Telford Homes has now released its final results for the year ending 2015.

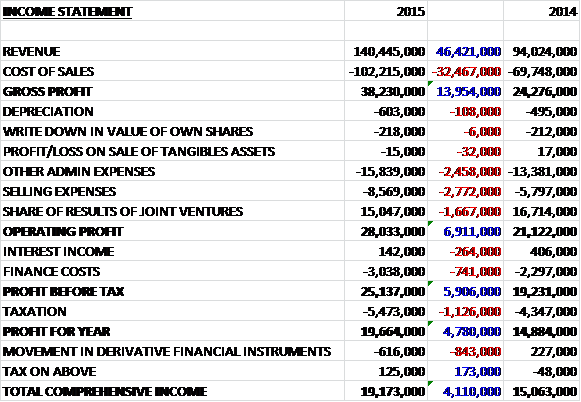

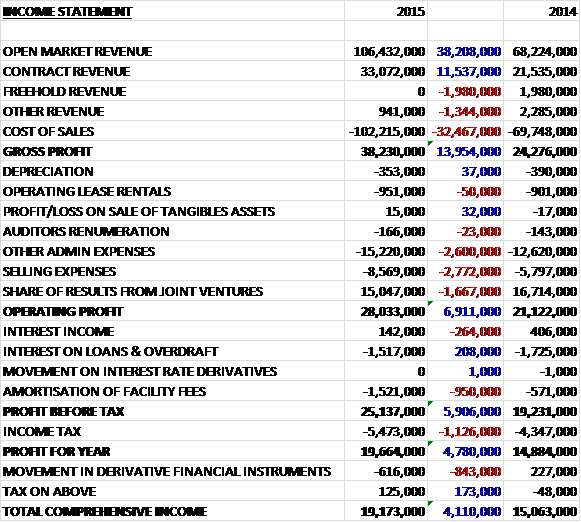

Revenues increased by £46.4M when compared to last year and a smaller increase in cost of sales meant that gross profit was some £14M ahead. We then see an increase in depreciation, a growth in admin costs, mainly due to higher employee costs, and a £2.8M increase in selling expenses due to an increase in agent commission following three significant sales launches, along with a £1.7M fall in the profit from the joint venture as 77 open market sales were completed at Bishopgate Apartments compared to 180 last year, which leaves operating profit some £6.9M higher at £28M. There was then a fall in finance income and a £741K increase in finance costs due to a growth in loan arrangement fees due to the new borrowing taken out which, along with a hike in the tax paid, meant that the profit for the year stood at £19.7M, an increase of £4.8M year on year.

