E2V has now released its final results for the year ending 2015.

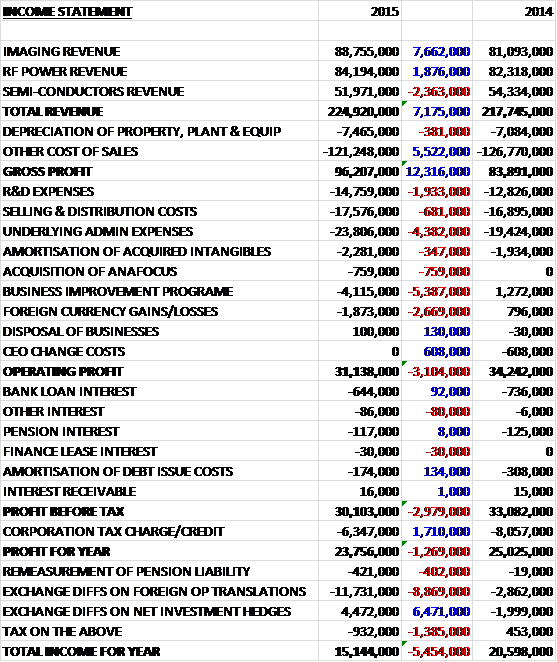

Overall, when compared to 2014, revenues increased as a £7.7M growth in imaging revenue and a £1.9M increase in RF Power revenue was partially offset by a £2.4M decline in semi-conductor sales. Cost of sales fell during the year to give a gross profit some £12.3M ahead of last year. We then see a £1.9M increase in R&D expenses and a £4.4M hike in underlying admin expenses relating to increased staff costs, IT investment and the costs of expansion in Asia and the US, before a £5.4M negative swing associated with the business improvement programme (after the last year saw credits relating to the release of provisions), and a £2.7M detrimental movement in foreign currency losses meant that operating profit was £3.1M lower than in 2014. Finance costs improved somewhat, mainly due to a fall in bank loan interest and lower amortisation of debt issue costs and tax was also some £1.7M lower, mainly due to a decline in deferred tax liabilities relating to origination and reversal of temporary differences, to give a profit for the year of £23.8M, a decline of £1.3M year on year.

