Conviviality Retail has now released its final results for the year ending 2015.

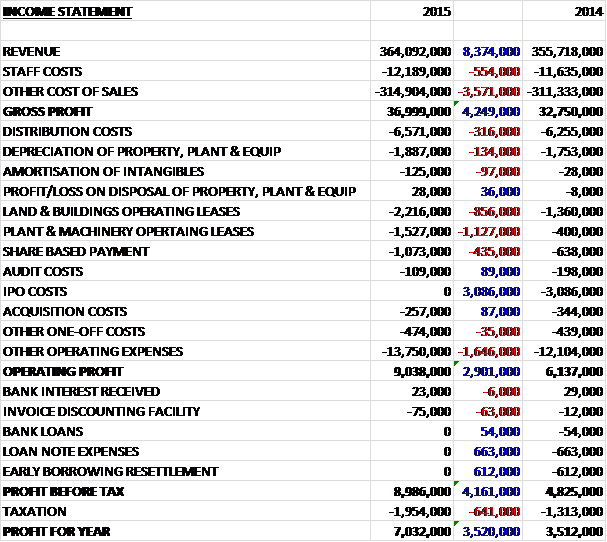

When compared to last year, total revenue increased by £8.4M and with a smaller increase in cost of sales, aided by nearly £1M worth of lower receivables impairments, gross profit was up £4.2M year on year. We then see distribution costs increase by £316K and operating leases up a considerable £2M when compared to last year. There was also a £435K increase in share based payments due to the awarding of options to franchisees, and a £1.6M growth in other operating expenses due to the increase in owned stores. This was offset by the lack of £3.1M worth of IPO costs that occurred last year which meant that operating profit was ahead to the tune of £2.9M. There were also a host of one-off finance costs that did not recur such as the £663K loan note expense and the £612K relating to the early resettlement of borrowings. After a £641K increase in tax the profit for the year stood at £7M, an increase of £3.5M, but if we discount a lot of the one-off costs incurred last year, the underlying profit is actually below that of last year.

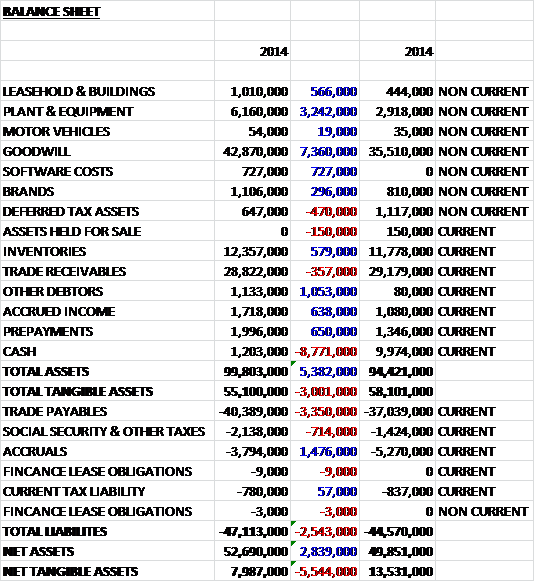

When compared to the end point of last year, total assets increased by £5.4M driven by a £7.4M increase in goodwill, a £3.2M growth in plant and equipment and a £1.1M increase in “other debtors” partially offset by an £8.8M fall in the cash level. Liabilities also increased during the year as a £3.4M increase in trade payables and a £714K growth in social security and other tax payables was partially offset by a £1.5M fall in accruals. The end result is a £5.5M decline in net tangible assets to £8M.

