Avon Rubber is a design and engineering group specialising in two core markets; Protection & Defence and Dairy. They are a recognised market leader in Chemical, Biological, Radiological and Nuclear respiratory protection systems serving the military, homeland security, fire and industrial markets. In dairy, they manufacture liners and tubing for the milking industry. A niche market seems to be the supply of hovercraft skirting assemblies, fuel storage tanks and water storage tanks to the US Army and Navy. The group is part of the FTSE small cap index and they have now released their final results for the year ending 2014.

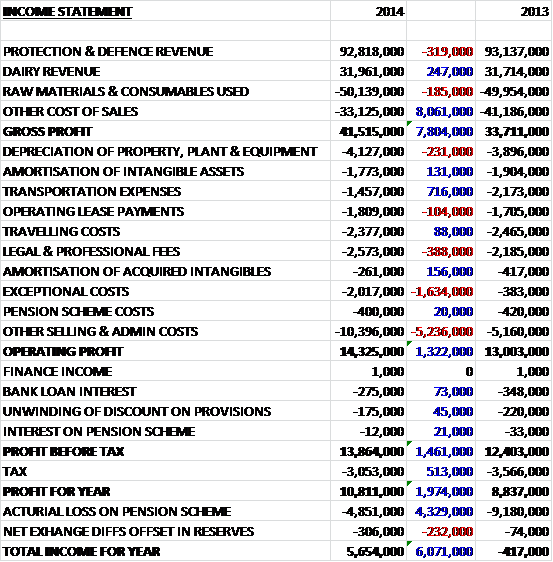

When compared to last year, revenues were broadly flat with a small fall in protection and defence revenue, despite a £2.4M increase of customer funded R&D being included in the figure. This fall was offset by a small increase in dairy sales although these revenues show the adverse changes in currency exchange rates as at constant exchange rates revenues would have increased by £5.6M. Costs of sales fell considerably during the year, however, to give a gross profit some £7.8M higher. There was also a big fall in transportation expenses but a £1.6M increase in exceptional costs relating to the relocation of the Lawrenceville facility and consolidation of US operations, and an increase in other costs in general meant that the operating profit was £1.3M higher at £14.3M despite the £800K effect of currency headwinds. There were modest declines in all of the finance costs and there was a more favourable geographic mix as far as tax was concerned so the total profit for the year was £10.8M, a £2M increase on the outcome in 2013.

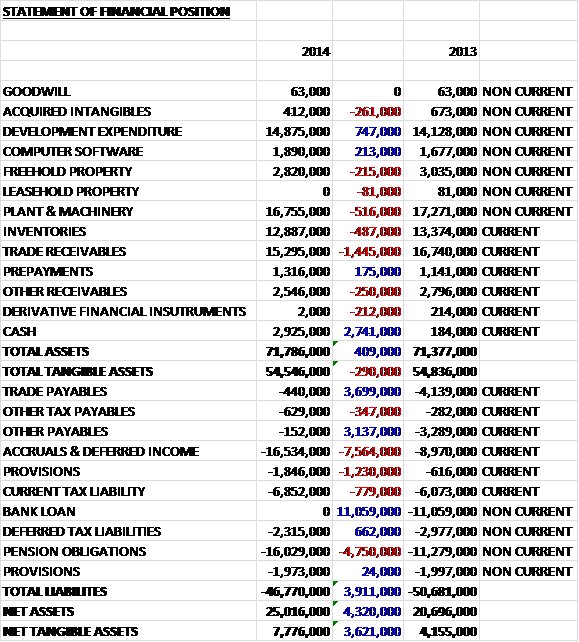

When compared to the end point of last year, total assets were just £409K higher. The increase was driven by a £2.7M hike in cash levels and a £747K increase in development expenditure capitalised, partially offset by a £1.4M decrease in trade receivables, a £516K decline in plant and machinery and a £487K fall in inventories. Liabilities fell during the period due to an £11.1M fall in the bank loan, a £3.7M decline in trade payables and a £3.1M decrease in other payables, somewhat offset by a £7.6M jump in accurals & deferred income, a £4.8M increase in pension obligations and a £1.2M growth in provisions relating to the cost of consolidating the four US sites into three after the expiry of the lease on the Lawrenceville facility. The result is a net increase in assets of £4.3M to £25M. There were £11.8M of non-cancellable operating leases not included in the above balance sheet, a fall of £1.8M on last year.

