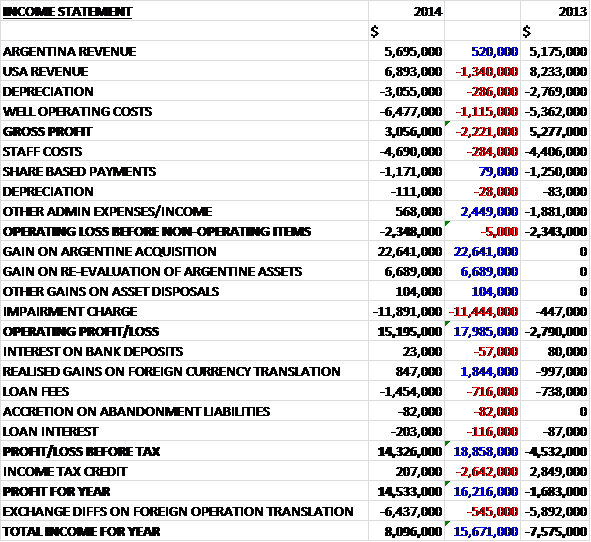

President Energy has now released its final results for the year ending 2014.  Overall revenues fell year on year as a $520K growth in Argentinean sales was more than offset by a $1.3M decline in USA revenue as the average oil price fell from $86 to $81. Well operating costs increased by $1.1M due to the 50% share of Puesto Guardian gained, work over costs on East Lake Verret and the ending of severance tax holidays on certain wells to give a gross profit some $2.2M lower than last year at $3.1M. Staff costs increased slightly but other admin costs were substantially lower because it included some $3.1M ($2.11M) of costs that were capitalised, to give an underlying operating loss flat on last year at $2.3M. There were some large non-underlying gains and losses, however, as a $22.6M gain on the Argentine acquisition relating to the remaining 50% interest acquired at the Puesto Guardian concession and a $6.7M gain on the re-evaluation of the Argentina assets following the revaluation after the Puesto Guardian acquisition, was partially offset by an $11.9M impairment charge, mainly relating to the Australia PEL82 license which was fully impaired during the year. The group also benefited from an $847K gain on foreign currency translation but loan fees were some $716K higher and the tax credit fell by $2.6M to give a profit for the year of $14.5M compared to a $1.7M loss in 2013.

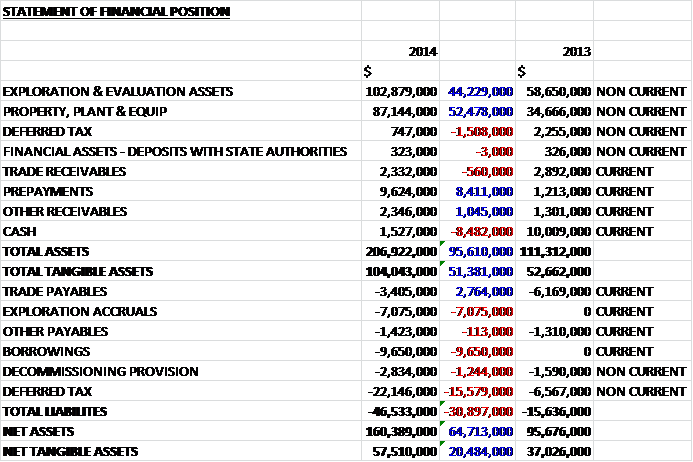

Overall revenues fell year on year as a $520K growth in Argentinean sales was more than offset by a $1.3M decline in USA revenue as the average oil price fell from $86 to $81. Well operating costs increased by $1.1M due to the 50% share of Puesto Guardian gained, work over costs on East Lake Verret and the ending of severance tax holidays on certain wells to give a gross profit some $2.2M lower than last year at $3.1M. Staff costs increased slightly but other admin costs were substantially lower because it included some $3.1M ($2.11M) of costs that were capitalised, to give an underlying operating loss flat on last year at $2.3M. There were some large non-underlying gains and losses, however, as a $22.6M gain on the Argentine acquisition relating to the remaining 50% interest acquired at the Puesto Guardian concession and a $6.7M gain on the re-evaluation of the Argentina assets following the revaluation after the Puesto Guardian acquisition, was partially offset by an $11.9M impairment charge, mainly relating to the Australia PEL82 license which was fully impaired during the year. The group also benefited from an $847K gain on foreign currency translation but loan fees were some $716K higher and the tax credit fell by $2.6M to give a profit for the year of $14.5M compared to a $1.7M loss in 2013.  When compared to the end point of last year, total assets increased by $95.6M, driven by a $52.5M increase in property, plant & equipment; a $44.2M growth in exploration assets relating to expenditure on drilling activities at the Jacaranda and Lapacho wells in Paraguay and the acquisition of a further 5% of the Pirity concession; an $8.4M growth in prepayments and a $1M increase in other receivables, partially offset by an $8.5M decline in cash levels and a $1.5M fall in deferred tax assets. Liabilities also increased with a $15.6M increase in deferred tax liabilities due to the profit made on the Argentinian acquisition and the revaluation of the assets there (there are still plenty of unrecognised losses that are available for offset against future profits), a $9.7M growth in borrowings, a $7.1M increase in exploration accruals and a $1.2M growth in the decommissioning provision, partially counteracted by a $2.8M fall in trade payables to give a net tangible asset level of $57.5M, an increase of $20.5M when compared to 2013.

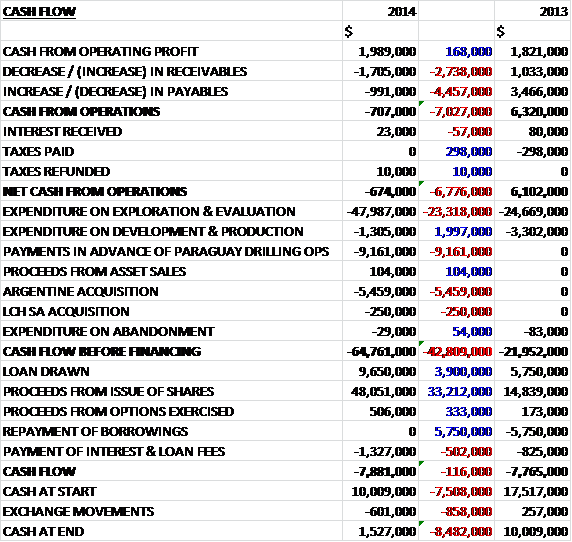

