Pure Wafer reclaims and reprocesses silicon test wafers in the UK and the US. The group is also involved in the design, manufacture and installation of photovoltaic systems in the UK and they are listed on the AIM exchange. They have now released full year results for year ending 2014.

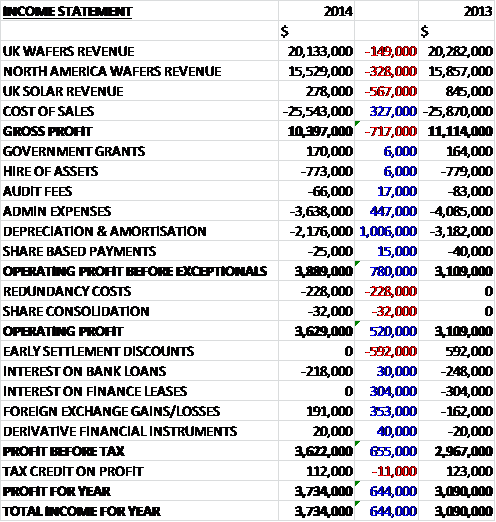

When compared to last year, revenues were down across all divisions with UK Wafers falling $149K, North America Wafers down $328K and UK Solar sales collapsing by $567K to just $278K reflecting the impact that change in the UK government backed feed-in tariff continues to have on the solar market. Cost of sales also fell but not by as much and gross profits were some $717K lower. Admin expenses also showed a $447K decline but the pre-exceptional operating profit only showed a $780K improvement on last year due to depreciation and amortisation falling by $1M, partly due to last year’s $700K increase due to a review of the useful lives of solar development assets. Exceptional redundancy costs meant that actual operating profit was only $520K better at $3.6M. Interest on bank loans was broadly cancelled out by foreign exchange gains and income from derivative financial instruments and a small tax credit helped to push the profit for the year up $644K to $3.7M. A decent increase but this was only due to lower amortisation costs.

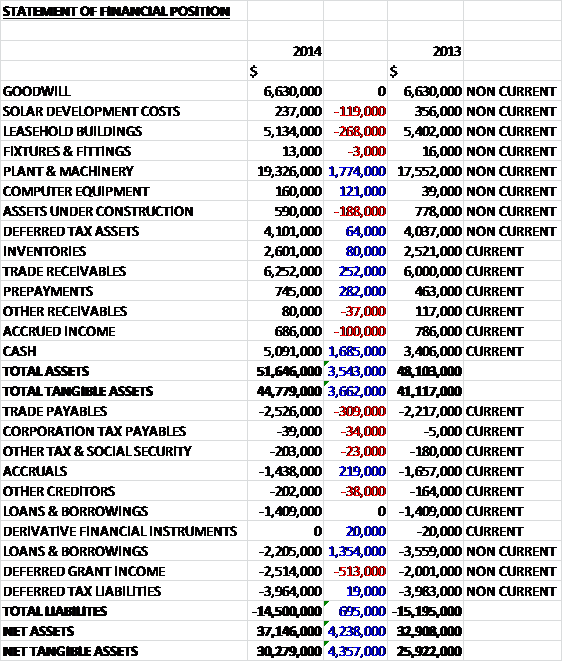

When compared to the end point of last year, total assets increased by $3.5M, driven by a $1.8M growth in the value of plant and machinery and a $1.7M increase in cash. Conversely liabilities fell as a $1.4M decrease in loans was only partially offset by a $513K increase in deferred grant income and a $309K growth in trade payables. This has resulted in net tangible assets up some $4.4M to $30.3M.

Before movements in working capital the cash profits were down $284K to $6M. After an increase in receivables as the average credit period for sales increased from 57 to 63 days with some $1.6M overdue, cash from operations was down $276K to $5.6M but a much lower interest paid than last year meant that net cash from operations, at $5.5M was some $346K higher. The group then spent $3.6M on property plant & equipment, somewhat offset by a government grant to give a free cash flow of $2.6M, down by $1.2M on 2013. The group then paid back some bank loans and still ended the year with a cash inflow of $1.7M. Despite there not being much progress on cash flows from last year, there is still a comfortable amount of cash being generated.

UK Wafers saw a result of $1.5M, a reduction of $700K when compared to last year and North America Wafers showed profits of $3.1M, an increase of $700K compared to 2013. Overall there was a 6% growth in the mature 200mm business but 300mm volumes remained flat as pricing pressures, which have now stabilised, impacted volumes in the second half of the year. The loss at the UK Solar business was $207K, an improvement of $750K compared to last year. Due to the further reduction in revenues, the business has been restructured to bring its costs base back in line with anticipated revenues.

The group has one customer who accounts for $6.4M of revenues, but no others that account for more than 10%. During the year there has been some pricing pressure due to the USD/YEN exchange rate favouring Japanese competitors which has now stabilised and tight cost control has meant that this has not had an adverse effect on profitability. The strength of Sterling has had an adverse effect of $200K on the year’s cost base.