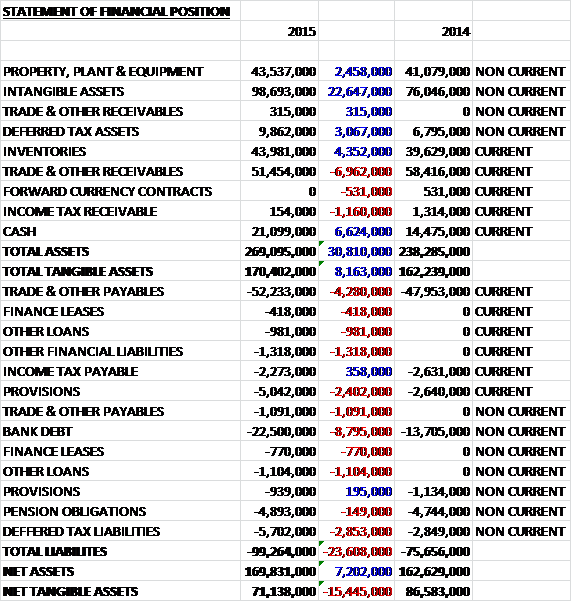

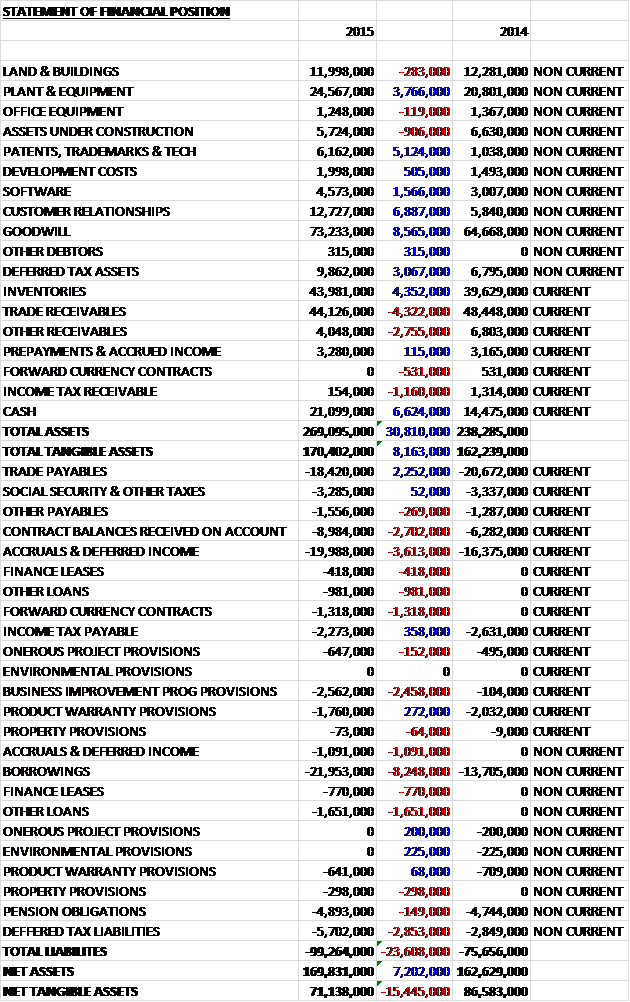

When compared to the end point of last year, total assets increased by £30.8M, driven by a £22.6M growth in intangible assets, a £6.6M increase in cash, a £4.4M increase in inventories and a £3.1M growth in deferred tax assets, partially offset by a £7M fall in receivables. We also see liabilities increase during the year due to an £8.8M increase in bank debt, a £4.3M growth in payables, a £2.9M increase in deferred tax liabilities and a £2.2M increase in provisions. The end result is a £15.4M fall in net tangible assets to £71.1M.

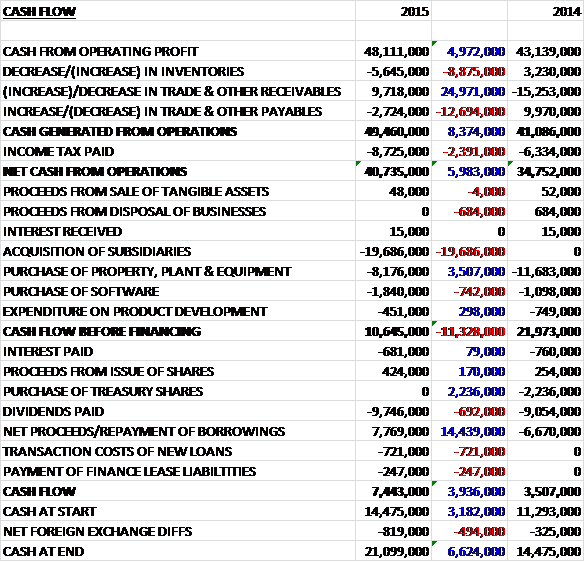

Before movements in working capital, cash profits increased by nearly £5M to £48.1M. A decline in receivables, reflecting good cash collection, was nearly completely offset by a fall in payables and an increase in inventories as the group increased levels to improve their responsiveness to customer requirements, and after an increased tax payment, the net cash from operations was some £6M higher at £40.7M. Impressively the group managed to pay for its capital expenditure needs, plus nearly £20M on an acquisition and still have £10.6M of free cash flow left. This just about covered the interest paid and dividends but the group still took out £7.8M of new borrowings which incurred £721K in costs to give a cash flow of £7.4M for the year and a cash pile of £21.1M.

The results represent a particularly strong Q4 with the benefit of the Anafocus acquisition and steady growth in the industrial vision, radiotherapy, commercial and industrial businesses. The space, scientific imaging and semiconductors businesses remained flat whilst revenues in RF Defence and thermal imaging fell. The order book at the end of the year looked good with orders for delivery within the year increasing by 14% to £146M with particularly good coverage in the Space and Industrial Vision businesses and full coverage from the Radiotherapy customers with an active pipeline of opportunities. The group really seem to have a focus on customers now, actively delivering what they value rather than what the group wants to achieve technically. The total order book increased by a more modest £7M to £191M.

Imaging is now arranged into two business streams – professional imaging and space. Professional imaging demand is driven by the increased use of sensors in industrial automation with growth driven by the improvement in industrial markets and recent product innovations such as the new CMOS based camera. Further growth is planned from new product introductions in 2016. Scientific imaging is expected to remain steady with the market highly concentrated with three major customers. In Space, governments increasingly seek to maintain independent observation capabilities and the expansion of climate change monitoring is driving growing demand for new observation satellite programmes.

