Wynnstay has now released its interim results for the year ending 2015.

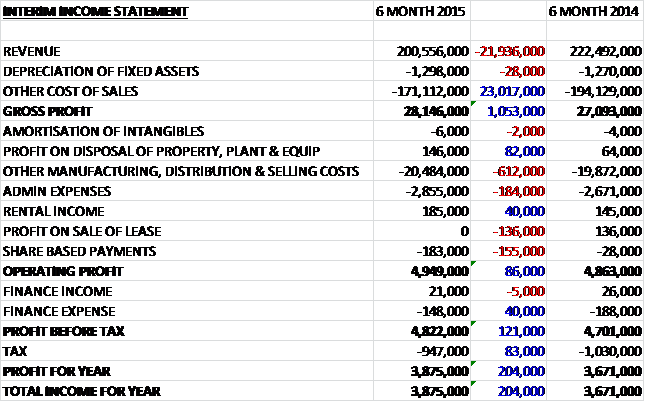

Revenues fell by £21.9M when compared to the first half of 2014, reflecting continued commodity price deflation in grain and traded raw materials, but cost of sales also fell to give a gross profit some £1.1M ahead. The manufacturing, distribution and selling costs increased, as did admin expenses, and we also see the group did not receive a £136K profit on the sale of leases that occurred last time. Due to lower debt levels, though, finance expenses did fall by £40K and tax was also some £83K lower to give a profit for the first six months of 2015 of £3.9M, an increase of £204K when compared to the first half of last year.

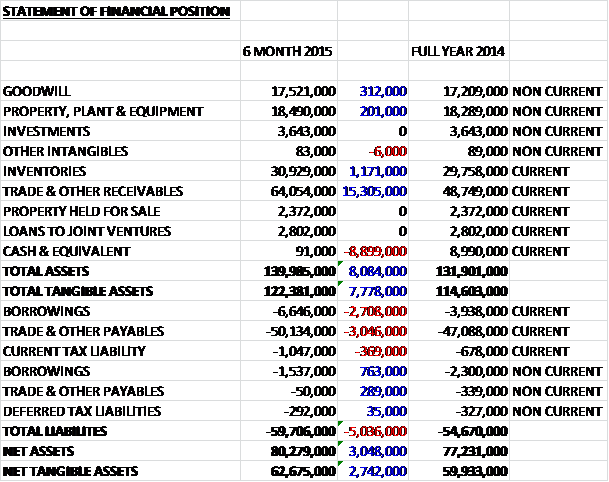

When compared to the end point of last year, total assets increased by £8.1M driven by a £15.3M increase in receivables and a £1.1M growth in inventories, partially offset by an £8.9M fall in cash levels. Liabilities also increased during the year due to a £2M growth in borrowings and a £3M increase in payables. The end result is a £2.7M increase in net tangible assets to £62.7M.

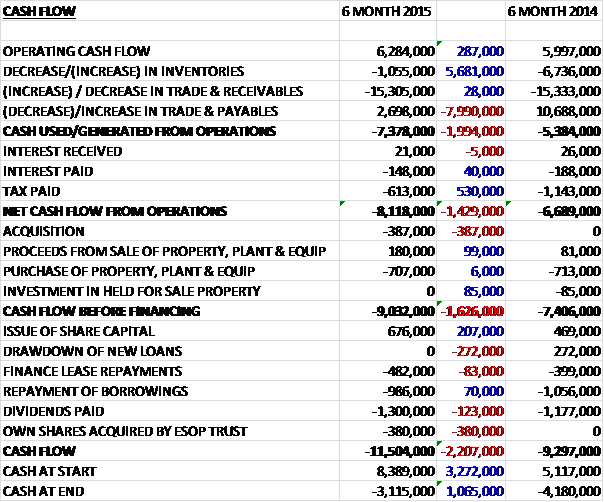

Before movements in working capital, cash profits increased by £287K to £6.3M. We then see a huge increase in receivables, which appears to be seasonal, and after tax and interest, there was a net cash outflow from operations of £8.1M, some £1.4M more than last year. The group spent £387K on an acquisition and a net £523K on property, plant and equipment to give a cash outflow of £9M before financing, which involved repaying finance leases, and loans along with £1.3M worth of dividends. In all, there was an £11.5M outflow of cash to leave an overdraft of £3.1M at the period end. This looks alarming but there should be a cash inflow from the second half of the year.

The output prices remained low for many farmers but the balance of trade is expected to reverse in the foreseeable future. The group have recently completed their planning exercise to map out the potential organic and acquisitive growth opportunities over the next five year and they are investing in production and marketing initiatives to support their development. There is no detail about the plan, which is a shame but perhaps it will be detailed in the annual report later in the year.

