Photo-Me has now released its final results for the year ending 2015.

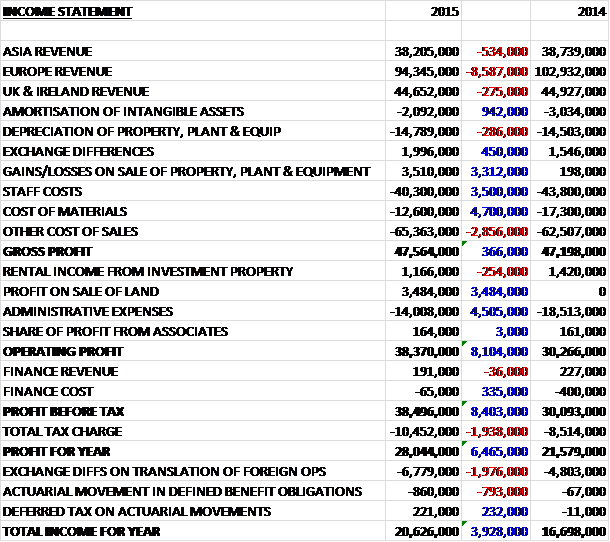

When compared to last year, revenue fell across all regions with a particularly large £8.6M decline in Europe. Underlying revenue did increase, however, as changes in exchange rates had the effect of reducing revenue by £11M and some £2.7M of falling revenues was due to the decline in the minilab business. We then see a lower amortisation and depreciation charge, the group gained on exchange differences and there was a one-off £3.5M gain from selling the vacant land at the Bookham site. In addition, staff costs fell by £3.5M as a result of the restructuring of the former sales and servicing division and cost of materials were down £4.7M due to the winding down of minilab division as well as the reductions achieved through enhanced efficiencies in the supply chain, which left other costs of sales up some £2.9M to give a gross profit just £366K above 2014. We then see a large decline in admin expenses and a £335K fall in finance costs before a £1.9M growth in the tax bill meant that the profit for the year stood at £28M, an increase of £6.5M when compared to 2014.

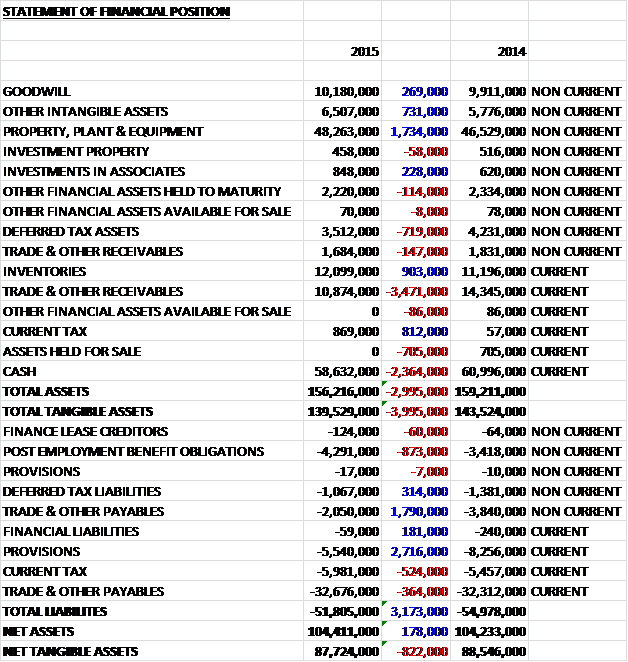

When compared to last year, total assets fell by £3M, driven by a £3.5M decline in receivables and a £2.4M fall in cash, partially offset by a £1.7M increase in property, plant and equipment. Total liabilities also declined during the year due to a £2.7M fall in provisions and a £1.8M decrease in payables. The end result is an £822K decline in net tangible assets at £87.7M.

