Creston has now released its final results for the year ending 2015.

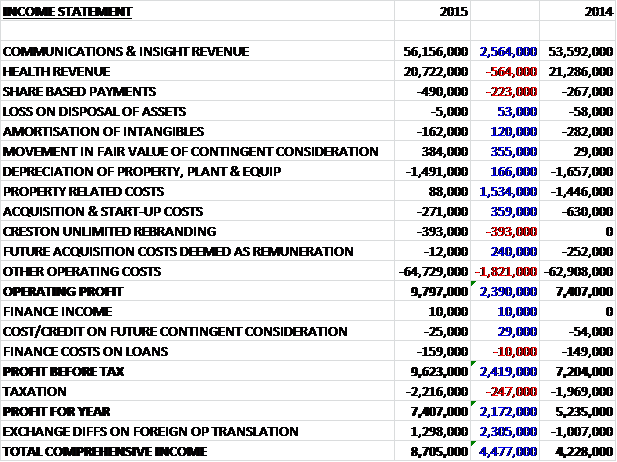

Overall revenues increased year on year as a £564K decline in health revenue was more than offset by a £2.6M increase in communications and insight revenue. Although underlying operating costs did increase, there were a number of costs that fell with both depreciation and amortisation costs declining, a £240K reduction in future acquisition costs deemed as remuneration, a £359K decrease in acquisition and start-up costs, a £355K positive movement in the fair value of the contingent consideration and a £1.5M positive movement in property related costs that disappeared year on year as some £100K was credited back due to a rebate of costs incurred during the vacant period at the HQ. The end result is a £2.4M growth in operating profit which, after an increase in tax, became a £2.2M increase in profits for the year at £7.4M.

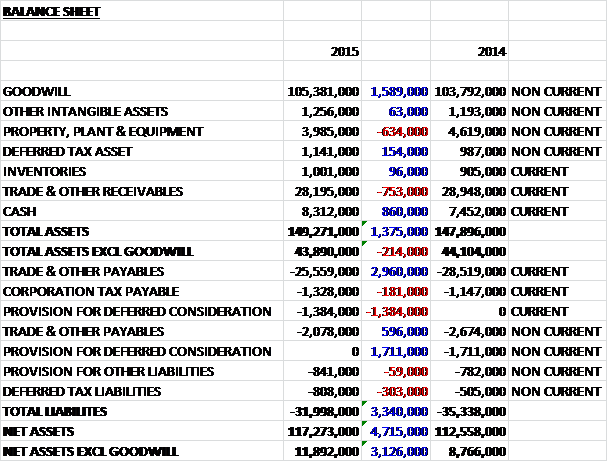

When compared to the end point of last year, total assets increased by £1.4M, driven by a £1.6M growth in goodwill, an £860K increase in cash and a £154K increase in deferred tax assets, partially offset by a £753K fall in receivables and a £634K decline in property, plant and equipment. Conversely, total liabilities declined year on year as a £3.6M fall in payables and a £327K decline in deferred consideration was partially offset by a £303K growth in deferred tax liabilities and a £181K increase in corporation tax payable. The end result is a net asset base, excluding goodwill, of £11.9M which represents a £3.1M increase year on year.

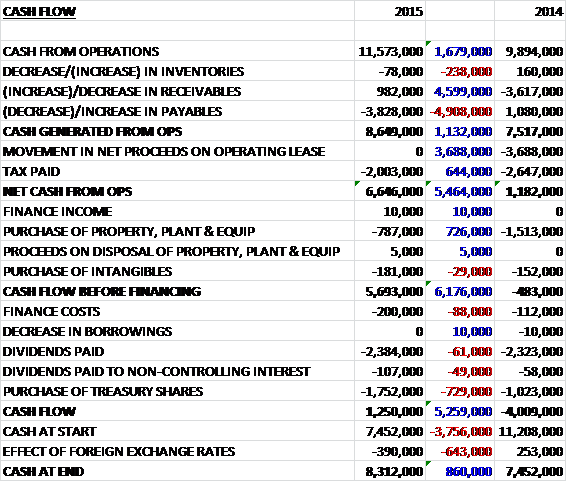

Before movements in working capital, cash profits increased by £1.7M when compared to last year to £11.6M. This was eroded somewhat by a fall in payables relating to a reduction in deferred revenue where scope for pre-billing has reduced across the client base, so that cash generated from operations increased by £1.1M. After tax, the net operational cash flow stood at £6.6M. There was little in the way of capital expenditure with £787K spent on tangible assets and £181K spent on intangibles to give a strong free cash flow of £5.7M. This was more than enough to pay for the £2.4M of dividends and £1.8M in share purchases to give a cash flow for the year of £1.3M compared to an outflow last year that was affected by cash payments to fulfil the dilapidation obligations with the signing of a new operating lease at the head office, and higher capital expenditure.

