Dechra Pharmaceuticals has now released its interim results for the year ending 2015.

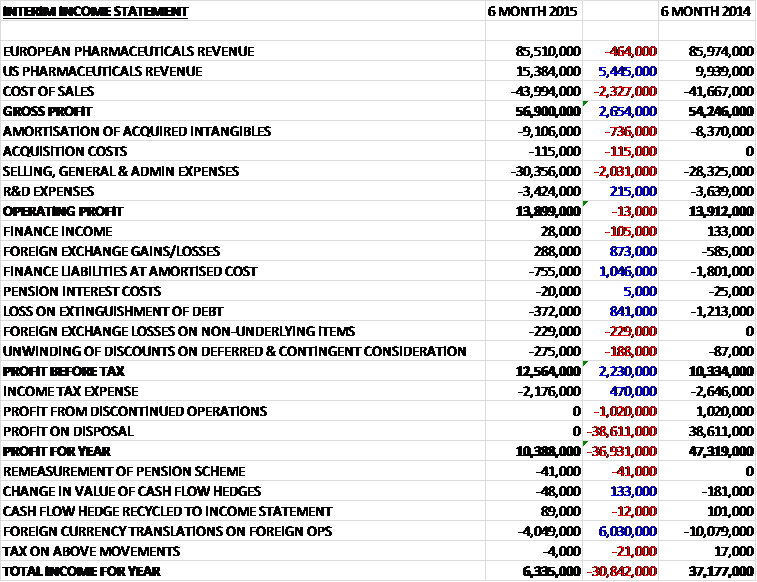

When compared to last year, revenues increased against a soft comparator during the first half of last year due to the £5.4M growth in sales from US pharmaceuticals, somewhat offset by a small decline in European sales due to the weakening Euro. An increase in Sales for Companion Animals, Equine products and third party man was partially offset by falling revenues in Food Producing animals and Diets. Cost of sales also increased so that gross profit was some £2.7M higher than in the first half of 2014. There was a slightly higher amortisation of acquired intangibles and selling & admin costs increased by £2M year on year as the group supported the launch of Osphos and established the infrastructure for the new subsidiaries to give an operating profit that was flat on last time at £13.9M.

As far as finance costs are concerned, there was an advantageous swing in foreign exchange losses/gains and we saw finance liabilities at amortised cost decline by more than £1M (whatever they are) and an £841K improvement in the loss with the extinguishment of debt which pushed profits before tax up to the tune of £2.2M. A lower tax expense, due to lower corporation taxes in Denmark and the UK along with savings from government backed incentive schemes, was dwarfed by the lack of the profits at the discontinued operation so that profit for the year fell by £36.9M to £10.4M. Underlying operating profits, where the biggest reductions are those intangible amortisations (that occur seemingly every year) were £22.7M this half year, an increase of £2.7M.

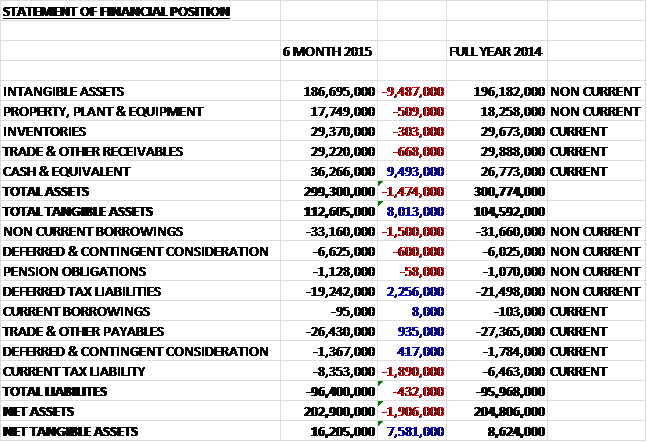

When compared to the end point of last year, total assets at the six month mark this year were down by £1.5M to £299.3M. This was driven by a £9.5M decline in intangible assets, along with smaller falls in most of the other asset classes, somewhat offset by a £9.5M increase in cash. Total liabilities also increased due to a £1.5M increase in borrowings, somewhat offset by a net £366K fall in tax liabilities and a £935K decline in trade & other payables. The overall result is a £1.9M decline in net assets but when the intangibles are stripped out, net tangible assets actually increased by £7.6M to £16.2M which actually makes the balance sheet look rather better than before.