When compared to the end point of last year, total assets increased by $95.6M, driven by a $52.5M increase in property, plant & equipment; a $44.2M growth in exploration assets relating to expenditure on drilling activities at the Jacaranda and Lapacho wells in Paraguay and the acquisition of a further 5% of the Pirity concession; an $8.4M growth in prepayments and a $1M increase in other receivables, partially offset by an $8.5M decline in cash levels and a $1.5M fall in deferred tax assets. Liabilities also increased with a $15.6M increase in deferred tax liabilities due to the profit made on the Argentinian acquisition and the revaluation of the assets there (there are still plenty of unrecognised losses that are available for offset against future profits), a $9.7M growth in borrowings, a $7.1M increase in exploration accruals and a $1.2M growth in the decommissioning provision, partially counteracted by a $2.8M fall in trade payables to give a net tangible asset level of $57.5M, an increase of $20.5M when compared to 2013.  Before movements in working capital, cash profits increased by $68K before an increase in receivables and a decrease in payables, offset partially by a $298K fall in tax paid, meant that there was a $674K net cash outflow from operations as opposed to the $6.1M cash inflow last year. The group then spent $48M on exploration and evaluation; $1.3M on development and production and $5.5M on the Argentine acquisition with a payment of $9.2M in advance of the Paraguay drilling operations to give a cash outflow before financing of $64.8M. There was a share placing of $48.1M and new loans of $9.7M to give a cash outflow for the year as a whole of $7.9M that left a cash pile of just $1.5M at the year-end – clearly not enough to fund further operations. In Paraguay, the group currently owns a 64% working interest in the Pirity concession, a 10% working interest in the Demattei concession, with the right to earn up to 60% and a 40% working interest in the Hernandarias concession with the right to earn up to 80%. This combined acreage of 34,000 square km includes an extension of both the deeper Paleozoic and Silurian petroleum systems from which the gas condensate fields in Bolivia are formed along with the shallower Cretaceous petroleum system across the border in Argentina. During the year the group drilled the Jacaranda and Lapacho wells on the Pirity block which proved the existence of the Devonian and Silurian Paleozoic petroleum systems in the basin and made hydrocarbon discoveries in the Sara, Santa Rosa and Icla reservoices with a light oil discovery in the Icla interval (covering 24m) and a gas condensate discovery below 4,060m in the Santa Rosa and Sara sands. Unfortunately there were problems with the well testing operations on both occasions so the group could not demonstrate commercial flow rates, which was a real blow. The majority of the Paleozoic prospectivity is in the Hernandarias concession where the Santa Rosa and Sara target intervals can be reached at much lower depths. The exploration programme in the Pirity basin is continuing with a 607km 2D seismic survey currently underway, the results of which are expected in mid-2015. The survey is focused on the Boqueron, Labon and Tuna leads which are thought to contain the Devonian and Silurian packages identified in the Jacaranda and Lapacho wells at a depth of between 2,000 and 3,000 metres. The operating loss in Argentina was $948K, an increase of $486K when compared to last year. Since acquiring full ownership of the Puesto Guardian concession, the group has carried out reprocessing of seismic and reservoir engineering analysis and as a result of this is now commencing with well work overs and with drilling of new production wells in a second phase. The increase in production will also benefit from a government announcement of a $3 per barrel increase to the barrel realisation price for each increased barrel produced over existing production. The group has also commenced the farm out of a deep Paleozoic gas prospect at the Martinez del Tineo field in the Puesto Guardian concession which is assessed to contain unrisked recoverable prospective resources of 570 Bcf of gas and 14.5 mmbbls. The phase 2 programme is targeted to commence during the latter part of 2015 subject to finance being in place, which consists of up to 17 new wells targeting proved oil reserves. It