RM supplies products, services and solutions to the UK and international education markets. There are three divisions: Resources, Results and Education. The Resources division comprises of two businesses – TTS and SpaceKraft. TTS is a provider of physical resources to UK schools with a leadership position in primary and early years age groups. SpaceKraft is a provider of resources and immersive environments to meet the specific requirements of learners with special education needs. The Results division supplies government ministries, exam boards and professional awarding organisations with technology and expertise to improve the assessment cycle, both in the UK and overseas and this includes the systems required to provide the league tables for English schools. It also provides exams and tests, onscreen testing, onscreen marking and the management and analysis of education data. RM Education provides technology based software and services designed for UK schools and other education establishment. Their products and services include the outsourcing, support and implementation services such as managed services, telephone support and consultancy services; network software, tools and infrastructure services; access to curriculum resources and school management solutions such as e-books; and the provision of broadband and e-safety solutions. They have now released their final results for the year ending 2014.

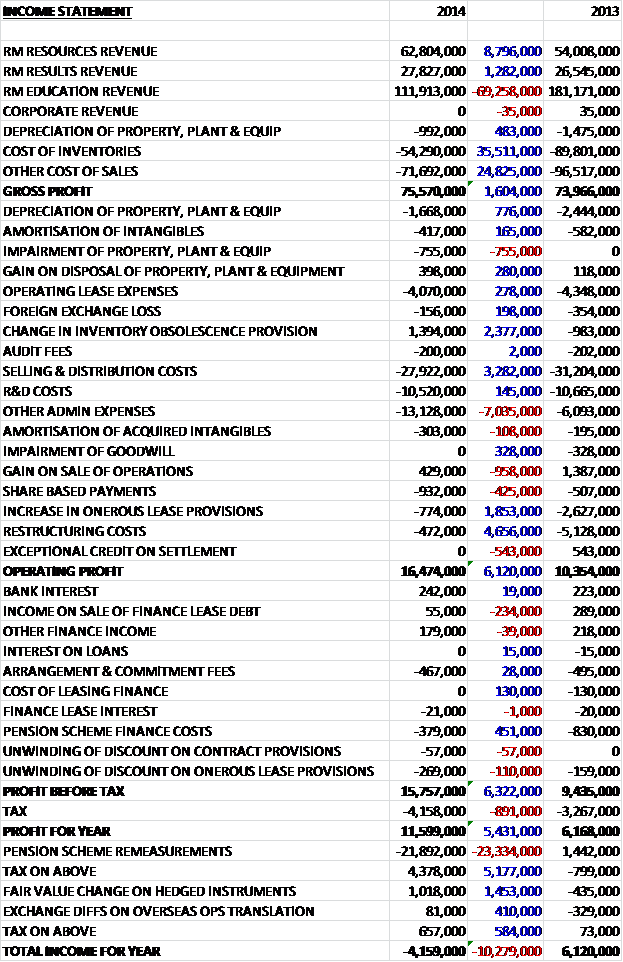

Revenues declined when compared to last year as an £8.8M growth in Resources sales and a £1.3M increase in Results revenue was more than offset by a £69.3M decline in Education revenue. Cost of sales also declined to give a gross profit some £1.6M above that of 2013. Other costs were also generally down as depreciation fell £776K, sales and distribution costs fell by £3.3M and there was a reversal of the inventory obsolescence provision. Other admin expenses did increase by £7M but there were declines in some one-off costs as onerous lease provisions fell by £1.9M and restructuring costs declined by £4.7M to give an operating profit of £16.5M, a £6.1M improvement when compared to last year. Finance costs also improved, driven by a £451K improvement in the pension scheme finance costs but tax increased to give a profit for the year some £5.4M higher than last year at £11.6M. The adjusted profit for the year, discounting the share based charges (not sure these should be taken out really), amortisation of acquired intangibles, restructuring and a few other items, was £13.7M, an increase of £2.2M when compared to last year.

