Wentworth Resources has now released its Q3 results for the year ending 2015.

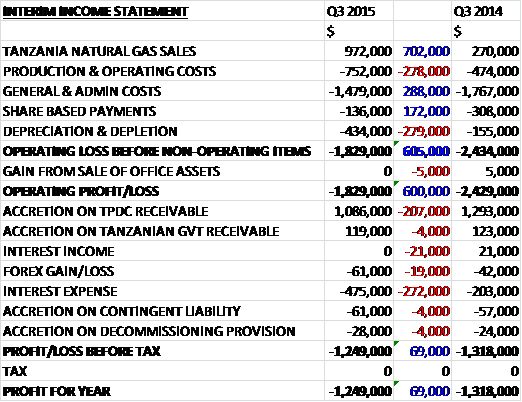

The sales of natural gas in Tanzania increased by $702K when compared to Q3 last year. Production and operating costs also grew, up $278K (including $190K relating to the tax settlement in Tanzania) and depreciation and depletion increased by $279K due to the start of gas deliveries to the pipeline. Offsetting this was a $288K fall in admin costs due to lower professional & legal fees along with office costs that nearly halved, and a $172K decline in share based payments. Although an improvement on last time, there was still an operating loss, however, as the $1.8M loss represented a $600M improvement over last time. We also see a $272K increase in interest expense, which at $475K was pretty much half the total gas sales, but there was a $1.1M accretion on the TPDC receivable as the receipt of these receivables should come closer due to the delivery to the pipeline, so that the loss for the quarter came in at $1.2M, broadly flat when compared to Q3 2014.

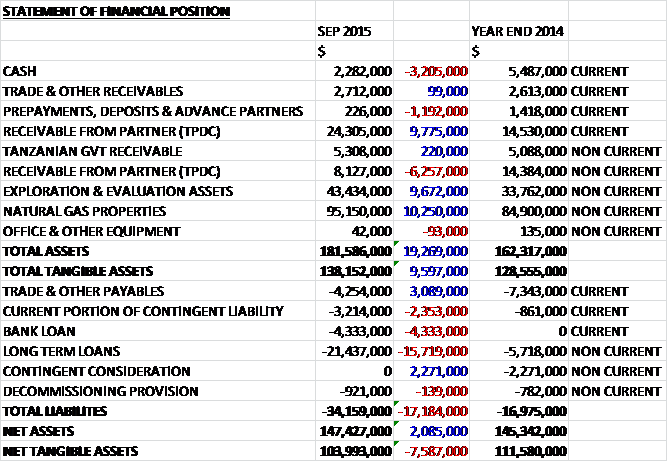

When compared to the end point of last year, total assets increased by $19.3M driven by a $10.3M growth in the value of natural gas properties, a $9.7M increase in exploration and evaluation assets and a $3.5M growth in TPDC receivables, partially offset by a $3.2M fall in cash and a $1.2M decline in prepayments from partners. Total liabilities also increased during the nine month period as a $15.7M growth in long term loans, and a $4.3M increase in current bank loans was partially offset by a $3.1M decrease in payables. The end result is a net tangible asset level of $104M, a decline of $7.6M when compared to the end point of 2014.

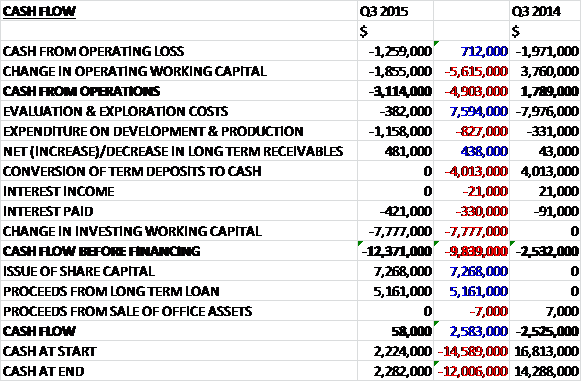

Before movements in working capital, cash losses decreased by $712K to $1.3M but a working capital cash outflow meant that the cash outflow from operations was $3.1M, a detrimental movement of $4.9M when compared to Q3 last year. The group then spent $382K on exploration relating to drilling and operator overheads in Mozambique, $1.2M on production, mainly relating to field infrastructure connection works and $421K on bank interest before another large cash outflow from working capital, this time at the investing stage, meant that before financing there was cash outflow of $12.4M. The group then issued $7.3M-worth of new share capital and increased loans by $5.2M to give a cash flow for the quarter of $58K and $2.3M of cash at the period-end.

