Amino Technology is a company specialising in IPTV software technologies and hardware platforms that enable delivery of digital programming and interactivity over IP networks. They provide set top boxes to the industry and their products are deployed by worldwide network operators and service providers. Revenues are principally derived from the sale of IPTV set top boxes and associated customer support services. They are listed on the AIM exchange and have now released their final results for the year ending 2014.

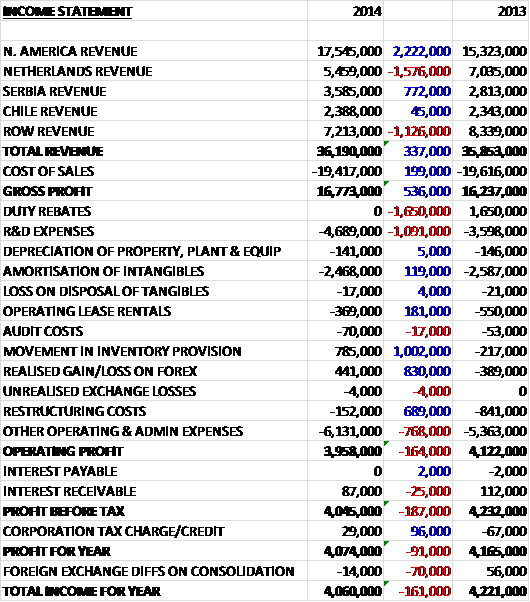

When compared to last year total revenues were £337K higher, driven by North America and Serbia, somewhat offset by reductions in Netherlands and ROW sales due to difficult conditions in Western Europe. Cost of sales were also somewhat lower so that gross profits were £536K higher at £16.8M. R&D expenses increased by £1M as less expenditure was capitalised but there was a reversal with regards to inventory provisions. Other operating costs were also some £768K higher and there was the lack of the duty rebates that occurred last year but restructuring costs were some £689K lower so that operating profit fell by £164K. There was then slightly less interest receivable, offset by a corporation tax rebate so that the overall profit for the year was £4.1M, a decline of £91K when compared to 2013, although those duty rebates last year were the underlying cause of this fall.

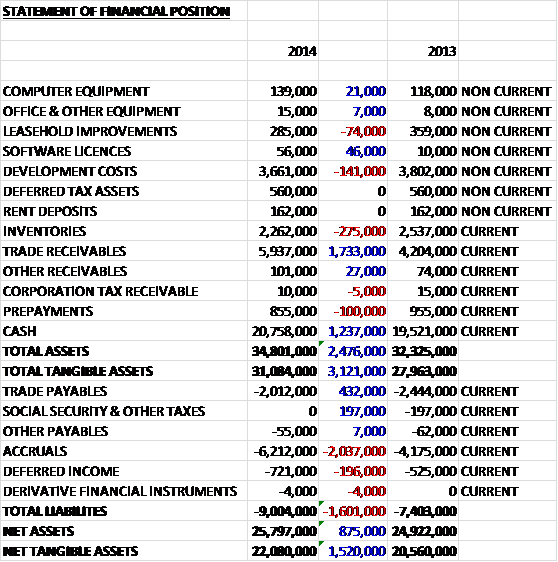

When compared to the end point of last year, total assets were some £2.5M higher. This increase was driven by a £1.7M growth in trade receivables and a £1.2M increase in cash, only partially offset by a £275K fall in inventories. Liabilities also increased during the year as a £2M increase in accruals was partially mitigated by a £432K fall in trade payables. In all, net tangible assets were £1.5M higher at £22.1M. In addition there was £1.5M of operating lease liabilities not on the balance sheet but this doesn’t make much of a dent in the net asset level.

