XP Power has now released their interim results for the year ending 2017.

Revenues increased when compared to the first half of the year due to a £12.9M growth in North American revenue, a £4.8M increase in European revenue and a £2.2M growth in Asian revenue. Cost of inventories increased by £17.6M but there was a £4.1M positive movement in changes in inventories and other cost of sales were down £1.7M to give a gross profit £8.1M ahead. R&D expenses grew by £1.7M and other operating costs increased by £4.4M which meant that the operating profit increased by £1.5M. Finance costs were flat but there was a small increase in tax charges so the profit for the period was £10.9M, a growth of £1.1M year on year.

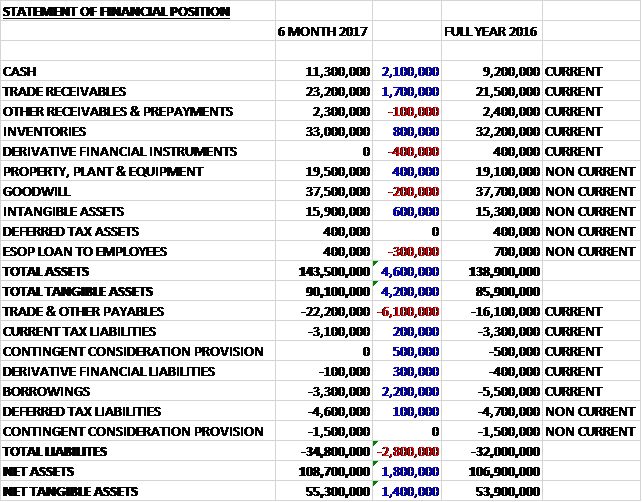

When compared to the end point of last year, total assets increased by £4.6M driven by a £2.1M growth in cash, a £1.7M increase in trade receivables and an £800K growth in inventories. Total liabilities also grew during the period as a £2.2M fall in borrowings was more than offset by a £6.1M increase in payables. The end result was a net tangible asset level of £55.3M, a growth of £1.4M over the past six months.

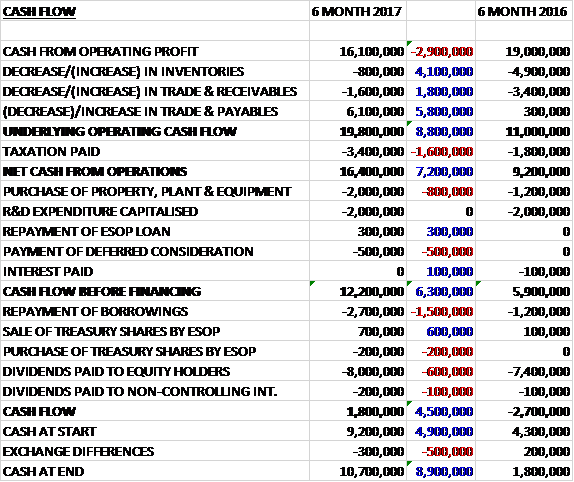

Before movements in working capital, cash profits declined by £2.9M to £16.1M. There was a cash inflow from working capital due to an increase in payables and after tax payments grew by £1.6M the net cash from operations was £16.4M, a growth of £7.2M year on year. The group spent £2M on fixed assets, £2M on R&D capitalised (the rest came out of the cash profit figure) and £500k on deferred consideration which meant that the free cash flow was £12.2M. Of this, £8.2M went on dividends and £2.7M was used to pay back loans which meant the cash flow was £1.8M and the cash level at the period-end was £10.7M.

Overall, pre-tax profit grew by £1.5M and this growth was entirely down to favourable forex movements. The operating profit in Europe was £7.7M, a growth of £1.7M year on year. The operating profit in North America was £14.5M, an increase of £4.1M when compared to the first half of last year. The operating profit in Asia was £1.1M which was flat year on year.

The order intake was up 52% (35% at constant currency). Asia increased by 38% and North America increased by 58%. Overall momentum has continued to build in the business and they enter the second half of the year with an order book of £70.9M (£59.1M). Approximately half of the 35% order intake growth came from existing programmes with half from programmes that have entered production over the past year or so.

The healthcare, industrial and technology sectors all delivered increased revenue in all three regions, suggesting a general market recovery in the capital equipment markets they serve. On a sector basis, revenues from healthcare grew by 36%, industrial revenues increased by 19% and technology revenues were up 58% driven by the semiconductor manufacturing equipment makers who are exhibiting strong and sustained growth.

The gross margin declined from 49% to 46.9%. Proportionally more cost of sales are denominated in US dollars than revenues so the weakness in sterling increased costs which is estimated to have reduced margins by 110 basis points. In addition, some costs which were operating costs last year were considered to be cost of sales this year due to the continuous integration of EMCO. Operating costs increased by £3.9M. Of this, £2.8M was advisory and aborted acquisition costs. In addition, the sterling weakness increased these costs by around £2M and there were extra costs associated with the growth of the business.

