Utilitywise is a utility cost management consultancy offering energy procurement, energy and water management products and services to its business customers throughout Europe. They provide services to its customers designed to assist them in achieving better value from their utility contracts, reducing their energy and water consumption and lowering their carbon footprint. Services include energy procurement, energy and water management, energy and water efficiency, carbon management, energy and water saving product installation and project management. They have now released their final results for the year ending 2014.

Before I start, I want to have a bit of a rant. The annual report and general shareholder facing financial reporting is one of the most awkward to use/read that I have seen. First of all, I found it very difficult to find the interim results on the website, although the annual report was easy enough to see. The report itself, though, has two pages to each A4 sized sheet which makes the writing very small and hard to read. In addition, why do companies insist on using coloured backgrounds and non-black text? Who decided that a red background with white text was going to be the best idea? The group also made a mistake in last year’s accounts and failed to include rental payments of £510K in their lease payment disclosure. Anyway, rant over, hopefully the financial performance is a bit better.

The group provides services through negotiating rates with energy suppliers on behalf of business customers and generates revenues by way of commissions from those suppliers. This revenue is recognised when the contract between the customer and supplier becomes live and are calculated based on expected energy use by the business customer at agreed commission rates. The cash receipts from these sales can be received before the date that the contract goes live or spread over the term of the contract between the energy supplier and the customer, which can be up to three years. Accrued revenues relate to these commissions earned and not yet invoiced or paid.

The group also earns revenue from the sale of energy management products to business customers and contracts for on-going services. Energy management product revenue is recognised as soon as the work has been completed and for on-going service contracts, the revenue represents the value of work done in the year with revenue for contracts for on-going consultancy services being recognised as it becomes due to the group as services are delivered.

There are two business segments that are reported on in the group. The Enterprise division derives its revenues from the commissions earned from energy suppliers for contracts with small and medium sized business customers throughout the UK, Ireland and some European markets. The Corporate division derives its revenues from energy procurement of larger industrial and commercial customers, providing an account care service and offering a variety of utility management products and services designed to assist customers manage their energy consumption.

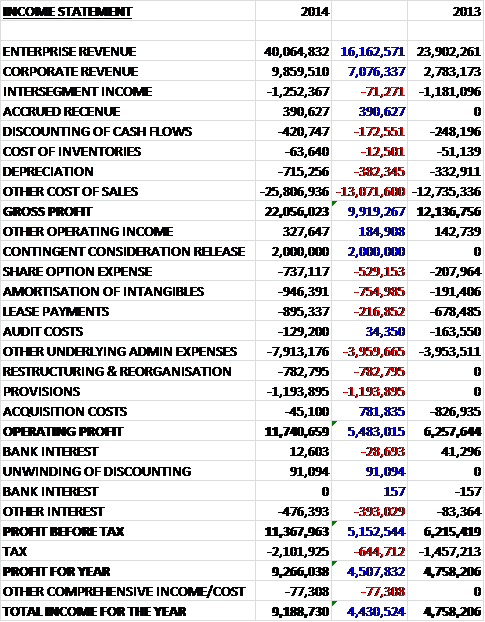

When compared to last year, revenues increased across both business sectors with Enterprise revenue up £16.2M and corporate revenue up £7.1M giving rise to a 93% overall, although like for like revenues were “only” up 62%. We also see an increase in cost of sales to give a gross profit £9.9M ahead of 2013. There was a one-off gain of £2M relating to a contingent consideration release which was offset by a £783K charge for restructuring and a £1.2M provision. Underlying admin costs were also up, with increases seen in share option expenses, amortisation and lease payments to give an operating profit of £11.7M, an increase of £5.5M. After an increase in “other” interest and a higher tax charge, the profit for the year was £9.3M, a £4.5M increase year on year.

