St. Ives is a marketing and print business. The marketing services segments includes data marketing, digital marketing, consultancy services and field marketing whilst the print segment includes marketing print, comprising of exhibitions, events and point of sale specialists and print management business and books. The group does not act as a single entity but as a group of different businesses, each with its own unique proposition and brands. It has now released its final results for the year ending 2014.

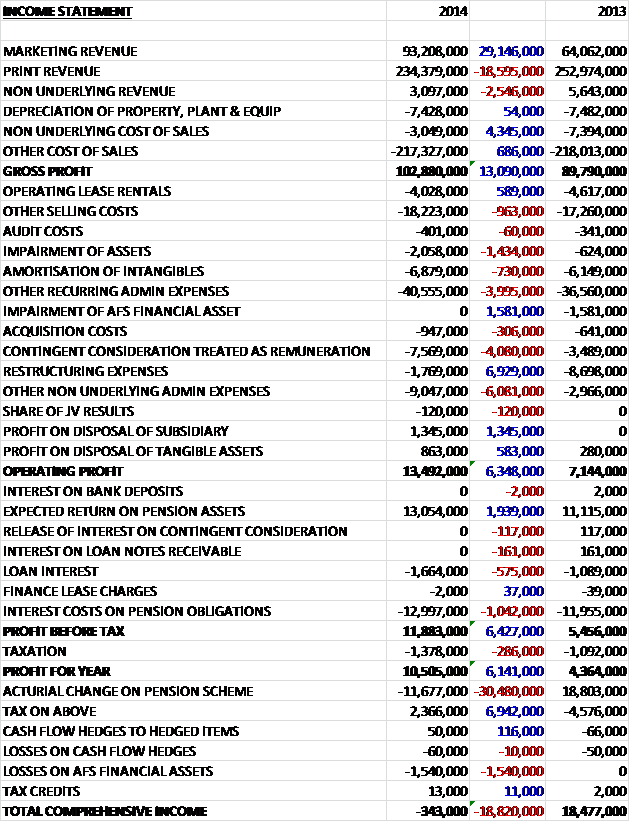

When compared to 2013 revenues were up as a £29.1M increase in marketing revenue, due to acquisitions and organic growth, was partially offset by an £18.6M fall in print revenue due to the disposal. Cost of sales fell during the year so that gross profits increased by £13.1M to £102.9M. There were then several one-off impairments and a big increase in other non-recurring admin expenses, somewhat offset by the lack of the impairment on available for sale financial assets, relating to non-controlling interests in Easypress, Wiforia and Ebeltoft. There was a £4.1M increase in contingent consideration treated as remuneration and a large decrease in restructuring costs, counteracted by a £6.1M increase in other admin expenses due to the continued investment in the marketing businesses. Finally the group also made nearly £2M more than last year on disposals so that operating profit was £6.3M higher than last year at £13.5M. The pension interests broadly cancelled each other out which left loan interest as the main finance cost, which increased by £575K during the year. Tax charges were slightly higher which made the profit for the year £10.5M, a £6.1M growth when compared to the profit in 2013 with underlying profits before tax increasing by £4.2M to £29.4M.