The group is continuing to develop their CMOS based technology platform for Space, which is in part funded by a £3.8M award from the UK Regional Growth fund. During the year more than £40M of new orders were secured and key wins included the first phases of the Large Synoptic Survey Telescope contract in the US, a number of ESA contracts and new opportunities in Korea, China and Russia. Two major science projects have started including LSST and Plato for ESA with a potential combined total value of £50M. Within the Earth observation sector, £11M of orders were booked in the year. The group has invested in their Chelmsford facility to increase their wafer processing capability and expand the assembly area and characterisation lab and they will continue to invest in production facilities in the coming year with the reorganisation programme being delayed and inexplicably renamed project Sunrise.

The operating profit at the Imaging business fell by £4.9M to £7.3M with adjusted operating profit down by 17% to £9.3M despite revenue increasing by 9% to £88.7M. The revenue growth came from strong demand in automatic data collection, machine vision sensors and optical inspection CMOS cameras in Asia. Scientific imaging was steady reflecting end user demand remaining at similar levels to the year before. In Space, activity was sustained although the programmes are challenging and the group has had to commit more resources to improve delivery to customers. The thermal imaging business saw lower demand in core markets with sales significantly below that of last year.

The lower profits reflect a decline in margins due to delayed milestones in the Space programmes which lead to cost increases. The lower thermal imaging sales also led to declining margins and the cost base has been reduced accordingly. AnaFocus performed strongly, contributing ahead of expectations and R&D activities have been increased significantly to drive future growth, focusing on machine vision and space. The order book looks good, increasing by £29M to £90M reflecting key programmes in Space, including a £1M increase in the level of overdue orders along with growth coming from Industrial Vision and AnaFocus. The orders due in the next year were up £20M to £70M which underpins the expected revenue growth.

The group produces systems that deliver higher performance radio frequency power generation for healthcare, defence and industrial applications. The key growth drivers are the increasing incidence of Cancer worldwide, industrial growth and defence spending. In radiotherapy the group produces systems that deliver power at radio frequencies used for the generation of x-rays in the treatment of cancer where they are established as market leader with an incredible market share of 90% for the supply of magnetrons.

In Radiotherapy the group anticipates spares revenue will grow in line with the past expansion of the installed base over the last five to ten years with revenue growth anticipated to be driven by continued new build demand, which accounts for about a third of growth. There has been increasing demand in Asia, especially China with new equipment demand being dependent on healthcare spending. In defence, the key driver is the level of NATO spending and budgets across the NATO countries are currently constrained and the board does not see this changing any time soon so investment is being targeted at the growth business of radiotherapy. During the year the group finished a further phase of their development programme with Rio Tinto in their industrial processing systems business, covering the design and supply of large scale microwave and RF generators for use in products to demonstrate the improvement in the efficiency of metals recovery. Rio is now in the process of deciding whether to take the project onto the next stage of development.

The operating profit at the RF Power business grew by £1.4M to £18.4M with adjusted operating profit increasing by 21% to £19.4M and revenues increasing by £1.9M, driven by a strong growth in radiotherapy reflecting increased demand from the key OEM customers, along with good growth in the Commercial and Industrial markets, particularly marine. This was partially offset by weakness in Defence with slower than anticipated programme wins and lower activity levels in Industrial Processing Systems. The increase in profit also reflects improved operating effectiveness with good cost control and lower inventory write-offs. R&D activities were below that of last year, focusing primarily on radiotherapy applications. The order book at the end of the year was £20M lower than last year at £80M, reflecting the cycle of the multi-year radiotherapy contracts and a reduction in the defence order book. The order book for delivery in the next year was broadly flat at £58M reflecting a full year coverage for Radiotherapy and good coverage in Commercial and Industrial, partially offset by a decline in Defence.

In the semi-conductors sector, the board sees continued growth for high reliability products in civil aviation applications such as flight control computers, engine management systems and cockpit display systems. In addition, there is a growing demand for high reliability, radiation tolerant products tested for low earth orbit space applications including weather monitoring, earth observation and telecoms satellites. The growth in these sectors has offset delayed demand for defence programs associated with Typhoon, F-16, F-18 and the Joint Strike Fighter.

