Bonmarche has now released its interim results for the year ending 2016.

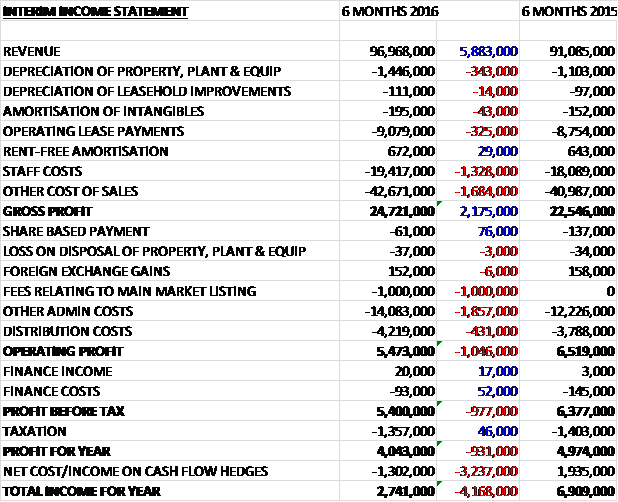

Revenues increased by £5.9M when compared to the first half of last year but we also see an increase in depreciation, operating leases, staff costs and other cost of sales so that the gross profit increased by £2.2M. Underlying admin costs were up £1.9M and distribution costs increase by £431K but the £1M fee relating to the main market listing takes the operating profit £1M below that of last time. Finance costs were fairly negligible and tax was slightly lower so the profit for the first half of the year was £4M, a decline of £931K year on year.

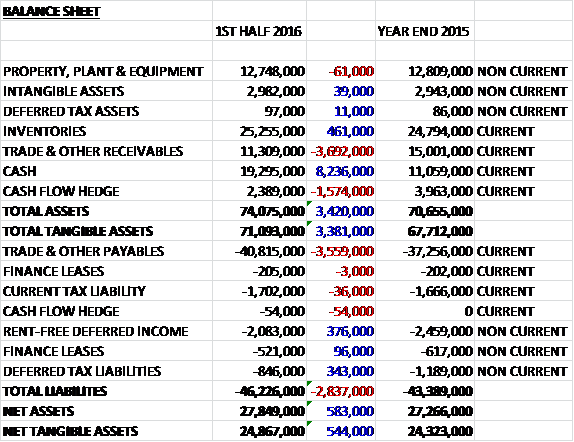

When compared to the end point of last year, total assets increased by £3.4M driven by an £8.2M growth in cash and a £461K increase in inventories, partially offset by a £3.7M fall in receivables and a £1.6M decline in the value of the hedging instrument. Total liabilities also increased during the period as a £3.6M growth in payables was partially offset by a £376K decline in rent-free deferred income and a £343K fall in deferred tax liabilities. The end result is a net tangible asset level of £24.9M, an increase of £544K over the past six months.

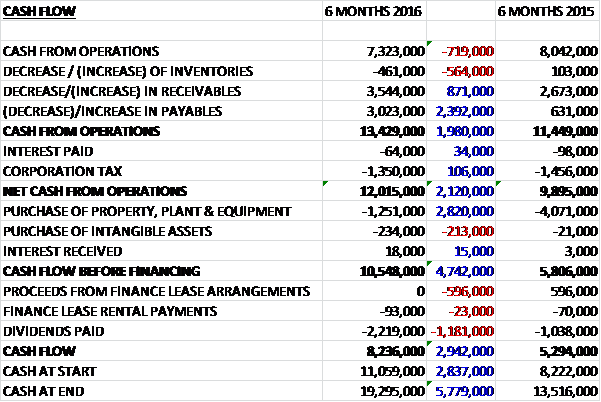

Before movements in working capital, cash profits fell by £719K to £7.3M. There was a large cash inflow from working capital, however, with a fall in receivables and a growth in payables due to the timing of stock and capex payments of £1.7M which had previously been expected to be paid during the period and slipped into the second half. There was also £1M in main market listing fees that were unpaid at the period-end. The tax payment was also lower than last time so that the net cash from operations was £12M, an increase of £2.1M year on year. They then spent £1.3M on property, plant & equipment and £234K on intangible assets to give an impressive free cash flow of £10.5M. After the dividends were paid along with a small amount of finance lease rentals, the cash flow for the first half of the year came in at £8.2M with a cash level of £19.3M at the period-end.

