Havelock Europa has now released its preliminary results for the year ending 2014.

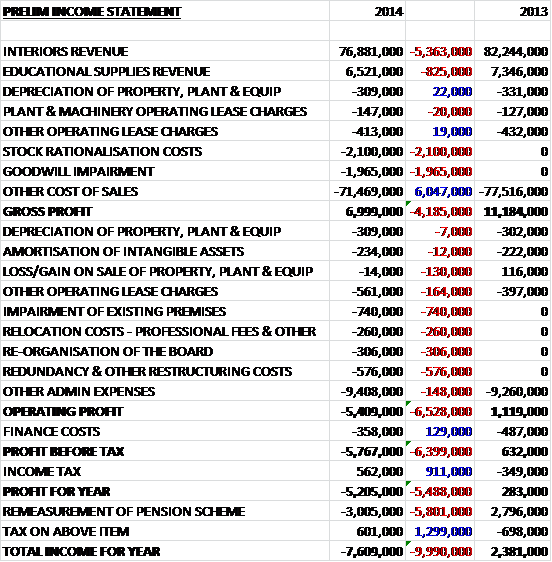

When compared to last year, revenues declined considerably with interiors sales down by £5.4M and education supplies revenue falling by £825K. Underlying cost of sales fell by a similar amount but we see a £2.1M stock rationalisation cost and a £2M goodwill impairment impacting results to give a gross profit some £4.2M lower than in 2013. We then see various admin costs increasing with several one-off costs here too including a £740K impairment of premises and a £576K charge relating to restructuring and redundancy. There was some respite with a small reduction in finance costs and there was an income tax rebate (the group does not expect to be in a tax paying position for a significant period of time) to give a loss for the year of £5.2M, a £5.5M reversal on last year.

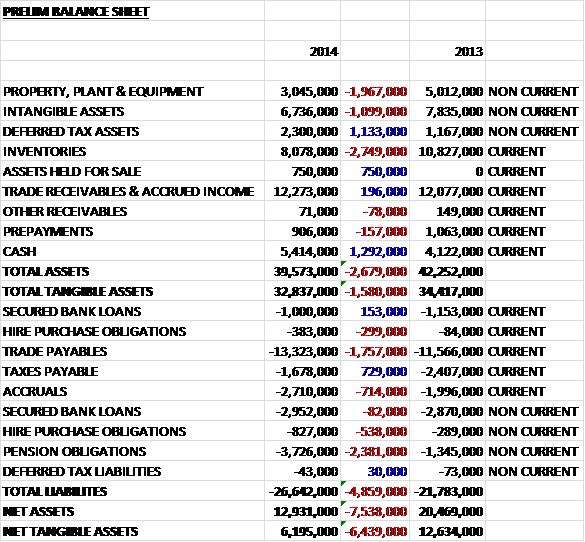

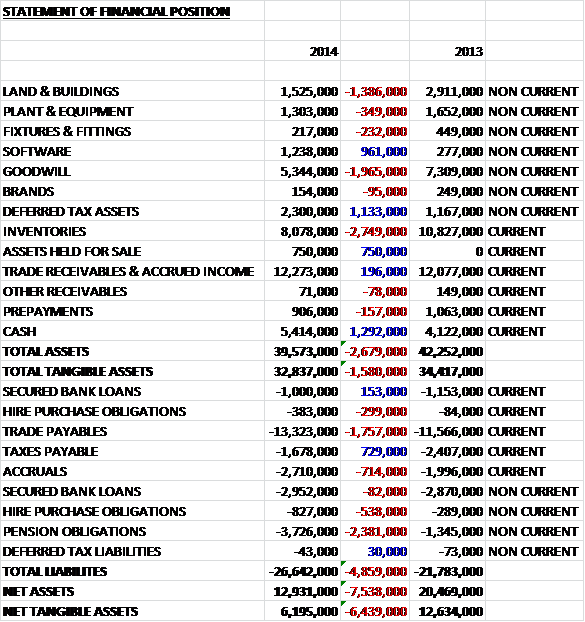

Total assets fell by £2.7M when compared to 2013, driven by a £2.7M decline in inventories, a £2M fall in property plant & equipment and a £1.1M fall in the value of intangible assets, partially offset by a £1.3M increase in cash levels and a £1.1M growth in deferred tax assets. Liabilities increased during the year with a £2.4M increase in pension obligations, a £1.8M growth in trade payables and a £714K increase in accruals, only being partially offset by a £729K reduction in taxes payable. The end result is a net tangible asset base that more than halved to £6.2M, a disappointing performance.