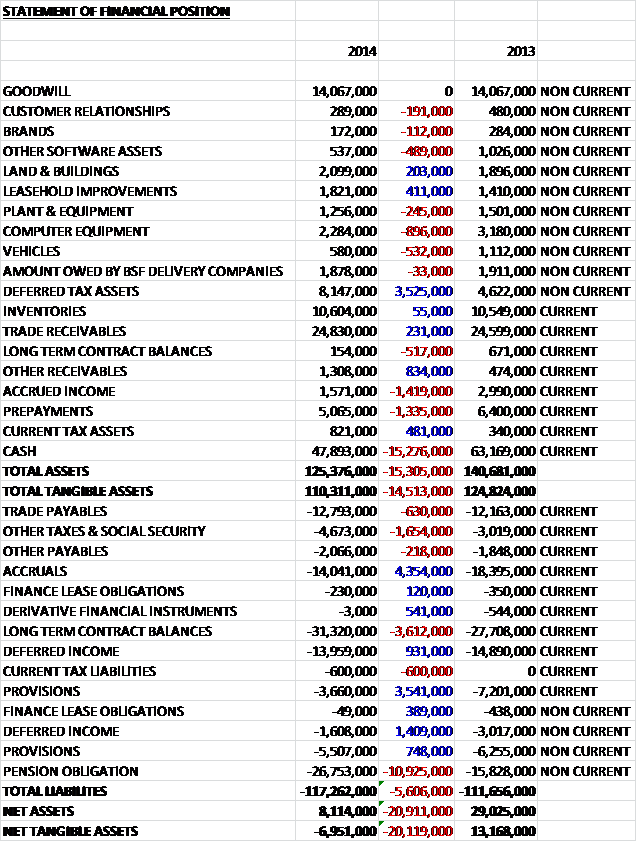

When compared to the end point of last year, total assets fell by £15.3M driven by a £15.3M fall in cash levels, a £1.4M decline in accrued income and a £1.3M fall in prepayments, partially offset by a £3.5M increase in deferred tax assets. Conversely liabilities increased due to a £10.9M increase in pension obligations, a £3.6M growth in long term contract balance payments and a £1.7M increase in other taxes and social security, somewhat offset by a £4.4M fall in accruals, a £4.3M decline in provisions, mainly relating to lower employee related restructuring provisions – the large amount of onerous lease provisions remain, and a £1.4M fall in deferred income to give a net tangible asset level some £20.1M worse than last time to a negative £7M so this is not a strong balance sheet at all which becomes even worse when the £13.8M worth of operating lease commitments off the balance sheet are taken into account.

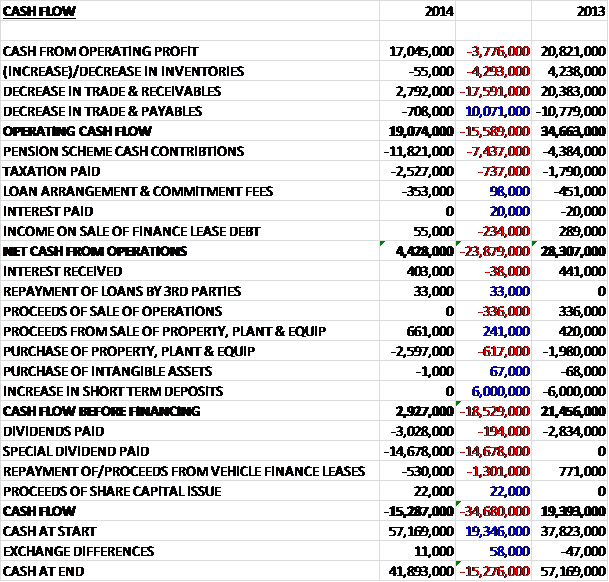

Before movements in working capital, cash profits fell by £3.8M to £17M, although a decrease in receivables meant that operational cash flow was £19.1M, a £15.6M decline when compared to last year due to the huge fall in receivables that happened that year. As the inventory level declines due to a run-down of long term contracts, it is expected that this situation will reverse going forward. The bulk of this cash was shunted into the pension scheme (£11.8M, although £8M was a one-off payment in an escrow account to reduce risk) and after tax took its toll, the net cash from operations was just £4.4M. There was not much in the way of capital expenditure, though, as a net £2M was spent on property, plant and equipment to give a free cash flow of £2.9M which was nearly enough to pay the regular dividends, although the £14.7M spent on the special dividend meant there was a cash outflow of £15.3M which left a still decent cash pile of £41.9M at the end of the year.