is expected that some $30M of development finance will be required for the programme, at which point it should become self-funding. Additionally, an application is being made under new government legislation relating to unconventional hydrocarbons to obtain extended license terms over their concessions with tight reservoirs now qualifying for these extended license terms. If granted, the end date of the Puesto Guardian concession would become 2050 with the 3P oil reserves of 17.5 mmbls most likely increasing by a further 16.5 mmbls due to the transfer from contingent resources into reserves. It is hoped that that the application will be finalised before the end of 2015. The operating profit in the US was $2.5M, a fall of $1.5M when compared to 2013 as a falling oil price combined with increased operating costs due to some work overs increase production. The producing East White Lake and East Lake Verret fields continue to provide a cash flow base that covers the majority of the group’s overheads. Production fell from 236 bopd to 222 boepd but the Eagle Crest well at East Lake Verret was brought on stream at no cost to the company because it was farmed out in return for a full carry of costs, a 3% gross overriding royalty and a further 12% working interest. The well came on stream in 2014 with payout expected to occur by mid-2015. The company continues to believe there is some value in the PEL 82 license in Australia where 250 Bcf of conventional prospective resources and unconventional prospective resources of between 460 Bcf to 1.98 Tcf have been identified. Discussions with potential farm in partners have been placed on hold, however, while the South Australia state conducts a review into unconventional drilling activity. An application has been made to extend the license from September 2015 for a potential further year. Due to the hiatus, the group has impaired $11.5M of intangible assets at the license. A the year end the cash position stood at $1.5M and a further $14M was raised after the year end to fund the acquisition of new seismic lines on the Hernandarias concession in Paraguay and an initial workover programme in Argentina. During the year, discussions with potential farm-in partners for the PEL82 license in Australia were placed on hold while the South Australian state conducts a review into unconventional drilling activity. An application has been made to extend the license up to September 2016 but in view of the current hiatus, the group has impaired the $11.5M of intangible asset value related to the concession. Apparently management do see value in there but I suppose the favourable Argentinian acquisition which enabled the group to revalue the current asset there with an increase of $12.9M, allows the group to conceal the impairment somewhat and it is probably the sensible thing to do to protect against a possible impairment in the future. There are quite a lot of share options outstanding and over the past year they have been issued at the rather generous exercise price of 1p which is a trend that I find rather dubious. The good side is that these options will only be exercised if the share price hits 80p, so this is quite an upside from the 13p-ish that the shares are languishing at, so perhaps the directors would deserve their pay day if this is the case. During the year, the group acquired the remaining 50% interest in the Puesto Guardian concession in Argentina which gives them complete ownership and operational control. The group spent $5.5M in cash, $247K in deferred consideration and waived a loan of $1.6M in order to acquire assets worth $22.6M. Taken at face value, this really is an excellent acquisition with a huge amount of assets acquired for really very little (an incredible $1.04 per 2P barrel). During the year, the extra 50% acquired contributed a cash operating profit of $200K on revenues of $1.6M and had it been acquired at the start of the year, it would have contributed some $1.2M in cash operating profits – excellent stuff! In addition, a further 5% was acquired in the Pirity concessions due to the acquisition of the Paraguayan company