Before movements in working capital, cash profits were some £1.5M higher at £21.3M. Favourable movements in all parts of working capital meant that cash from operations was £10.2M higher at £25.5M, although part of this was due to a £3.5M accelerated payment from a major customer before their financial year end. Slightly more tax than last year meant that net cash from operations was £21.8M, an increase of £9.7M. About £3.8M of this cash was spent on tangible assets and another £3.1M on development costs and IT. The resulting free cash flow of £14.9M was some £14.3M higher than last year. This was used predominantly to pay off all of the bank loans with another £1.4M used for dividends. The resultant cash flow was £2.7M compared to a neutral position last year. This really was a good performance and now that loans are paid off, there should be great scope for acquisitions or increased dividends going forward.

Protection and Defence profits were £11.3M in 2014, an increase of £1.1M on last year. The order intake during the year was £93M with increased orders from the DOD, EMEA and North American customers. The long-running DOD M50 mask contract is now in its seventh year (of ten) and 168,000 systems were supplied during the year (which relates to sales of £34M compared to £45.2M last year) and due to the high order intake of mask systems, they enter 2015 with an order book covering the first half of the year sales at a slightly accelerated rate. Follow on orders are expected in the first half of next year as 2015 budgets are released. The filter requirement has less visibility but it is expected that this consumable item will be a good source of repeat revenue in the long term as more masks enter service. During the year the Joint Service Aircrew Mask programme design, development and testing work progressed well. This $6.7M development contract is due to finish at the end of 2015 and should lead to a production contract worth up to $74M.

Sales to law enforcement and non-US military increased from £25M to £31M and the group won an industrial order in the final quarter for 27,000 escape hoods of which the majority will be delivered next year. Sales to the fire market were flat in the first half of the year as buyers held off ordering until the delayed NFPA standard was released. The Deltair SCBA was designed to meet these new US standards and to enhance operational performance and it has been well received in early customer trials with orders received for 600 units that were carried forward into next year.

The newly developed Emergency Escape Breathing Device received NIOSH approval to the new standard with Avon being the only manufacturer to achieve this. The product has applications on board navy ships and in the mining sector and the US Navy has an open solicitation to replace its ageing installed base which the group expects to respond to in early 2015. The non-DOD side of the business includes the North American first responder market and the Rest of the World military and law enforcement market, both of which are being driven by an increased need to provide improved protection against growing global CBRN (Chemical, Biological, Radiological and Nuclear) threats. Competition in the fire market is intense and at present the new Deltair self-contained breathing apparatus is one of three approved to the new standard and has been well received in the market which the group anticipates will help it improve market share in this area next year.

In non-US markets, the CBRN respiratory protection device is building business in South America and the Middle East and the group have started to make progress into new markets such as the oil and gas sector and the broader industrial sector is seen as an opportunity for growth. In total sales in the ROW market increased by 26% which is a helpful improvement in diversification. Eleven new products received regulatory approval during 2014 and a pipeline of further products has been submitted for approval in 2015 which should deliver further product launches.

Dairy profits were £5.7M in 2014, an increase of £520K when compared to last year. Sales in the Dairy business have become less dependent on OEMs in recent years as the group continues to grow their higher margin own brand Milkrite products and the proportion of revenue made up of OEM customers has fallen from 47% to 31% in four years. Market conditions improved during the year with milk prices and feed costs returning to more normal levels and demand for the consumable products was generally at a higher level than last year. The industry seems receptive to new products and the new Impulse Air product has gained a 21% market share in the US. A new product that is being launched is the Cluster Exchange Service. Under this programme farmers outsource their liner change proves to Avon who handle all aspects of this process. So far it is servicing 887 farms, ahead of initial expectations and the service has the potential to grow significant recurring revenue streams in the years to come as more farms sign up.

The group see a huge potential for their dairy products in emerging markets, particularly in the BRIC nations as the growing demand for animal protein in diets has led to an increased demand for dairy products, driving demand for the group’s consumable product. A sales and distribution facility was established in China during 2012 and in the first half of 2015 the group expect to open a similar facility in Brazil which is another exciting market. In the US the Milkrite brand has a 40% market share with Impulse Air having a 21% share. In the EU the market shares are 16% and 2.5% respectively whilst in China contracts have been secured with the country’s largest milk suppliers and distributors, Mengniu and Yili. After a soft first half in China following the contaminated milk scandal in the country and an outbreak of foot and mouth, volumes returned to expected levels in the second half

Some of the new products included AvonAir, a new range of powered air purifying respirators; the M62 filter supplied to the DOD and designed to cover a wider variety of threat scenarios; Delatair, the new fire service offering that was launched to the market in the second half of 2014; EEBD, an emergency escape breathing device which has military applications on board ships along with additional mining applications.; HMK150 Helmet Mark Kombination that was launched in 2014 and became the first product to meet a new German police standard for respiratory protection; and further development activity is expanding the respiratory product offering in the aerospace market and underwater diving market.