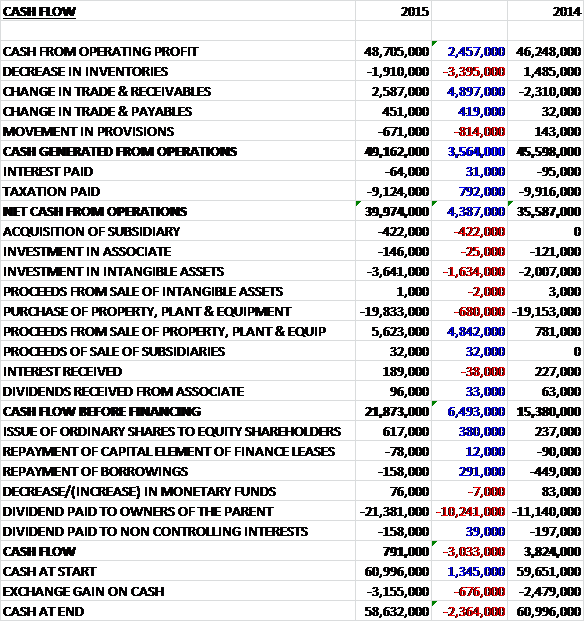

Before movements in working capital, cash profits increased by £2.5M to £48.7M. A relatively modest fall in receivables drove the cash from operations to £49.2M, a £3.6M increase year on year. The tax bill was then somewhat lower so that the net cash from operations stood at just under £40M. The group then spent nearly half, some £19.8M, on property, plant and equipment with another £3.6M spent on intangible assets, offset by a receipt of £5.6M from the sale of property plant and equipment to give a cash flow before financing of £21.9M. The bulk of this was spent on dividends to give a cash flow for the year of £791K, although due to exchange rate losses, the actual cash level at the year-end fell by £2.4M to £58.6M.

The operating profit at the Asia division was £6.9M, an increase of £1.2M year on year. By far the largest territory in the region is Japan which showed a strong performance with revenues up 6.4% and profits up 18.6% on a constant currency basis. The group is deploying an additional 1,000 booths in Japan to take advantage of the new ID card regulation which is scheduled to come into force in January 2016. Under this regulation, all Japanese citizens will need a new photo ID card and with a population of some 87 million, this is expected to lead to a substantial increase in demand over the next two to three years. Gradual progress continues to be made in China, where turnover rose by 25% on a constant currency basis and operational efficiencies along with better siting of machines resulted in a profit in the country compared with the loss last year. Positive progress is also being made in South Korea, where some 100 photo booths have been sited.

The operating profit at the Europe division was £22M, an increase of £800K when compared to last year despite reported revenues falling by 8.4% which was mainly due to adverse currency movements and the declining minilab business. In addition the profit would have been considerably higher on a constant currency basis. The European photobooth estate increased by 4.5% year on year with the main areas of growth being France and Switzerland. The group continued to roll out its higher margin Starck booths and there are now 3,213 deployed across the continent, an increase of 883 over last year. The roll out of the laundry product continued to progress well with an increase in the owned estate of 442 to 644 machines. The average revenue per owned unit in France was €14.396 which represents a 4% increase year on year and the turnover of the laundry business as a whole was £6.3M, up from £3.3M in 2014.

The group now has laundry units in nine countries, with the most significant coverage being in France and Belgium. Besides the traditional laundrette locations, they are also seeing potential demand in sites like equestrian centres, campsites, universities and military barracks. Prospects are particularly good in Portugal and Ireland with 37 machines now in Portugal which represents 28% of the total revenue from that country from a standing start. Following the relocation of the outsourced manufacturing capability to Hungary last year, the plan is to have deployed 6,000 laundry units in Europe by 2020.

The group continues to operate over 5,000 digital printing kiosks, primarily in France and Switzerland and is currently upgrading the estate to the latest technology to accept all models of memory cards and smart phones. A new Starck designed kiosk was unveiled in November last year which is a new generation with no real comparator which the board considers to be very promising and the product should be launched over the next few months. The group is also looking to introduce 3D technology into its photobooth and as an example of this, they have started to introduce 3D figurine booths. Another new concept is Photolight, a solar-powered streetlight that has been under development over the past couple of years which is now beginning to be marketed more widely. Additionally, the carwash concept is still under trial with the initial results being encouraging – during 2016 the group expects to scale up the trials.