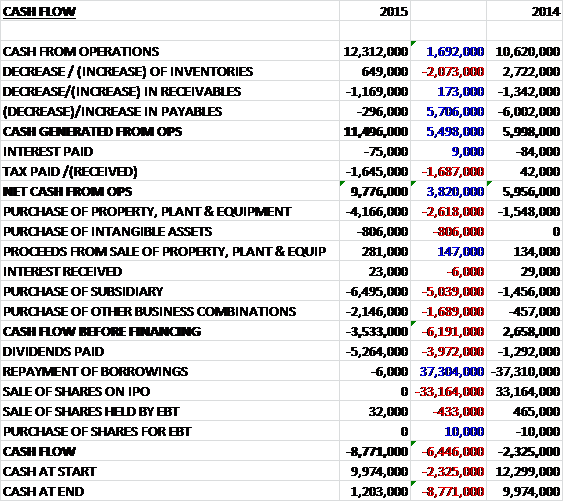

Before movements in working capital, cash profits were £12.3M, an increase of £1.7M year on year. This was eroded somewhat by working capital movements but when compared to last year, the fall in payables was much less pronounced and the cash generated from operations increased by £5.5M to £11.5 which then became £9.8M after tax (no tax was paid last year for some reason). Of this cash, the group used £4.2M to purchase fixed assets and £806K went on intangible assets which gave a free cash flow of just over £5M. This was not enough to cover the £5.3M of dividends and certainly not enough to pay for the £8.6M of acquisition so the cash outflow for the year was £8.8M to leave just £1.2M in cash at the year end.

The group saw more than 20 existing franchisees open new stores during the year and the number of stores owned by multiple franchisees increased by 22%. For the last two years, the group has embarked on a major restructuring of their franchisee base but this programme has now come to an end, arresting the number of store closures with total store numbers increasing by nearly 5% to 624. The franchisees are obviously very important for the structure of the group and some 94% of all goods purchased by them are sourced from Conviviality. The group offer a franchisee share scheme to help encourage loyalty with up to 3,500 shares offered per store for achieving annual standards targets and this year some 1.4 million share options have been allocated with almost £900K offered through the overrider scheme to the franchisees. Over the past year, 35 new franchisees have joined the network.

The group are continuing to expand their geographical coverage and have identified the North East, Yorkshire, the SW and Scotland as priority target areas. In the North East, the group expects to expand through a combination of current and new franchisees, the Rhythm & Booze acquisition took care of Yorkshire and the GT News acquisition builds their presence in the East Midlands. Their ambition to grow in Scotland is being pursued via a trial with Scotmid to franchise stores. This trial is apparently showing some positive early signs and the first stores has opened in Stevenston, followed by Annan with further stores to be opened during this month.

Conviviality seems to be doing well with engaging with its customers. They have the highest number of active Facebook fans in their sector with some 68,000 and they actively use social media to communicate offers and promotions. In April they piloted their Click and Collect service and rolled this out to their franchisees. The group have also updated the image of their brands with the roll out of the new fascias that is nearing completion with the completed stores showing a 1.3% sales differential after the change. They have also launched an app that has been downloaded over 30,000 times that can be used to redeem offers.

As far as products are concerned, the group now have over 70 premium bottled ales and over 20 craft ales in their range. The spirits range also continues to improve and there is a focus on the growing trend for premium and flavoured spirits. The wine buyers have also been strengthening their category and sales of wine have increased 10% year on year. On average the off-license range has been 12% cheaper than the competition despite the heavy discounting experienced in the market.

The group has made significant investments during the year to become more efficient and have modernised the Crewe warehouse without any disruption in trade to ensure the flow of the warehouse is as efficient as possible and poised for further growth. They have also undertaken maintenance works and refurbishments to their corporate stores, ensuring that they are an attractive for transfer to franchisees. At the end of March the full transport operation of 160 drivers and staff from the third party provider CVL have been taken under the control of the group. It is expected that this operation will improve service levels to the franchisees. Going forward, the group is initiating a programme of space optimisation in the stores which should be completed by the 2016 financial year.

Within the flat retail sales, the 0.4% increase in the average number of stores was offset by a 0.5% reduction in sales per store due to the lower sales from the two acquisitions. Retails from the Bargain Booze stores that had traded throughout the year were 0.5% higher than from the stores that traded throughout the previous year as the quality of the estate improved, although apparently overall like for like sales fell by 1.7%

During the year the group made a couple of acquisitions. RNB Stores was purchased for £1.8M in cash and came with 31 shops. The acquisition generated £1.4M of goodwill and contributed £700K to the group’s profits this year with some £700K being spent on refitting the stores. In February the group also acquired GT News Group for a cash consideration (including costs) of £6.7M which generated goodwill of £5.7M. The acquired group is a convenience retailer that operates 37 stores in the East Midlands and Yorkshire. From the date of acquisition, the stores did not contribute to profits but if they had been acquired at the start of the year, they would have contributed about £800K. This did not come that cheap but it should add value to the group going forwards.