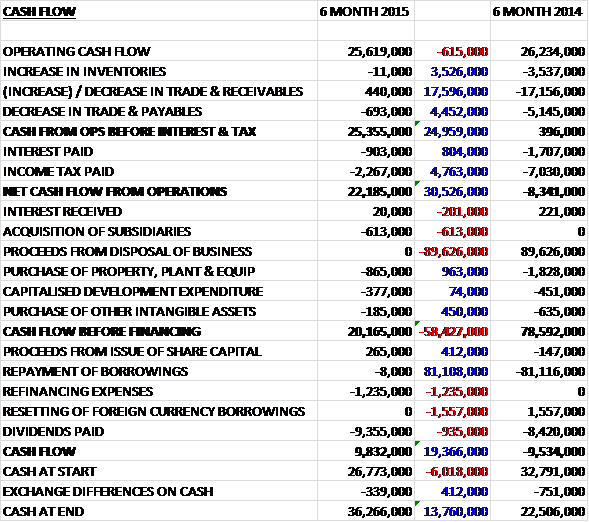

Before movements in working capital, cash profits during the first half of the year fell by £615K to £25.6M. Strong working capital control meant that operational cash flow was similar, at £25.4M and far better than last time due to the large increase in receivables that happened previously, presumably related to the disposal. Interest fell considerably compared to the first half of last year as the group paid off debt, and tax was also lower so that the net cash generated from operations was some £30.5M better than in H1 2014 and stood at £22.2M. A small amount of this cash was paid to acquire a business and less than £1.5M was spent on capital expenditure to give a staggering free cash flow of £20.2M. The only other expenses were the £1.2M of refinancing costs and £9.8M spent on dividends. The resulting cash flow for the half year was £9.8M to leave a cash pile at the end of the period of £36.3M.

Operating profit for European Pharmaceuticals fell by £1.1M to £24.1M although this was entirely due to adverse movements in exchange rates as the positive momentum that started during the second half of last year continued into this period with a revenue growth of 5.7% at constant currency rates. The increase was driven by the Companion Animal portfolio with sales ahead of expectations and a strong performance across all home markets. Equine products also performed well, benefiting from the launch of Osphos in the UK. Sales of diets fell slightly during the period as the external supplier was changed which affected supply somewhat. The transfer is now nearly complete with the new supplier providing improved palatability, quality and packaging leading to a re-launch for the brand. The Food Producing animal portfolio had a more difficult six months as the continued pressure on vets to reduce antibiotic prescribing affected sales. The problem was particularly acute in the Netherlands and Germany where the group has a large market share but management don’t see such large issues in their other, smaller, markets.

Operating profits for US Pharmaceuticals increased by £2.1M to £5.4M which represented a 61% increase at constant currency rates. The key therapeutic sectors of dermatology and endocrinology have both delivered organic growth close to 30% as the group gains market share and improves awareness of their products. Osphos was launched in Q1 and two ophthalmic products have been re-launched following the resolution of the long standing supply problems. Sales of the acquired Phycox have performed well during the period and the group also launched a new endocrine product, Levocrine Chewable tablets which were developed at the Phycox facility. Based on the strength of the recent growth and new product launches, the group is accelerating their investment in the sales and marketing infrastructure in the country.

The group is looking to expand geographically with the newly opened Italian facility trading in line with expectations and the Canadian subsidiary being successfully opened in January with further territories, including Poland being planned.

