Portmeirion has now released its final results for the year ended 2015.

Revenues increased when compared to last year as a £2.7M decline in South Korean revenue was more than offset by a £2.2M growth in US revenue, aided by the strength of the US dollar, a £2M increase in UK revenue and a £5.8M growth in ROW revenue. Depreciation and amortisation fell by £142K but other operating expenses were up £6.4M as staff costs increased, to give an operating profit £8M above that of 2014. A small increase in the pension scheme interest was offset by a decline in loan interest and a £52K growth in the share of profit from associates and after a £214K increase in tax payments, the profit for the year came in at £6.9M, a growth of £824K.

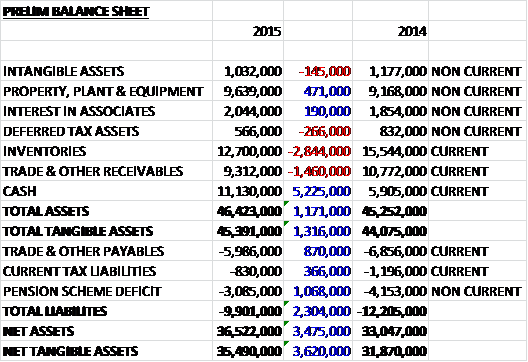

When compared to the end point of last year, total assets increased by £1.2M, driven by a £5.2M increase in cash and a £471K growth in property, plant and equipment, partially offset by a £2.8M decline in inventories and a £1.5M fall in receivables. Total liabilities fell during the year due to a £1.1M decline in the pension deficit, an £870K decrease in payables and a £366K fall in current tax liabilities. The end result is a net tangible asset level of £35.5M, a growth of £35.5M year on year.

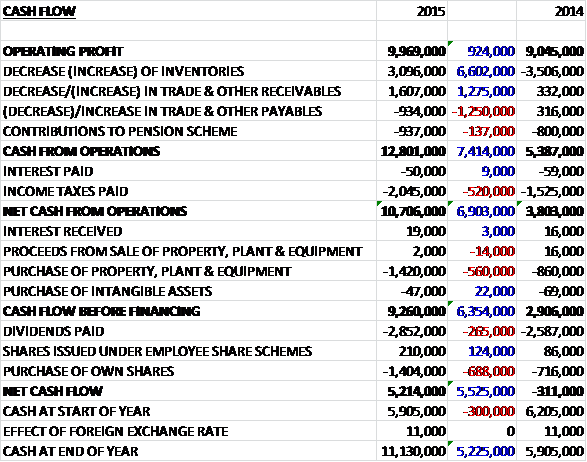

Before movements in working capital, cash profits increased by £924K to £10M. There was a cash inflow through working capital, with a decrease in inventories compared to an increase last year and after taxes increased by £520K, the net cash from operations was £10.7M, a growth of £6.9M year on year. The group spent £1.4M on property, plant and equipment and £47K on intangibles to give a stonking free cash flow of £9.3M, of which £2.9M was spent on dividends and £1.4M on share purchases to give a cash flow for the year of £5.2M and a cash level of £11.1M at the year-end. As seen above, there was a large working capital swing during the year and the year-end cash balances were broadly at the peak level that was achieved. It is therefore assumed that there will be a cash swing approaching £9M for 2016 which means the end of year cash balance is not all that excessive.

Although revenues were up by 11% in the US, much of this was due to the strength of the dollar and in constant currency terms, sales in the US increased by 3.1%. Continuing improvements in economic conditions in the country give cause for optimism but there is some uncertainty around the upcoming presidential elections. Sales increased by 12.5% in the UK. The EU referendum carries uncertainties for both the UK and the wider EU market but sales to the EU, other than the UK only account for 3% of revenues so the board feel the short term impact of Brexit would be slight in terms of global sales, although they do see the EU as a market of potential.

Sales to South Korea fell back by 18% year on year. The local economy has been weak which has translated into a greater effect on the sales of luxury goods. The board believe that this is a temporary slowdown, however, and the market is beginning to stabilise. Sales growth to the rest of the world was strong, at over 56% with an excellent performance in India which more than doubled to consolidate its place as the fourth largest market at over 8% of total sales. Thailand and Taiwan were also areas of high growth for the group.

Online sales, principally to the UK and the US, were £2.5M which represented a 26.6% increase over 2014. This route to market continues to provide growth opportunities. Profit growth was ahead of revenue growth as the group have a manufacturing facility with a fixed cost base. They continue to suffer from the imposition of anti-dumping duty, however, which has been applied to some of the European sales and costed the business over £2M cumulatively.

The Botanic Garden product saw sales of over £33M during the year and the design remains at the heart of the group’s future prosperity. Spode Christmas Tree is the second largest pattern, its main market is North America where it achieves sales of more than $10M per annum. The group also have other Christmas patterns such as The Holly and The Ivy. Annual sales of Blue Italian exceed £1.5M and Ted Baker Portmeirion tableware patterns, a range of licensed designs produced in collaboration with the fashion designer, were launched in 2015 with sales above budget.