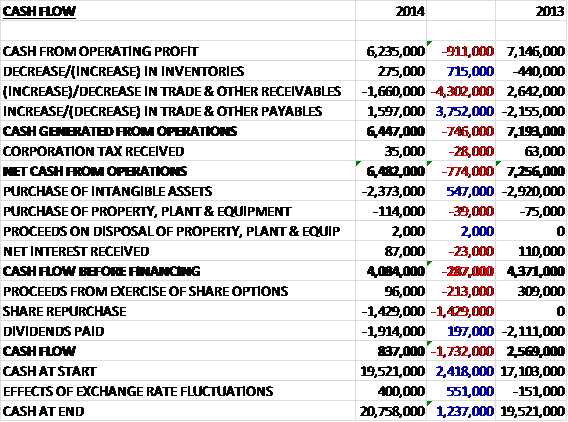

Before movements in working capital, the cash profits fell by £911K to £6.2M before payables and receivables broadly cancelled each other out so that net cash from operations was some £774K lower at £6.5M. The bulk of this cash was spent on intangible assets with a small amount on the purchase of property, plant and equipment so that free cash flow was down £287K to £4.1M. The group spent this fee cash on dividends and a share buy-back programme which still left a cash inflow of £837K, added to the big £19.5M cash pile at the beginning of the year. Despite the decline, the group is still pleasingly cash generative.

The move towards Internet Protocol as the means of delivering multiscreen services to customers is changing the entertainment service delivery industry, particularly in the cable TV market. In addition, the move towards 4K Ultra HD TV delivery is gathering pace and creating opportunities for the group, although mass market take-up will not likely be achieved before 2018. The group’s markets are evolving quickly as the way entertainment is consumed reshapes the operator strategies but operator demand for simple, reliable IPTV devices remains strong, particularly in emerging markets although they are looking for higher performance devices that blend IPTV with OTT content delivered over the open internet along with a greater demand for the “internet of things”.

Some new products include the integration of Youtube, achieved after the year end and the addition of the company’s new app store. A new service layer based around home monitoring and control was also launched towards the end of the year called Home Reach. This service uses cameras, door and movement sensors to enable users to monitor their homes using their smartphones and customer interest has been high with a few early stage trials underway. New opportunities in the pay TV industry are also emerging with the wider industry transition to IP as the means of delivering multiscreen and connected home services presents new opportunities for the group in different markets and analysts see the entire industry moving to IP for service delivery after some satellite and cable operators have already begun to add IP based services to their offerings. Another product opportunity is the delivery of HD services at much slower network speeds than previously experienced.

In North America the company achieved decent revenue growth. The launch of the Live Advanced Media Platform was well received with contracts secured with ITC and C-Spire, which in the case of the latter is a company that has recently transition from a mobile services provider to a fibre based delivery model encompassing broadband, telephony and entertainment services. This trend was echoed the Middle East where Turkcell deployed the platform as part of its multi-service broadband, mobile and entertainment offering.

The company received solid demand for its lower spec product in Latin America and Eastern Europe where new contracts were secured in Argentina where de-regulation is opening up the market for operators to deploy IPTV services and a new contract was secured with the leading Albanian operator. The new A150 device was taken on by a long established operator in the Latin American market as a replacement for their existing Amino product and in the Caribbean the group secured a contract with LIME, part of the Cable and Wireless group, for the provision of devices for a service rollout across a number of territories.

Western Europe was a challenging market during the year with a combination of economic uncertainty and market saturation in certain territories. A key customer in the Netherlands re-entered the market towards the end of the year, placing new orders for the new A150 device and another operator in the Netherlands is now deploying the group’s new Timeshift pause live TV solution which is a USB flash drive that enables users to pause and rewind live TV.

A new VP of global sales and new specialists on the sales team has given it sharper focus on customer engagement which is feeding through to an upturn in tender activity through the second half of the year and stronger lead generation. It seems like the Chinese venture is at an end with the office closed and functions being moved back to the UK.

The group is somewhat susceptible to changes in exchange rates. A 5% strengthening of Sterling against the US Dollar would have an adverse £200K effect on post tax profit whereas the same change of the currency against the Euro would not have an effect. There are three customers that account for more than 10%of revenues. One US customer accounts for a whopping 29% of sales with another one making up 15%. There is also a Dutch customer who accounted for 11% of turnover and sales to this customer seem to be declining. It seems that the group is very reliant on just a few clients which is a potentially dangerous place to be. One other thing that I have noticed is that there seem to be quite a lot of receivables that are overdue and in fact 18% of all the group’s receivables are past the due date which is something that the company might want to take more control of as none of them were covered by credit insurance.

As already seen there were a number of one-off costs and rebates. This year the restructuring costs related to the closure of the Chinese office whereas the higher costs last year reflect the closure of the Swedish office and some additional reorganisation in the UK as the group concentrated its R&D facilities in Cambridge. Last year the group received two rebates in respect of duties paid on previously recognised international sales. In addition the group has received a further favourable ruling with respect to duties rebate at a tax tribunal, HMRC appeal not withstanding, that could realise a cash receipt of about £700K next year.

