Wynnstay manufactures and supplies agricultural products to farmers and the wider rural community in Wales, the Midlands, Lancashire and Yorkshire. The group has two main segments. Agriculture involves the manufacturing and supply of animal feeds, fertilizer, seeds and associated agricultural products whilst Specialist Retail involves the supply of a wide range of specialist products to farmers, smallholders and pet owners.

Within the agriculture division, there are a number of businesses. The Feed division operates two compound feed mills and one blending plant. Both mills can produce multi-species products. Glasson operates Glasson Dock near Lancaster and has traditionally been a raw materials trader and fertiliser blender. Their activities now include the packaging of added value products supplied to specialist animal feed retailers. The business is also involved in a joint venture, FertLink, which has production facilities at Birkenhead and Goole.

The Arable division supplies a wide range of products to arable and grassland farmers. It is a significant supplier of fertiliser, acting as a principle supplier of GrowHow and Yara products together with its own Top Crop brand. Seed is processed in Shropshire at the arable base as well as Woodhead seeds in Yorkshire. Agrochemicals are also supplied by the business. Grainlink is the group’s in-house grain marketing company and provides farmers with an independent professional marketing service. Woodheads seeds operates a seed processing plant near Selby in Yorkshire supplying a full range of cereal and herbage seeds to farmers and wholesale customers. It also trades grain and supplies fertiliser to farmers.

The retail division covers Wales, the Midlands and Lancashire. There are three main businesses within the division. Wynnstay Stores provide a comprehensive range of products for farmers and rural dwellers and now numbers 42 stores. Just for Pets is based in Worcestershire and consists of 20 specialist pet product stores from Cambridge to Bristol. Two stores also have an easipetcare concession offering vet clinic advice and services to customers and six stores include vaccination clinics. Youngs Animal Feeds manufactures equine and small animal feeds from its facility in Staffordshire. It also acts as a distributor of products to the equine market through wholesalers and retailers in the West of the UK.

The company is listed on the AIM exchange and it has now released its final results for the year ended 2014.

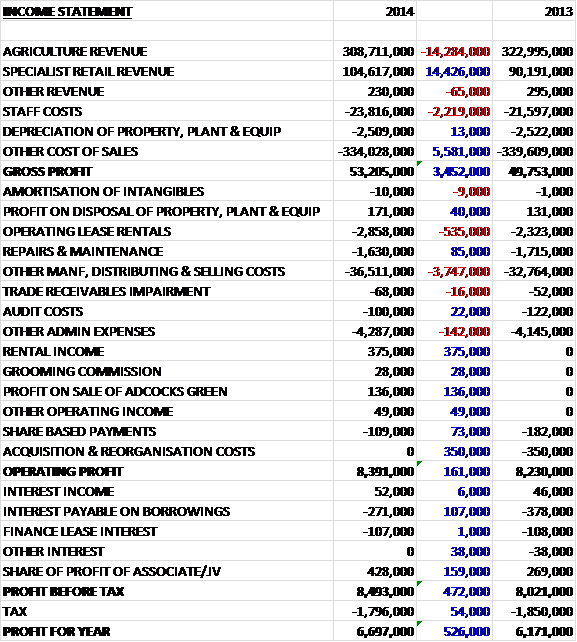

Revenues were broadly flat year on year as a £14.3M reduction in agriculture revenue was offset by a £14.4M increase in specialist retail revenue, which was boosted by the contribution from Carmarthen & Pumsaint which was acquired in 2013. Despite an increase in staff costs, cost of sales fell when compared to 2013 to give a gross profit £3.5M higher at £53.2M. We then see a £535K increase in operating lease rentals and a £3.7M growth in other manufacturing, distribution and selling costs partially offset by £375K or rental income and various other small income sources that did not occur last year. The lack of £350K worth of acquisition costs that occurred in 2013 pushed operating profit £161K ahead of last year, however. We then see a reduction in interest payments as borrowings came down and an increase in the share of profit from the associate and joint ventures before a slightly lower tax bill meant that the profit for the year was £6.7M, an increase of £526K year on year.