Underlying profit at the Communications and Insight division fell by £156K to £8.1M with the profit margin declining from 15% to 14%. The decline was due to the weakening Euro in the second half of the year and temporary additional freelancer costs incurred following a strong new business performance. The division managed to mitigate some £500K of property related costs incurred in the first half of the year following a successful rates review across a number of properties in the second half. Significant new business wins during the year included work for new and existing clients such as Activision, Allianz, Arthritis Research UK, Asda, Varilla, Bentley, Deezer, McCarthy & Stone, McLaren, Mind Candy, Sainsbury’s Energy, Sky, Sony Mobile, Superfast Broadband and Vue Cinemas. Post period end wins included Costa and further assignments from Canon.

Underlying profit at the Health division fell by £178K to £4.3M with a profit margin remaining steady at 21%. The decline was exacerbated by the weakening Euro during the year but constant currency profits fell too. As previously reported, after a strong first half, Q3 revenue performance was impacted by some client budget cuts and project delays within the UK Health business, which also affected Q4 revenue at which point actions were taken to re-align the cost base. The effect was mitigated somewhat, however, due to a revaluation credit relating to the contingent consideration for DJM Unlimited due to project delays and cancellations, partly as a result of a failed clinical trial. Significant new business wins during the year included Abbot, Baxter, Bayer, Danone, International AIDS Society, Parent Project Muscular Dystrophy and Unilever. The group has also expanded its remit with CDC, Novartis, National Meningitis Association, Pfizer and Sanofi.

This has been a year of change for the group with a new board and a new strategy that was set out at the start of the year which sought to build an agency group band, develop a group full service client offer, develop the consultancy offer, invest in the existing company’s offer and services, and to grow international services. This has been implemented with the launch of the new agency group brand and offer, Creston Unlimited, with the rebranding of all Creston companies.

The board have also sought to target investments and partnerships on skills that are currently missing within the group’s offering. During the year the group has entered into four new partnerships – each in a complementary area. Two new partnership agreements will enhance the international services offering. In November, they signed an agreement with Serviceplan, the leading independent marketing communications agency group in Europe which has already resulted in a number of new client referrals and joint pitches such as a joint CRM assignment for Danone in Germany and the Middle East. In April 2015, the group signed an agreement with Propeller Communications, a digital healthcare communications agency based in the US and in the same month they also signed with Future Foundation, a global consumer trends and insight consultancy to complement their insight offer, and with the digital strategist, the Digital Consultancy to further add to the group’s consultancy offer.

The KPIs for the group are all financial and includes international revenue, digital revenue, EBITDA, cash conversion and net cash along with a few others. All indicators either improved or remained flat except revenue and profit per head, both of which reduced year on year. During the year the group embarked on a share buy-back scheme and as of the year-end some £1.8M has been spent with a remaining balance of £200K still to be purchase depending on the share price performance.

As previously touched upon, this year was a year of change for the board. Barrie Brien joined as CEO and Kathryn Herrick joined as CFO. David Grigson stepped down as Chairman and was replaced by Richard Huntingford who was an existing member of the board so at least provides some continuity. Additionally, Kate Burns joined the board as non-executive director and David Marshall stepped down. Finally, after the year-end, Nigel Lingwood will join as non-executive director with Andrew Dougal stepping down.

The group has been adversely affected by the strengthening Sterling against the Euro and given that further volatility is expected, management are working to renegotiate Euro denominated contracts where possible and are considering available hedging arrangements.

As can be seen from the above accounts, there is now £1.4M of contingent consideration to pay after a £400K credit was received due to its revaluation. This will become payable in cash by July of this year. Also, after the end of the balance sheet date the group paid out £8.7M for the acquisition of How Splendid so it is quite likely that they will finish 2016 in a small net debt position.

After the year end the group announced the acquisition of 51% of How Splendid, a digital design and development consultancy. The acquisition added some significant new clients such as Barclaycard, Boots, Gamesys, News UK, Skrill, SSE and Star Alliance, two of which will become one of the top 20 clients in terms of revenue. On completion there was an initial cash payment of £8.7M funded from existing resources with a further cash payment of up to £7M due by June 2017. In addition, Creston will have the option to acquire a further 24% from April 2017 for up to £8.6M and the remaining 25% from April 2019 for up to £11.9M.

Going forward, the group is now one year into its five year strategy and there is a real feeling of momentum across the company. The board are encouraged by the early success of this strategy which gives a strong platform to deliver value to shareholders over the medium term. That is a quote from the outlook statement and it gives next to nothing away about trading in the current year!

At the current share price, the company trades on a P/E ratio of 11, falling to a rather good value 9.8 on next year’s consensus forecast. After an 8% increase in the full year dividend, the shares currently yield 3.1% in dividends, which increases to a decent looking 3.4% on next year’s forecast. At the end of the year, the group was in a net cash position of £8.3M compared to £7.5M at this point of last year. After the year end, the banking facility was renegotiated to include a £25M revolving credit facility which suggest that perhaps further acquisitions are on the cards after the recently announced acquisition and previously announced deferred consideration use up the net cash reserves.