The Stoke factory produced volumes at a similar level to 2014 and maintained quality standards at the same time as coping with the building of a new tunnel kiln and major movements of equipment to accommodate it. The installation of the kiln was not without its challenges but it is now fully commissioned and the group have just started to increase production by some 20,000 pieces per week. Other bottlenecks will occur as this is increased further, particularly in decoration, but the board believe that can add another 80,000 pieces a week on top of this 20,000 pieces, subject to customer demand of course. They have purchased a hollowware decal application machine and will be increasing the use of heat transfer decals in order to drive further production efficiencies.

The pension scheme deficit on the defined benefit scheme which was closed 17 years ago reduced to £3.1M from £4.2M last year, mainly due to the cash payment made and the discount rates used to evaluate the liabilities. £900K of cash contributions were made into the scheme over the year.

Trading in the first two months of the current year is ahead of the same period of 2015 and the outlook for 2016 is positive but as the results are becoming increasingly second half weighted, sales in these months are low in comparison to the rest of the year.

At the current share price the shares are trading on a PE ratio of 17.1 which reduces to 16.4 on next year’s consensus forecast. After a 13% increase in the total dividend, the shares are yielding 2.7% which increases to 2.8% on next year’s forecast.

Overall then this was a very strong year for the group. Profits were up, net assets increased and the operating cash flow grew, producing copious amounts of free cash. Although a lot of this cash performance was due to a fall in inventories that will likely reverse in 2016, cash profits were also up year on year. There was a decent performance in the US, helped by the strong dollar and a very good performance in the UK. India saw sales double and the country is becoming more important to the group with Thailand and Taiwan also showing growth, albeit from a smaller base. The main decline was seen in South Korea which has suffered from economic problems over the past year.

The new kiln is fully commissioned and production capacity has increased and so far in 2016, the performance has been above that of last year – although it should be noted that the second half is far more important for sales. With a forward PE of 16.4 and dividend yield of 2.8% the shares are not cheap but they are good value for such a solid, prudently run business and I am very happy to continue holding at these levels.

On the 5th May the group announced the acquisition of Lighthouse Holdings and its subsidiary, Wax Lyrical, for a total cash consideration of £17.5M. Wax Lyrical is the UK’s largest manufacturer of home fragrances, primarily scented candles and reed diffusers. Their brands of Wax Lyrical and Colony are sold in high quality stores together with ranges produced for other brands. They export to over forty countries around the world.

The consideration has been funded from cash reserves and debt draw down on new banking facilities comprising a £10M loan facility, a £10M revolving credit facility and a £2M overdraft from Lloyds.

The business made a pre-tax profit of £2.1M and had net assets of £7.6M at the end of last year. The acquisition is expected to be earnings enhancing in the current year and the group expects to grow Wax Lyrical’s sales the group’s existing customers, websites and retail outlets as well as into export markets such as the US and South Korea.

Joanne Barber, the current MD of the acquired business will continue to run it from its existing facilities in the Lake District.

Overall, I like this acquisition. With goodwill generated of about £10M and pre-tax profits of the business of £2.1M, the price seems right and the products seem a nice fit with those the group already sells.

On the 19th May the group released a trading statement. The US and the UK have both performed better than during the same period last year but sales to South Korea have not recovered as expected. As a result, total sales for the first four months of the year were 2% below the corresponding period last year. The group have also experienced an unexpected decrease in demand from some of their other Asian markets, although the board do not think this is a permanent trend. They are taking action in response to the decrease in demand and are confident that this, along with the recent acquisition, will provide overall growth for the group this year and therefore they expect profits to be in line with market expectations.

This is disappointing news, South Korea was probably expected but last time, India was flagged as doing especially well so this is most unwelcome. I have decided to take profits here.

On the 15th June the group announced that Finance Director Brett Phillips sold 25,000 shares at a value of £254K which leaves him with 61,745 shares. This is not a great sign justifies my decision to sell up here in my view.

On the 7th July the group released a profits warning. Total revenue for 2016 is expected to be ahead of last year due to the Wax Lyrical acquisition but pre-tax profits are expected to be materially below the £8.6M reported in 2015. In particular, sales to South Korea still show no signs of recovery and the performance of the distributor in India has continued to be extremely disappointing. In addition they have seen negative effects on demand in the UK before and following the leave vote at the EU referendum. The potential benefits of a weaker pound have yet to translate into firm overseas orders but the US has continued to perform well.

The board believe that this is a short term setback so they still intend to increase the interim dividend by 14%. This is a real shave as it is a quality company but the issues expressed here are enough to stop be buying back in.