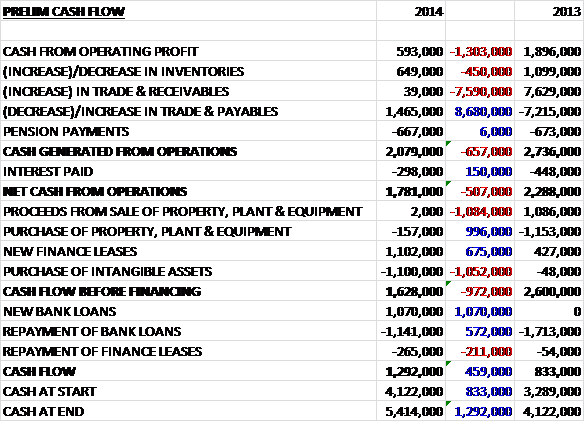

Before movements in working capital, cash profits fell by £1.3M to just £593K before a large increase in payables and a smaller interest cost meant that net cash from operations was £1.8M, a fall of £507K when compares to last year. There was very little in the way of capital expenditure and the purchase of intangible assets, relating to the new ERP system was paid for with new finance leases (which are now fully drawn). Even if we discount the finance leases, we still get a positive free cash flow of £500K. After the different financing operations where finance leases increased and other loans remained broadly similar, the group posted a £1.3M cash inflow, although this is flattered by the increase in payables that suggests the group is delaying payment to conserve cash flow.

The interiors business posted an operating loss of £1.3M, a negative swing of £3.4M when compared to last year as both Financial Services and Education showed a reduction in activity. In Retail the group had a strong year with the development of an Eastern European supply chain helping to complement the existing capabilities in China and the UK. During the next year the group aim to develop the new customer relationships established with a number of major retailers into significant sales. Within Financial Services, a number of the group’s customers are evaluating their offering which has led to reduced opportunities from their estates, although this was mitigated somewhat by the new three year framework contract with the Post Office.

The recovery in Education forecasted for 2015 has begun to start and management expect to benefit from this throughout the new year and Healthcare, underpinned by two major orders secured during the year, is expected to start delivering significant sales in 2015. The increase in international sales was achieved by the continued development of the relationship with a major Australian retailer and by partnering with a number of established UK customers’ overseas operations. The design process of the ERP system is complete and the build phase has commenced with the system remaining on course to be implemented during Q4 2015

The Educational Supplies business posted a loss of £2.6M, compared to a £258K profit recorded last year. The Teacherboard business had a challenging year with reduced opportunities in universities, schools and interiors with the fall in sales also reflecting the withdrawal from the sound, light and seating business at the end of October. The group continues to develop its web-based sales offering and good progress was made against this at least, during the year.

The sale of the Dalgety Bay premises and lease of the new premesis in Kirkcaldy was completed with Fife council towards the start of April 2015 and the head office relocation is on plan for the start of May. The £700K of proceeds from the4 sale will be reinvested in fitting out the new head office.

As can be seen, there were a number of one-off costs to affect the group this year. There was a £750K impairment charge relating to writing down the carrying value of the Dalgety Bay site that was sold. There was a £2.1M provision against the carrying value of surplus stock which was disposed of after rationalising the stock holding policy so that they carried less stock. It is a shame that this stock could not have been sold and it seems that this forced disposal could be due to the sale of their previous facility. An impairment of £2M was recognised against the carrying amount of goodwill in relation to Teacherboards ltd, there was a £306K charge relating to compensation for loss of office and fees related to recruitment of a new finance director and £576K of redundancy costs and other costs incurred in the restructuring of the business.