On the same date as the results the group announced that it had made a strategic investment in 18 Feet and Rising, a London based advertising agency. The group currently works with Allianz, Cuprinol, Kopparberg, Nandos, House of Fraser and Skoda, for which they created the world’s first ad campaign to use eye tracking technology. The investment is for £1M in cash for a 27% stake in the business. Last year it grew revenues by 245 to £2.7M but is presumably still loss making as no figures were given for profits.

Overall then, I think this update was better than I was expecting. Reported profits increased considerably, although underlying profits showed a more modest growth. Net assets improved and the balance sheet looks good for a company of this nature. Also, operational cash flows improved and the group had a very good level of free cash flow which more than paid for the dividends and share buy-backs. Operationally, the weak Euro seems to be a bit of a drag on performance, and this along with some of their health clients cutting budgets meant that the performance in the second half was a bit of a struggle. The cash pile has already been used up in acquisitions and I do hope that the new board, which has brought with it a new energy and strategy doesn’t go overboard with the acquisitions. In conclusion then, the good performance this year combines with the cheap looking forward P/E and decent dividend make up for the operational difficulties and I have made a small purchase.

As we can see, the share price has responded well to the results.

Creston has now released its annual report for the year ending 2015.

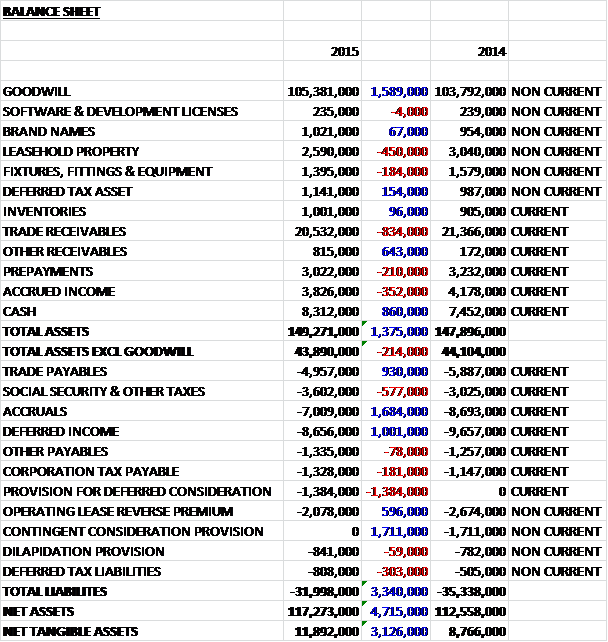

The only extra information gleaned from the income statement is that audit costs grew by £17K, operating lease costs fell by £166K and there was a £127K positive swing in foreign exchange items. This had the effect of giving an “other” operating cost of £11.2M, an increase of £834K year on year. It is good to see the operating leases come down but there is not really much else of interest here – I do with operating lease costs were listed separately at the prelim results stage but I guess I can’t have everything. I also wish the receivables, payables and intangible assets were split on the prelim balance sheet too so we will have a look at that now.

So, we can now see that the small increase in intangible assets is down to the increase in the value of brand names and within property, plant and equipment the fall was driven by a £450K decline in leasehold property. Within receivables we can see an £834K fall in trade receivables, a £352K decline in accrued income and a £210K fall in prepayments was partially offset by a £643K increase in “other” receivables. As far as liabilities are concerned, we can see that a £577K increase in social security and other tax payables was more than offset by a £930K fall in trade payables, a £1.7M decline in accruals and a £1M decrease in deferred income. The operating lease liability off the balance sheet was broadly flat at £21.5M.

The reminder that the group is somewhat susceptible to exchange rate changes should be notes. A 10% strengthening of Sterling against the Euro would reduce profits by £175K and a 10% appreciation against the US Dollar would reduce profit by £20K. Net cash at the year-end stood at £6.9M not including the operating leases but including the deferred consideration due to be paid this year.

There are a few case studies included in the report. The objective with Vue Cinemas was to increase cinema admissions and market share so the group used local audience insight and mapping to define the target audience and create new film related creative content across multiple channels. For Magnum they created an integrated brand engagement campaign spanning digital, social, experiential, print and outdoor to drive excitement around the release of two limited edition Magnum ice cream flavours. For BMW they were tasked with revolutionising the user experience of the retailer network websites so they balanced centrally managed and localised content to empower dealers to market in their local area. The group also worked with Virgin Trains across social, digital advertising and CRM to get more people on their trains.

I have to say that to me the new CEO seems to be very well paid, perhaps excessively and this year earned £696K with a substantial annual bonus and LTIP award. The annual bonuses are based on profit before tax (75%) and client satisfaction (25%) which seems sensible enough but a 2% increase in the former was enough to trigger the minimum bonus.

In all though, I feel that this is a decent company only part way through a tangible improvement drive so I am happy to hold.