In the Protection and Defence business the US DOD accounted for £43M of the total revenues which is the equivalent of a staggering 35% of sales. Clearly the group is very reliance on this one client which does represent a potential risk going forwards. Also, the bulk of sales are made in the US in general, making the group susceptible to swings in the USD/GBP exchange rate and a 5c change in the exchange rate would have a £415K impact on profit before interest and tax. The pension scheme is another potential banana skin but the group currently have the deficit under control and will make recovery payments of £300K in addition to £250K towards scheme expenses next year with total payments increasing to £675K in 2016, and £700K in both 2017 and 2018. Other risks to look out for are problems or delays in obtaining regulatory approval for new products and any potential increase in animal feed prices or a fall in milk demand.

During the year the group acquired VR Technology for total consideration of £833K, £300K of which is deferred with £200K of this contingent on certain performance conditions. There was a £63K payment of goodwill, although the intangible assets were valued at £923K. The company designs and manufactures diving rebreather systems and dive computers. The relatively low tax rate is because the group only currently pay tax in the US as in the UK they are still utilising tax losses and have unrecognised tax assets amounting to £1.4M still to be used. It was announced that non-executive director Stella Pirie will stand down at the AGM after completing a 10 year stint and a recruitment process to find a replacement in underway.

Going forward, the outlook for next year seems positive. The DOD contract gives good visibility to earnings and the board expect to see growth in the fire and industrial markets. In the dairy business, they expect to see growth from the investments made in China and Brazil and from the Cluster Exchange Programme.

The shares are not cheap on a P/E basis as they are 22.7 at the current share price, although this does fall to 17.6 on next year’s estimate which given the quality growth story doesn’t seem too bad. The shares yield 0.7% after a 30% increase in the final dividend, rising to 0.9% on next year’s estimation so at present I could not consider them an income story. At the end of the year the group is in a net cash position of £2.9M which is clearly very favourable compared to the net debt of £10.9M the group had this time last year and really gives the group some freedom to invest or return some cash to shareholders.

Overall then, this is a good set of results. Profit are up, as are net assets but it is the cash flow and elimination of debt that makes this quite exciting. If cash flows are similar next year, there will be a lot spare to invest where management sees fit. I do think the reliance on the US DOD, although it does give good visibility to earnings in the short term, has the potential to be a problem and I am not sure what happens when the 10 year contract runs out (we are now in year seven). The new products do sound exciting and the push into emerging markets with the dairy product has the potential for a good growth story, although I suspect things will not completely run according to plan – they never seem to in China. Altogether though, this seems like a good, strong company and I will look to enter at a suitable point.

On the 23rd January the group released a statement that informed the market that the company’s own pension trustees had sold 194,495 shares, equivalent to about £1.4M. This now means the trustees have less than a 3% stake in the business which is hardly a ringing endorsement of the value of the shares!

On the 29th January the group released an AGM statement covering the first quarter of the year. Trading was in line with board expectations and the group was strongly cash generative with a net cash position at the end of Q1 of £6.4M. In Protection and Defence, the focus, as planned, has been on fulfilling the orders for the DOD and this is likely to continue for the rest of the half year. There is a high level of quotes out for the higher margin export military masks but the timing of order receipts remains unpredictable. There was a year on year growth in the fire service products and the level of enquiries for the new Deltair unit has been strong. The positive momentum in the Dairy business has continued into the first quarter with trading being very strong. The take up of the Cluster Exchange service has been encouraging in North America and Europe and the Brazilian facility has been set up. All in all this is an excellent update and I will definitely be looking to enter here.

The chart for Avon looks pretty good, after a year or so of consolidation, the shares seem to be on a bullish run again having set a new all-time record high in late January.

On the 17th February the group released an announcement that informed the market that Blackrock sold nearly 9,000 shares for about £70,000 to bring their holding to just under 11% of the total capital. This is a shame as I don’t really like to see these large institutions selling shares I own despite the sale being quite a modest amount. Since the chart I posted above, the shares have had a bit of a retrace but the 50 day moving average could act as some support. I am also slightly concerned that the falling milk price might affect the dairy sales so I’m less confident than I was and wondering if I mis-timed my entry point. I am still holding on but might sell out for re-entry later if the shares continue to fall.

On the 25th February it was announced that Pim Vervaat had been appointed as a non-executive director. He is CEO if RPC, a UK based manufacturer of rigid plastic packaging and a FTSE 250 company. This seems like a pretty good appointment to me.