With high utilisation levels at both plants, the group has implemented a programme to increase 300mm capacity and it is now fully operational. The group also invested in leading edge measuring equipment. As part of the restructuring that took place in 2009 there are a number of warrants issued to a number of people covering up to 22% of the total share capital and RBS also hold warrants covering nearly 3M shares, 750K of which have already been exercised. Operating leases increased considerably to $12.2M relating to a 99 year lease of land at the Swansea premises and the lease of land and buildings in Prescott, Arizona.

Going forward the board see the market as a whole growing driven by internet capable technologies such as TVs and home appliances and demand for mobile electronic devices such as tablet PCs and smart phones. Due to these trends, the group’s customers continue to invest in additional capacity and technology advancements which gives rise to wafer reclaim opportunities. Since the year end demand for the group’s services has remained strong with opportunities for growth in Asia and the large foundry sector and with good cost control, the board expect to make further progress during 2015. Given the high level of investment and capital, the board see new competitor risk as unlikely but sales are dependent on the continuation of industry growth, which, if not sustained could give rise to reduced sales volumes.

There have been a number of board changes over the past year. Stephen Boyd has stepped down as chairman due to other business commitments but he remains on the board as a non-executive director. His post has been taken up by Peter Harrington. Richard Howells has taken over as CEO, he was previously the CFO of the group. His post has been taken by Huw Lewis who has experience within the technology industry and in the financial structuring and management of international companies.

At the current share price the P/E rating is a very undemanding 4.8, but this increases to 7.4 on next year’s forecast. At the end point of the year the group moved into a net cash position on $1.5M from a net debt position of $1.6M last year which has prompted management to look at providing a maiden final dividend of 0.43p per share that represents a yield of 0.7% at the current share price with the predicted interim dividend bumping this up to 1.1% next year.

Overall then, I see this company as being a bit of a mixed bag. Profits were up on last year, but this was only due to a reduction in amortisation and would otherwise be lower. Net assets were up due to strong increases in the value of fixed assets, and an increase in cash along with a reduction in loans, but here too it is perhaps not as positive as it initially seems as the group has taken on much larger finance leases, which are kept of the balance sheet. There is a decent cash flow, and although it is not that different from last year, the reducing debt has given rise to lower interest payments and the company was able to spend quite highly on capital expenditure, pay back some bank loans and still have a positive cash flow. Operationally, it seems that there has been some recent pricing pressure which has now stabilised and the UK solar business is making a smaller loss, although it remains to be seen as to whether there is a future here. Finally, there seems to be a large number of outstanding warrants on the shares which might lead to dilution in future. On a P/E basis the shares are very cheap and although modest, the introduction of dividends is good but there seem to be a number of reasons to keep me on the side lines for now.

On the 27th November the group released a trading update. Trading was in line with market expectations and recent engagement with customers in the US and Asia has been particularly positive. Nothing else was added so nothing seems to have changed.

On the 22nd December the group announce that their facility in Swansea had suffered fire damage and it is anticipated that production at the site will be affected and in the interim some production will be moved to the Arizona site temporarily. A further announcement will detail the full scale of the problems but although the group is insured, this is sure to cause some short term disruption.

On the 25th February the group gave an update on the situation with the fire. The group was comprehensively insured which included a 3 year business interruption cover. It is anticipated that it may take up to a year for full scale production to recommence. The Prescott facility is currently undertaking a qualification process with a number of Swansea’s customers which will enable some of the production to be switched which should take place from May onwards. The interim results will include an impairment charge of $15.3M in respect of the loss estimated to have been incurred due to the fire. While the assets are insured and the insurers have accepted liability, any reimbursement is a separate economic event for accounting purposes and is only recognised when the claim has been quantified and agreed by the insurance company which is not expected to happen before the end of the year.

On the 1st May the group released a statement covering the insurance claim. Negotiations with the insurers have now concluded and the board believe they have reached satisfactory settlement terms. The claim comprised of replacement costs of property, plant & equipment and three years business interruption with a cash sum settlement being agreed. The board is now not planning on resuming operations at Swansea but to continue operations in Arizona, instead electing to return some cash to shareholders. The settlement represents a discount to the potential full cost of reinstatement of the Swansea facility, including compensation for business interruption. There are also a number of significant liabilities which will need to be settled with regards to the closure of the Swansea site.

The board believes the settlement will enable a return to shareholders at a value significantly higher than the average price of 60p per share that the company’s shares have been trading at but it is unlikely to be more than 125p per share. Given that by the time the Swansea facility is up and running, many customers are likely to be entrenched with the competition, this really seems to be the most sensible course of action and quite an amazing result for shareholders, of which I am sadly not one.

On the 12th August the group released a trading update. They have confirmed the disposal of the fire damaged property in Swansea and the assignment of the 99 year lease to Breathless LLP. It is also confirmed that all outstanding obligations under Government grant funding have been settled and all redundancy liabilities have been substantially settled following the expiry of the statutory consultation period. Based upon current information, the board now estimate the return of surplus funds resulting from the insurance settlement will be in the region of 140p to 145p share which is significantly higher than yesterday’s closing price! In addition, the underlying profits for the year at the remaining Prescott facility are in line with management expectations with the facility currently running at record levels of productivity and high utilisation.

Clearly this is great news for anyone holding the shares from yesterday and although there might be some further improvement in the share price, I suspect most of the good news is now factored in here.