Following the acquisition of GT News, Jonathan James, the former chairman of the Association of Convenience Stores entered into a ten year franchise agreement, taking control of 36 stores from the acquisition. There were some board changes during the year. Andrew Humphreys joined as CFO and Amanda Jones joined as COO. After the year-end the group also appointed Ian Jones as a non-executive director.

Going forward, the group plan to leverage their wholesale capability into new markets. By acting as a wholesaler to their franchisees, they have built relationships with their suppliers and understand the market dynamics and plan to embark on some corporate accounts. Now that the realignment and closure of poorer quality stores has been completed, the group should be well placed for growth in the coming year.

At the current share price, the shares are on a PE ratio of 15.4, reducing to 13.2 on next year’s forecast which seems about right. After a 5% increase in the final dividend, the yield stands at 5.4%, increasing to 5.5% in 2016, which is a very good pay-out. At the year-end the group had net cash of £1.2M although it is worth nothing that there are some £16.2M of operating leases outstanding off the balance sheet so whether the group really is in a net cash position is debatable.

Overall this year seems to be one of fairly slow progress for the group. Profits were up but when we strip out the one-off costs relating to the IPO last year, underlying profits actually fell year on year. Net tangible assets also fell with cash being used to pay for goodwill and the balance sheet is not looking that great really. At least operating cash flow increased, both actual and underlying but this was not enough to cover the costs of the acquisitions and not quite enough to even cover the dividend, which is yielding an impressive 5.4%, although how sustainable it is has to be open to debate so up to now, pretty uninspiring stuff. All this is irrelevant, however, as the shares are suspended due to the earlier announcement that the group is looking to reverse takeover Matthew Clark, an alcohol distributer. If the deal goes ahead it will be genuinely transformational so the investment case will totally depend on the details of that – more of that to come at some point in the future.

The group has now confirmed that it has entered into an agreement to acquire Matthew Clark from the Accolade Wines Group and Punch Taverns for a total cash consideration of £198.4M. Matthew Clark is a UK based alcohol and soft drinks wholesaler which primarily serves the non-tied on-trade market via a national distribution network. Over the past year, they have delivered to about 17,000 premises that have included pubs, bars, hotels and restaurants and generated an EBITDA of £25.3M and a post-tax profit of £13.4M after £4.4M of exceptional items. The acquisition is being funded by a £130M placing and £80M to be drawn under new banking facilities. Appropriate working capital facilities of up to £92.5M will be in place for the enlarged group to cover seasonal and intra-month fluctuations in working capital.

The directors believe that the increased scale of the enlarged business will increase its buying power, enabling buying synergies to be achieved. In addition, combining the two businesses has the potential to realise distribution, operational and revenue synergies. The acquisition is expected to be earnings enhancing from the first full year of ownership. It is estimated that the net debt of the enlarged group will be about £80M, excluding any amounts drawn under the revolving credit facility. The group will incur advisers’ fees, commissions and expenses of about £7.5M in connection with the acquisition, placing, admission and new banking facilities.

Andrew Humphreys, the group’s CFO has been granted an option over 149,519 shares. It has an exercise price of 155p and a three year vesting period. Some £130M is being raised by way of a placing of 86,666,667 shares at a price of 150p. These new shares will represent nearly 56% of the enlarged share capital which will stand at 154,943,024 shares in total.

The group has also included a trading update where it stated that since the end of the year, both Conviviality and Matthew Clark have traded in line with management expectations.

On the 12th November the group announced a trading update covering the first half of the year. The revenues for the period were 38% ahead of last year at £252M and 4.4% higher excluding the impact of the acquisition. The retail business generated revenues of £191M, an increase of 0.4% but a decline of 1.3% on a like for like basis, although the Wine Rack stores performed well with like for like sales up 5.3%. Matthew Clark generated revenues of £61M over the month or so since acquisition, an increase of 4% year on year and good progress is being made integrating the business with the synergy sales on track. In all, the group continues to perform in line with market expectations.

On the 26th January the group announced that David Robinson has been appointed as MD of Conviviality Retail. He joins from the Home Retail Group where he was COO of Argos. They board have also appointed Mark Simmonds as Commercial Finance Director for Conviviality Retail. He joins from Mitchells and Butlers where he was Director of Financial Planning and Analysis.