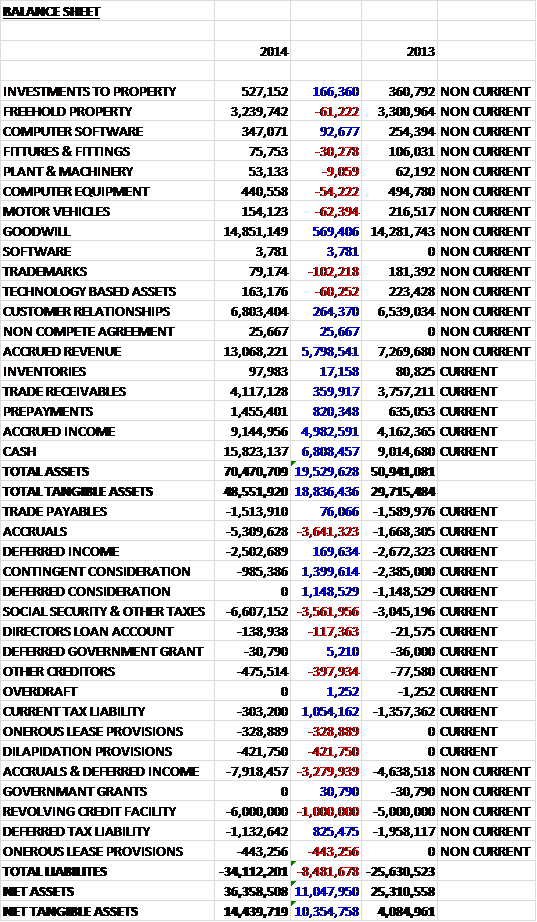

When compared to the end point of last year, total assets increased by £19.5M, driven by a £6.8M growth in the cash level, a £10.8M increase in accrued income, and an £820K increase in prepayments. Liabilities also increased during the year as a £6.8M increase in accruals & deferred income, a £1M growth in the revolving credit facility and a £3.6M increase in social security and other tax payables was partially offset by a £1.4M fall in contingent consideration, a £1.1M decline in deferred consideration, a £1.1M fall in the current tax liability and an £825K decrease in the deferred tax liability. The end result of all this is a £10.3M growth in the net tangible asset position at £14.4M. It is worth noting, though, that this corresponds to a significant increase in outstanding operating leased which now stand at £15.8M due to the new head office but these are mostly long term lease commitments with current commitment standing at just £772K.

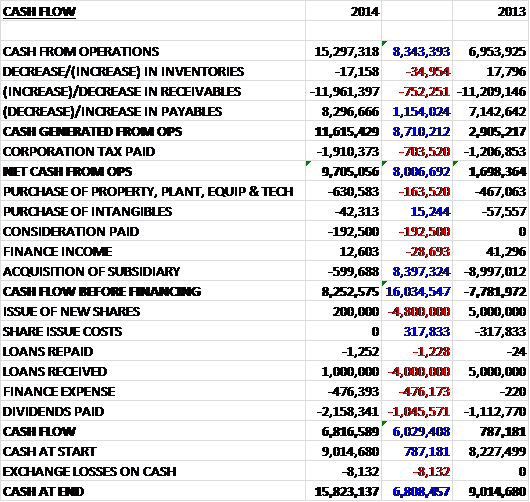

Before movements in working capital, cash profits increased by £8.3M to £15.3M. This was eroded somewhat by a large increase in receivables, and a small growth in tax to give a net cash from operations of £9.7M, a growth of £8M year on year. This cash easily covered capital expenditure and the small spend on an acquisition to give a free cash flow of £8.3M. The group then took out £1M more in loans and paid dividends of £2.2M give a cash flow of £6.8M and a cash pile at the year end of £15.8M. This looks to be very impressive but I’m not sure why more loans (albeit fairly modest amounts) are being taken out if cash flow is this strong – there are currently undrawn facilities of £3M.

Profit before tax at the Enterprise business was £6.3M, an increase of £500K year on year and profit before tax at the Corporate business was £1.7M, an increase of £200K when compared to last year. The KPI’s are quite interesting and don’t seem to include the usual EPS/revenue/margin metrics. The number of energy consultants increased from 281 to 363, the number of contracts secured increased by 36% 37,824 and the future secured revenue grew by 70% to £28.2M which all seems good, although I would have thought that hitting the target of one of the KPIs would probably filter through to the others too.

Given the nature of the services the group offers, it is clear that actual revenue earned from commission is dependent on the amount of energy actually used by the customer. The group has determined that there is a likely variability of 15% but if the usage varies by more than that, there may be an impact on revenue – with each extra 1% potentially affecting revenue by the tune of £421K. Due to the way the group earns commission in the Enterprise segment, they are very reliant on a small number of energy suppliers. One energy supplier accounts for some 36% of revenue with another one accounting for 15%. Clearly this leaves the group very susceptible to any changes in their agreement with that one large customer.

