Zytronic has now released their interim results for the year ending 2018.

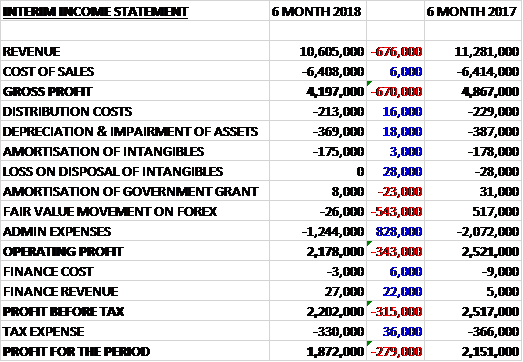

Revenues declined by £676K when compared to the first half of last year and with costs of sales remaining broadly the same, gross profit fell by £670K. There was a modest decrease in distribution costs and depreciation along with no loss on intangible disposals which was £28K last time. We then see a £543K detrimental movement in the fair value of forex hedges offset by an £828K decline in admin expenses to give an operating profit £343K lower. There was a £22K increase in financial revenue and a £36K decrease in tax charges which meant that the profit for the period was £1.9M, a decline of £279K year on year.

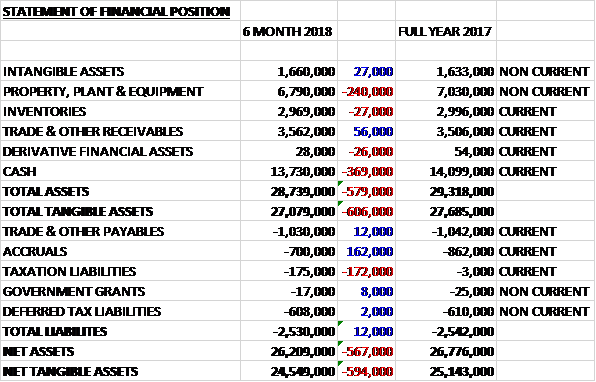

When compared to the end point of last year, total assets declined by £579K driven by a £369K decrease in cash and a £240K reduction in the value of property, plant and equipment. Total liabilities also saw a modest decline as a £172K growth in tax liabilities was offset by a £162K decrease in accruals and some other small reductions. The end result was a net tangible asset level of £24.5M, a decline of £594K year on year.

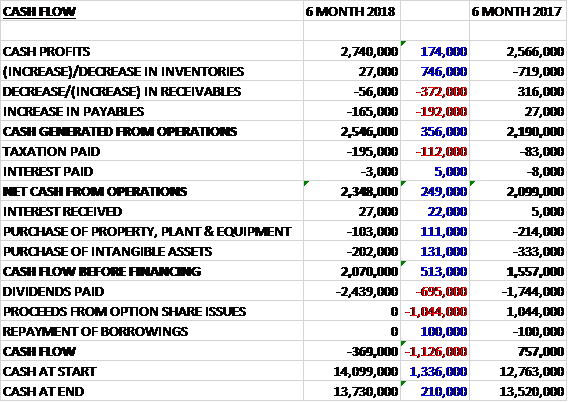

Before movements in working capital, cash profits increased by £174K to £2.7M. There was a cash outflow from working capital and a £112K increase in tax payments to give a net cash from operations of £2.3M, a growth of £249K year on year. The group spent £103K on tangible assets and £202K on intangibles to give a free cash flow of £2.1M. Of this, £2.4M was paid out in dividends which meant there was a cash outflow of £369K and a cash level of £13.7M at the period-end.

There has been a considerable variation in demand across the various sectors, resulting in a reduction in revenues. The most positive has been gaming which has increased by 17% with increases in large, ultra-large and curved solutions, whereas the financial sector, where they supply product for ATM manufacturers, demand has been unpredictable with projects being deferred and sales lower than last year.

In addition, margin has been impacted by forex movements and the reduction in financial customer demand. The vending market has been affected by the move to obsolescence of the existing freestyle drinks cabinet’ there was growth in industrial mainly due to sales through EMEA across a balance of products; signage was down slightly and others decreased with Bosch Siemens cooktops moving to end of life.

Going forward, the second half of the year has started with some improvement in demand from the ATM market and an increased number of projects in the gaming sectors, although growth is suppressed when compared to recent years.

At the current share price the shares are trading on a PE ratio of 16.5 which increases to 17.3 on the full year consensus forecast. After the interim dividend was doubled the shares are yielding 4.8% which is forecast to remain the same for the full year. At the period-end the group had a net cash position of £13.7M compared to £14.1M at the end of last year.

Overall then this has been a bit of a tough period for the group. Profits and net assets both declined, although the operating cash flow improved with some free cash being generated. The gaming market seems to be performing well but there also seem to be a number of projects coming to an end in the other markets with no indication of them being replaced. Indeed I have to wonder whether the ATM market is in structural decline. Given the amount of net cash here the shares aren’t terrible value with a forward PE of 17.3 and yield of 4.8% but I’d like to see some more clarity about better performing markets before buying back in here.

On the 18th October the group released a trading update covering 2018. Trading in the second half of the year showed a 10% improvement in revenues over the first half, totalling £11.7M, which resulted in total revenues for the year of £22.3M which is in line with market expectations.

The increase in business required the introduction of some new designs and production techniques which have resulted in lower than expected margins, particularly in the final two months of the year. In addition, a spurious patent claim was settled for £72K plus the group’s own cost of £240K. Lower margins coupled with litigation costs have resulted in full year profits before tax of £4.2M, being behind market expectations. I am staying out for now.