LCH for $7.1M At the end of the year, the group was committed to funding a three year exploration programme on each of the Matorras and Ocultar license areas surrounding Puesto Guardian in Argentina. There is a seismic re-processing and new seismic acquisition commitments of $2M each with a drill or drop decision after three years. In Paraguay, the group has entered into farm in agreements to spend a further $32M on the Demattei concession to earn the remaining 50% working interest and a further $15.4M on the Hernandarias concession to earn the remaining 40% working interest. The KPIs all involve production and costs at the two producing countries with production in Argentina increasing (only due to the 50% Puesto Guardian acquisition, gross production fell) but falling in USA. Operating costs have increased across both territories and now stand at $22.9 per boe in the US and $61.8 per boe in Argentina. Finally, there is one financial KPI which is cash balances which fell during the year. After the end of the balance sheet date, there have been a number of significant events. Due to the lower oil price environment, the group is looking to reduce its overhead cost base, hence the depart in January of CEO John Hamilton, COO Richard Hubbard and non-exec director Michael Cochran with Peter Levine becoming chairman and CEO with Miles Biggins assuming the role of COO. Alistair Burt MP joined in February as a non-executive director. In March, the company placed nearly 30M shares at 12.5p per share with a further 43M then added at 12.5p per share with attached warrant that are exercisable at 18.75p per share during a three year period. A total of $14M was raised in the placing to fund an acquisition of new seismic lines on the Hernandarias concession in Paraguay and an initial workover programme in Argentina. The existing $15M loan facility was extended to the end of 2016 with a company owned by largest shareholder, CEO and Chairman Peter Levine. This involved loan fees of $1.5M being paid to the company, which seems as though it could be a potential conflict of interest. Going forward, not-withstanding the current oil price environment, the board are confident that the group will progress this year in Paraguay and Argentina. The first priority is the focus on exploration and production whilst maintaining cost control. On the 14th May it was announced that Alistair Burt MP has resigned from the board. He didn’t last long but after the election, he has become a minister of state so I guess that is fair enough. On the 16th May it was announced that CEO, Chairman and largest shareholder Peter Levine had upped his holding even further with the purchase of 2,350,000 shares at a value of £276,125 which is a good vote of confidence. Overall then, this has been an eventful year for Presidents. Revenues have fallen due to the lower oil price environment but operating losses were flat as increased operating costs were more than offset by the capitalisation of more admin costs. The group did achieve a profit, however, due to the excellent Puesto Guardian acquisition which is also the reason for the increase in net tangible assets. Cash profits actually increased by detrimental movements in working capital meant that there was a cash outflow from operations and the year end cash position was down to $1.5M with a further $14M raised in a share placing post year-end. The main news this year was the failure of the two Paraguay wells to find commercial hydrocarbons. The future of the company is based upon finding something in the country so hopefully at some point they do manage to make a valid test on an exploration well. The focus for the next year is in Argentina, however, and a further $30M will have to be found from somewhere to fund an extensive production well campaign in the country so there will be a further fund raising at some point. I do feel that at some point, these shares will be worth investing in. Now that the dispute with the partner in Paraguay has been resolved and some real upside potential in Argentina, that time may well be this year at some point, possibly after the next placing.