Initial feedback from the UK and US Osphos launch has been positive. In Q2 of this year, the group obtained approval in all European territories for TAF Spray, an antibiotic aerosol for a wide range of species including cattle. This antibiotic is used to treat superficial wound infections and contains an antibiotic that is not used in human health for the most part, which might make it attractive in markets where these antibiotics are tightly controlled. Progress has been made on the next global novel product which will be branded Zycortal with the group already completing the safety and efficacy sections of the final part of the dossier which has been submitted to the FDA for US approval. The dossier has also been submitted in Europe and it is hoped that the product will be available for launch in the next financial year in at least one major territory. There has also been an increase in the number of current projects in pre-clinical development which enhances the pipeline in future with several other opportunities in the exploratory phase also being reviewed.

During the period the group acquired PSPC Inc for a total consideration of £8.4M which consists of just over £5M in cash, £891K of contingent consideration that has already been paid due to the successful registration of Levocrine, and £2.5M still to be paid depending on future sales. The acquisition generated goodwill of just £84K but the vast bulk of assets were intangibles, relating to product rights, at £7.5M. The principle product of the acquired group is Phycox, a neutraceutical which competes in the US veterinary joint health supplement market. The group is still paying for the Dermapet acquisition with a further £600K of deferred consideration which was paid on the fourth anniversary of the deal. The maximum consideration still payable is $5M contingent on revenue exceeding $20M in any rolling 12 month period for a further two years. The PSPC acquisitions seems like it could be good value but despite the useful foothold in the US, it seems to me that the group did overpay somewhat for Dermapet and it is still a bit of a drag having the contingent consideration hanging over potential earnings.

The group has a similar list of potential risks as previously. The competitive environment remains with the launch of generic products in their key markets being a considerable risk. The generics of Felimazole and Comfortan have now been launched and the defence strategy against the Felimazole generic seems to be fairly successful so far with the group maintaining market position in most of its markets. As has been seen during this period, much of the group’s sales occur overseas which leads to exchange rate risk. The Euro continues to weaken against Sterling which could be a continuing problem for Dechra. The antibiotic prescription issue in farm animals continues to be a problem in Germany and the Netherlands but management doesn’t consider any other markets to be at significant risk.

Going forward, despite the continued focus on reducing antibiotic prescribing in Europe and ongoing global financial uncertainty, the group is meeting constant currency earnings expectations. The core portfolio is demonstrating growth, the product pipeline is delivering results and global expansion is progressing which gives management confidence that the group will “continue to deliver value to shareholders”. That sounds a bit noncommittal to me but most of the points made should give the group some basis for growth.

Following the 7.8% in the interim dividend of 5.12p the shares now yield 1.7% at the current share price. At the half year point the net cash position was £3M which is a very favourable position compared to the £5M of net debt at the end of last year. Overall then this has been a solid update. As previously highlighted, the supply issues in the US seem to have been resolved but the control on antibiotics in European farm animals continues to be a problem. Likewise, the weak Euro is a drag on earnings with underlying profits faring slightly better than the comparator period last year. As the intangibles continue to be amortised, the balance sheet is losing some of the huge number of intangibles and actually seems a bit healthier to me despite the decline in overall net assets. The cash generation has been fantastic during the period with a positive net cash balance and a tight control on working capital meaning there is a huge amount of free cash flow available. The group has not used the cash to pay down debt which makes me wonder whether they are going to use it for another acquisition. Overall, a decent if not spectacular performance which gives me some confidence to continue holding.

The chart has been rather bullish since the summer of last year and the shares have perhaps become a bit overbought after today’s results – we shall see what happens in the short term but the long term trend is very much up.

