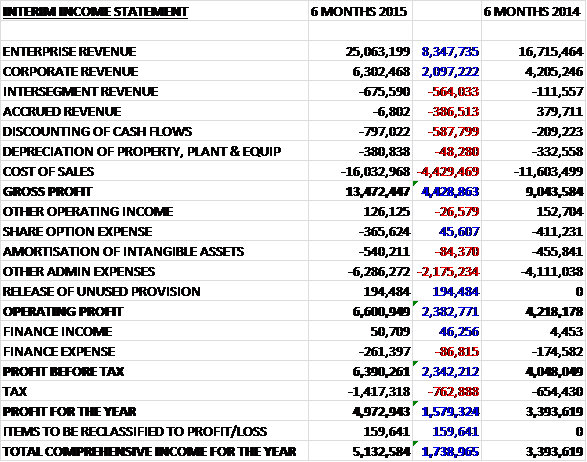

Revenues increased across both sectors year on year with enterprise revenue up £8.3M and corporate revenue increasing by £2.1M. Cost of sales also increased to give a gross profit some £4.4M ahead of the same period of 2014. We then see admin expenses increase, partially offset by the £194K release of an unused provision to give an operating profit some £2.4M higher. Finance expenses increased somewhat and the tax bill almost doubled to give a profit for the year of just under £5M, an increase of £1.6M year on year.

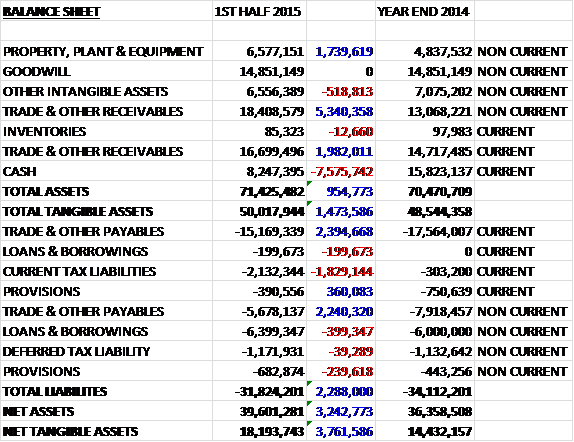

When compared to the end of last year, total assets at the half year point were some £955K higher driven by a £7.3M growth in receivables as the group concentrated on renewing existing customer contracts, and a £1.7M increase in the value of property, plant and equipment partially offset by a £7.6M fall in cash. Liabilities fell during the period as a £1.8M increase in current tax liabilities was more than offset by a £4.6M decline in payables to give a net tangible asset level of £18.2M, an increase of £3.8M over the past six months.

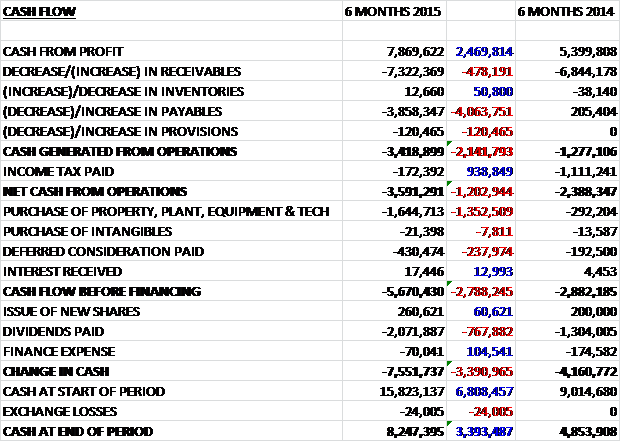

Before movements in working capital, cash profits increased by £2.5M to £7.9M. This was wiped out, however, by the £7.3M increase in receivables and the £3.9M decrease in payables to give a net cash outflow from operations of £3.6M, a decline of £1.2M year on year. The group then spent £1.6M on the purchase of property, plant and equipment relating to the new head office, and £430K on deferred consideration, along with £2.1M on dividends to give a cash outflow of £7.6M for the year and a cash pile at the period end of £8.2M. Hopefully, the group will begin to recoup some of those receivables soon as they will run out of cash at this rate! It is worth pointing out, however, that the group does seem to have a cash outflow in the first half to be reversed in the second half.