The operating profit at the UK and Ireland division was £8.5M, a decline of £1M when compared to 2014. Growth in photobook numbers was just 1% year on year while there was a 30% reduction of the amusement machines which are not material to the group’s business. With the market background remaining difficult, turnover in the region was flat. The group rolled out 32 laundry units in Ireland, where results to date have been promising as they are currently the highest earning machines in the portfolio.

The group is looking to increase its contactless systems deployment programme to improve the customer offering and is also considering expanding into new Asian markets and the US. South Korea is one new market and small operations have now been launched in Poland. Many of the KPIs are various different iterations of revenue and profits but underlying EBITDA margin is up 3.6% to 29.2% with the other indicators being a slight slowdown in the number of photo booths being opened to 916 and an increase in the rate of laundry machines being added at 525 this year.

Going forward, although the continued strengthening of Sterling against both the euro and the yen will likely have an adverse effect in the coming year, the board expects another year of strong underlying progress next year. As well as foreign exchange risks, I guess the other big one is the potential for a government to implement centralised image capture for biometric passports and other applications which would seriously affect profits if it occurred in a big market such as France or Japan.

At the current share price, the shares trade on a P/E ratio of 21.7, falling to 20.7 on FinnCap’s estimate for next year which looks expensive but doesn’t taking into account the huge cash pile. After a 30% increase in the total dividend this year, the shares have a dividend yield of 3.4% which is nice to have but on FinnCap’s estimate for next year it is down as an incredible 7.9%. This seems almost like it could be a mistake but perhaps they are guessing what the special dividend might be and if this figure is correct, these shares look very good value indeed. I suppose this has stemmed from the comment from the Chairman that having raised dividends substantially in recent years, the board intend to increase the ordinary dividend by 10% per annum and any net cash on the balance sheet at the year-end in excess of £50M will be spent on a special dividend. At the year end the group had a net cash position of £60.7M, a decline of £2.4M year on year.

Overall then, this has been another good year of progress for the group. Profits were up, as was operational cash flow with a good level of free cash covering the generous dividend. We did see net tangible assets fall slightly, however, but the balance sheet remains strong. Asia did well this year and the new photo ID legislation in Japan should provide some good earnings growth in the next few years. Europe is also doing well and would be doing even better were it not for the weakness of the Euro. The UK is probably one of the weaker areas at the moment but that region is still profitable, Going forward, although penetration in the more mature markets means that photo booth growth will probably be limited, the roll out of the laundry machines looks exciting and the new style photo booths should also add something to the group.

The strength of Sterling against the Euro and Yen is likely to continue to drag on results going forward but with the potential of some good payments to shareholders going forward, I am very comfortable to have Photo-Me as my largest shareholding.

It’s fair to say the share price has not got anywhere in a year and in recent months I think it has been suffering from exchange rate worries but these results might help stop the rot.