The group has continued to invest in its IT systems and processes to support further growth, and this has included the development of Quantum, the core CRM solution. Additionally they have developed the system to support their presence in the French and German markets and the recent acquisitions have enabled them to invest further in Energy Services with improvements to their Edd:e sub-metering solution that is now fully integrated in to the multi-utility reporting platform “Utility Insight”.

There were a number of exceptional items during the year, many relating to the costs incurred in the acquisition of Icon Communication Centres and other aborted acquisition costs. There were also settlement payments of £469K, costs of £167K incurred in the set-up of a new head office which will be occupied in the next financial year as well as a dilapidations provision and an onerous lease provision for the current premises of £422K and £772K respectively. The £2M credit arose from the release of deferred consideration where earn out criteria were not met, so I suppose that cloud did have a silver lining.

There are a number of ways in which the group gains new customers. They employ “energy consultants” who cold-call potential customers who might benefit from reduced energy tariffs, some organisations, such as the British Chamber of Commerce, refer customers to Utilitywise, where commissions are split between both companies. Field based energy consultants target organisations that can’t be reached through the telemarketing channel and the business development team target larger prospective customers. The board believes that due to the UK market fragmentation, the low penetration of third party intermediaries in the UK commercial market and the company’s share of the total potential market means that there is an opportunity to increase market share through both organic growth and acquisitions. In addition, following the Icon acquisition, a market opportunity exists to expand the model into other European markets.

There are a number of potential risks that face the group. As mentioned above, the group derives a significant portion of its revenue from the commissions paid by a small number of energy suppliers. Should these suppliers decide in future not to engage with the group or with intermediaries generally, and instead to engage directly with customers, the group would suffer pretty drastic declines in earnings. There is also a risk that the government implements legislation requiring changes to the current fee structures for TPI’s which could have a material impact on the operating results of the group. Finally, the energy procurement market is currently unregulated and any future regulations, whilst not as catastrophic as the above two risks, could add to the costs incurred by the group.

In April the group acquired Icon Communication in the Czech republic for a total consideration of nearly £2M consisting £897K in cash, £99K in shares and £985K in contingent consideration. The transaction generated goodwill of £569K and came with intangible assets of £1.2M. Since the data of the acquisition the business has generated revenue of £867K and a loss before tax of £65K. If it were acquired at the beginning of the year, group revenue would be £52.2M and profit before tax £10.9M. The group was acquired predominantly to facilitate expansion into certain European markets.

Some board changes during the year include Andrew Richardson taking on an enhanced role as deputy CEO (whatever that means) and Jon Kempster has become CFO, a role he previously held at Wincanton. Given that group’s dire financial struggles, I am not sure that is a good thing. The group is run by CEO Geoff Thompson who also founded the group. For the most part the board looks quite impressive and young, although the COO is a guy called Adam Thompson aged just 27, I assume he is the founder’s son. The board also has substantial shareholdings which is good to see, although not that unusual when the founders are still running the show.

In addition to the lease commitments of £772K for next year, the group also has some £774K to pay for the fit out of the new head office. The new office will enable the group to grow headcount to 1,400 over the next two years from around 745 in 2014.

At the current share price, the shares trade on a hefty historic P/E of 22.3 which falls to a more reasonable 16.1 on next year’s forecasted earnings. The shares have a yield of 1.5%, rising to 2.1% which is nice to have in a growing company, if not altogether that exciting.

Overall then, this seems as though it has been a good year of progress for the group. Profits and net tangible assets are up considerably, along with operational cash flow to give a good level of free cash. The new head office should offer a good platform for further growth and the group should be able to absorb the fit out costs without too many problems. There seems to be plenty of opportunity for future growth and the forward looking P/E ratio doesn’t look too stretched. There is one major potential risk here though, and that is the fact that the group makes money from commissions from energy companies. One of these suppliers accounts for 36% of revenues which is a huge amount and should this supplier decide to targets these customers direct, the implications for Utilitywise are fairly catastrophic. In conclusion, though, I think this is an interesting looking company, albeit one that does come with considerable risk. I may look to take a position if I feel bold.