On the 28th April, the group released a management statement covering Q3 2015. Overall, trading continues to be in line with expectations. Strong third quarter sales have been flattered by the phasing of pre-Easter ordering in Europe and competitor stock shortages in the US. Revenues in the quarter increased by 6% compared to a year to date increase of 6.6% (although this quarter showed a 14% increase at constant exchange rates). Revenues in Europe fell by 3.3% in the quarter but this was entirely down to the weakening Euro as constant currency revenues increased by more than 7%. Companion animal products grew by 13.5% (at constant rates), Equine products were up 30% but food producing animal products fell by 13%. The diets franchise is showing signs of recovery as the back order issues are resolved following the transfer of manufacture to a new supplier.

The Canadian subsidiary started trading in January and North American revenue as a whole grew by 67% in the quarter with US revenues up 58%. This impressive growth is partly attributable to the recent acquisition of Phycox, the launch of Osphos and the re-launch of two Ophthalmic products following the resolution of long term supply issues. This quarter has also seen strong trading in the dermatology product range due to a competitor running out of stock. The new Polish entity has been established and a sales and marketing team have now been recruited with the office to start trading next year. FDA approval has been received for the injection facility in Skipton, which is important for the US launch of Zycortal as it will be manufactured there and in March the group made a $1M investment in Jaguar Animal Health to potentially gain access to the EU marketing rights for their companion animal products.

Things seem to be ticking along nicely, currency headwinds not withstanding and I feel comfortable with this investment.

On the 8th July the group released a trading update covering the full year. Group revenue increased by 5% year on year and at 10% on a constant currency basis and trading results were in line with management expectations. Revenue in European Pharmaceuticals increased by 4% on a constant currency basis driven by a buoyant UK market but the continued weakening of the Euro has meant that at actual exchange rates revenue in the division fell by 2%. There was a continued strong performance across the portfolio in companion animal products partly offset by a decline in food producing animal products with the German and Danish businesses continuing to be impacted by the increasing focus on the use of antibiotics. After the completion of the transfer to a new third-party manufacturer, the pet diet sales recovered from the stock-out issues reported in Q3 and sales ended broadly in line with last year. The new subsidiary in Poland started trading in May, ahead of schedule.

In North American pharmaceuticals, revenue grew by 60% at a constant currency basis (a bit more on actual exchange rates). The performance was enhanced by the full year trading of Phycox, the relaunch of Ophthalmics, the launch of Osphos and Levocrine and the start of the Canadian subsidiary. Adjusting for these items, the sales of core products grew by 16% which is still an impressive performance. During the year Osphos for equine lameness was launched in the US and UK in Q1 with approval in the EU following in Q4; TAF Spray, a generic antibiotic aerosol, received approval in Q2 across Europe; and FDA approval was achieved for the injection facility in Skipton in Q3 to manufacture Zycortal, a new canine endocrine product.

So, there seems to be steady growth here, although the continued weakening of the Euro and the ongoing reduction in antibiotic use in food producing animals are both having an impact on results.

On the 3rd August the group announced that it had signed a conditional share purchase agreement with the owner to acquire his 63.3% holding in Genera, a Croatian listed pharmaceutical business. Dechra is offering the equivalent of £19.4M for the shares which relates to €51.4M for the total share capital which will be funded through the existing debt facilities. Under Croatian takeover rules, the offer required Dechra to make a mandatory offer for the remaining share capital of Genera.

Genera is the largest manufacturer of animal health products in Croatia. It operates three main divisions: Animal Health, which represents the majority of revenue; Agrochemicals and Human Pharmaceuticals. Over the past few years, vaccines have become a key part of the animal health division with particular investment going into its poultry vaccine capabilities including regulatory submissions into the EU. Last year, Genera made a profit before tax of just €400K on revenues of €28.4M and net assets totalled €19.7M.

The transaction is expected to be earnings neutral for the first two years of ownership and enhancing thereafter. The rationale I think must be that Dechra want to move into vaccines since animal antibiotics seem to be a declining field in Europe which I think makes strategic sense. I am not sure what they are going to do with the human pharmaceuticals though. In all, it seems a decent fit but the valuation looks a bit rich to me.