One area of brightness is international sales, which exceeded the board’s target of being 10% of group revenue with a new target of 15% being set. Healthcare revenue is currently small but this is another area of growth and in the near term, this is planned to grow to 5%. Financial Services is expected to become more challenging and after accounting for 43% of revenues in 2013, this is expected to fall to below 30% in 2015 but Education is expected to rebound strongly over the next two years with the group working hard to try and make this improvement sustainable in the long term.

Going forward the Financial Services and Retail markets are expected to be challenging but the opening order book of £25M against the £14M at this time last year looks good and the head office move along with the ERP system should bring significant benefits to the group. The board expects that the upturn in the Education sector will more than offset the decline in the Financial Services sector but the continued reliance on second half orders means that visibility for the whole year remains difficult. Trading at the start of the year, however, has been in line with expectations.

After the end of the year, the group agreed a new £5M overdraft facility that should offer some much needed headroom. Unsurprisingly given the performance there is no dividend this year and the lack of profit makes valuation on a P/E basis rather pointless which is exacerbated by the fact that I cannot find any analyst predictions for future. The group is in a net cash position of £200K compared to net debt of £300K last year.

Overall then this is certainly a disappointing update but one that was largely expected. The loss for the year did not make good reading but it seems this is mainly down to one-off costs with the £2.1M provision for surplus stock being particularly disappointing. The cash generation was not too bad with a positive free cash flow recorded despite the ERP investment but this is flattered by favourable working capital movements, in particular increased payables. It is the balance sheet where the group has felt most of the pain, though, with net assets more than halving due to the stock write-off, impairments against the previous office, an increased pension deficit and higher payables. It does seem as though, the board may have “kitchen sinked” the bad news. Operationally, the financial services decline has been difficult for Havelock but the education division is expected to improve and the group has a much better order book than this time last year which does offer a glimmer of hope that the worst may be over here – I will watch to see if a recovery might be underway.

After a steady decline, the chart seems to have levelled off. It is too early to call a recovery but this might be one to watch.

On the 5th May it was announced that the group appointed David Ritchie as CEO. He joined the company in 2013 as commercial manager having previously worked for Balfour Beatty and Wimpey. Additionally, it was announced that the move to the new head office has been completed as scheduled.

Havelock has now released its annual report which gives a bit more detail to the prelim results.

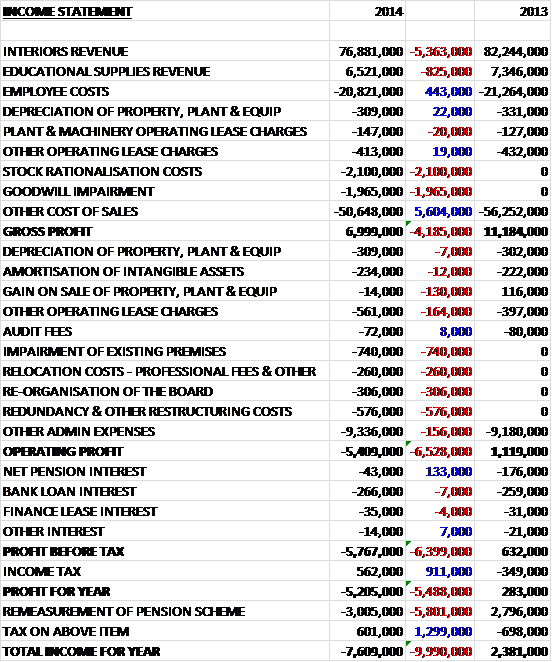

The only real things of interest is the extra detail for the finance costs which shows that the decline is due to a reduction in pension interest.

There is a bit more detail with regards to the assets. We can see that the decline in property, plant and equipment was across the board with a particularly large fall in the value of land and buildings. There is also a bit more detail with regards to the intangible asset mix, which is almost entirely goodwill. Finally, within receivables, there was a small increase in trade receivables offset by a decline in prepayments and other receivables. Offset against the £6.2M of net tangible assets, it is also worth noting that the group has some £2.2M in operating leases off the balance sheet.