Before movements in working capital, cash profits increased by $68K before an increase in receivables and a decrease in payables, offset partially by a $298K fall in tax paid, meant that there was a $674K net cash outflow from operations as opposed to the $6.1M cash inflow last year. The group then spent $48M on exploration and evaluation; $1.3M on development and production and $5.5M on the Argentine acquisition with a payment of $9.2M in advance of the Paraguay drilling operations to give a cash outflow before financing of $64.8M. There was a share placing of $48.1M and new loans of $9.7M to give a cash outflow for the year as a whole of $7.9M that left a cash pile of just $1.5M at the year-end – clearly not enough to fund further operations. In Paraguay, the group currently owns a 64% working interest in the Pirity concession, a 10% working interest in the Demattei concession, with the right to earn up to 60% and a 40% working interest in the Hernandarias concession with the right to earn up to 80%. This combined acreage of 34,000 square km includes an extension of both the deeper Paleozoic and Silurian petroleum systems from which the gas condensate fields in Bolivia are formed along with the shallower Cretaceous petroleum system across the border in Argentina. During the year the group drilled the Jacaranda and Lapacho wells on the Pirity block which proved the existence of the Devonian and Silurian Paleozoic petroleum systems in the basin and made hydrocarbon discoveries in the Sara, Santa Rosa and Icla reservoices with a light oil discovery in the Icla interval (covering 24m) and a gas condensate discovery below 4,060m in the Santa Rosa and Sara sands. Unfortunately there were problems with the well testing operations on both occasions so the group could not demonstrate commercial flow rates, which was a real blow. The majority of the Paleozoic prospectivity is in the Hernandarias concession where the Santa Rosa and Sara target intervals can be reached at much lower depths. The exploration programme in the Pirity basin is continuing with a 607km 2D seismic survey currently underway, the results of which are expected in mid-2015. The survey is focused on the Boqueron, Labon and Tuna leads which are thought to contain the Devonian and Silurian packages identified in the Jacaranda and Lapacho wells at a depth of between 2,000 and 3,000 metres. The operating loss in Argentina was $948K, an increase of $486K when compared to last year. Since acquiring full ownership of the Puesto Guardian concession, the group has carried out reprocessing of seismic and reservoir engineering analysis and as a result of this is now commencing with well work overs and with drilling of new production wells in a second phase. The increase in production will also benefit from a government announcement of a $3 per barrel increase to the barrel realisation price for each increased barrel produced over existing production. The group has also commenced the farm out of a deep Paleozoic gas prospect at the Martinez del Tineo field in the Puesto Guardian concession which is assessed to contain unrisked recoverable prospective resources of 570 Bcf of gas and 14.5 mmbbls. The phase 2 programme is targeted to commence during the latter part of 2015 subject to finance being in place, which consists of up to 17 new wells targeting proved oil reserves. It is expected that some $30M of development finance will be required for the programme, at which point it should become self-funding. Additionally, an application is being made under new government legislation relating to unconventional hydrocarbons to obtain extended license terms over their concessions with tight reservoirs now qualifying for these extended license terms. If granted, the end date of the Puesto Guardian concession would become 2050 with the 3P oil reserves of 17.5 mmbls most likely increasing by a further 16.5 mmbls due to the transfer from contingent resources into reserves. It is hoped that that the application will be finalised before the end of 2015. The operating profit in the US was $2.5M, a fall of $1.5M when compared to 2013 as a falling oil price combined with increased operating costs due to some work overs increase production. The producing East White Lake and East Lake Verret fields continue to provide a cash flow base that covers the majority of the group’s overheads. Production fell from 236 bopd to 222 boepd but the Eagle Crest well at East Lake Verret was brought on stream at no cost to the company because it was farmed out in return for a full carry of costs, a 3% gross overriding royalty and a further 12% working interest. The well came on stream in 2014 with payout expected to occur by mid-2015. The company continues to believe there is some value in the PEL 82 license in Australia where 250 Bcf of conventional