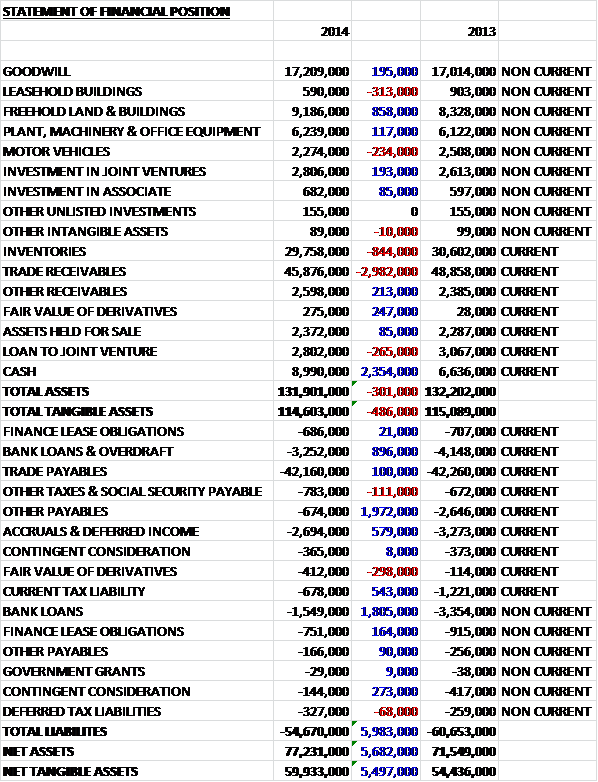

When compared to the end point of last year, total assets fell by £301K as a £3M decline in trade receivables and an £844K fall in inventories were partially offset by an £858K increase in freehold land and buildings and a £2.4M growth in cash. Total liabilities also fell during the year due to a £2.7M decline in bank loans and overdrafts, a £2M fall in other payables and a £579K decrease in accruals and deferred income. The net result is a £5.5M increase in net tangible assets to £59.9M which looks good to me.

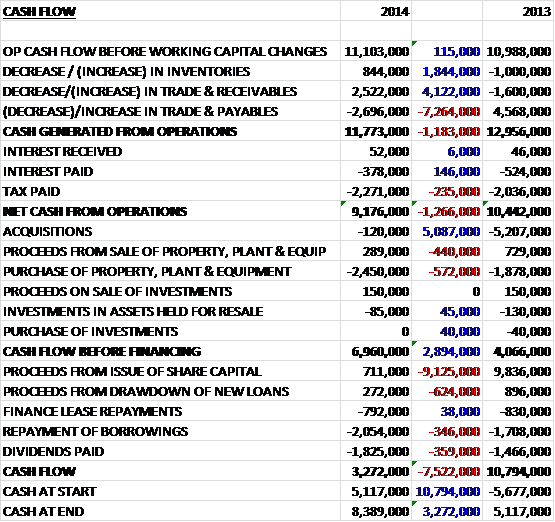

Before movements in working capital, cash profits increased by just £115K to £11.1M. A decrease in payables was more than offset by falls in inventories and receivables, driven by commodity deflation, to give a cash generated from operations of £11.8N, a £1.2M fall year on year due to the negative swing in payables. After tax and interest, the net cash from operations stood at £9.2M, a £1.3M fall when compared to last year. This was more than enough to pay for the capital expenditure and before financing, there was a free cash flow of nearly seven million pounds. The group used this to pay off finance leased and borrowings and to pay a dividend of £1.8M which meant that for the year as a whole, there was a cash inflow of £3.3M and a cash pile at the year-end of £8.4M – this looks pretty good to me, although the finance director helpfully points out that this represents an artificially high number and the group moves into short term debt at certain points of the year. This is true for most businesses and it is refreshing to see this being specifically pointed out in this case.

During the year there was a significant variation in yields of agricultural outputs which led to a reduction in commodity pricing over the last year. Deflation was particularly evident within the agricultural division where, despite an overall increase in volumes of trade, revenues reduced by 4%. Average manufactured freed prices were some £14 per tonne lower across the year while fertiliser and grain prices averaged falls of £22 and £46 per tonne respectively.

Profit in the agriculture division was £3.8M, a decline of £1.1M year on year as margin pressure on agricultural inputs and lower than expected market activity in fertiliser and grain in H2 put pressure on margins. Results for the year also reflected the mild weather conditions of the winter which contrasted significantly to those experienced in the previous winter. A return to more normal weather patterns from Spring benefited crop production, resulting in good grazing and forage production for livestock farmers as well as high yields for many arable units.

Demand for ruminant feed has been lower this year against the prior year, mainly due to the mild weather and lower milk prices. It was a story of two halves for the feed products business, though, as a 2% fall in sales in the first half of the year was followed by strong sales in the second half. There was a notable rise in blended products which offset reduced sheep feed volumes in early spring. The group’s investment in production facilities improved efficiency which contributed an improved performance in manufactured feeds.

After two years of outperformance, the contribution from Glasson was below the level of the last two years. This reflected reduced margins across both the raw materials trading and fertiliser activities. Volumes in raw materials were buoyant, however, as feed manufacturers sourced alternative raw materials to replace UK grain which was in short supply following the poor 2013 harvest. Fertiliser sales increased during the year but sales at Fertlink in the latter part of the year were lower as farmers held back from buying for the 2015 cropping year.

In arable products, sales of cereal and herbage seeds over the year reached record levels but margins came under pressure as a result of the reduction in grain prices across the industry. Fertiliser sales in the division increased by 19% year on year, benefiting from CPF’s first year of full contribution. Demand was buoyant in the spring as farmers embraced ideal growing conditions but tempered in the autumn with reduced margins. The UK grain harvest was good in 2014 and while this brings opportunity for the GrainLink and Woodheads grain trading teams, the fall in grain prices in the autumn to levels last seen in 2008 has meant that farmers have been reluctant to sell. It is therefore expected that a high proportion of the volume will be marketed during the 2015 financial year.