Profit in the Agriculture division was £2.2M, a decline of £127K year on year as the low grain price affected arable product margins, particularly in fertiliser and grain trading, partially offset by a good feed performance. The output prices for many products remain below the realistic cost of production for many farmers, mainly as a result of the current surplus in the global supply of grain and dairy products which has resulted in a reduction in demand for fertiliser. Volumes of compound and blended feeds increased by 9% year on year, though, gaining market share. The investment in the production and distribution facilities has improved efficiency within the feed products division enabling the group to maintain competitive prices for their customers.

Glasson delivered a solid performance despite a reduction in sales of fertiliser and raw materials for feed as compounders reverted to the use of home produced cereals following the good UK crop in 2014. The business benefited from increased sales of specialist products which have supported a good contribution to the group. In the arable products division, sales of cereal and herbage seeds have been buoyant and the business continues to increase its presence in the market but demand for fertiliser has been lower than the equivalent last year, as farmers geld back from buying in anticipation of a fall in prices. The fertiliser spot market has been encouraging, however, helped by the recent realignment of prices which will benefit sales over the summer period.

The large grain harvest in 2014 has contributed to an increase in traded volume but the continuing low grain price has resulted in pressure on margins. Grain stocks at farms remain higher than normal and with a good harvest predicted for 2015, volumes are expected to be high for the foreseeable future.

Profit in the Specialist Retail division was £2.9M, an increase of £266K when compared to the first half of last year and was aided by the further integration of the stores acquired in the CPF acquisition. The Wynnstay stores business now has 42 outlets which includes the seven stores acquired in 2013, as well as two new stores added in the last six months. Total sales over the period increased by 6%, with like for like sales rising by 2%. New initiatives to work alongside the group’s customers to bring improved efficiency to the industry are apparently progressing well with the introduction of specialist ventilation and lighting systems for dairy enterprises being an example of this. The group plans to continue to grow their network of stores to expand their geographical presence and extend their farmer customer base.

The pet product business performed well during the period with like for like sales up 2.8% but its profit contribution is below that of the same period of last year due to costs associated with business expansion. A new store was opened in June in Cambourne, Cambs and further new stores are planned to open over the next year. During the first half there was £126K of other losses compared to £73K during the same period of last year. All joint venture and associates have been performing in line with management expectation but their result is not included in the interim results, instead being added to the final results at the end of the year. The FertLink fertiliser joint venture is now directly handling fertiliser trade previously managed by the Glasson operation so this business will now be reported at the full year stage.

Going forward, trading conditions for farmers have been difficult over the past two years as a result of the downward pressure on farm gate prices and adverse weather conditions. The industry is cyclical, however, and the macro economic factors around the world food demand remain compelling. The board believes that the changing marketing environment will bring opportunities to the industry as customers strive for efficiency within production systems. The board are confident about the group’s continued future growth and overall trading is in line with management expectations.

After an 8.8% increase in the interim dividend, at the current share price the shares yield 1.9% which is what is expected for the full year consensus. The net debt at the period end stood at £8.1M compared to £10.9M at the same point of last year and reflects the peak of the group’s working capital cycle.

Overall then, this was a pretty decent if unexciting update. Profits increased modestly as did net assets to further strengthen that rock solid balance sheet. Underlying operating cash flows also improved year on year but due to movements in working capital, this was reversed at the actual operational cash flow stage. The business is very seasonal and the half year point seems to mark a bit of a low as per working capital cycles so the negative cash flow at the period end is probably no cause for concern. The agriculture business continued to struggle, mainly due to the world surplus in grain causing prices to fall which has a knock on effect on fertiliser sales but the retail business is picking up the slack with a steady like for like growth in both the country store network and pet stores.

All in all, I quite like this share for its dependability and will look to add on any weakness.

After rallying since May the shares have come off the boil somewhat so now might now be the right time to take my position. I will keep a close eye on this.

On the 19th October the group announced an acquisition and a trading update. They have agreed terms for the acquisition with TG Jeary for its West Country farm supplies operation, Agricentre. They will utilise their existing bank facilities to fund the acquisition, the terms of which are not yet being disclosed.

Agricentre operates a network of eight units supplying a wide range of agricultural inputs including animal healthcare, dairy hygiene and animal nutrition products as well as feed related equipment and other hardware. Its units are located in Bristol, Calne, Langport, Honiton, Salisbury, Shepton Mallet, Sturminster Newton and the Isle of Wight. It has historically generated sales of about £15M and the current financial year is expected to show a small operating loss. The acquisition extends the group’s trading presence into a major new geographic region and the stores will be integrated into the current network with a significantly enhanced product range and operational efficiencies. The full benefits of the acquisition are not expected to come through for about a year, however.

The group is also reporting satisfactory trading in the second half of the year to date with results expected to be in line with expectations. Looking ahead, the trading backdrop for farmers remains difficult and the group is taking a cautious view on the expected recovery in output prices over the next twelve months.