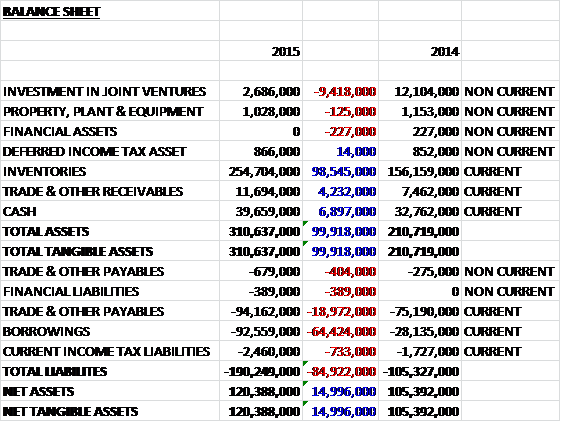

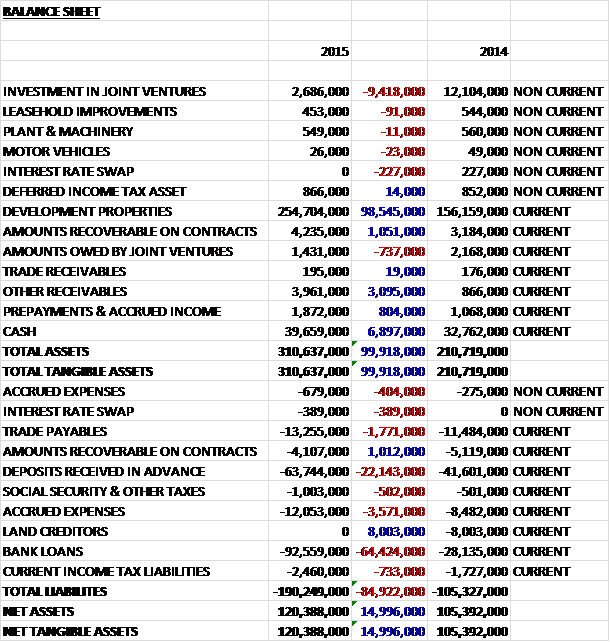

When compared to the end point of last year, total assets increased by nearly £100M driven by a £98.5M growth in inventories, a £6.9M increase in cash and a £4.2M increase in receivables, partially offset by the £9.4M crash in the investment in the joint venture, relating to the reduction in inventory at Bishopgate Apartments as some 77 open market apartments were sold. Liabilities also increased during the year due to a £64.4M increase in borrowings and a £19M growth in payables to give a net tangible asset level some £15M higher at £120.4M which looks rather healthy.

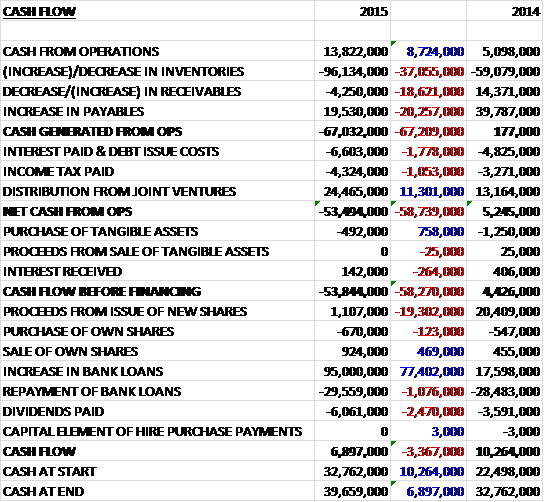

Before movements in working capital, cash profits increased by £8.7M to £13.8M. This was entirely counteracted by a huge increase in inventories, however, to give a cash outflow from operations of £67M compared to a broadly neutral position last year. We then see an increase in both interest paid and tax, more than offset by an £11.3M increase in the distribution from joint ventures to give a net cash outflow from operations of £53.8M, an adverse swing of £58.7M. There was a small amount of intangible asset buys but the cash outflow before financing stood at £53.8M. In order to cover this cash outflow, new bank loans were taken out so that after the payment of £6.1M worth of dividends, the cash flow for the year stood at £6.9M to give a cash pile at the year-end of £39.7M, most of which has been committed to future land and development costs.

The group exchanged contracts for the sale of 661 open market properties during the year and has sold a further 105 so far in since the end of March. The most recent sales launch was Manhattan Plaza in E14 close to Canary Wharf. The launch took place over three weekends and 71 out of the 120 open market properties were sold to investors at prices around £800 per square foot. A quarter of these properties went to UK investors with the bulk sold overseas, particularly into China. During the year there were several smaller launches including The Junction in E1 where half of the 26 open market homes were sold and the Town Apartments in Kentish Town where all 15 open market homes sold in a single weekend. In October, the group launches Stratosphere in Stratford that resulted in over £110M of sales in less than a month with nearly 90% of the 307 open market homes being sold. There are currently no unsold completed homes and they are being sold quicker than they can be built. The next significant sales launch will be Bermondsey Works in SE16 in June with 148 open market homes being available for about £600 per square foot.