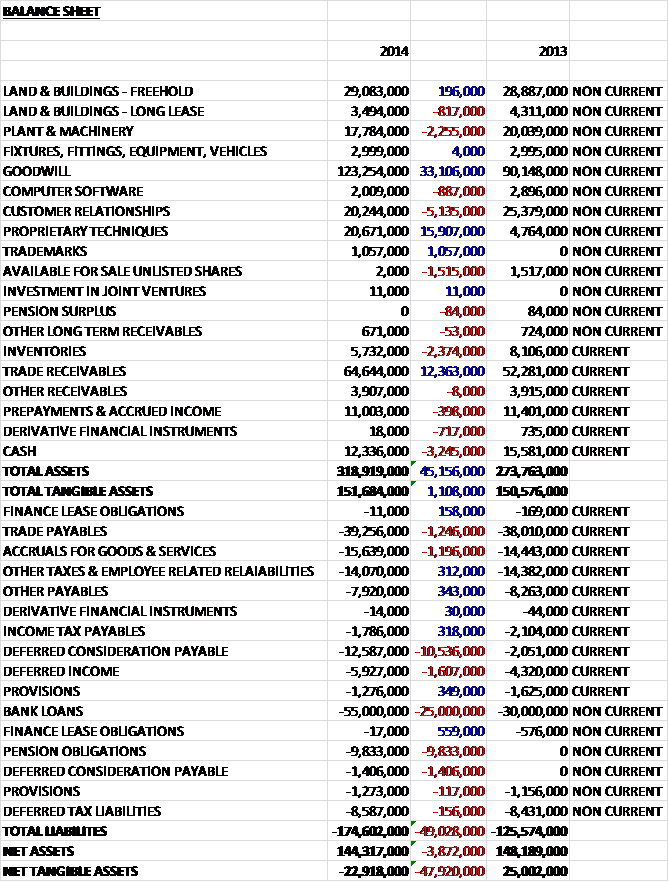

When compared to the end point of last year, total assets increased by £1.1M, driven by a £33.1M hike in the value of goodwill, a £15.9M growth in the value of “proprietary techniques” due to this year’s acquisitions, and a £12.4M increase in trade payables, somewhat offset by a £5.1M fall in customer relationships, a £3.2M decline in cash, a £2.4M fall in inventories and a £2.3M decline in plant and machinery. Liabilities also increased during the year due to a £25M growth in loans, a £10.5M increase in deferred consideration payable and a £9.8M growth in pension obligations. The end result is a massive £47.9M decline in net tangible assets to a negative £22.9M as the group’s “strength” in the balance sheet relates to intangibles – it does not look that strong to me, particularly when it is considered that there are also over £18M of operating lease obligations off the balance sheet. I read somewhere once that when a company makes a point of stating how strong its balance sheet is, it generally is rather weak and they are trying to make it sound stronger than it is. This certainly seems the case here as new CEO Matt Armitage makes a point of mentioning the “strength” of the balance sheet in his note to shareholders.

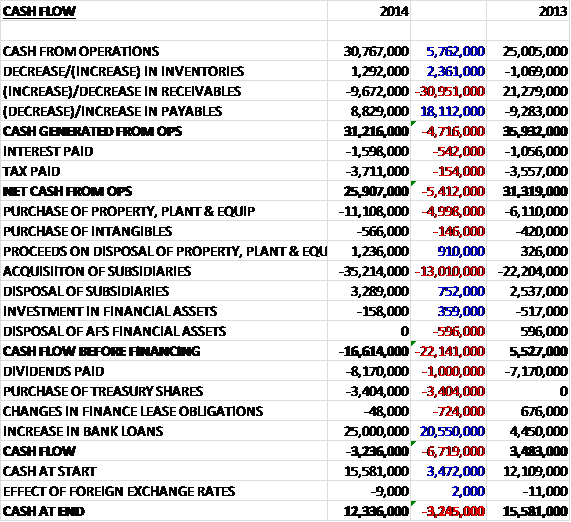

Before movements in working capital, cash profits were £30.8M, a £5.8M increase when compared to last year. Changes in working capital broadly cancelled each other out so that cash generated from operations was £31.2M, and after increases in interest and tax paid, the net cash from operations was some £5.4M higher at £25.9M. The group spent about £11.7M on capital expenditure which included new digital print equipment for Clays, SP Group and Service Graphics, and the purchase of the office occupied by Response One but the resulting free cash flow did not cover the net £32M spent on acquisitions so before financing, the cash outflow was £16.6M. The group then increased bank loans by £25M to cover this expense, plus the £8.2M of dividends paid and £3.4M spent on treasury shares. The resultant cash outflow was £3.2M to give a cash level of £12.3M by the year end. If we take out the acquisition, there is a decent amount of cash generated here but the group needed to increase borrowings to buy the businesses.

Underlying profits in Marketing Services were £4.1M higher than last year at £11.6M. Data Marketing revenues increased by £6.8M to £35.5M and represent the most important marketing division. Occam developed and launched an enterprise level data solution which was subsequently sold to new clients in the leisure, media and automotive sectors and the group sees these product led solutions as a key area of future growth. The growth within Response One was driven by a combination of new customer wins and existing client growth. They provided new data services for clients including Sainsbury, the Conservative Party, Royal Mail and HSBC. In addition, the two businesses collaborated on a successful joint pitch to Guide Dogs.

The Digital Marketing sector had a good year, increasing revenues by £20.4M to £28.1M as the group acquired Realise which slots into this segment. Amaze saw strong growth in demand for its e-commerce services with continued work on a global e-commerce solution for ASICS and new business wins including Waocol Eveden. The group is investing in this part of the business as it sees it as an area for future growth. Branded3 continued to perform well, completing a large project for Virgin Holidays and a European campaign for Norton and Symantec. The business also won a contract with car dealer Inchcape to deliver nine manufacturer websites focusing on the UK with the potential for wider global implementation. The three businesses in this segment, Amaze, Branded3 and Realise combined would rank as a top 10 digital business in the UK. The newly acquired Realise had previously built a digital marketing campaign around Standard Life’s Ryder Cup sponsorship, a full marketing strategy for Spurs football club and the delivery of brand refresh across Lloyds bank’s websites. They also won business from clients such as Universal Films, the BBC, Scot Rail and OVO Energy.