For the long term contracts, revenue is recognised proportionately to the stage of completion of the contract based on the fair value of goods and services provided to date, taking into account the sign-off of milestone delivery by customers. Where the cumulative value of goods and services provided exceeds amounts invoiced, the balance is included in receivables. Where amounts invoiced exceed the fair value of goods and services provided, the excess is first set off against long term contract balances and then included in amounts due to long term contract customers in payables.

Overall RM Resources had a good year as TTS generated strong organic growth based on market share gains and achieved an increase in margins whilst the SpaceKraft business is no longer loss making. RM Results secured new customers and delivered growth with improving markets and the reshaping of RM Education continued with the move away from manufacture and sale of hardware devices with more of a focus on services and software.

The Resources business had profits of £10.3M, an increase of £3.1M when compared to last year with an increase in profit margins from 13.3% to 16.4%. Investment is being made in direct marketing across online and traditional channels and in export business development to support growth. Revenue from the TTS UK direct marketing business increased by 19% to £46.2M with a particularly strong performance from products targeted at the new English primary school curriculum with the proportion of online sales showing further increases. TTS revenues from overseas resellers and international schools increased by 20% to £8.5M, driven by growth in Europe, the Middle East and the Americas. Revenue from sales to UK trade partners fell by 7% to £4.4M, though. The recent trend of declining sales at SpaceKraft was reversed with a growth of 11% to £3.7M which means that the business is no longer loss making.

The Results business had profits of £4.6M, an increase of £300K when compared to 2013 with margins increasing slightly from 16.1% to 16.7%. The business secured a new contract with the Caribbean Examinations Council during the year and the summer e-marketing pilot with education charity AQA was completed successfully with the group subsequently being appointed as one of two preferred suppliers for long term e-marketing contracts. Internationally the business is pursuing opportunities for the onscreen marking of paper based exams while in the UK, the exam and curricular changes introduced have reduced the number of exam retakes and a move away from modular courses to final exam based assessment will also impact the business. There is a long term trend from paper based to onscreen testing though the take-up for school based exams has been low. The educational data side of the business is dependent on one customer, the Department for Education. The National Pupil Database and RAISE online contracts, which included the capture and publishing of data for the school performance tables in England, were extended during the year following the agreement to stop work on the School Performance Data Programme.

The Education business had profits of £7.7M, a decline of £1.7M when compared to last year with profit margins increasing from 5.2% to 6.9% reflecting the continued shift away from hardware devices. The staff cost reductions were implemented ahead of plan and write downs in the value of remaining inventory were lower than expected. The services business saw a tough year as revenues declined by 29% to £61.2M with a reduction of new schools being built under the Building Schools for the Future programme. Digital Platforms and Content revenues increased by 4% to 7.6M with RM Integris sales increasing following good market share gains, including Oxfordshire won last year in a market that is dominated by one competitor with low levels of customer switching.

RM Unify was launched last year as a technology solution to allow customers easy access to the varied digital, cloud based, educational specific content and materials that are now available with revenue derived from annual school subscriptions and from fees from sales of third party applications. RM Books provides the first e-book solution designed for schools and now has about 16,000 titles available. The service is free to schools with the group taking a share of revenue from content sold through the system. E-book adoption in schools has been much slower than in the outside world and as such, revenue is still limited with the current focus on demonstrating the educational value added of the system.

Network solutions includes sales of network management tools and related hardware such as routers and wireless systems. Revenues collapsed by 45% to £8.6M as demand for established products reduced with lower school capital budgets. Sales of the new generation of network and device monitoring tools launched during the year have been disappointing and the focus is on ensuring that existing customers are on the latest version of the group’s software and on developing enhanced propositions which meet users changing requirements. The broadband and e-safety service provider is dominated by one large regional consortium which accounts for a large percentage of revenue, a relationship that is underpinned by a contract that runs until 2018, although volumes can be variable. Revenues decreased by 14% to £16.7M reflecting the end of some regional consortium contracts and the movement from private to public networks. Revenue from hardware fell by 67% to £17.8M reflecting the group’s exit of the PC devices business over the course of the year but revenue was significantly higher than planned with the costs of exit being much lower than expected, benefits that will not be repeated going forward. Third party partners Misco and Kelway have been appointed to provide hardware to customers where still required under existing contracts.