Overall there are 2,200 homes under construction across 16 developments compared to 1,700 two years ago but the total number of completions during the year fell from 492 to 374. Despite this, revenues improved due to the increase in the average selling price per property from £329K to £439K, partly due to the mix of developments and partly due to an underlying price growth. Commercial revenue increased from £7.7M to £16M due to a significant sale in Bishopsgate Apartments of £9.65M net to the group.

There is very good earnings visibility here as shown by the fact that they are 95% forward sold for next year already with the total value of forward sales now over £550M compared to £341M this time last year. The group takes a minimum 10% deposit on exchange of contracts and where sales are more than two years ahead of completion, usually another 10% a year after exchange. This means there is a good cash flow coming in and during the year some £63.7M was taken in deposits. This success in forward selling homes meant that there was a greater proportion of properties sold to investors this year as they typically buy further in advance of completion than owner-occupiers and it is good to see that many customers make repeat purchases.

During the year margins were head of last year and expectations with operating margins up from 17.1% to 17.5% due to some commercial property sales at higher than expected prices and build cost inflation being slightly less than anticipated. The board expects margins to reduce in the future, mainly due to the more subdued level of house price inflation and some cost inflation. The gross margin has been targeted at 24% compared to the 32.4% achieved this year (31.9% last year). The board are still targeting a profit before tax of £40M by 2019 but have warned that profit growth may not be smooth and might not occur each year due the timing of project completions. This is reflected in brokers predictions for 2017, where it seems profits may drop back slightly so hopefully this will not come as too much of a shock to investors when/if it occurs.

Recent projects that have been acquired include a site in Upton Park where planning permission for more than 170 homes will be submitted later this year and terms have been agreed with an affordable housing partner on a regeneration scheme with planning permission for more than 100 homes. There are apparently no shortages of development sites but unlocking them is more of a challenge. As at the end of the year, the development pipeline stood at £1.07BN of future revenue compared to £878M at the same point of 2014.

There have been a couple of changes at the management and board level with Robert Clark stepping down as non-executive director in July after many years in the position. Also, joint group managing director Mark Parker was made redundant having been in the job since 2007 with the other joint group managing director, John Fitzgerald, now responsible for production across the entire group.

The planning process continues to be a challenge and the time taken to achieve it restricts the supply of new homes and can delay the planned development programmes. In December the group finally secured a resolution to grant planning consent for a development of 156 homes in Caledonian Road but some five months later, formal consent has still not been issued which exemplifies the problems faced by developers in London. Some small adjustments that can make a big difference include additional planning resources in local councils and setting defined time limits for various stages of the process. I doubt progress will be made on the former issue but the latter one sounds sensible and should be something that is introduced in my view.

There is one main future commitment which involves a joint venture with Notting Hill housing which has exchange contracts to purchase a significant site with outline planning permission in Stratford for £44M which is payable by January 2016 and funding for this will be sought later in 2015. The company has signed a new £180M corporate loan facility which extends to March 2019 which replaces the previous £120M loan facility. The interest payable varies depending on the gearing level from between 2.8% to 4% which is an improvement on the minimum level of 4% previously. As of the end of March, there was an unutilised balance of £85M (remembering the £39.7M cash level too) and gearing has increased to 44% with the covenant set at 150%. It is expected that this gearing will increase further as the group continues to invest in site acquisitions and development costs.

At the current share price the shares trade on a P/E of 15 which reduces to a cheap looking 12.2 on next year’s forecast, although it is expected to increase again to 14.6 in 2017. The shares are currently yielding 2.3% in dividends which is expected to increase to 2.8% next year which reflects the policy of paying one third of earnings in dividends. Net debt at the yea- end stood at £55.3M compared to a net cash position of £3.4M last year and this is a trend likely to continue next year.

The outcome of the General Election has provided some stability to the political environment and the housing market and the relatively affordable homes in London that the group focuses on are experiencing high demand from tenants, investors and owner-occupiers due to a shortage in the number of new homes, so the fundamental attractions of these markets are likely to be present for the foreseeable future. The board therefore expects significant growth in output and profits over the next few years and remains very confident in the long term prospects for the group.