Going forward the board expects the new enhanced portfolio will increase the company’s addressable market to build on the trends seen in the second half of 2014 and should contribute to revenue growth in 2015. In addition they continue to evaluate options to broaden the company’s position in the wider IP market pace and that the outlook for 2015 seems positive.

At the current share price the underlying P/E is standing at 16.6, reducing to 16 on next year’s forecast and the shares yield 3.8% in dividends, representing a 45% increase year on year. The pay -out increases to 4.2% on next year’s forecast. The board is committed to using that big cash pile to grow the dividend by 10% or more per year for the next two years.

Overall this seems to be a decent update. Although profits are pretty flat, this does reflect one-off charges and rebates and the underlying profit is actually up on last year. The balance sheet seems very healthy with net assets increasing somewhat as a higher number of orders in the second half increased the amount of trade receivables on the book. Cash generation was also strong, although it did decline at an operational level, with the cash pile pretty massive. The new products seem interesting and it appears the group has a few exciting new opportunities in what is a fast growing market. Given the cash levels, the P/E ratio is not high and there is a decent yield on the shares. The only thing holding me back is the reliance on a small number of major customers but despite this I will probably look to buy some shares in this company.

Looking at the chart we can see the share price has recently improved so is this trend continues it may be a good time to buy the shares.

On the 24th February the group announced that it had received a rebate of £700K relating to duties paid on historic international product sales. This was expected but nice to see the confirmation nonetheless.

On the 5th March it was announced that Donald McGarva, CEO, has purchased 10,701 shares at a cost of just under £15,000. Whilst not a large buy for someone who owns £438,000 of the share capital, it is still good to see director buying when it is not forced upon them by poor share performance.

On the 23rd March it was announced that Schroders had sold 663,419 shares in the company at a value of about £925K. While disappointing, they still own just under 13% of the share capital.

On the 20th May the group announced the acquisition of Booxmedia for an initial consideration of €7.9M. Booxmedia was founded in Finland in 2009 and is a software as a service cloud TV platform provider. Its core product suite enables operators and service providers to launch TV Everywhere services using an off the shelf cloud platform, removing the need to build their own bespoke technology infrastructure. Booxmedia customers can provide their subscriber base with pay-TV features such as DH quality streaming of live TV; access to catch up TV, video on demand and cloud based recording; playback of content that can be started on one device and finished on another; and functionality that turns a mobile device into an intelligent remote controller for internet connected TV screens. Existing customers of the group include quad play operator DNA that offers a TV everywhere smartphone and tablet service based on the Booxmedia platform.

The acquisition will enable Amino to offer solutions to new customer segments including mobile operators, OTT service providers, media companies and broadcasters alongside its current fixed line telecoms operator customers and should provide a number of cross selling opportunities. It will also strengthen Amino’s core IP entertainment software capabilities which will now extend to include IPTV devices, mobile devices and the cloud. The initial consideration will be satisfied with €7.2M cash and €700K in Amino shares and will be funded from existing resources. Additional consideration of up to €2.6M, shared equally between cash and shares will be payable based on future performances up to the end of 2017.Booxmedia’s revenue and EBIT last year were €1.4M and €200K respectively with about 54% of recurring revenues.

This does seem like a good opportunity for expanding both services offered and the customer base and looks to me like a good use of that massive cash pile, although it could be argued that the acquisition is not cheap based on the EBIT performance of Booxmedia last year.

On the 4th June the group released a trading update covering the first half of the year and it expects both revenue and pre-tax profits to be ahead of last year. The net cash balance currently stands at £16.8M compared to £19.7M at the end of the first half of last year even after £5.2M of cash was used to acquire Booxmedia. The company expects the second half weighting of revenues to continue this year and is confident that the results for the year as a whole will be in line with expectations. Good progress has been made in Western Europe and North America in particular where performance has been consistently strong during the period and momentum in new markets such as the Middle East and Africa has been encouraging with good traction and initial orders achieved. The board is recommending an interim dividend of 1.265p per share, a 10% year on year increase and representing a rolling annual dividend yield of 3.7%. So, overall this is a steady rather than spectacular update in my view.