The net loss in Q3 of the Tanzania operations was $170K compared to a net loss of $20K in the same quarter of 2014. The group produced 276MMScf, a five-fold increase compare to Q3 last year at an operating cost of $2.72 per MScf. They sold 229,287MMbtu to gas pipeline at a price of $3 per MMbtu compared to none this time last year and 53,188MMbtu to the Power Plant at a price of $5.36 per MMbtu which represented an increase in quantity of 6% due to new electricity customers and lower downtime at the Mtwara power plant. Tanesco has also become more current on settlements for gas sales, paying all outstanding invoices up to the end of July.

The first gas delivery to the Dar es Salaam pipeline started on August 20th. Currently the Mnazi Bay gas field is supplying approximately 45MMscf per day to Dar es Salaam for power generation at the Kinyerezi-1, Symbion and Ubungo power generation facilities with two of the four turbines having been commissioned at Kinyerezi-1. At full operating capacity the Kinyerezi-1 station, excluding a future planned expansion, will utilise about 30MMScf per day of natural gas, while idle capacity at the other plants will consume about 50MMScf per day once they are operating at full capacity. Future gas demand is expected to come from the expansion of the Kinyerezi-1 plant, construction of Kinyerezi-2, 3 and 4, the Kiwa Power station and growth in industrial demand with total demand in Tanzania far exceeding gas supply by the end of 2018.

Under the gas sales agreement, the joint venture partners are contracted to supply up to a maximum 80MMscf per day of natural gas during the first eight months after the commercial operations date, which is expected to be reached during Q1 2016, with an option to increase over time to a maximum 130MMscf per day of gas during the supply contract period which ends in 2031. The first payment for gas was received in early November for gas sales delivered during October. Initial volumes of 640MMscf and 320MMscf delivered during August and September respectively were purchased by TPDC to fill and pack the pipeline, commission the Kinyerezi receiving station and generate power.

The company’s five existing development wells in the concession are expected to produce a combined minimum 80MMscf per day and will therefore be able to meet the initial contracted delivery volume specified in the agreement. Four wells have been tied in to the connection point of the new pipeline and are currently producing a combined 45MMscf per day which is limited to the current nomination from TPDC with gas production expected to reach 80MMScf per day by the end of 2015. The fifth well is currently supplying just 2MMscf per day to the local 18MW power plant in Mtwara which provides the local population with electrical power. The company expects gas sales to the pipeline to increase to 130MMscf per day as market demand grows.

The MB-3 and MS1X wells were both tied in to the connection point of the new pipeline during the quarter while the surface infrastructure activity comprising the installation of separation facilities, piping, flow lines and civil works was ongoing. It is necessary to separate liquids and clean gas ahead of delivery into the pipeline as the joint venture partners are responsible for the properties of the gas such as temperature, water content, pressure and sulphur content.

Given the immediate access to market for the gas and the spare capacity available in the pipeline, the company will seek to advance and exploration drilling programme in 2016. The company expects the cost of these exploration activities to be fully funded from internally generated cash flow.

The net quarterly loss of the Mozambique operations was $140K compared to a loss of $482K in Q3 last year. In July the company provided formal notification of its intention to proceed with an appraisal of the gas discovery in the Tembo-1 well. All the work programme and comments of the Rovuma Onshore Block concession agreement have been fulfilled and the third and last exploration phase of the block expired at the end of August. Anadarko, the current operator and most of the other partners have notified INP of the relinquishment of their participating interests in the block but the group plans to continue with the other remaining party, state owned ENH, and reach an agreement on assigning the participation interest of the relinquished parties, appoint an operator of the block, determine an appropriate appraisal area of the Tembo-1 gas discovery and agree an appraisal plan. A definitive plan is subject to a resolution of these issues and approval granted by the INP to proceed with an appraisal programme.

The processing of the seismic data could take up to 18 months depending on the acquisition parameters and the weather conditions and contingent on identifying a suitable appraisal target, an appraisal well may be proposed. Prior to the allocation of the 73.41% participation interest in production operations relinquished on the block, Wentworth held an 11.59% interest and ENH held a 15% interest.

During the quarter the Tanzanian president assented the Petroleum Act 2015 which became effective in September. Some of the key changes included the formal designation of TPDC as the national oil company and that it shall hold at least 25% of interests in oil and gas blocks except where TPDC decides otherwise but the company does not expect operations in Tanzania to be materially impacted by the introduction of the act, although they continue to engage with industry and government to determine the full extent of the changes in the energy industry in the country. In Mozambique, the government also passed a new petroleum law in 2015 which, among other things, allows the national oil company to compete with other private oil companies and introduces new terms for exploration licenses and new regulations regarding local content. The group does not expect the changes to have an impact on their activities in this country either.