The Enterprise division recorded a profit before tax of £5.1M, an increase of £1.8M year on year. This growth was achieved despite operating from a similar revenue generating average headcount before the office move. During the period, there was a consistent renewal rate above 80% in the division. A feature of the first half was an increase in revenue from contract extensions (85% of revenues are recognised at the renewal date) as following the introduction of new, longer term energy supply contracts by several energy suppliers, the group focused on extending and renewing energy contracts for its existing customers. The extension of these contracts for existing customers helped secure revenue, profit and cash flow over the longer term and secured price certainty for customers along with generating revenue for Utilitywise. In all, renewal and extension revenue represented about 42% of the division’s sales in the period compared to 32% in the first half of last year.

For the contract renewals, 85% of revenue is recognised when the contract is extended and they are not included in the company’s secured pipeline. After the period end, the group has increased efforts towards the acquisition of new customers. During the half year, the total customer base increased by 23% to 22,048 and since the period end, the group have secured 1,061 new customers with March representing the highest monthly acquisition performance ever. The Corporate division recorded a profit before tax of £1.4M, an increase of £935K when compared to the first half of last year. This growth was supported by significant customer wins in the medium sizes business space and the renewal rate increased to 98% which sounds impressive.

The two divisions have differing growth prospects with the Enterprise growth being fuelled by the addition of headcount as the group acquires new customers in a market that remains large compared to the current customer count. The Corporate division operates in a much more mature market and some of the growth initially is driven by the transfer of some of the larger customers in the Enterprise division in to the Corporate account managed customer function as their contracts come up for renewal

As far as the KPIs are concerned, the group increased the number of energy consultants by 29% to 449 and the total number of customers increased by 23% to 22,048. The secured pipeline fell by 1%, however, to £23.5M although this did then increase after the period end to some £26M.

The move to the head office was completed on schedule on in budget which now enables the group to accelerate the recruitment of additional staff in order to drive future growth.

The group is still susceptible to a small number of energy suppliers who make up a large amount of revenues with the two largest accounting for 28% and 15% compared to 24% and 18% respectively during the same period of last year. The relationship with these companies remains strong, apparently, and the group has secured new commercial terms with a number of suppliers during the half year.

Going forward, the board believes a significant market opportunity exists for continued profitable growth and they look forward to a second half of continued positive momentum. They consider that they are still at an early stage in terms of their growth potential and there are some exciting opportunities ahead, for example in the water market when it de-regulates in 2017. In the meantime the group is continuing to build their energy services capability and recent government initiatives such as the Energy Savings Opportunity Scheme have presented opportunities to engage with large corporate clients to assist them in their regulatory compliance and reduce energy consumption. The second half of the year has started well and performance over the period is predicted to continue this positive momentum.

After a 55% increase in the interim dividend, at the current share price the shares are on a rolling dividend yield of 1.7% which increases to 2.1% on the full year consensus. At the end of the half year, the group was in a net cash position of £1.6M compared to a net debt position of £100K at the same point of last year, although immediately after the period end the group made a £4M PAYE payment that was related to share awards and then made the acquisition so they will now be back in a net debt position.

After the period end the group acquired T-mac Technologies Ltd for an initial consideration of £10M, £6.25M in cash with the rest in shares. A further £12M could become payable once earn out accounts have been finalised with 70% of this in cash and the rest in new shares based upon six times EBITDA above a hurdle for the years ending the first and second anniversary of completion. In 2015, the acquired group reported EBITDA of £300K on revenues of £3.6M. The initial cash consideration is being funded by a new £25M revolving credit facility, of which £13M will be immediately drawn to fund the acquisition and to refinance the group’s existing facilities.

T-mac has cloud based technology that provides business energy management systems that enable clients to monitor and reduce their utility consumption, make savings and help them comply with government legislation. It services both SME and industrial and commercial customers in the retail, education manufacturing, transport and leisure sectors. Whilst this does seem like a good fit for the group, it does seem as though it has paid a lot of money for a company that only earned £300K in EBITDA last year.