Overall then this was a good update but one in which the group used considerable resources in expansion. Profits were up, mainly as a result in the increasing property prices and net assets improved. Operational cash flow was heavily negative, however, due to the investment in housing inventory and most of the cash is already earmarked for investment in the coming year, although there is still £85M of headroom in the debt facility. There are more homes under construction than this time last year and the group has a strong development pipeline with a 95% forward sold position. It is difficult to see the fundamental demand in affordable London homes declining any time soon and medium term, there is likely to be a strong increase in profits.

As with any company, there are a few issues to be aware of though. The slow-down in house price inflation and increase in costs will reduce margins going forward and it seems that profits will fall back in 2017 before increasing again in 2018 due to the timings of completion. Also, the group is taking on a lot of debt to fund expansion. Indeed, as further amounts of cash is utilised and the gearing increases further I think Telford may find it hard to keep the current pace of expansion going, at which point it is possible the shares could suffer a bit. Overall though, this seems to be a good investment and I will continue to hold on to my shares.

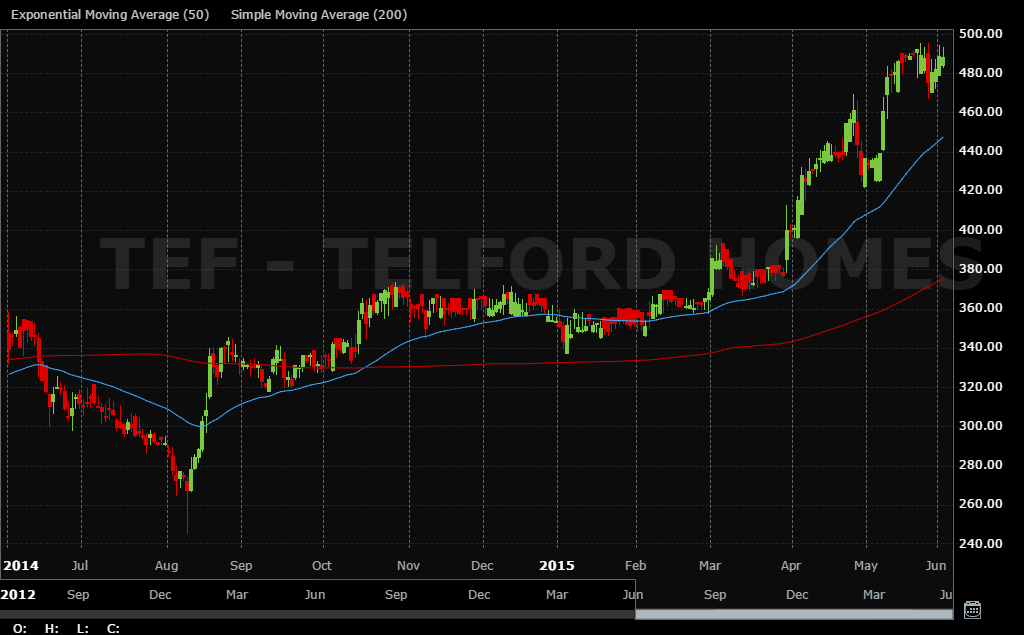

This chart looks good with an uptrend in place since mid-August.

Telford Homes has now released its annual report that gives a bit more detail to some areas.

So, we can see a break-down of the revenues received and the increase is accounted for by growth in both open market and contract revenue with freehold sales disappearing. We can also see that operating leases increased slightly to £951K and the other main area that has more detail is the finance costs and here we see that a small reduction in the interest on the loan was more than offset by the £950K increase in the amortisation of facility fees relating to the early payment of the previous facility.