The group has a £30M revolving credit facility, of which £26.4M remains unallocated. The interest is payable at 2.5% above LIBOR and there is also a 1.2% fee payable on unutilised balance so given this, it is quite surprising this was entered into with the group having nearly £42M in cash. The shareholder roster looks pretty healthy with plenty of institutional names and Schroders taking the place of largest shareholder with more than 18% of the company’s equity. On the flip side, it does not look as though the directors have large investments in the company, however.

Of the £24.8M of trade receivables some £1.7M are overdue by more than 90 days which seems like quite a substantial amount to me, and a huge increase on the equivalent £400K last year. The group is potentially affected by a number of other risks. The majority of the group’s business is funded from local government sources so changes in political administration or policy priorities could result in a fall in education spending and global economic conditions may result in a reduction in budgets available for education spending. In addition, education practices and priorities could change which might mean that the group’s products and services no longer meet customer requirements and the company is reliant on some key contracts, the loss of which could materially affect earnings.

One major issue for the group is the pension scheme. The last valuation in 2012 revealed a deficit of £53.5M and it was agreed that the group would pay £4M per annum towards the deficit until 2013 and £3.6M until 2027. The next valuation is due in May which may result in further charges. A further contribution of £8M was made this year into an escrow account, £4.7M of which was paid to help fund a pension buy-in, the income from which will closely match payments to existing pensioners, eliminating inflation, interest rate and longevity risks associated with these pensioners. The cost of this insurance premium was £30.7M, paid with £26M from the pension assets and £4.7M from the escrow account which leaves £3.3M in the account for future risk reduction exercises. This only covers 13% of the scheme’s liabilities.

Going forward, it is expected that Results and Resources will continue to perform well and Education will take further steps towards building a platform for development. It is anticipated that cash generated from operations will be below operating profit in the coming years, reflecting the reversal of a favourable working capital position related to long term contracts and the utilisation of those onerous lease dilapidation provisions.

At the current price the shares trade on an inexpensive P/E ratio of 10.8 which falls to an even cheaper looking 9.5 on Numis’ 2015 forecast. After a 21% increase in the dividend, the shares have a yield of 2.8%, rising to 3.4% on next year’s forecast. It has been stated that the board will adopt a progressive dividend policy towards a more appropriate level of cover.

Overall then this is a set of results reflecting the transition of the group. Profits were up but net assets were down, mainly as a result of increased pension liabilities which seem to be a real drag on results with the group already paying £3.6M a year towards the deficit for the next 12 years and potentially more when it gets revalued in May. Despite these pension payments and the one-off escrow pension costs, the group had a decent free cash position, enough to mostly cover the normal dividends but a reversal in the working capital position flagged up for next year may put some pressure on this. Operationally the resources business is doing well but the education business, which is still a large contributor to the bottom line, is struggling with less schools being built under the schools for the future programme and management guiding for a lower profit from the division next year. The group is clearly susceptible to education spending political change so the upcoming election may be cause for uncertainty. Valuation wise, though, the shares seem to be very cheap, with a very low forward P/E ratio despite the cash pile and they offer a decent dividend yield too. I may look to buy the shares at an opportune time.

After a decent rise, the shares have been treading water for the last year or so and with the price dropping below both the 50 day and 200 day moving averages, now does not seem to be the time to buy the shares so I will keep a close watch instead.

On the 25th March the group released an AGM statement. Trading in the first quarter has been in line with expectations and cash deposits at the end of February stood at £40.5M. Following successful pilots, RM Results signed a three year contract to provide the education charity AQA with e-marketing services. The group has also sublet one of it’s buildings in Abingdon to the South Oxfordshire District Council. This building was surplus to requirements and should reduce the onerous lease provision by about £2.4M so this has to be a good move. Things seem to be ticking along fine here, not sure whether to buy yet – I will have a think!

On the 20th May the group announced that after five year CFO Iain McIntosh will be leaving the company, looking for a “new challenge”. He will be succeeded by Neil Martin who joins from Adecco where he is currently CFO for UK and Ireland at the Swiss HR company having been CFO at Spring when it was acquired by Adecco.