Paypoint is a service provider for consumer transactions through various distribution channels. There are a number of different activities that the group is involved in with retail networks being one of the most important. In the UK the network includes terminals in over 26,700 local shops including Co-Op, Spar, McColls, Costcutter, Sainsbury Local, Tesco Express, Asda, Londis and various independents. Some of the services provided includes energy meter prepayments, bill payments, benefit payments, mobile phone top-ups, transport tickets, TV licenses and cash withdrawals which are made available to customers by most leading utilities and a range of telecoms and other service companies. There are more than 8,350 terminals in local shops across Romania which enable to people to make bill payments, money transfers, road tax payments and mobile phone top-ups whilst in Ireland there are 500 terminals in shops and credit unions for mobile top-ups and bill payments. In the UK the network also includes 3,600 Link branded ATMs and 8,800 of the group’s terminals enables retailers to accept debit and credit cards.

The Collect+ service is a joint venture with Yodel that offers parcel drop-off and pick up services in 5,600 convenience stores so that customers can use the service to handle parcels from retailers including Amazon, eBay, ASOS, New Look, Boden, John Lewis, House of Fraser, M&S, Asda Direct and Very. In major cities across the UK, Canada, USA, France, Switzerland and Australia the group’s parking solutions enables people to pay for parking by mobile, increasingly through Paypoint’s own app. Electronic parking permits, automatic number plate recognition systems for car parks and penalty charge notices are also provided. The core online payments platform is linked to 16 major acquiring banks in the UK, Europe and North America. It delivers secure credit and debit card payments for over 5,100 online merchants including Hungry House, Moon Pig, WH Smith, London and Zurich insurance, Moneysupermarket.com and British Gas. Services include transaction gateway and a bureau service where they take the merchant’s credit risk and manage settlement for them. There are also a number of value added services such as Fraud Guard, a service that mitigates the risk of fraud in card not present transactions.

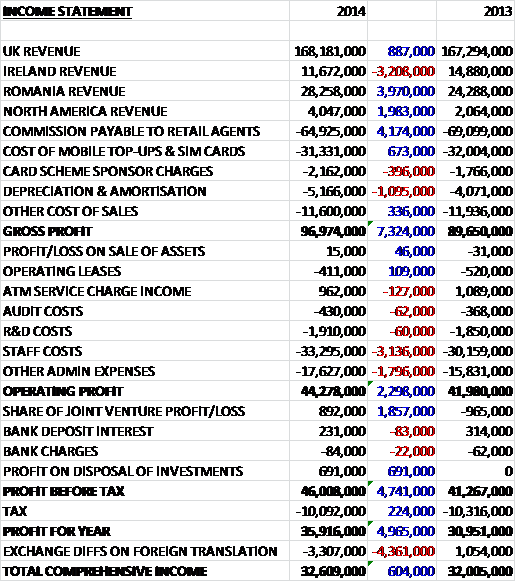

When compared to last year, revenues in general increased with Romanian sales in particular doing well, up by £4M and North American sales increasing by £2M, partially offset by a £3.2M decline in Irish revenues. Overall retail network revenue was up 1.1% and mobile & online revenue increased by 9.3%. The commission paid to retail agents fell by £4.2M due to lower mobile top-ups, whereas depreciation and amortisation increased by £1.1M to give a gross profit of £97M, a growth of £7.3M when compared to last year. Staff costs then increased, as did other admin expenses relating to the increasing cost of IT operations to support new products and the continued investment in mobile and online, a trend that is expected to continue next year, so that operating profit was just £2.3M higher than in 2013. The joint venture, Collect+, seems to be gaining traction, with a £1.9M swing into profit and the group also made a £691K profit on investment sales, relating to the disposal of the investment in OB10. The tax bill fell slightly so that profit for the year was £35.9M, an increase of £5M when compared to last year.