Consultancy Services revenue increased by £6.1M to £22.9M which included the acquisition of Health Hive. Incite recorded strong growth during the year due in part to the expansion into New York and Singapore which means that about 15% of the business’ overall revenue is generated overseas. They are planning on adding an office in Shanghai shortly that is due to start trading by the end of Q1. Pragma also saw strong demand for its services and during the year delivered successful engagements to support a number of retail businesses including Maplin and Bench as well as further developing its airports and commercial spaces offering. Field Marketing sales fell by £1.1M to £11.6M as the business suffered a difficult year with growing competitive pressure within the grocery retail market. It is investing in new data and technology capabilities to enhance the offering and a new management team is expected to add new impetus to the business.

Underlying profits in Print Services were flat when compared to last year at £19.3M. Marketing Print saw an £18.3M fall in revenues to £162.1M as increases in exhibitions, events and point of sale were offset by a £30.2M fall in print management sales due to the sale of a business in this segment. Discounting this effect, revenues at Marketing Print increased by 3% on a like for like basis with strong growth occurring in the second half of the year. SP group continued to provide POS services for retail clients such as Sainsbury, M&S and Holland & Barrett, adding New Look it its client list during the year. Service Graphics won exhibitions and events work from customers including the Rugby Football Union, Network Rail, Strada Restraurants, Wilko, Cotswold outdoor and Bentley, as well as delivering a significant amount of work for the Glasgow Commonwealth Games. The SIMS team continued to provide print management solutions to clients including Royal Mail, HSBC, the Conservative Party and Digital Mobile Spectrum’s consumer brand at800.

Books revenue fell by £3.4M to £67.4M, although market share was maintained. Clays is the market leader in UK monochrome book production services and continues to extend its range of value added services to the publishing market through digital and supply chain related investment. It has increased market share in the academic market by producing large format books, paperback, cased and short-run cased books as well as the distribution and print model it has built through print partnerships. It now works with a number of academic publishers including Pearson, Oxford University Press and Cambridge University Press. The business has also extended its services into the fast growing self-publishing sector.

On the 2nd March the group acquired Realise Holdings, a digital marketing business, for a total consideration of £29.9M which generated goodwill of £19.7M. Had the company been part of the group from the start of the year, it would have generated operating profits of £2M. On the 1st May the group acquired the Health Hive group for a total consideration of £26M which generated goodwill of £13.4M. It provides consulting and communications services to the healthcare and pharmaceuticals industries and more than half of the top 15 world pharmaceutical companies are clients. If the business had been acquired at the end of the year it would have contributed £2.7M of operating profit. The group also disposed of St Ives Bradford, a print management business. £3M of cash was received with another £775K of deferred consideration. Net assets of £2.2M were lost in the disposal so with £221K of selling costs, the group made a £1.3M profit on it. The strategy going forwards seems to include further acquisitions which operate in growth areas of the marketing proposition.

The Hive business seems quite interesting and has three main segments. Hive is a strategic consultancy and communications business which seeks to understand how patient’s relationships with their conditions affects the way they engage with doctors and the medicines prescribed to them which enables brand messaging to be aligned to their needs, resulting in more effective communication. Ebee creates bespoke strategies for effective communication on behalf of healthcare brands. It analyses user behaviour, accurately profiling how people interact with the entire digital landscape and has a database of user surveys that contains profiles for more than 1,200 doctors. Pollen is the newest division and uses specialised storytelling techniques to create narratives for clients to deliver scientific messages to targeted audience.

As can be seen above, there were quite a large number of non-recurring items. Restructuring items included £1.1M costs relating to restructuring activities in the head office, books, point of sale and events businesses. Redundancy and restructuring costs of £446K were recorded in the consultancy services and digital services businesses. An impairment charge of £824K and £738K of empty property costs were recorded in respect of properties held by head office. Profit on disposal of fixed assets included a £297K gain on the disposal of plant and machinery in the point of sale and print management businesses and a gain of £543K in respect of the sale of the building at the Edenbridge site. Finally, revenues of £3.1M and operating losses of £441K arose in respect of the Bradford site. Apparently the restructuring of the print division is now complete so hopefully that will signal a reduction in these exceptional items going forward.

Other non-underlying items included the amortisation of acquired intangibles relating to proprietary techniques and trademarks acquired with Realise and Hive as well as customer relationships, proprietary techniques and in house developed software acquired with data marketing, consultancy and field marketing businesses. An impairment charge of £1.2M relates to customer relationship assets where there has been a higher level of customer churn in the data marketing and field marketing businesses than expected at the date of acquisition. Costs associated with the acquisition of subsidiaries include £947K in respect of Realise and Hive. Contingent consideration payable to former owners of the acquisitions, who continue to be employed by the group, of £7.6M is required to be treated as remuneration.