At the end of the quarter there was still a long-term receivable of $33.7M due from Tanzania Petroleum Development Company, a partner in the Mnazi Bay concession. The company currently receives a significant proportion of TPDC’s share of gas sales direct from the operator to reduce the receivables due and during the period they received $1.4M relating to this but this did not even offset the $2.9M share of TPDC’s Mnazi Bay costs that the company paid during the quarter. The group believe that it will be fully recovered within two years which will obviously provide a significant source of cash flow if it comes to pass. There is also $6.5M related from the company’s disposal of transmission and distribution assets receivable from TANESCO but there seems to be little progress being made on actually recovering this amount.

In 2014 the group accrued an estimated tax liability for the period from 2008 to 2012 of $280K and the final tax assessment for the period was received this year and totalled $130K which was settled by way of an offset against a deposit on account with the Tanzania Revenue Authority. Also in 2015, the company received a tax assessment relating to a discontinued subsidiary totalling a hefty $1.2M and covering the period from 2009 to 2012. During the period the company made a cash payment of $250K and in October the TRA approved their request to offset $480K against the remaining deposit on account with the TRA leaving an accrued payable balance of $150K.

At the period-end the group had drawn down the entire $26M credit facilities from its Tanzanian lenders and had just $2.3M of cash left and the first repayment is due in Q2 2016. Following the commencement of gas sales under the long term agreement the company expects to generate sufficient cash flow to meet ongoing obligations extending beyond a year, however.

Gas sales into the new pipeline are expected to reach 80MMscf per day by the end of 2015 as the power plants at Kinyerezi and Ubungo reach full operational status. Production volumes are expected to be maintained at 80MMscf per day for at least eight months to allow for the gas fields within Mnazi Bay to be properly evaluated from a reservoir management perspective.

Overall then this has been a period of progress for the group. The loss has declined somewhat but they are still loss making at the operating level and similarly although the operating cash outflow increased, this was due to the working capital build and underlying cash losses fell. Net tangible assets were also down during the period and the group still seems to be some way off being cash flow positive. The delivery to the pipeline took place in August and this is clearly a very important event for the group. Just as important, TPDC seem to have paid for their gas on time but I have concerns over whether that will continue.

The current delivery rate is 45MMscf per day but the board reckon this will nearly double to 80MMscf by Q1 2016. The new petroleum acts in both countries the group operates in is cause for concern, although the board don’t seem overly cautious about them and in Mozambique, all of the exploration partners don’t seem that impressed by the concession and have relinquished their interest – hopefully Wentworth sees something they don’t. A further drilling programme has been mentioned in Tanzania which it is thought will be self-funding which will be great if true.

The cash levels have become a bit precarious here. They have $2.3M left in the bank and are fully drawn down on their debt with the first repayment due in Q2 2016. It is vital, therefore, that TPDC continues to make regular payment and that huge long-term receivable is clawed back from them. If this doesn’t take place it would appear further funding will be necessary. Having said that, the prospects here are rather exciting and whilst nothing ever seems to run smoothly for oil and gas operators in Africa, I retain the faith and hold these shares in the small speculative part of my portfolio.

On the 13th January the group released an operational update. In Q4, gross gas production into the pipeline and directly to a power plant in Mtwara averaged 46MMscf per day with production averaging 55MMscf in December. To date, growing gas demand from the power sector has been impacted to delays experienced in commissioning the new Kinyerezei power plant and the conversion of the Ubungo power plant from diesel to gas. These delays are considered to be short term in nature and all of the power generation facilities that will utilise Mnazi Bay gas in the generation of electricity are expected to become fully operational during Q1.

As a result, production volumes into the pipeline are now expected to reach between 70 and 80MMscf per day during Q1 and remain at that level for the rest of the year. The existing wells performed in line with expectations and are expected to be more than capable of meeting expected demand so no development wells are planned for the year.

Payments by TPDC have been paid in accordance with the agreed terms and the company ended the year with $2.7M in cash and debt of $26M, of which $7.4M is due to be repaid from cash flows in the second half of the year.

While the delay is a bit disappointing and adds a bit of uncertainty, the story remains good here in my view, although if any further delays are incurred the company could have trouble paying the debt that comes due this year.

On the 17th February the group announced the resignation of non-executive director Richard Schmitt with immediate effect after five years at the company to allow him to pursue his other business opportunities.