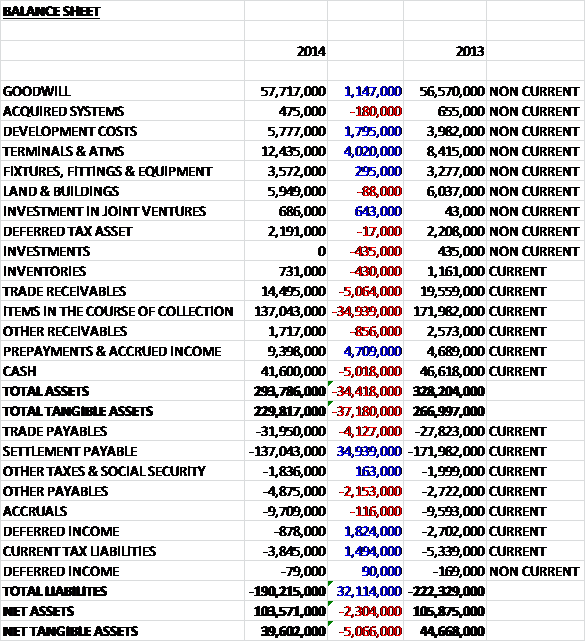

When compared to the end point of last year, total assets fell by £34.4M, driven by a £34.9M decline in items in the course of collection, a £5.1M fall in trade receivables and a £5M reduction in cash levels, partially offset by a £4.7M increase in prepayments and accrued income, a £4M growth in terminals and ATMs, a £1.8M increase in development costs and a £1.1M growth in goodwill. Liabilities also fell during the year due to a £35M fall in settlements payable (offsetting the items in the course of collection), a £1.8M decline in deferred income and a £1.5M fall in current tax liabilities, partially offset by a £4.1M increase in trade payables and a £2.2M growth in other payables. The end result is a net tangible asset level of £39.6M, a decline of £5.1M when compared to last year, which is a shame but the balance sheet looks pretty healthy nonetheless.

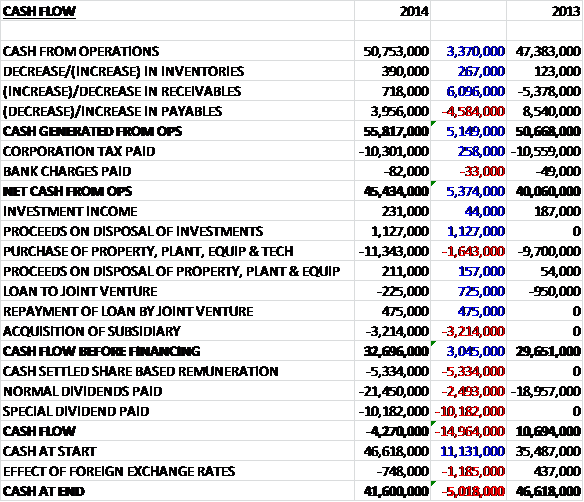

Before movements in working capital, cash profits increased by £3.4M to £50.8M. All working capital movements improved the cash level, in particular an increase in payables and there was a slightly lower tax bill to give a net cash generated from operations some £5.4M higher than last year at £45.4M. This cash comfortably covered an £11.3M investment in property, plant & equipment relating to IT expenditure, developments for new products, terminals, ATMs and prepaid energy and card readers, and a £3.2M acquisition of subsidiary which meant that after a £1.1M cash income from the disposal of an investment, the free cash flow was an impressive £32.7M. This comfortably covered the £21.5M spent on normal dividends and the £5.3M paid for the cash settlement of share based remuneration. The group then spent £10.2M on a special dividend which meant that there was a net cash outflow of £4.3M for the year to give a large cash pile of £41.6M at the year end. Aside from all that cash, there is also an undrawn five year £35M revolving loan facility so there really is plenty of headroom here.

Overall transactions increased from 739M to 767.5M with a 1.7% growth in retail networks and a 15.8% increase in mobile and online. Transaction values increased to £14.7BN with a 6% growth in retail payments and a 1.8% increase in mobile and online. In the Bill and General category, revenue was up 4% and net revenues increase by 7.2% to £54M. Transactions were ahead of last year due to a 54% growth in Romanian bill payment transactions as the group added clients including RCS and RDS, a pay TV and communications supplier that is one of the country’s biggest bill issuers, but the group blamed slow UK transactions on an extra week being in last year’s trading and warmer winter weather impacting energy spending. Simple Payment service transactions were lower than expected as a substantial proportion of the cheque payments that the system was designed to replace migrated to other payment methods. The strong growth in Romania was due to increasing market share and adding new clients.

Retail Services volumes increased across all products. ATM transactions increased by 21%, credit and debit transactions by 18%, SIM card sales by 5%, money transfer transactions by 59% and parcels by a massive 76% over the year. A higher average ATM transaction value drove an increased total transaction value in excess of the volume increases. A strong net revenue growth of 20% was driven by increases in credit and debit, parcels and income from broadband (enabling faster terminals) but was held back by a flat ATM performance in the first half of the year.