prospective resources and unconventional prospective resources of between 460 Bcf to 1.98 Tcf have been identified. Discussions with potential farm in partners have been placed on hold, however, while the South Australia state conducts a review into unconventional drilling activity. An application has been made to extend the license from September 2015 for a potential further year. Due to the hiatus, the group has impaired $11.5M of intangible assets at the license. A the year end the cash position stood at $1.5M and a further $14M was raised after the year end to fund the acquisition of new seismic lines on the Hernandarias concession in Paraguay and an initial workover programme in Argentina. During the year, discussions with potential farm-in partners for the PEL82 license in Australia were placed on hold while the South Australian state conducts a review into unconventional drilling activity. An application has been made to extend the license up to September 2016 but in view of the current hiatus, the group has impaired the $11.5M of intangible asset value related to the concession. Apparently management do see value in there but I suppose the favourable Argentinian acquisition which enabled the group to revalue the current asset there with an increase of $12.9M, allows the group to conceal the impairment somewhat and it is probably the sensible thing to do to protect against a possible impairment in the future. There are quite a lot of share options outstanding and over the past year they have been issued at the rather generous exercise price of 1p which is a trend that I find rather dubious. The good side is that these options will only be exercised if the share price hits 80p, so this is quite an upside from the 13p-ish that the shares are languishing at, so perhaps the directors would deserve their pay day if this is the case. During the year, the group acquired the remaining 50% interest in the Puesto Guardian concession in Argentina which gives them complete ownership and operational control. The group spent $5.5M in cash, $247K in deferred consideration and waived a loan of $1.6M in order to acquire assets worth $22.6M. Taken at face value, this really is an excellent acquisition with a huge amount of assets acquired for really very little (an incredible $1.04 per 2P barrel). During the year, the extra 50% acquired contributed a cash operating profit of $200K on revenues of $1.6M and had it been acquired at the start of the year, it would have contributed some $1.2M in cash operating profits – excellent stuff! In addition, a further 5% was acquired in the Pirity concessions due to the acquisition of the Paraguayan company LCH for $7.1M At the end of the year, the group was committed to funding a three year exploration programme on each of the Matorras and Ocultar license areas surrounding Puesto Guardian in Argentina. There is a seismic re-processing and new seismic acquisition commitments of $2M each with a drill or drop decision after three years. In Paraguay, the group has entered into farm in agreements to spend a further $32M on the Demattei concession to earn the remaining 50% working interest and a further $15.4M on the Hernandarias concession to earn the remaining 40% working interest. The KPIs all involve production and costs at the two producing countries with production in Argentina increasing (only due to the 50% Puesto Guardian acquisition, gross production fell) but falling in USA. Operating costs have increased across both territories and now stand at $22.9 per boe in the US and $61.8 per boe in Argentina. Finally, there is one financial KPI which is cash balances which fell during the year. After the end of the balance sheet date, there have been a number of significant events. Due to the lower oil price environment, the group is looking to reduce its overhead cost base, hence the depart in January of CEO John Hamilton, COO Richard Hubbard and non-exec director Michael Cochran with Peter Levine becoming chairman and CEO with Miles Biggins assuming the role of COO. Alistair Burt MP joined in February as a non-executive director. In March, the company placed nearly 30M shares at 12.5p per share with a further 43M then added at 12.5p per share with attached warrant that are exercisable at 18.75p per share during a three year period. A total of $14M was raised in the placing to fund an acquisition of new seismic lines on the Hernandarias concession in Paraguay and an initial workover programme in Argentina. The existing $15M loan facility was extended to the end of 2016 with a company owned by largest shareholder, CEO and Chairman Peter Levine. This involved loan fees of $1.5M being paid to the company, which seems as though it could be a potential conflict of interest. Going forward, not-withstanding the current oil price environment, the