Entu sells replacement windows, double glazing, entrance doors, patio doors and exterior improvement products in the UK. They are listed in the AIM exchange after being brought to the market by Mr. B Kennedy, the previous controlling owner in October 2014. They have now released their full year results for the year ending 2014.

In the Home Improvement Products sector the group supplies a range uPVC double glazed residential doors, French doors and patio doors; a range of bespoke uPVC conservatories, garden rooms and orangeries in various styles and finishes, offering heat control systems and insulated roofs which prevent heat loss during cold weather; and roofline products that include uPVC bargeboards, cladding and soffits and fascias which form the frontage below the roofs and eaves of many homes.

In the Energy Generation and Saving Products sector the group supplies a range of energy efficient double glazed windows in various designs; solar photovoltaic panels which reduce energy bills and generate income for the customer via feed-in tariffs that pays the customer for each kilowatt of energy the panels produce; and a range of energy efficient boilers including combination, conventional and system boilers.

In the Eco Products sector the group provides cavity wall insulation that is a filling blown into the gap between the exterior walls of a house to reduce heat loss. They also provide external wall insulation which is an insulation system fixed to external walls of a property with mechanical fixings and adhesive. It is then covered with a mesh reinforcement, base coat and finally a decorative finish. The process significantly enhances the thermal insulation of a building whilst providing the added benefits of sound proofing, enhancing the exterior appearance of the home and damp proofing. Finally in the segment, the group provides loft insulation which works in a similar way to cavity wall insulation.

The Installation Partners division includes Job Worth Doing, which is the group’s national installation service that uses a network of self-employed tradesmen operating out of 14 service centres across the country. The services range from hanging a picture to installing a conservatory. The group acquires new customers through door-to-door canvassing, with 1,216 self-employed canvassers; internet marketing, which is becoming more important and is driven by the website; and media and internet advertising.

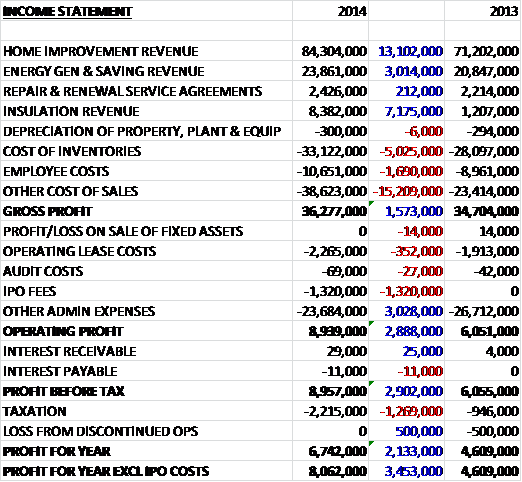

When compared to last year, revenues increased considerably with a £13.1M increase in home improvement revenue, a £3M growth in energy saving revenue and a huge £7.2M increase in insulation revenue from nearly a standing start. We then see cost of inventories up £5M, employee costs up £1.7M and other cost of sales up £15.2M which gives a gross profit some £1.6M higher than in 2013. There was a £352K growth in operating costs but a decline in other underlying admin expenses, partially offset by a £1.3M IPO charge to give an operating profit ahead by £2.9M higher and after a £1.3M growth in tax, the profit for the year stood at £6.7M, an increase of £2.1M year on year.

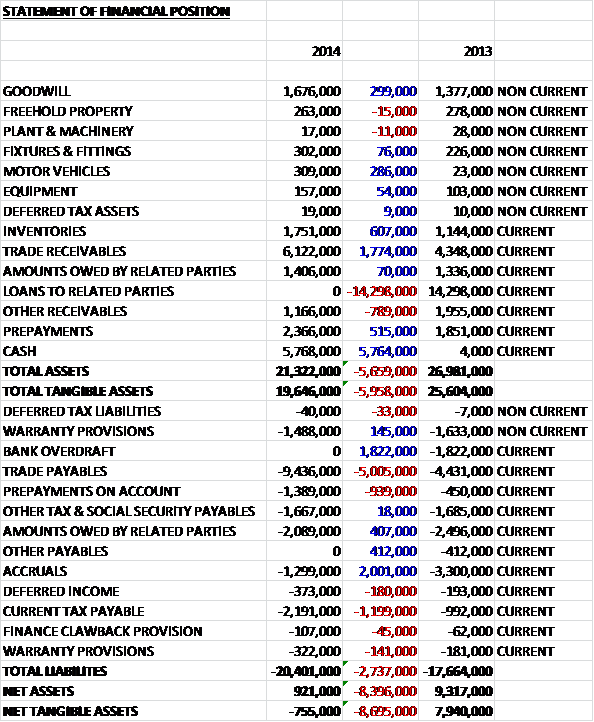

When compared to the end point of last year, total assets declined by £5.7M driven by a £14.3M fall in loans to related parties, which were waived when the company listed (the related parties were also controlled by the owners of Entu and included Sale Rugby club!– I am not sure I like that), partially offset by a £5.8M increase in cash and a £1.8M growth in trade receivables. Conversely liabilities increased during the year as a £5M growth in trade payables, a £1.2M growth in current tax payable and a £939K increase in prepayments on account was partially offset by a £2M fall in accruals and a £1.8M decline in bank overdrafts. The end result is an £8.7M negative swing in net tangible assets to a negative £755K which doesn’t look that great to me, despite the group stating they have a strong balance sheet (always a red flag). It is also worth noting that there are £8.9M worth of operating lease commitments off the balance sheet.

