Zytronic is a manufacturer of touch sensor products for public access and industrial applications. The products incorporate an embedded array of metallic micro-sensing electrodes which offer durability, environmental stability and optical enhancement benefits to designers of system integrated interactive displays. It develops and manufactures customised optical filters to enhance electronic display performance and is traded on the London AIM exchange. It has now released its final results for the year ending 2014.

Overall revenues increased by £1.6M when compared to 2013 as increases in most territories, with particularly good growth seen in Americas, was counteracted by a fall in UK sales. Cost of sales were broadly flat but the group benefited this year from the lack of £413K of royal write-offs that happened in 2013 due to a reduction in forecast sales meaning that a prepayment held on account would not be recoverable. The gross profit, therefore, increased by £2M to £6.9M. Admin expenses increased with an unfavourable movement in foreign currency exchanges, the lack of capital grant amortisation and other costs taking their toll so that operating profit was £1.3M higher than last year. Interest broadly cancelled itself out and taxes increases slightly, with the rise in taxable profits being offset by enhanced tax reliefs so that the profit for the year was £1.3M higher at £3M.

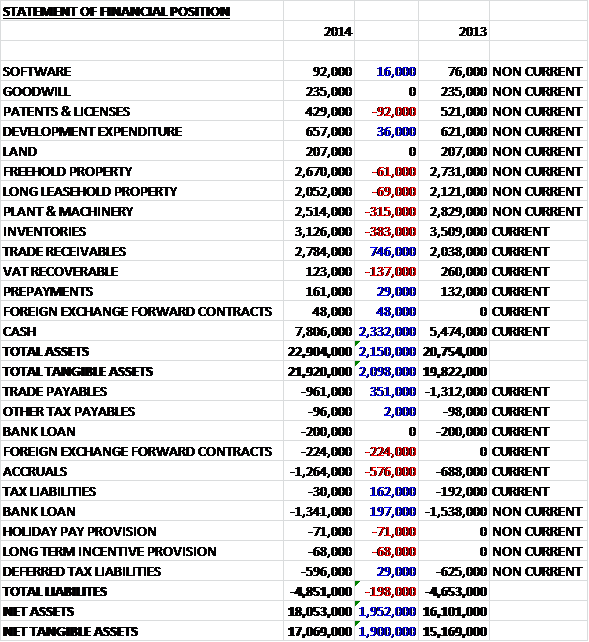

When compared to the end point of last year, total assets increased by £2.2M to £22.9M, driven by a £2.3M increase in cash and a £746K growth in trade receivables, somewhat offset by a £383K decline in inventories and a £315K fall in the value of plant and machinery. Liabilities also increased slightly as a £576K increase in accruals and a new £224K worth of foreign exchange forward contracts were counteracted by a £351K fall in trade receivables and a £197K reduction in the mortgage outstanding. The end result is a £1.9M increase in net tangible assets to £17.1M. I have included patents and licenses in this calculation despite them being intangible as it seems to me that they have some value. In any case, this balance sheet looks strong and is improving year on year whilst the group also has negligible operating leases off the balance sheet.

Before movements in working capital, the cash profit increased by £1.6M to £4.6M with an increase in receivables being broadly counteracted by other working capital movements giving a £4.7M cash inflow from operations, an £800K increase when compared to last year which then widened to £917K due to a fall in the tax paid. The only capital expenditure of note was a £322K paid for intangible assets (probably development expenditure) and £263K paid for property plant and equipment relating to two additional large format plotters which should treble manufacturing capacity. This gave a free cash flow of £3.7M, an increase of £1M on 2013. The bulk of this cash went on dividends with a further £200K relating to the regular mortgage payments to leave the group with a positive cash flow of £2.3M, an improvement of £1.1M when compared to 2013 and an impressive result.

Overall the significant improvement in trading over the last year continued the trend of second half performance being better than in the first half of the year. Touch product revenues increased by 18% and remain by far the most important part of the business with 79% of total sales. Non-touch product revenues showed an expected decline, falling by £700K driven by a decline in ATM display filter glass. The group is heavily export focused with 94% of total sales being export derived.

Financial applications continued to be the largest market with sales increasing by £200K to £5.7M and included applications such as ATMs, bill payment kiosks and financial point of information kiosks. This market is the strongest touch market area due to the durability and reliability of the group’s products designed for high volume unattended use and locations. The volume increase was driven by a 15,000 unit increase of ATM sensors sold to 46,000 as some new customer projects moved into production and existing customer demand increased after last year’s redesigns. The downside of this was the fact that the redesigns and the different customer mix meant that the average selling price of the units fell by 24%. Non-ATM kiosks have historically been a buoyant market in CIS countries but the ongoing conflict in Ukraine meant sales collapsed by 10,500 units to just 3,300 units.

