Waterman has now released its final results for the year ended 2016.

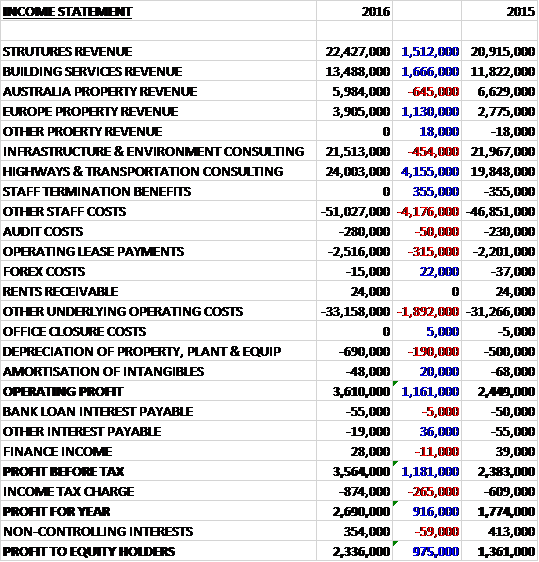

Revenues increased when compared to last year as a £645K decline in Australia property revenue and a £454K fall in infrastructure and environment consulting was more than offset by a £4.2M growth in highways and transportation consulting, a £1.7M increase in building services revenue, a £1.5M growth in structures revenue and a £1.1M increase in European property revenue. Staff costs were up £4.2M, operating lease payments grew by £315K and other operating costs increased by £1.9M to give an operating profit £1.2M above last time. There was a small reduction in finance costs but tax charges increased by £265K as a result of an increase in deferred tax to give a profit for the year of £2.3M, a growth of £975K year on year.

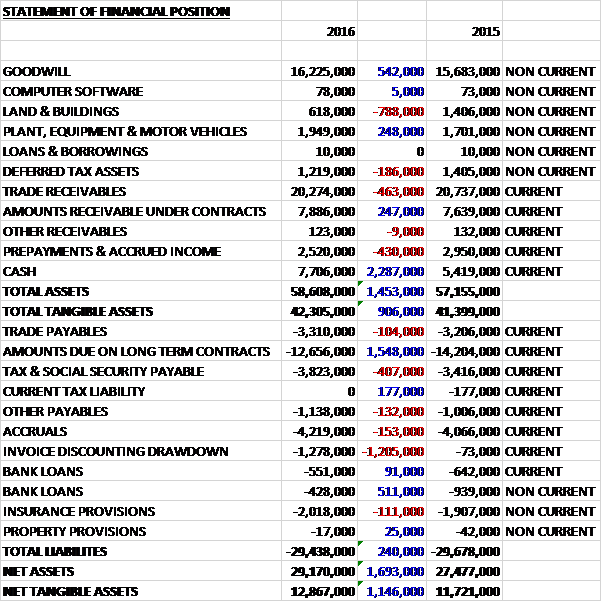

When compared to the end point of last year, total assets increased by £1.5M to £58.6M driven by a £2.3M growth in cash, a £542K increase in goodwill, a £248K growth in plant and equipment and a £247K increase in amounts receivable under contracts, partially offset by a £788K reduction in land and buildings due to an impairment on a Leeds freehold property following a change in its future use, a £463K fall in trade receivables and a £430K decline in prepayments and accrued income. Total liabilities declined during the period as a £1.2M growth in the invoice discounting drawdown and a £407K increase in tax payables were more than offset by a £1.5M decline in amounts due on long term contracts and a £600K fall in bank loans outstanding. The end result was a net tangible asset level of £12.9M, a growth of £1.1M year on year.

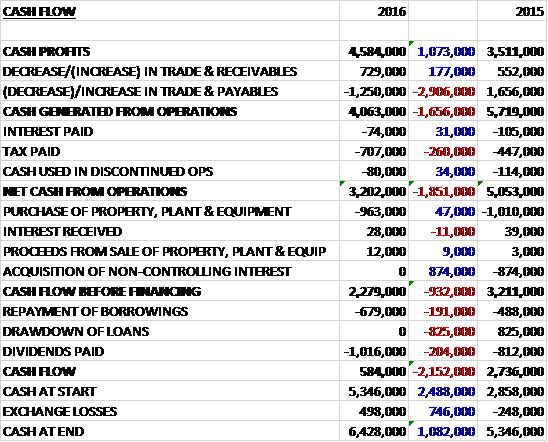

Before movements in working capital, cash profits increased by £1.1M to £4.6M. There was a cash outflow from working capital, however, due to a fall in payables and after tax payments grew by £260K the net cash from operations was £3.2M, a decline of £1.9M year on year. The group spent £963K on capex top give a free cash flow of £2.3M. Of this, £679K went on paying back borrowings and £1M was spent on dividends which left a cash flow of £584K and a cash level of £6.4M at the year-end.

The operating profit in the UK structures consulting business was £1.8M, a growth of £131K year on year following an investment in the recruitment of staff in the previous year. The group won awards for some of their work. New Ludgate was recognised as the best commercial building in London by the RICS and NEO Bankside was shortlisted for the Royal Institute of British Architects Stirling Prize.