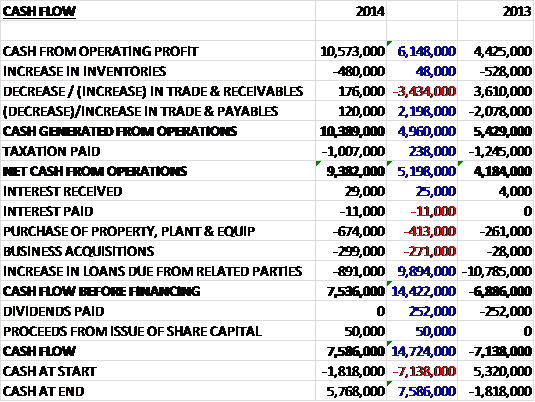

Before movements in working capital, cash profits increased by £6.1M to £10.6M. The increase in inventories was broadly offset by beneficial movements in payables and receivables and after the tax was paid, the net cash from operations was £9.4M, an increase of £5.2M year on year. There was not that much in the way of capital expenditure with £674K spent on fixed assets and £299K spent on acquisitions. After a £900K increase in loans due from related parties, the cash flow for the year stood at an impressive £7.6M to give a cash level at the year-end of £5.8M

Underlying operating profit at the home improvements segment was £3.8M, an increase of £200K year on year with a met margin of 4.5% (down from 5%), which represents an increase in market share, along with an improvement in consumer confidence that meant homeowners are more likely to make improvements to their home. The division was expanded during the year with the acquisition of the Europlas brand. Underlying operating profit at the energy generation and saving business was £1.8M, a huge jump of £1.6M when compared to last year. These products include solar photovoltaic installations, air to heat pumps, voltage regulators, remote heating controls and boilers.

Underlying operating profit at the repair and renewal service agreements business was £1.9M, an increase of £84K when compared to 2013. This segment is an annual warranty plan offered to customers on the vast majority of the group’s products and has a gross margin of 78.7%, down from 82.5% and about 60% of customers are members of the programme. Underlying profit at the insulation business was £2.7M, an impressive growth of £2.3M year on year. Products in this segment include cavity wall insulation, external wall insulation and loft insulation.

The board sees opportunities for growth in energy generation and efficiency products which are growing in popularity due to increasing consumer awareness, high costs of traditional home energy products and government incentives towards the adoption of green technology in the home. The general strategy is to grow by offering cross-selling a wide range of complementary products, including energy efficient windows, doors, conservatories, external and cavity wall insulations, solar power generation products and energy efficient boilers. It is thought that in the UK there are 24 million homes which could be suitable for loft insulation, 19 million suitable for cavity wall insulation and 27 million suitable for high efficiency boilers.

The group are currently developing a technology that will enable customers to monitor their energy usage online on a daily, weekly and monthly basis to understand where they are consuming most energy and how energy efficient products can save them money which Entu can then use to offer their energy assessments and bespoke energy efficient solutions. They are also actively seeking to grow their existing product line, especially in energy efficient boilers and in solar panel installations, and to capitalise on emerging trends by entering into partnership agreements with other players in the sector.

The previous owners, the Kennedys still own some 30% of the total share equity and CEO Ian Blackhurst and his family also owns about 15% with Darren Cornwall also owning more than 3% so it could be said that the executive directors’ interests are still aligned well with shareholders.

During the period the group acquired Europlas, a provider of home improvement products for a cash consideration of £299K, all of which was goodwill. The business contributed an astonishing £485K to profits since its acquisition in December so this looks like a great deal.

There does seem to be a high level of trade receivable impairments. This year, some £725K was impaired which is an incredible 11% of the total – is the company not making proper checks when it sells its products? This amount is based on the past default experience and the current economic conditions. The group does operate a defined contribution pension scheme and the total contributions during the year were £232K.

The current year has started well and trading is in line with management expectations. They are expecting continued organic growth through greater customer engagement and cross-selling as well as taking advantage of opportunities in the energy efficiency market. In addition, they will supplement this growth through the use of strategic acquisitions.

At the current share price, the shares trade on a cheap looking PE ratio of 9.4. I cannot find any forecasts for earnings going forward, I suppose it is still early days for this business. Net cash at the year-end stood at £5.8M compared to a net debt position of £1.8M at the end of 2013. The directors have declared a special interim dividend which yields 1.3% but they intend to pay a total dividend corresponding to a yield of 6.9% for 2015 as a whole, which is a spectacular return.

Overall then, this looks like an interesting potential investment. Profits increased year on year and the operational cash flow looks great, with plenty of free cash and a decent cash pile at the year end. On the other hand, net tangible assets fell considerably as related part loans were written off which leaves a negative net tangible asset base in this asset-light business. The energy saving and insulation divisions have done very well over the past year, growing very quickly. The shares look very cheap on a number of metrics, the PE is just 9.4 and the dividend yield is an incredible 6.9%. So, what’s the catch? Well, the market where the group operates in is very cyclical but it is in a sweet spot at the moment and the business is still very new – cobbled together and sold off just last year so this could be the peak of the performance.

This is perhaps a little cynical but the interim results are out shortly and I will wait to see what is said then before making a final decision.

It has to be said that the share price graph looks a little alarming too.