During the year the group negotiated an increase to the revolving loan facility from £70M to £90M at a rate of LIBOR plus 2% to 2.5% depending on the ratio of the group’s net debt to EBITDA. The outstanding loans within this facility were £55M meaning that there was £35M left undrawn. There will have to be more negotiations shortly, however, as the facility expires at the end of October 2015. At the last pension valuation, there was a funding deficit of £36.7M and the group agreed to pay £167K per month until August 2019 in order to eliminate the shortfall. This means they are expected to pay contributions of £2.4M over the next year which is not an inconsiderable amount. The group is somewhat susceptible to exchange rate changes with a 100% LIBOR hike reducing profits by £308K. There is limited exchange rate risk but the group does supply some customers in Euros, USD, Yen and Singapore dollars.

Other risks include the unsuccessful integration of an acquisition, although the group has certainly has quite a bit of practice in this regard. The market decline in books due to the emergence of ebooks with the resulting reduced print run lengths is going to affect the printing sector and the book printing sector in particular and any deterioration in the UK economy could lead to lower marketing spend by the group’s clients which would clearly have an adverse effect on earnings. One customer accounts for £35M of group revenues, equivalent to about 11% of total sales so whilst the group is not totally dependent on this client, they would certainly feel its loss.

During the year CEO Patrick Martell informed the board of his intention to stand down. He was immediately succeeded by Matt Armitage, who was previously CFO and MD having been with the group since 2007. Matt is being succeeded as CFO by Brad Gray who joined the group in 1988 from Grant Thornton and was previously deputy finance director. Patrick has been with the group for 35 years and served as CEO since 2009 but the disruption should be minimised by the quick appointments of other old hands.

Going forward, with the more favourable economic climate and no immediate prospect of a slowdown, businesses are increasing their marketing spend which should improve revenues and profits for the group in the coming year. The strategy is to increase the underlying profit from the higher margin marketing segment by growing organically, including internationally with offices already in the US and Singapore, soon to be joined by a planned office in Shanghai, and selected acquisitions. So far this year trading has been in line with expectations with the marketing services segment benefiting from the UK economic recovery, from increasing marketing spend by their UK and international clients and from their own organic growth initiatives. Nothing is mentioned about the print segment but overall the board are confident that the group will make further progress this year.

At the current price the shares trade on an undemanding underlying P/E of 10.5, although including all the “one-off” costs the P/E stood at 22.5. On next year’s consensus forecast the P/E ratio look even cheaper at 9.9. After a 10% hike in the dividend pay-out, the shares yield 3.8%, increasing to 4.1% on the 2015 forecast. Net debt at the year-end stood at £42.7M, a large increase on the £15.2M level recorded this time last year.

Overall then, this has been quite a good year for the group. Underlying profits were up and the group is certainly generating decent cash levels at the operating level, although this is not enough to cover the cost of the acquisitions so the group has to rely on increased borrowings that need to be renegotiated this year. Operationally most of the divisions seem to be doing well but the field marketing business is struggling from the competition in the grocery sector and the books business could be in a state of terminal decline. The balance sheet does look rather weak when the large amount of intangibles are discounted, which makes me a little uneasy and that pension deficit is likely to cause a bit of a drag on results for years to come. It is pleasing that the restructuring seems to have been completed but I fully expect to see more “one-off” costs relating to further acquisitions and further impairments. When the economy is doing well and companies are spending a lot on marketing, I suspect St. Ives will thrive but in times of economic strife I would have thought the group will be particularly badly hit.

On the 16th December the group released a trading update covering the first five months or so of the year. The group made good progress and the underlying operating profit and margin were both ahead of the equivalent period of last year. Group revenue is running approximately 9% ahead of last year due to a combination of acquisition and organic growth. The marketing segment continued to grow and performed well, in line with expectations. Revenues were significantly ahead of the same period last year, driven primarily by acquisitions, and the operating margin also increased. The two most recent acquisitions are performing well having been successfully integrated into the group and investment has been made in additional headcount for organic growth.

The print services business continued to perform well despite challenging trading conditions, particularly in the retail sector. Print Services revenues were broadly flat reflecting the exit from the direct mail printing market in the prior year. Going forward, it looks like the group is looking to acquire further companies in the marketing services segment but no definite target has been declared. Overall, the new year has started well and I might look to take a position and perhaps keep a keen eye out for any potential economic slowdown.

The St. Ives chart seems rather interesting. Since October the share price seemed to have been retracing but towards the end of January the tables have turned and it seems to have broken out of the four month decline. If this recovery holds, now might be a good time to buy in – this is one I am keeping an eye on over the coming weeks.