The operating profit in the UK building services consulting business was £677K, an increase of £275K when compared to last year. London office development has continued to provide opportunities for the planning and design team and they have many different projects at different stages of the development cycle. The residential market has remained a buoyant source of revenue, London in particular. The workload on education projects has remained at a consistent level throughout the year.

The operating profit in the Australia business was £892K, a decline of £196K when compared to 2015 as the Sydney operation suffered a small loss. The board’s priority is to return this business to profit over the coming year.

The operating profit in the European business was £390K, a growth of £242K year on year. The Irish economy has continued to perform strongly and demand for the group’s services in the country continues to increase. Investment in commercial property remains strong and the residential sector is now becoming more active with output expected to double over the next three years. The property sector in Poland is less buoyant but there has been significant activity in the investment market.

The operating loss in the Infrastructure and Environmental Consulting business was £378K, an improvement of £412K when compared to last year and was not helped by a £300K one-off provision on a project and the impact of a slowdown in planning applications before the London Mayor elections and Brexit. Since June the situation has improved, however, and planning for development in London has returned to normal levels.

The operating profit in the highways and transportation outsourcing business was £921K, a growth of £134K when compared to 2015. The government’s renewed focus on infrastructure project, particularly in the highways market, may create a skills shortage in the future which will benefit the group and margins are likely to increase as they respond to market conditions. The year has seen continued demand for the group’s specialist secondment services but growth in headcount at the start of the year was tempered by some uncertainty around the Brexit vote although government investment in the highways programme and on major infrastructure projects has held up and demand for the group’s services to support public sector capex remains strong.

Reductions in Local Authority headcount and their revenue expenditure has been more than offset by the requirement to deliver a large capex programme and this capital rich/revenue poor status has increased demand. The group won a number of awards through their frameworks and they also secured positions on new framework contracts with Highways England and In Birmingham, West Yorkshire, Manchester and the South West. These long term contracts will provide access to new clients, including newly formed combined authorities and will secure a future pipeline of work.

Diversification into additional sectors, including water and environment, has also given them a broader offering and an expanded client base. The initiative is to establish the same track record and reputation that they have earned in their core highways and transportation market and achieve sustainable, organic growth in these new sectors over the medium term.

The group have recently announced new commissions including Tedding Film Studios and Mortlake Stag Brewery sites in West London (two residential developments totalling over 26.5 acres); Capital Dock for Kennedy Wilson, a 60,000m2 office and residential development which includes the tallest tower in Dublin; and Canary Wharf Group, to assist them with their plans for a further phase of the overall Canary Wharf development which is likely to involve over 200m2 of mixed use buildings.

In the three months since the Brexit vote, the group has continued to experience good levels of enquiries and new commissions and they have not yet noticed any significant change in trading activity. They await clarity on the government’s future plans including for infrastructure investment which will have a bearing on their medium term prospects. The outsourcing business continues to experience high levels of opportunities and has secured new public sector frameworks covering Swindon and W. Yorkshire. Overall the order book has remained at a consistent level year on year of £130M and beyond that the board looks to the future with measured optimism.

At the current share price the shares are trading on a PE ratio of 10.6 which is expected to remain flat on this year’s consensus forecast. After a 50% increase in the final dividend, the shares are yielding 3.7% which increases to 5% on this year’s forecast. At the year-end the group had a net cash position of £5.4M compared to £3.8M at the end of last year.

On the 15th November the group announced that it had been appointed to the MODs Army Basing Programme delivered by Aspire Defence which is set to vastly improve the quality of life for army soldiers. The group will be retained as engineering designer for over 50% of the development programme and the value of the whole construction programme is expected to be about £680M.

On the 9th December the group released a trading update covering the first four months of the year when overall performance was in line with board expectations with revenue slightly above the prior year period, in part due to beneficial forex movements.

As well as the Army Basing Programme, the group were also instructed to progress scheme and tender information for the planned 90,000m2 extension to the Brent Cross shopping centre for Hammerson and Standard Life; they have been appointed by Turner and Townsend to provide technical advice for the feasibility studies of each school under the priority schools building programme; and the group also notes the Autumn statement where the government confirmed its commitment to invest of 1.3BN to ease congestion on roads.

On the 30th January the group released a trading update covering the first half of the year. The board expect to report interim results in line with market expectations with revenue, profit and operating margin generally in line with last year. A continuing emphasis on working capital management has resulted in the group expecting to report net cash of £6.7M at the end of the period compared to £5.5M at the year-end.

Overall then this has been a good year for the group. Profits were up, net assets increased and although the operating cash flow declined, cash profits grew and there was plenty of free cash generated. All divisions saw some improvement except for Australia where the Sydney office incurred a loss. The Brexit vote doesn’t seem to have hurt the group too much but I suppose the work is fairly long term in nature so perhaps this won’t become apparent yet. So far this year, the performance seems to be rather flat but a forward PE of 10.6 and yield of 5% look decent value. Tricky one this, I am not sure if this year is just taking a breather or a sign that business has peaked.