Profit in the specialist retail division was £4.9M, an increase of £500K when compared to last year. These results benefited from the first full year’s contribution from CPF with the business moving into profitability in the second half as expected. The acquired network of stores in SW Wales have now been fully integrated. Just for Pets has seen pleasing like for like sales growth. Since the year end the group has added two new stores to the Wynnstay stores network, one in Aberystwyth and one in Ross On Wye. These additions take the number of stores up to 42 and further extends their geographic reach.

On a like for like basis, Wynnstay stores saw a 2% increase in sales compared to the 25% seen including the new stores. They have introduced some new products such as large-scale ventilation and lighting systems for dairy units and a growing range of hardware products. These have apparently been well received and have contributed to the stores’ performance this year. The Just for Pets stores have benefited from the marketing initiatives implemented over the past two years and has seen consumer sentiment improve with average spend increasing over the year and contributing to a 4.5% increase in like for like sales. The number of outlets currently stands at 20 stores with an additional store expected to be opened in the spring of 2015. The Youngs Animal Feeds business has performed well, maintaining its position in the market.

Other profits were £250K compared to losses of £386K in 2013 which might include £108K worth of profit from the petroleum products associate, Wynnstay Fuels ltd (£69K last year). All joint venture and associate businesses have performed in line with management expectations.

There were a number of board changes over the year. Howell Richards has joined as non-executive director. He has some 30 years’ experience in the agricultural sector and has established one of the largest dairy farms in the UK. He replaces Jeff Kendrick who retired after an incredible 25 years of service. It was also announced that Lord Carlile will be retiring having been a non-executive director of the company for over 16 years – the non-execs here certainly spend a decent amount of time with the company. It is good to see that the board are not on a gravy train here with their salaries at a sensible level. For the most part they seem to be farmers with the exception of the Chairman who has a background in retail and currently CEO of Poundland – he should be quite an asset.

During the year the group completed the purchase of Mansell Powell Suppliers, a supplier of agricultural goods based in Herefordshire, for an initial consideration of £154K with a further £75K of contingent consideration. The acquisition generated goodwill of £195K and extends the group’s geographic trading area and farmer customer base as well as adding an additional outlet to the country store chain. The group have stated that their strategy involves geographic expansion and organic growth.

The group is already contracted to spend some £598K in capital expenditure next year and will be investing in their IT sand management systems over the coming year. Also, after the year end the group completed the acquisition of Ross Feed Ltd, a supplier of agricultural and hardware goods based in Herefordshire for a total potential consideration of £501K which includes £60K of contingent consideration. The acquisition generated £312K of goodwill and profit before tax last year was £123K. The business extends the group’s geographic trading area and adds an additional outlet to the country store chain. This looks like a good value acquisition to me if that profit figure was not a one-off.

Whilst Wynnstay is not really affected by interest rate changes and exchange rates, although relevant to raw material prices, are not a huge risk, they are susceptible to changes in commodity prices, particularly with regards to the animal feed manufacturing activities and some wheat futures contracts are used to manage exposure.

Going forward, long-term prospects for the UK agricultural industry remain buoyant but shore term issues have arisen as a result of the decline in output prices. The changes to the Common Agricultural Policy will also bring further changes to the industry, including some short term challenges. The industry remains driven by climatic conditions with the resultant price volatility but while output prices for farmers are currently weak, especially for the dairy sector, increasing global food demand should drive a return to more “realistic” prices.

At the current share price, the shares trade on a PE ratio of 16 which falls to 15.5 next year which is not exactly bargain territory but not too bad. After a 10% increase in the total dividend, the dividend yield currently stands at 1.8%, increasing to 1.9% on next year’s consensus forecast – again not bad, but not that great either. At the year end, the group has a net cash position of £2.75M compared to net debt of £2.5M at the end of 2013 and there is some £14.8M of operating leases off the balance sheet.

Overall then, this seems like a decent update. Profits increased but they did seem to be flattered by a few one-off items and there was a decent level of free cash generated, despite the underlying operational cash flow only showing modest improvements year on year. There was a good growth in the net tangible asset level and the balance sheet does look very strong here. Operationally, the two divisions experienced different trading fortunes. The agriculture business is suffering somewhat with low output prices as the price of raw materials, particularly grain, and fertiliser fell. The retail side is doing rather better with the pet store in particular looking promising with a decent level of like for like growth.

The shares do not look a bargain on a PE level or a dividend level and this company is susceptible to commodity prices and weather which are both out of their control. Having said that, the performance seems solid enough and the balance sheet looks very good. This could be one to tuck away on weakness perhaps?