The adjusted profit, not including the main market listing cost was in line with the first half of last year which had benefited from particularly good sales during the summer, driven by good weather. The summer of 2015 was more typical of the norm, although there were few prolonged spells of fine weather after April.

During the first half of the year, store like for like sales increased by 2%. During Q1 there was store like for like contraction of 1.7% compared to a growth of 13.5% in the first quarter of 2015. The comparatives softened for Q2 and as a result they achieved a 6.1% store like for like growth in Q2. During the period the group opened a net eight new solus stores and concessions.

During the first half, online sales grew by just 4.2% compared to last year. They grew by 11.4% during Q1 but during Q2 there was a decline due to disruption connected with the launch of the new responsive website. It was launched in July and its development required making significant changes to the underlying structure of the site which interrupted the operation of SEO, an important generator of traffic. As a result, online sales during Q2 were 3.6% lower than last year. Following the launch of the site, work has been carried out on rebuilding the SEO links, using a new digital agency, and it is expected that online sales will show year on year growth by the end of the year. The website itself seems to be performing well and has been voted the “best online shop” alongside John Lewis in a Which report.

The group are in ongoing discussions with Oracle, the supplier of the new EPOS system, about the continuation of the rollout of its “Retail J” system. It is hoped that they will be in a position to move this project forward soon. Although the delays to the rollout of the new EPOS system have been disappointing, most of the behind the scenes work is complete and there is relatively little to do in terms of further development.

The product gross margin was lower than last year as the average summer conditions necessitated a more normal level of discounting in order to clear summer stock at the end of the season. Underlying operating costs increased as a result of the addition of new space, inflation, the launch of an improved delivery service to stores in June, a trial of TV advertising which began in September, new hires to strengthen marketing, and higher costs of online marketing due to the problems with SEO.

Greater emphasis is now being placed on bringing the company to the attention of people who don’t know the brand. A new media agency is working on offline marketing, as well as online in order to achieve a greater consistency in the group’s marketing. In the autumn, a test TV advertising campaign comprised two phases has been conducted in northern TV regions. Prelim results from the first phase broadcast in September are promising, and the analysis of the second phase is in progress. The rationale for investing in further advertising is sound in principle, but there is more work to do to establish where the right balance lies between short term costs and the longer term benefits from increasing brand awareness.

Following last year’s very mild autumn, this year the group had planned to make the transitional autumn ranges less heavily dependent on cool weather by “de-seasonalising” their coat and knitwear ranges. By offering customers a range of products more geared to autumn in lighter weight fabrics the idea is to reduce their reliance at this time of year on heavier items – whether this is working in the current warm weather is open to debate. They have also introduced “wardrobe favourites” to bridge a gap between the running line ranges and seasonal ranges.

Ann Harvey is distinguished from the group’s main ranges by offering plus-sized designs in more contemporary styles. It was relaunched in August in fifty stores with lower price points than in the previous trial and aimed at existing Bonmarche customers rather than former customers of the Ann Harvey brand. Early feedback supports the view that there is demand for a more contemporary plus-sized offer and they will continue to evaluate this to decide how best to capture this market and utilise the Ann Harvey brand.

The view of how best to position menswear products has continued to evolve since the group trialled their first items in this range last year. The strongest demand has been for gifts rather than replacement purchases, and they will therefore focus the menswear offer on the months immediately before Christmas with an emphasis on popular gift items such as tops and accessories. They will therefore consider the opportunity in future to offer complementary gift items alongside the core offer.

