Red24 is a crisis assistance company that provides a range of security and business support services, offering preventative and reactive advice to avoid or manage security and business risk. The security assistance segment provides preventative and reactive security advice whilst the business support segment comprises the provision of advice on product safety, particularly within the food industry. The products are distributed through financial services companies and they are listed on the AIM exchange. Red24 has now released its final results for the year ending 2014.

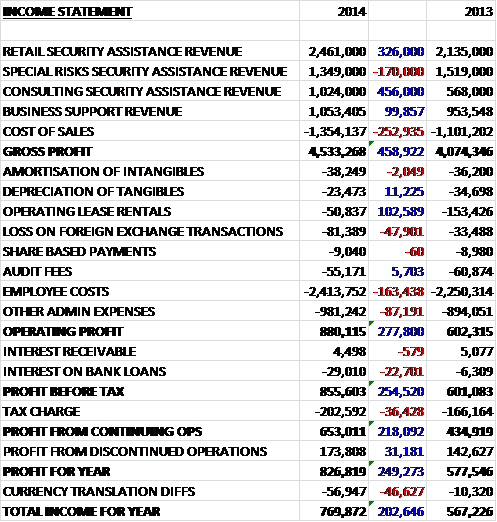

Revenues increased across most sectors with Consulting up £456K and Retail Security up £326K, slightly offset by a £170K fall in special risk security. Cost of sales were also up to give a gross profit some £459K higher than last year. Employee Costs and other admin expenses were higher during the year but operating lease rentals fell by just over £100K to give an operating profit £278K higher. An increase in interest payable and tax, due in part to an increasing proportion of earnings being made in high tax South Africa, gave a profit from continuing operations of £653K, a growth of £218K when compared to 2013 and with the profit from the discontinued operation added to the total, this came to £174K for the year, some £249K higher than in 2013.

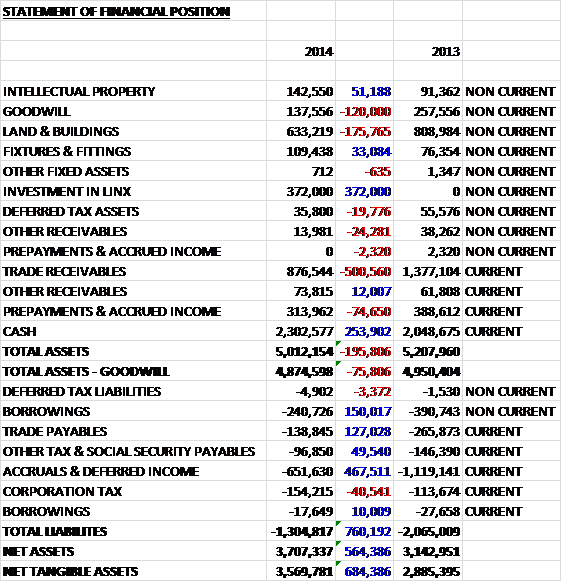

When compared to the end of last year, total assets fell by nearly £200K. This decline was driven by a £500K collapse in trade receivables, a £176K fall in the value of land & buildings due to foreign currency adjustments and a £120K decline in goodwill due to the disposal, somewhat mitigated by the £372K new investment in Linx and a £254K increase in cash levels. Liabilities also fell during the year due to a £468K reduction in accruals & deferred income (services invoiced in advance), a £160K decline in borrowings and a £127K fall in trade payables to give a net asset value, discounting goodwill, of £3.6M, an increase of £684K on 2013. It is worth noting, however, that there were £3.4M worth of office equipment operating leases not on the balance sheet, along with £70K of land and building leases.

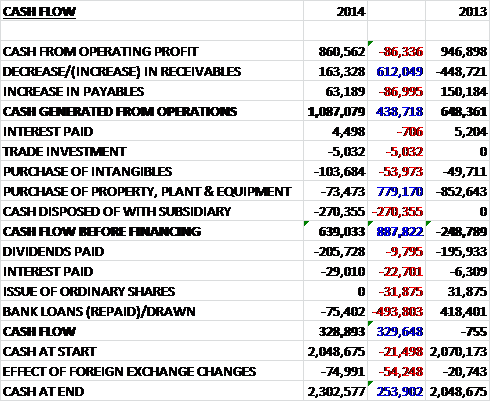

Before movements in working capital, cash profits fell by £86K to £861K before a large decrease in receivables, as the average credit period fell from 80 days last year to 55 days in 2014, pushed the cash generated from operations up to £1.1M, an increase of £439K. The group spent £104K on intangibles, £73K on tangible assets and lost £270K of cash with the disposal but before financing, the cash flow was still a decent £640K, an increase of £888K compared to 2013. The group repaid £75K worth of loans, forked out £29K on interest and was still able to pay £206K in dividends to give a positive cash flow of £329K against a neutral position last year. This is pretty decent, although it must be pointed out that the group had a favourable flow of working capital and spent much less on capex. It should also be noted that £433K of that cash is held with banks in South Africa and subject to South African exchange control legislation.