The division has made significant progress in the growing space market. They have been part of a NASA-led consortium to develop QML standards for non-hermetic space qualified products and following the publication of this standard, the group has now introduced a range of microprocessors based on a Freescale power PC platform which complement their own design space qualified ADC and DACs that form an integral part of their portfolio. They plan to introduce other QML qualified semiconductor products over the coming months. Recognising the opportunity for growth in North America, in December the group opened a new facility in Texas in order to be closer to customers.

During the year, the company saw a reduction in revenues related to the outsourced assembly and test services that they provide customers who lack the in-house capability, reflecting demand fluctuations in their customer’s end user markets. There has been an increased interest in high reliability microprocessors for space applications that require greater levels of on-board processing in the last two years. In addition, E2V continues to support their legacy products for sensor signal conditioning ASICs and ASSPs. They had previously decided to cease the R&D activities associated with these product lines and the revenue from them now reflects the anticipated decline.

The operating profit at the Semi-conductors business grew by £400K to £10.3M with adjusted operating profit increasing by under 1% to £11.9M while revenues fell by 4% to £52M. This decline in revenue reflects the fact that good growth from US based product lines, along with the business’ own design high speed data converters for space applications has been offset by lower demand for microprocessors and the anticipated decline in the legacy smart sensor business as those products approach the end of their lifecycle. The better performance with regard operating profit is due to improved product mix with growth in higher margin lines, along with good cost control. The order book fell by £3M to £20M reflecting the anticipated decline in the legacy smart sensor business along with lower demand for microprocessors, partially offset by improved order cover from the US. The order book for the next year declined by £1M to £18M.

The main R&D programmes currently include the next generation RF generating sub-systems for radiotherapy, sensors for industrial vision, the CMOS platform, process capability, coatings and CMOS for space along with the next generation semiconductor products.

During the year the group undertook restructuring of their central operations, RF Power and Imaging teams with an announcement to cease manufacturing in Beijing during H1 2016 and a consultation regarding the planned closure of the sales office in Bievres, France. A charge of £3.4M was recognised during the year, mainly relating to staff and onerous lease costs. The group is also undertaking a reorganisation of it Chelmsford facility which has incurred costs of £686K during the period.

During the year the group entered into a new revolving credit facility which expires in July 2018, predominantly denominated in Sterling and US Dollars which relates to about £93.2M at the current exchange rate compared to £79.3M under the old facility. By the end of the year some £22.5M was drawn down under the facility. There are currently commitments of £3.8M relating to the acquisition of new plant and equipment.

During the period the group acquired Spanish based AnaFocus, which specialises in the design and development of customised CMOS image sensors. The acquired group had net assets of £11M, some £15.6M of which related to identified intangible assets, mostly relating to current technology and customer relationships. The group paid £17.9M in up-front cash with a further £4.1M in contingent consideration possible, which the board estimates will be paid in full, so the purchase generated goodwill of £11M. During the year AnaFocus contributed adjusted operating profit of £1.8M on revenues of £5.8M. The first payment of the deferred consideration is likely to be £1.8M in the first half of the current year with the potential for two further payments, the first of which is due in the second half of the year with the final payment in the first half of the following year.

Going forward, whilst the board remains cautious about the broader economic environment, assuming no deterioration in market conditions, the outlook for the current year remains unchanged – which doesn’t give much away really. They have stated that they want to double operating profit by 2020, however, with a focus on industrial vision, space, radiotherapy and semiconductors with both organic growth and acquisitions which are expected to contribute to up to a third of the growth.

At the current share price the shares trade on a P/E ratio of 19.6 which falls slightly to 18.7 on next year’s forecast which seems fairly fully valued. The dividend yield stands at 1.9% after a 16% increase year on year, growing further to 2% which again, seems fairly average. Net debt stood at £5.2M at the year end compared to a net cash position of £770K at the end of last year.