There are also some examples of the projects that the group has undertaken that I like to read about as it give some more detail about what they have been up to. Some of these include a new M&S store in Hong Kong where the group was responsible for ordering and delivering every item required from M&S approved suppliers with 98% of the fixtures and fittings being made by Havelock, enough to fill 16 shipping containers. The group also worked to fit out a North Face store next to Wembley stadium and the fit out of a new concept between House of Fraser and Café Nero where the ground floor of the coffee shop in Cambridge features House of Fraser tablets where customers can shop whilst drinking their coffee. In the House of Fraser branded 1st floor, customers can view products and try them on. If the concept rolls out further, the group may benefit from further orders.

The group manufactured and delivered from 4,338 fixtures and 19,143 display ads for Boots’ Christmas range, along with nearly 3,000 photo kiosks and also fitted out store rebrands and new openings which makes the retailer an important customer of the group. Another project was Primark’s first store opening in the Netherlands with three further stores in Germany. The group acted as an installation contractor for 7 Tesco general merchandise stores along with the main general merchandise hub. In Australia, the group commenced on a project with a new client – Kmart. This year nine stores were refitted but there are a total of 190 across the group as a whole and in 2015 the group expects to undertake a growing amount of work for them.

During the year the group undertook the refurbishment of Lloyds Banking office in Fife which is used by more than 1,200 staff and a new branch in Manchester. Also in financial services, the group fitted out and office for Halifax in Edinburgh that employed “challenger digital” technology. In Education the group supplied, designed and installed the furniture, fittings and equipment for a new primary school in Burntisland and also in East Irvine which despite difficulties such as the flooding of the local river was delivered on time. The first phase of student accommodation blocks in Edinburgh was completed during the year where the group was responsible for the design and development of all bedroom furniture as well as fitting out the loose furnishings in the lounge, window blinds and bathroom accessories.

I find it quite interesting to have a look at the KPI’s to see what management are prioritising. Here we have revenues and profits split by segment, along with EPS as far as financial performance indicators are concerned along with waste to landfill and accidents per hour worked. Pretty standard stuff really, with the only improvement being probably the least important with landfill tonnes per £1 of revenue reducing.

So, a bit more of interest but nothing really to change the overall story here. On the same day, however, the group also announced the resignation of Andrew Burgess as non-executive director, apparently due to a new full time role overseas. He has indicated that he intends to retain is 19% shareholding in the company. This is interesting news, perhaps he sees that the turnaround work is done? As long as he is not selling his shares, I do not see this as a negative and I am tempted to take a little position here for any recovery potential after the comment about the order book at the full year results.

On the 5th June the group released an AGM statement. The head office move was completed during May to a location nearer the factory. Demand in Retail and Financial Services in currently subdued but the board are encouraged by good levels of activity in the Education and International Sectors. Forward visibility for the second half, particularly within the Retail sector, remains limited which makes a full year prediction difficult. The group is taking action to ensure that their cost structures remain competitive and are streamlining processes to deliver improved profit margins, aided by the new ERP system that goes live at the end of the year. So, there doesn’t really seem to be much to get excited about here.

On the 1st September the group announced a profit warning and some changes to the structure of the company. Following a review, a number of immediate changes have been announced that include reducing staffing levels by 10% and the sale of Teacherboards to Sundeala for £1.358M. The planned changes will reduce operational gearing and deliver annualised cost savings of £3M but is expected to reduce group operating profits in the short term. Last year Teacherboards made a profit of £160K and had net assets of £1.6M and before the completion of the sale, the group managed to get £678K cash out of the business in the form of a “pre-completion dividend”.

The consideration will be used to reduce net debt which stands at about £3.1M. Some £1.258M of the consideration was paid on completion and the balance of £100K will be paid on the finalisation of the completion accounts. In addition, the group announced that demand in the retail and financial services sector remains subdued and the results for the year as a whole will be materially below previous guidance.

This is clearly disappointing for holders, but I have to say that the profit warning has not really come as a shock. There does not seem to be any point in owning the shares at the moment as I can’t really see any coherent strategy for growth.