board are confident that the group will progress this year in Paraguay and Argentina. The first priority is the focus on exploration and production whilst maintaining cost control. On the 14th May it was announced that Alistair Burt MP has resigned from the board. He didn’t last long but after the election, he has become a minister of state so I guess that is fair enough. On the 16th May it was announced that CEO, Chairman and largest shareholder Peter Levine had upped his holding even further with the purchase of 2,350,000 shares at a value of £276,125 which is a good vote of confidence. Overall then, this has been an eventful year for Presidents. Revenues have fallen due to the lower oil price environment but operating losses were flat as increased operating costs were more than offset by the capitalisation of more admin costs. The group did achieve a profit, however, due to the excellent Puesto Guardian acquisition which is also the reason for the increase in net tangible assets. Cash profits actually increased by detrimental movements in working capital meant that there was a cash outflow from operations and the year end cash position was down to $1.5M with a further $14M raised in a share placing post year-end. The main news this year was the failure of the two Paraguay wells to find commercial hydrocarbons. The future of the company is based upon finding something in the country so hopefully at some point they do manage to make a valid test on an exploration well. The focus for the next year is in Argentina, however, and a further $30M will have to be found from somewhere to fund an extensive production well campaign in the country so there will be a further fund raising at some point. I do feel that at some point, these shares will be worth investing in. Now that the dispute with the partner in Paraguay has been resolved and some real upside potential in Argentina, that time may well be this year at some point, possibly after the next placing.  The shares remain considerably lower than at their height but there does seem to be a gradual recovery from the lows in mid April. On the 15th June the group released an update coverings its operations, mainly in Argentina. They have completed the four well work-over programme on the Puesto Guardian concession within budget and the four previously shut-in wells are in the clean up phase and currently flowing ahead of expectations at an aggregate of 190 bopd, a 92% increase in current field production which provides a significant return on the $1.6M investment made. Realisation prices remain at about $70 per barrel with the additional oil from the work overs generating a further $3 per barrel from government incentives which gives a net $50 per barrel return to the company after costs. Planning now continues for a new multi-well and work over programme on the concession and work is currently being carried out to upgrade the facilities there which comprise two separate main central processing units, one on each of the Dos Puntitas and Puesto Guardian fields capable of processing an aggregate 6500 bfpd. The farm out process for the deep gas prospect at the MDT field commenced last month and prelim discussions have taken place with several potentially interested parties. In Paraguay, infield seismic data acquisition is proceeding in line with plans and, subject to weather, should be completed by the end of July with prelim results available in Q3 2015. On the 13th July the group released an operations update. In Paraguay data acquisition of the 603km of 2D seismic on the Hernandarias block has been completed on time and on budget and the preliminary review of the first raw data processed in the field is apparently “cautiously encouraging”. Final analysis is expected to be available in about two months. In Argentina, the recent four workovers produced approximately 200 bopd of steady production and the next series of workovers are now being considered together with new wells in due course. Realised price for production in June was $71 per barrel with a similar amount expected in July. Current daily aggregate production from the county is running between 380 and 400 bopd. In Louisiana, the group has acquired net incremental production of about 100 boepd of which 45% is oil. In addition a further $12K per month of facilities fee income has been acquired. The total consideration paid for this extra production and fee income was $120K. The increased production includes higher effective working interests in one well in each of the two fields and more than offsets the decline rate incurred in the East White Lake field. A new production well is due to spud during the course of this months and targeted to come on stream by the end of August. Current production in Louisiana net to President before the new well is about 285 boepd.