The group launched 14 new product families in the first half of the year compared to 27 last time. The relatively high number of new product introductions in 2016 was aided by the introduction of a new labelled product supplier to increase their offering of DC-DC converters. Of the 14 new products introduced, 12 were of high efficiency design. Revenue from own design products was up 39% and now represents 75% of the total, up from 72% last time.

The group now have 259 part numbers approved for production in Vietnam with more in the pipeline. Of the 693,000 power converters manufactured, 60% were made in the country compared to 25% last year. The board expect the proportion of power converters produced in Vietnam to increase further as they transfer more products to that facility. The Chinese factory will focus on the higher power, higher complexity products.

They intend to break ground and start construction of a second factory on their existing site in Vietnam in the second half of the year, with production scheduled to come on stream in 2019. The board estimate that their existing Asian manufacturing facilities have capacity to produce about $170M of end revenue on their own manufactured products with the second facility in Vietnam adding an additional capability or around $130M in revenue. It is estimated that the cost of the second building in Vietnam and the initial equipment set to be approximately $6.5M, of which $1.9M will be incurred in H2 with the remainder in 2018.

Reported order intake and revenues for the first half hit record levels, assisted by the weakness of Sterling, a recovery in the capital equipment markets and new design wins entering their production phase. While the board remain conscious of potential macroeconomic challenges, their strong order book, combined with designs won in 2016 and prior years entering production means that the board now expects the group’s performance for the full year will be comfortably ahead of existing expectations.

At the end of the period the group had net cash of £8M compared to £3.7M at the end of last year. At the current share price the shares are trading on a PE ratio of 24.2 which falls to 20.1 on the full year consensus forecast. After another increase in the quarterly dividend the shares are yielding 2.7% which grows to 2.8% on the full year forecast.

Overall then this has been another strong period for the group. Profits were up, but this was due to forex movements and otherwise they would have been flat. If we exclude the abortive acquisition costs, however, there was strong growth in profits. Net assets improved but although the operating cash flow increased, this was due to working capital movements and cash profits actually declined. There was a good amount of free cash generated.

The order intake has been very strong across all markets, which is good to see, and it seems some of the new projects are starting to make their way through to production. The shares are not cheap with a forward PE of 20.1 and yield of 2.8% but we are paying for quality here. Despite the fact that results have been inflated by favourable forex, I like this company a lot and continue to hold.

On the 2nd October the group announced that it had acquired Comdel, a designer and manufacturer of radio frequency power supplies for a total consideration of £17M paid in cash, funded by a new revolving credit facility of $40M with a $20M additional accordion option which was put in place to assist the acquisition strategy.

Comdel is based in Massachusetts and supplies the industrial and technology sectors with a range of standard, modified and custom high power RF power conversion products. They typically supply them into the semiconductor, thin film, photovoltaics and induction heating industries. Last year it recorded a pre-tax profit of £1.4M and the acquisition is expected to be earnings enhancing in 2018.

The businesses share several customers and the power supply solutions they offer are considered complementary. Comdel’s products and engineering capabilities will enhance the group’s ability to implement its strategy of winning a greater share of business from its largest customers and will also bring a number of new customers to the group. The CEO of Comdel will remain with the business to head up the newly formed RF Power divison.

This acquisition seems rather expensive to me but I guess time will tell…

On the 9th October the group released a trading update for Q3. Trading has been robust. Revenues for the nine months increased by 34% to £123.9M with a constant currency increase of 21%. Order intake was strong at £137.5M, a 44% increase (constant currency increase of 30%). The Q3 order intake was £44.1M compared to £34.2M in the prior year with continued growth in North America with semiconductor manufacturers enjoying an upturn in chip demand, and healthcare companies placing orders for new programmes. Net debt was £10.8M at the period-end following the draw down to finance the Comdel acquisition.

The board now expects the group performance for the full year will be ahead of previous expectations. Furthermore the acquisition of Comdel before the period-end will enable the group to provide their existing customers with a comprehensive product offering in Radio Frequency power supplies, increasing their addressable market and further expanding their revenue base. They are still looking for other acquisition opportunities.

On the 12th January the group released a trading update covering Q4. They had a good end to the year, in line with board expectations as the strong order intake reported in Q3 drove robust revenue growth in Q4. The momentum in order intake continued into the fourth quarter and both order intake and revenue growth has been strong across all regions. Order intake for the quarter was £46.8M, 24% ahead of the same quarter last year and revenue was £43.2M, 16% ahead.

The trading performance of Comdel was in line with expectations with orders in Q4 of £5.8M and revenues of £4.1M. Integration of the business is proceeding as planned and following the acquisition for $23M, net debt was £10.1M compared to a net cash position of £3.6M at the same point of last year.

Going forward the board are encouraged by continued strong order intake experienced across the business during H2 and they enter 2018 with positive momentum and therefore expect to grow orders and revenues in 2018 above that in 2017. This looks fine, I continue to hold.

On the 12th February the group released a tax update. The recently enacted Tax Cuts act in the US is expected to result in a non-cash tax credit in 2017 relating to the revaluation of deferred tax assets, of around £5.2M. The group have also received notice that claims relating to the DEI in Singapore have been accepted resulting in a £1.3M refund of tax paid in 2015 and 2016.