Top-up transactions decreased over the year as a result of the continued decline in mobile top-up volumes in the UK and Ireland of 17%. Other top-up transactions were also lower than last year and the fall in UK and Irish mobile transactions was only partially offset by a small increase in Romanian mobile top-ups where the impact of a larger network offset market decline. The average value of top-ups increased, however, which helped mitigate the volume drop-off. The joint venture, Collect+, saw transactions grow substantially with a richer mix of consumer parcels driving an increase in revenue and the integration of new merchants, growth in activity from existing clients and improvements in service levels for peak trading all helped the business to post its maiden profit. The ultimate goal is a lofty one, to provide a larger parcel network than the Post Office but operational gearing in the joint venture is not high so an increase in revenues will not necessarily lead to a huge increase in the bottom line due to greater costs.

In Mobile and Online, transactions increased by 16% with online transactions up 9% and mobile transactions up 44%. Transaction growth from online services was driven by the continued addition of large merchants and the organic growth of existing merchants. The group continued to add key mobile parking contracts with councils and parking authorities across the UK, North America and France, including the provision of services for 155,000 parking spaces in central Paris, as they provide a more convenient and cost effective method for collecting charges. The success in Paris follows other successful bids in Lambeth, Southwark, Chelmsford, Exeter, Seattle, Massachusetts and Dallas. The winning bid from NSL for Westminster’s parking does not include the Pay Point service, however, so this is a bit of a blow given the potential size of the contract and will delay profitability for mobile and online. Strong growth in mobile revenue was offset by a fall in online revenue due to the prior year impact of one-off software development income and a higher transaction growth for some larger merchants who benefit from lower pricing.

The company’s bill and general payments service has continued to be resilient as consumers’ discretion in expenditure is limited for essential services. Utility companies continue to install new prepay gas and electricity meters which will have a beneficial impact on transaction volumes and the online payment market as a whole continues to grow substantially. One major headwind, though, is the continued decline in mobile top-ups as mobile operators offer more airtime at lower costs and promote contracts ahead of prepay.

During the year the group acquired Adaptis Solutions Ltd, a business that specialises in providing a range of parking services including electronic parking permits, automatic number plate recognition systems for car parks and penalty charge notices. An initial consideration of £3.4M was paid in cash with the potential for £1.35M in deferred and contingent consideration, although the group does not think that £250K of this contingent consideration is likely to be paid. There were no net assets acquired and the acquisition generated goodwill of £3.8M. Adaptis contributed £93K to revenues and a loss of £88K to profit before tax for the period after acquisition and had the acquisition been completed on the first day of the year, it would have contributed £700K to revenues and a loss of £400K.

So far during the current year, trading is in line with expectations. The retail networks in the UK and Romania should continue to deliver profitable growth from the strong client base and the group will continue to invest in network expansion and new services to improve the quality of these networks. The group are looking at the possibility of further international expansion after the success of Romania. It was announced that senior independent director, Andrew Robb will retire at the AGM alongside chairman David Newlands, having been in the position for 16 years with Warren Tucker taking over as his successor. The shareholder base of the group looks fairly healthy with the majority of shares being held by various institutional investors with Invesco making up the largest one with 23% of the company. Some of the directors are also well invested with the CEO owning nearly 3% of the shares.

At the current share price the shares trade on a P/E ratio of 15.8 which falls to 14.8 on next year’s forecast. After an 18% increase in the dividend paid (excluding special dividends), the shares yield a decent 4.2% at the current share price, increasing to 4.5% on next year’s forecast. There was no debt so net cash stood at £41.6M compared to £46.6M last year. Some £6.5M of this cash is client cash and £13.5M is located in Romania.

Overall then, this is a solid update. Whilst profits were up, net tangible assets fell due to declining receivables and cash, no doubt attributable to the special dividend paid. The balance sheet remains strong and there is a good amount of free cash flow generated, easily enough to pay the normal dividends. Operationally, Romanian bill payments seem to be doing well but they slowed in the UK as cheque payments migrated to other methods. There were strong retail services with credit and debit transactions and money transfers doing well. The performance of the mobile top-up business was not so good and the trend for continued shifts towards contracts over prepay means that this is likely to continue in the future. Mobile payments seem to be doing well and the car parking angle seems like it has some decent potential, despite the Westminster parking contract blow. Finally, the joint venture with Yodel seems to be gaining traction and having used the service myself, I found it very convenient.

The shares are not that expensive on a P/E basis and the dividend is decent whilst many of the group’s markets seem to be growing, mobile top-ups notwithstanding.