The programme to replace older store fascias with new ones incorporating the new branding is progressing according to schedule and they are on track to complete 140 by the end of the year. This will leave about 60 stores to refresh during 2017. At the same time as replacing the fascias, certain elements of internal branding have also been updated with the cost of upgrades running at £9K per store and the 2016 capex impact at about £1.3M.

Following the trial last year of the personal shopping service, this has now been rolled out across all stores. Since its launch in April, they have seen good uptake from customers and a higher than average value per transaction where customers have used the service. It is estimated that this has contributed about 0.3% to like for like sales growth and the board see the opportunity for further growth from this service and are providing further training to staff to encourage this.

Trading conditions during November have been challenging due to very mild, wet weather. The expectation for the full years remain unchanged provided that trading conditions normalise for the rest of the year, which is quite a bit “if” in my opinion. Despite the fact that last year, the first half was stronger, this year the board expect the second half to be stronger this year as new stores begin to contribute and online growth returns, weather dependent of course.

At the current share price the shares are yielding 2.5%. The group has a net cash position of £18.6M at the end of the first half of the year compared to £10.2M at the end point of last year and £12.6M at the half year point of last year.

Overall then this has been a bit of a tricky half year for the group. Profits were down, although if we discount the main market listing costs, they were broadly flat. Net assets did increase and although operating cash flow increased, this was due to payment timings and cash profits fell. The group is still very cash generative though. Trading in stores had a poor Q1 followed by an improved Q2 as last year comparatives eased. Online trading was hit in Q2, however, due to a hit from google following the website upgrades that meant they were not appearing for relevant searches.

The Ann Harvey brand and menswear doesn’t appear to have gained much traction and they will only hit full year targets if weather conditions normalise. There is no guarantee of that and so I am not going to buy in here just yet.

On the 16th December the group announced that CEO Beth Butterwick will step down after four years in the role to join Karen Millen as CEO. She will remain at the group until her successor is appointed. In her time at Bonmarche, she led the business through a transformative period, through the acquisition by Sun Capital Partners, the IPO in 2013 and the transition to the main market. She will be quite a loss in my view.

To make matters worse, the group also released a profit warning. Trading conditions in December have been very challenging and have not normalised and the board believe that they are likely to continue for the remainder of the winter season. They have therefore revised their profit expectations for the current year with pre-tax profits expected to be within the range of £10.5M to £12M.

Given the warm weather and the fact that at the last update the group said they were relying on the weather to normalise in order to achieve expectations, this should come as no shock. The shares may actually be decent value but until the uncertainty over the CEO and whether the group can actually hit their revised targets, I am remaining out for now.

On the 15th January the group released a trading update covering the Christmas period and Q3. Sales for the quarter increased by 3.4% but like for like sales declined by 1.3% and the board’s expectations for the full year are in line with their revised guidance in the last update of pre-tax profits in the region of £10.5M and £12M. In the short period since Christmas, demand has trended towards normal levels so perhaps the worst is over for them?

On the 30th March the group announced the appointment of Helen Connolly as the new CEO and she will take up her position later in the year. She is currently Senior Buying Director for George at Asda having previously worked for Next and Dorothy Perkins in buying roles. This seems like a decent appointment.

On the 8th April the group released a trading update covering the year ended 2016. Total sales increased by 5.3% but like for like sales increased by just 1%. For the final quarter, total like for like sales grew by just 0.5%. The board expects that the pre-tax profit for the year will be at the lower end of guidance outlined in the last trading update but their financial position remains sound.

After Christmas, trading conditions continued to be quite challenging with the exception of January when the group saw a higher than average demand for autumn/winter sale stock. Although helpful in clearing these ranges, the continued colder weather has been unhelpful in kick-starting real demand for spring products. Overall consumer confidence does not appear buoyant and the board expect trading conditions to remain challenging and therefore their outlook for 2017 is cautious.

In addition, the group have appointed Mark McClennon as an independent non-executive director. He is currently Global VP for IT at Unilever so seems like a high calibre appointment. They have also announced the appointment of Sergei Spiridonov as a non-executive director and the nominee from the majority shareholder, BM Holdings. He replaces Michael Kalb.