As usual it is the balance sheet that shows the most new detail. Here we see that all property, plant and equipment items fell slightly during the year. As far as receivables are concerned, the £737K fall in amounts owed by joint ventures was more than offset by a £1.1M increase in amounts recoverable on contracts, a £3.1M growth in “other” receivables – not sure what this relates to, and an £804K growth in prepayments and accrued income. The large increase in payables was predominantly driven by the £22.1M increase in deposits received in advance (stretching the definition of “payables” in my view), although there was also a £3.6M growth in accrued expenses and a £1.8M increase in trade payables. These were partially offset by the elimination of £8M in payables to land creditors. Overall then, I think that this helps allay some potential fears over the nature of the increased payables. Although increasing somewhat, operating leases were fairly negligible.

Overall then, not much has changed here, the group still looks a good investment but I do wonder whether there may be some near-term volatility as investors start to look at the drop off in profits in 2017.

On the 6th July it was announced that managing director John Fitzgerald sold 100,000 shares at a value of £427K. The sale was apparently in order to fulfil some personal financial commitments. He still owns 282,718 shares in the company.

This was followed by an announcement that on the 8th July he sold a further 50,000 shares for £212K. This is quite some personal commitment and I don’t like this. Combined with the announcements in the budget I have decided to realise a profit here. I do still like this company but see a few short term issues and feel this is the prudent response.

On the 16th July the group released a statement from the AGM. They continue to experience very strong demand from investors, tenants and owner-occupiers across all of their developments. Most recently, they launched 148 open market homes at Bermondsey Works where 94 sales were achieved in June at a total value of £44M. since the start of April the group have secured 218 open market sales and the total value of forward sales due for completion this year is now over £620M, more than three times the revenue reported last year.

They also comment that they welcome the recent measures outlined by the government to improve the planning process and remove unnecessary delays, devolving more power to the Mayor of London and speeding up the process for brownfield land. The group continues to appraise opportunities to increase its development pipeline and is in negotiations on a number of prospective sites. The current pipeline extends into 2019 but the board is still keep to increase this when the right opportunities arise. They remain confident of achieving expectations for 2016 and laying the foundations for sustained long term growth.

All in all, this all reads very positively, the amount forward sold for this year is astonishing. There is no mention of the extra taxes on property investors though, and what effect this would have and I presume they are still expecting a fall in profits in 2017 so there are still some potential downward pressures.

On the 21st September the group announced the acquisition of the regeneration business of United House Developments for £23M which has been entirely funded from existing cash resources. The business consists of a group of companies that have various interests in development opportunities in North and East London. These are City North adjacent to Finsbury Park station, the refurbishment of the Balfron Tower in Poplar, two phases of development at Gallions Quarter near Royal Albert Dock and the regeneration of Chrisp Street market in Poplar. The developments are all at various stages in the planning process but they have the combined potential to add some £500M to the group’s existing £1BN development pipeline.

City North is a mixed use development comprising 355 apartments and 109,000 square feet of retail, leisure and office space in a joint venture with Business Design Centre. The scheme includes two 23 storey towers linked by a 12 storey terrace building. The site has full planning permission and incorporates plans to improve the facilities at the adjacent Finsbury Park station. The group will immediately work with the joint venture partner to ensure that construction can commence in 2016 with completion expected in 2020. The gross development value of City North is in excess of £200M so it should add over £100M to the group’s pipeline.

Balfron Tower is a 26 storey grade II listed building in Poplar. The project involves the refurbishment of 146 existing homes in a joint venture with Londonewcastle and the owners, Poplar HARCA. The development is subject to planning permission and allowing for this process, the refurbishment should commence in early 2016 to be completed by 2018. The group owns a 25% interest in the scheme which is expected to add over £15M of revenue to the development pipeline.