On the 8th May it was announced that Adam Thompson sold 450,000 shares in the company which seem to have been purchased by non-executive Jeremy Middleton. The transaction was worth a whopping £990K and following the announcement, Jeremy owns 2.99% of the total share capital and Adam Thompson owned 2.57%.

On the 3rd June it was announced that the group had been granted a European patent for Edd:e which offers business a measurement and verification tool that helps them make informed decisions about the actions they need to take to save energy. On average it shows customers ways to reduce energy consumption by 27%.

On the 5th June it was announced that non-executive director Jeremy Middleton acquired 300,000 shares at a value of £787K. He really seems to be accumulating at the moment and now has 3.4% of the total share capital which seems like a decent vote of confidence.

On the 10th June the group entered into a three year partnership with the RBS Mentor team to offer energy efficiency advice to customers. RBS Mentor already offers business customers support with employment law, HR protocols, health and safety and environmental management so this adds energy management to the list. Utilitywise will provide on-site energy audits to help business involved in the scheme better understand potential energy savings. The financial implications of this deal are unclear but I would have thought this scheme would enable to the group to reach significantly more customers.

On the 22nd June it was announced that Jeremy Middleton had purchased yet more shares. This time it was 703,603 at a value of nearly £1.9M. This is a very significant purchase and means that he now owns 4.3% of the total equity of the company.

Overall then, this seems like another period of progress, profits and net assets are both up in the six months but operational cash flow as negative due to the increase in receivables from the focus on renewing contracts where the cash receipts are split over a few years. Hopefully this situation will reverse once these contracts start paying out in cash. The group still relies very heavily on one customer, accounting for more than a quarter of all revenues so an investment here clearly has risks which have been amplified by a rather expensive looking acquisition. The shares do yield about 2.1% now though which is decent if unexciting and the good start to the year plus the accumulation by Jeremy Middleton is bullish. In conclusion I think I might look to buy some shares here.

The share price seems to have consolidated recently having climbed from its lows earlier in the year.

On the 12th August the group released a trading update covering the full year to 2015. Revenue for the period is expected to be slightly ahead of market expectations at about £69M, representing growth of about 42% year on year but the important bits are that EBITDA is expected to be slightly below market expectations due to the increased headcount, the initiation of an ecommerce capability, selected European trials and “strengthening” the management team. Also, of note given the fact that the company books revenues years in advance of actually receiving the cash in some cases, the net debt at the year-end increased to £7.5M.

In the Enterprise Division, the levels of new business in H2 have been strong with contract extensions and new customer acquisitions with the latter increasing in Q4. The group also benefited from a continuation of revenue from existing customer contract extensions while the additional headcount started to contribute to revenue and the new customer acquisition focus gained momentum which should be a primary driver of growth in the division going forward. The revenue pipeline that has been secured but not yet recognised stood at £26.2M at the year-end compared to £23.5M at the half-year point.

The Corporate division performed well in the second half and alongside the procurement activity the group is apparently capitalising on revenue opportunities from the EU’s mandatory ESOS initiative together with other adjacent revenue streams including the recently announced RBS Mentor scheme.

At the same time as the above announcement, the group announced that Andrew Richardson, deputy CEO tendered his resignation after spending the last six years at the company to allow him to “take a break from work and to pursue other interests”. Additionally, Steve Atwell has joined the board as MD of the Enterprise division having joined the group from Sage where he was MD of their SMB business across the UK and Ireland.

In all, the EBITDA miss is disappointing but not that detrimental to the investment case in the long term. What is more of an issue is that is seems the group is still unable to make any cash. I will have a closer look when the results are released in October but there is nothing above that makes me want to dip a toe in here.

On the 26th August the group announced that non-executive Paul Hailes had acquired 11,667 shares at a value of nearly £18.5K. He now owns 45,001 shares in the company. This is not a massive purchase but good to see a bit of director buyers at these low prices.