The shares remain considerably lower than at their height but there does seem to be a gradual recovery from the lows in mid April. On the 15th June the group released an update coverings its operations, mainly in Argentina. They have completed the four well work-over programme on the Puesto Guardian concession within budget and the four previously shut-in wells are in the clean up phase and currently flowing ahead of expectations at an aggregate of 190 bopd, a 92% increase in current field production which provides a significant return on the $1.6M investment made. Realisation prices remain at about $70 per barrel with the additional oil from the work overs generating a further $3 per barrel from government incentives which gives a net $50 per barrel return to the company after costs. Planning now continues for a new multi-well and work over programme on the concession and work is currently being carried out to upgrade the facilities there which comprise two separate main central processing units, one on each of the Dos Puntitas and Puesto Guardian fields capable of processing an aggregate 6500 bfpd. The farm out process for the deep gas prospect at the MDT field commenced last month and prelim discussions have taken place with several potentially interested parties. In Paraguay, infield seismic data acquisition is proceeding in line with plans and, subject to weather, should be completed by the end of July with prelim results available in Q3 2015. On the 13th July the group released an operations update. In Paraguay data acquisition of the 603km of 2D seismic on the Hernandarias block has been completed on time and on budget and the preliminary review of the first raw data processed in the field is apparently “cautiously encouraging”. Final analysis is expected to be available in about two months. In Argentina, the recent four workovers produced approximately 200 bopd of steady production and the next series of workovers are now being considered together with new wells in due course. Realised price for production in June was $71 per barrel with a similar amount expected in July. Current daily aggregate production from the county is running between 380 and 400 bopd. In Louisiana, the group has acquired net incremental production of about 100 boepd of which 45% is oil. In addition a further $12K per month of facilities fee income has been acquired. The total consideration paid for this extra production and fee income was $120K. The increased production includes higher effective working interests in one well in each of the two fields and more than offsets the decline rate incurred in the East White Lake field. A new production well is due to spud during the course of this months and targeted to come on stream by the end of August. Current production in Louisiana net to President before the new well is about 285 boepd.

On the 14th September the group released an update relating to the Hernandarias block. Whilst final processing by the independent contractor is ongoing, the seismic is of excellent quality and it is already clear from the data that several drillable Paleozoic prospects, in line with the company’s pre-acquisition expectations, exist at 2,500 to 3,000 metres depth, being some 1,000 metres shallower than the Lapacho and Jacaranda wells drilled last year. In light of the importance of the results, management is carrying out careful analysis and review before announcing the full results together with prospective resource estimates.

On the 25th September the group released an update for the reserves and prospective resources in Argentina. In the Puesto Guardian area 1P Proved Oil Reserves increased by 21% to 11MMBls; the 2P Proved and Probable Reserves increased by 28% to 18.1MMBls; the 3P Proved, Probable and Possible oil Reserves increased by 32% to 23.1MMBls; and the NPV10 net present value of the 2PO oil reserves increased by 10% to $329M. This statement takes into account the new concession terms including the extension to 2050.

Previously the Martinez Del Tineo prospect was assessed at having unrisked recoverable prospective resources of just 570 Bcf of gas and 14.5MMbbls of condensate. As a result of recent technical studies, re-processing of all regional seismic and incorporation of recent knowledge from the Paraguay drills, these estimates have been updated. They now assess the unrisked recoverable prospective resource of 2.3Tcf of gas and 59MMBls of condensate with an overall chance of success of 25%. With the inclusion of the prospective resources in the neighbouring Matorras license, the aggregated unrisked recoverable prospective resource is 6.6Tcf of gas and 166MMBls of condensate.

Given Argentina has a ready gas market currently offering a gas price of $7.5 per MMBtu and the asset is onshore and easily accessible and the previous NPV value was $1.028BN at a gas price of $4 per MMBtu and a condensate price of $65/bbl, the current value must be rather tasty. The Martinez Del Tineo prospect can be explored by the deeper leg of a development well at the MDT field drilled to intersect and produce the shallower proven and probable oil reserves, thereby saving costs of a dedicated exploration well. This would also act as a test of concept for the Paleozoic prospective resources in the Matorras license which are dependent prospects. The group is continuing discussions with potential partners relating to this prospect and the above all looks rather good to me (although I have thought that before with this company).