Overall then this was a fairly good year for the group. Profits fell but this was due to restructuring costs under the business improvement programme and underlying profits improved year on year. Net tangible assets fell as the group spent cash acquiring a large amount of intangible assets with AnaFocus but the cash flow looked good, operational cash flow improved and the group had a good level of free cash flow even after the acquisition was taken into account. Operationally, imaging profits fell due to cost increases in some of the space programmes and declining thermal imaging orders be growth in the order book, partially driven by the AnaFocus acquisition gives some confidence for next year. Profits were strong at the RF Power business driven by good levels of Radiotherapy projects, partially offset by declines in defence spending at NATO countries but the declining order book is rather disappointing, despite the board blaming timings of orders for the fall.

Profits were flat at the semi-conductors business and he order book was fairly static. Interestingly the group increased headroom in their borrowing facilities which suggests to me that another acquisition is on the cards for the year ahead. The board has stated that they aim to double operating profit by 2020. I am not sure that I like these kinds of targets though, and I hope that growth will not be chased to the detriment of prudency. In conclusion, this seems to be a company with decent prospects that is performing fairly well. The valuation does seem to be up to date with this, though so I will continue to hold rather than try and add some more.

This has been a good year for the share price so far, it could perhaps have become a bit overextended though?

The group has now released its annual report so let’s see what further information is contained there, starting with the income statement.

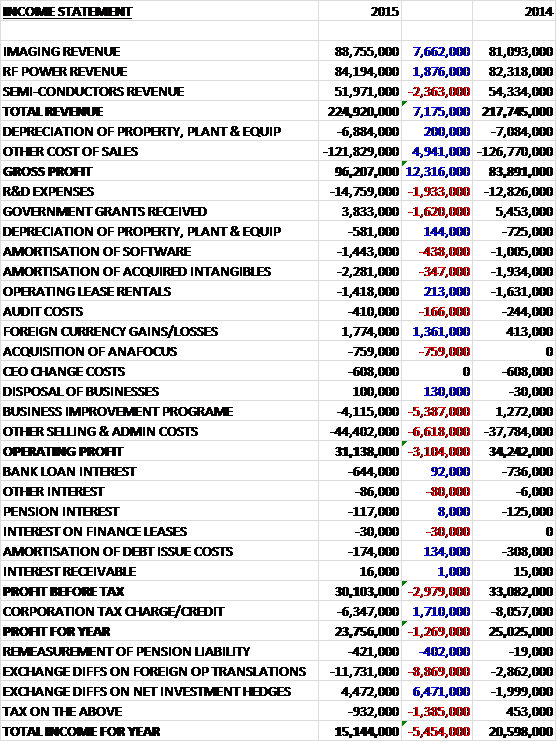

So there is a slightly larger breakdown in admin costs where we can see that amortisation increased along with audit costs but nothing really that important here. Probably more interesting is the more detail that comes with the balance sheet.

As we can see there is quite a lot of detail here. The increase in property, plant and equipment was due to the £3.8M increase in plant and equipment but of more interest is the breakdown of intangible assets where there were some large increases due to the AnaFocus acquisition. Goodwill was up £8.6M, customer relationships increased by £6.9M and patents & trademarks were up £5.1M. As far as receivables are concerned, both trade and “other” receivables declined during the year.

In liabilities, trade payables fell but contract balances received on account increased by £2.7M and accruals and deferred income grew by £3.6M. Within provisions, the big increase came from the £2.5M hike in the employee related provisions. Operating leases were broadly flat year on year and not a material amount.

There are also some interesting KPIs, most of which improved year on year with operating margin up to 17.8%, ROCE increasing and a 14% growth in the 12 month order book. We also see a 1 percentage point increase in the proportion of sales from outside Western Europe but the percentage of sales from customers of products which were new over the last three years declined slightly. We also see a fall in sales growth from 11% this year to just 3% this year.

We can also see that some £1M of trade receivables were impaired compared to £778K last year which seems disappointing and is not an insignificant amount. At the end of the year, the group had committed to £3.8M worth of capital spending, mainly relating to the acquisition of new plant and equipment. The group is also somewhat exposed to currency movements, particularly the US dollar with a 15% weakening of the currency against Sterling havening the effect of reducing profit by £294K. The exposure to the Euro seems fairly negligible thankfully.

On the 15th July the group released a trading update covering Q1 2016. During the quarter the group delivered modest revenue growth, reflecting the previously reported opening order cover in the Semiconductor division. Whilst the board remains cautious about the broader economic environment, the outlook for the current year remains unchanged. A fairly steady if not exactly inspiring update then, I will continue to hold.