In July the group sold its share in Arc Training International for a 25% stake in Linx International and it is therefore been treated as a discontinued activity in the above accounts. Linx international is the company that purchased Arc Training and they provide security consulting services. The board felt that this would prove more beneficial to shareholders in the long term. Arc Training was a profitable business, generating just under £60K last year and £159K the year before so it is a bit of a shame they couldn’t keep hold of it as it was a fairly hefty chunk of overall profits. It has become apparent that Red24 and Linx have some cultural differences and the exchange of directors has not yield as many benefits as initially thought and has been terminated. As such it has been decided that Linx and their principle shareholder, David Gill should acquire the group’s stake in Linx which will be put to vote at the next AGM. So, basically, Linx has just purchased a profitable part of the Red24 business and Red24 are left without a stake in the enlarged company.

The Security Assistance business gave a result of £1.4M, a £237K increase on last year. The retail unit saw revenues grow by 15% as it benefited from additional sales staff. The products in this division are provided to banks and insurance companies to supply to their customers and the major clients are HSBC and AIG, although Liberty Mutual has been gained as a new client. The Consulting business, which provides customers with support in terms of reports, planning and training and a range of response services saw turnover nearly double during the year. The service is used by corporate HR departments and the board are investing in this sector in the coming year. The Special Risk unit provides support to customers facing crises and acts for a number of insurance companies. Despite a busy year with a major incident in Syria, turnover fell in 2014 as some clients renew at lower income levels as their own revenues have not reached their expectations. The board see opportunities for the business in Germany and are investigating the opening of an office in Munich.

The Business Support business includes the product safety advice service, the environmental advisory service and the cybercrime product. It had a result of £184K, a decline of £17K when compared to 2013. At the product contamination service, revenues grew by more than 10% as more insured businesses in the US became aware of the benefits available to them through their insurer. The group are intending to develop a number of new training services during the next year or so. The environmental services business doesn’t generate revenues as such but is instead part of the other offerings supplied by the group. The group are developing a cybercrime business to supply the UK market. In the US about half of businesses insure against cybercrime but this figure is only 5% in the UK so there appears to be a clear market as awareness of the issue grows.

Within the Security Assistance business, two distributors accounted for more than 10% of group revenue with one accounting for 23.4% and the 10.4%. Clearly the group is very dependent on these distributors which is a bit of a concern and a key risk going forward. The group also seems to be rather exposed to currency fluctuations. A 10% appreciation of the Rand against Sterling would see the cost of operations in South Africa increase by £158K, somewhat mitigated by a £78K increase in their Rand assets. Likewise, a 10% depreciation of the US dollar against Sterling would reduce profit by £100K which are large swings for a company of this size.

Going forward management see significant opportunities in Europe that can be serviced from the prospective office in Munich which are likely to become apparent during the second half of next year but the first half of the year is unlikely to receive the benefit of the major assignment in the Middle East that boosted the first half of this year. Currency issues remain a problem as about half of revenue is received in US dollars but about half of all costs are incurred in South African Rand. The group are therefore looking to incur more dollar costs and have taken steps to purchase forward 60% of the forecast Rand requirements for next year.

At the current share price the shares are trading on a P/E ratio of 9.9 which seems rather cheap. The dividend yield currently stands at a decent 3.5% after a 15% increase was announced for the final dividend, rising to 3.8% on next year’s estimate. Net cash at the end point of the year stood at £2.04M, up from the £1.63M recorded at the end point of 2013 and the only debt is a South African bank loan used to fund the purchase of an office building in Cape Town.

We can see then, that profits have made some progress and the net asset situation is improving due to the lower accrual liabilities but the net asset level is pretty much zero once the operating lease liabilities are taken into account. The cash from operations improved but this was due to good control of working capital rather than any operational improvements but there is a decent free cash flow as the capital expenditure fell this year and the dividend is covered well by cash. Despite this cash cushion, there are a number of risks here. The group is susceptible to currency fluctuations but the main risk seems to be the small number of large customers that the group relies on. Should one of these leave, there could be issues. Operationally, there seems to be good prospects for growth both through the new German office and the cybercrime business in the UK but at this time the risks are just a bit too high at the moment and I am a bit uneasy about the confusion surrounding the Linx deal. Definitely one to watch, though.