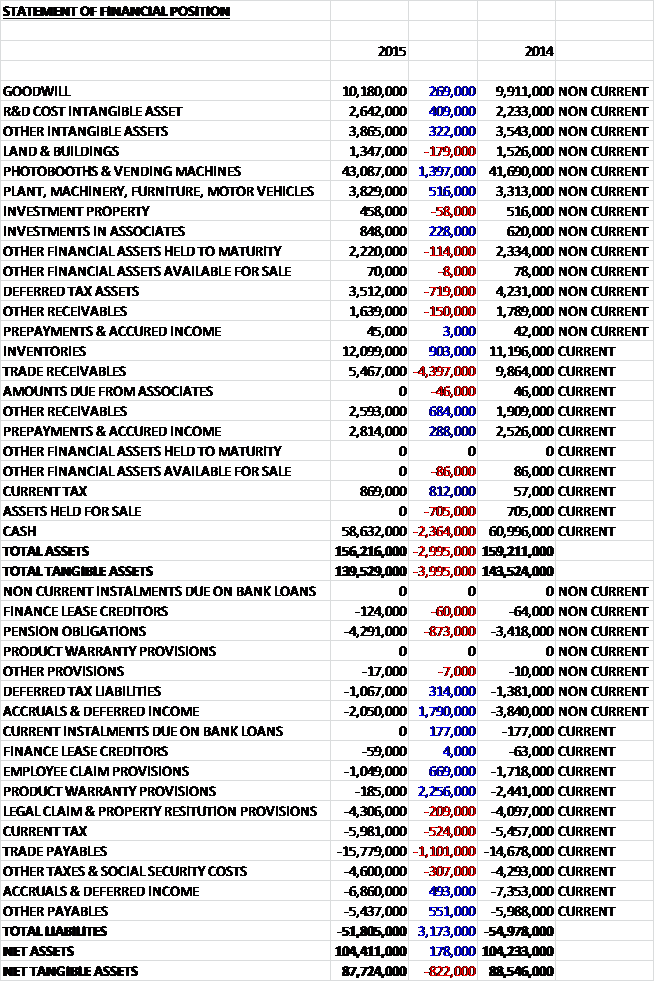

Photo-Me has now released its annual report. There is not really that much detail in the income statement but we do see that the fall in financial costs was driven by a £304K reduction in investment provisions. The statement of financial position, as usual, gives us some more useful information though.

We can see that the in property, plant and equipment was mostly due to a £1.4M increase in photo booths and vending machines and the fall in receivables was driven by the £4.4M decline in trade payables. As far as liabilities are concerned, the decline in provisions was due to the £2.3M decline in product warranty provisions and a £669K fall in employee claim provisions. As far as payables are concerned, the increase was driven by a £1.1M growth in trade payables.

Something else of interest that tends to be included in the annual report but not the preliminary results is operating leases, or in the case of PHTM, site owner agreements. Operating leases outstanding are fairly modest, being just £3.9M at the year-end but site owner agreements, which enables the company to site its machines, was £20.2M which is rather more material but given the cash levels at the company no cause for concern at all.

During the year the group acquired Copyphot based in Switzerland for £422K, representing goodwill of £513K (there was a negative net asset value). The group also disposed of its 51% interest in the Hungarian subsidiary for £80K.

On the 27th August it was announced that Francoise Coutaz-Replan had retired from her position as finance director from today. Mr. Gabriel Pirona has been appointed as interim finance director but he will not join the board at this time. Francoise will continue as a non-executive director of the company. I have to say this is an unwelcome announcement. Why has she resigned, are they looking for a permanent replacement, will the finance director continue to be an executive position? Normally, a sudden retirement by the finance director would really set alarm bells going but the fact that she is remaining as a non-exec does temper this somewhat so I am not sure it is that sinister, but it is a bit of a clumsy announcement in my view.

On the 21st October the group released an AGM statement covering the first four months of the year. Turnover improved by 4.4% on a constant rate of exchange (probably fell on actual exchange rates then) and pre-tax profits at a constant exchange rate were over 10% ahead and the board remains confident of the outlook for the full year.

The expansion of the laundry business in Europe is increasingly contributing to the financial performance of the business. In France, over 1,000 units have been deployed, delivering a very encouraging performance with the more established units continuing to deliver year on year revenue increases. In other countries such as Ireland and Portugal, the laundry business represents some 50% of recent months’ revenues in these countries. The laundry roll-out overall continues in accordance with the stated plan.

The group have agreed a three year period of exclusivity for carwash systems in the retail in market in France with Karcher with the initial focus being on large supermarkets. Since the agreement in August, four Karcher units have been deployed. Those units are preforming well and after investing in some 40 further units in the coming year, the group will re-assess the opportunity for further expansion at the end of 2016.

The group’s cash generation remains strong, trending ahead of last year’s performance.