Vending machines are the second largest application with sales growing 20% to £3M and volume growing 26% to 32,100 units. The volume of sensors sold to Coca Cola for the Freestyle drinks dispenser was in line with expectations and similar to last year at 4,700 units. Unit sales into the fuel vend application area were also similar to last year with a slightly different customer mix whilst growth came mainly from sales into the service vend application area in Eastern Europe.

Other significant growth came through the industrial, gaming and signage markets with sales into the industrial market for human machine interface control devices and general application kiosks growing by 54% to £2M and 61% to 26,000 units. The gaming and signage markets benefited from the manufacture of large sized sensors coupled with the mutual projected capacitive technology multi-touch solution which continues to gain greater market acceptance. Gaming revenues increased by £1.1M to £1.9M with all of the sales attributable to casino upright cabinet slot machine designs. Sensors smaller than 15 inches showed overall unit growth but the Bosch branded cooktop unit and the in-vehicle agricultural telematics system both reduced due to customer forecasted levels.

The group has quite a lot of concentrated risk on three major customers who account for 22%, 11% and 10% of total sales each. The group seems to hedge much of its exchange rate risk but a 5% movement in Sterling against both the Euro and the USD would affect profits by about £13K. Equally there is not much in the way of interest rate risk, with a 100% increase in rates reducing profit by £18K. Operationally the main risks are that someone else releases new, better touch sensor technologies but the group is also susceptible to client’s project timing and the cost of raw materials, particularly energy and oil which have both been declining in recent months.

The group’s borrowings consist of a 10 year mortgage with Barclays. The funds are repayable in quarterly instalments of £50K with interest payable at 2.35% above LIBOR and will be either refinanced or paid off by 2017. Next year it is expected that a project to refurbish the clean room will cost £400K in capital expenditure. The R&D division has released a new ZXY300 series controller which provides customers with multi-touch performance characteristics at similar levels to the 22 to 50 inch range using the ZXY200 series controller. Progress was also made on the commercialisation of the large format curved touch solutions which were showcased in a trade show in Las Vegas.

Geographic expansion is one target for the near term future. The group have established Zytronic Inc in Atlanta in order to focus on OEM and channel partner sales support in the US. They have also signed up for a new initiative in mainland China organised by the former UKTI and referred to as FastTrack China in order to aid engagement in this market. Along these lines, it is also intended to strengthen presence in the APAC region by establishing a sales office in Taiwan.

One interesting new application has been developed with Eurocomposant which is a sensor for a series of multi-touch table products for use in home, restaurant and hospitality settings where users can play games, order food, surf the web and connect with friends via social media. The sensors are supplied to HUMElab in 22, 32 and 42 inch formats. Another interesting application is a mirrored point of sale system in opticians Kite GB. The unit uses a PCT touch sensor with a 42inch active area sourced from Zytronic which has been applied to mirror-finished toughened glass and is capable of supporting up to 40 point multi-touch operations. Customers are able to take photos of themselves wearing different frames, post them to social medial sights and enable their friends to comment on the chosen frames.

Two months into the new year, both sales and the order book are ahead of last year which should be a decent platform for further growth. At the end of the year the group has 69 active projects. Digital signage remains the strongest application area in terms of project volume. Strengthening is also observed in the financial, gaming and industrial sectors where the number of active projects at the period end is almost double compared to the period start date.

At the current share price the P/E ratio stands at a rather average 15.5, falling to 14.6 on next year’s consensus forecast. After a 10% increase in dividends this year, the shares yield 3.3% at the current share price, covered nearly 2 times by profits. The yield is forecast to increase to 3.6% on next year’s predicted dividend. The net cash position at the end of the year increased by £2.3M to £7.8M.

Overall this was a strong update. Profits were up, the strong balance sheet improved further and the group continues to throw off cash. There is not much in the way of debt and group is in a net cash position. So far this year, it sounds as though trading is going well and this is certainly a market where there seems to be increasing demand. The ongoing issues in the Ukraine seem to have some effect on the group and the declines in the Bosch project could be potential cause for concern but I believe with the fairly attractive yield these shares may be worth a purchase.

The chart looks pretty good, there seems to have been a decent up trend since the low of August last year so I might look to enter on a retrace.

On the 26th February the group released a trading update covering the first four months of the year which was ahead of the same period last year in line with expectations. Short but sweet – sounds decent enough to me, I have made a purchase.