Gallions Quarter is a multi-phase development adjacent to Gallions Reach DLR station. The development is controlled by Notting Hill Housing Group, who have partnered with the group before. They are acquiring a 50% interest in the project. The first phase has planning consent for 292 new homes subject to signing a section 106 agreement and the other phase has outline consent for a further 254 homes. The process through which United House Developments is acquiring a legal interest in the development is not yet complete but the final steps are expected to be concluded shortly. A portion of the total consideration has been deferred therefore and becomes payable on securing the legal interest in the development, although the amount of the deferred consideration has not been disclosed. Assuming the condition is satisfied, the two phases will add over £75M to the group’s development pipeline. The first phase is expected to commence in 2016 and be completed by 2020 with the remaining phase starting at that point.

The regeneration of Chrisp Street market is a major development opportunity in partnership with Poplar HARCA, whom the group have a long standing relationship with. The development is expected to include several hundred new homes but the proposals require substantial consultation with local residents, commercial occupiers, Tower Hamlets borough (oh dear) and other interested parties. The ultimate acquisition of the development from Poplar HARCA is subject to achieving all the necessary consents. The aim is to start development in 2017 with phased completions expected over a seven year construction time. The development has the potential to add £300M to the group’s long term development pipeline.

These are all interesting acquisitions that add considerably to the forward pipeline of work. They will not add much in the short term and some of them seem to be subject to a number of conditions but this looks fairly positive overall.

On the 14th October the group released a trading update covering the first six months of the year.

They have recently opened a new sales and marketing centre in Stratford to give them a permanent presence in the area. The remaining 32 homes at Stratosphere were launched from this centre in October with 18 reservations secured by the end of the first day. Following several successful sales launches in the last six months, the forward sold position of over £685M to be recognised across five years compared to £550M at the start of the year. Legal completions on forward sold homes are also being achieved in line with expectations. These are weighted to the first half of the current year and as a result, the board expect the pre-tax profit to more than double compared to the £9.4M recorded last year. The group remains on track to meet profit expectations for 2016 and beyond.

The group has progressed planning for several of its key developments. After an initial delay, full planning permission is in place for 156 homes at Caledonian Road and work is underway on the site. In addition, planning permission has been granted in the last few weeks for 471 homes at Chobham Farm, Stratford, in partnership with Notting Hill Housing Group and for 192 homes at Redclyffe Road, E6. Both of these were approved at recent planning meetings and are subject to signing the usual legal agreements.

Demand remains high from all of Telford’s typical customers so the board are very confident in investing further in the development pipeline. This update sounds pretty positive to me, but I think it was always expected to be. The gap is likely to occur in next year’s figures but nonetheless I am tempted to dip back in here.

On the 27th October the group announced a placing to raise £50M. It is thought that the placing will enable them to take advantage of the current opportunities and achieve enhanced longer term growth in its output of new homes. The company will place 13,888,889 new shares at a price of 360p per share with the net proceeds expected to be £48.3M.

The proceeds are expected to be committed within one year and be fully utilised within two years and will initially be focused on driving sustained profit growth without reducing short term debt requirements such that gearing will increase in the short term as previously anticipated. Given its strong forward sold position, the group will invest the placing funds to target annual profit before tax of £45M from 2019. Beyond that the board expects to use recycled equity to manage future debt requirements and therefore reduce longer term gearing whilst still maintaining controlled growth towards a pre-tax profit of £60M.

As a result of the long term nature of the developments, the placing is expected to cause an initial dilution of earnings but this will enhance net asset value per share. As a result the board intends to increase its dividend payments above one third of earnings in the short term to offset this initial dilution. The placing shares will represent about 18.6% of the enlarged share capital and represents a discount of 12.2% on the closing price on the 26tth October.

The shares are expected to begin trading on the 16th November so I don’t expect to see much share price strength before then. The group are certainly going for growth at the moment which could be a mistake if there is a downturn any time soon.

On the 26th November the group announced that it had purchased a significant development site on Camden Street in Poplar for over £20M. The site has full detailed planning consent for a 22 storey development consisting of 206 new homes and a nursery. The group expect to commence work on the site in 2016 with completions anticipated in 2019 and 2020. The development is expected to add in excess of £80M of revenue to its development pipeline.