Martin & Co is a UK residential property franchise business whose franchisees operate from 282 offices and it is currently the 4th largest residential estate agency and lettings business in the country. Revenue represents the sale of franchise agreements, management service fees levied to franchisees monthly based on their turnover, and also the provision of training and ongoing support. The group listed on AIM in 2013 and it has now released its final results for the year ended 2014.

There are a number of brands in the MartinCo stable. Martin & Co itself earns 94% of its revenues from lettings and 6% through the estate agency business, although this grew by 138% year on year so is increasing in importance. Xperience was acquired during the year and was the property franchise arm of Legal and General and itself has four regional brands – Ellis & Co, Parkers, CJ Hole and Whitegates. Ellis & Co has 20 offices inside the M25 and one in Kent, CJ Hole is an estate agent with 19 offices throughout Bristol, Somerset and Gloucestershire; Parkers has 15 offices along the M4 corridor; and Whitegates is an estate agency with 36 offices across the North of England and derives about half of its income from lettings.

The group charges a management service fee of 9% on all franchisee fee income for Martin & Co franchisees and 7.5% for the acquired Xperience franchisees. A franchisee can only exit via a controlled sale to another franchisee approved by the group and a resale typically improves fee income of the business by 30% within a year of the change of franchisee.

Although the group is listed on AIM, the founder and current chairman has an interest of just under 50% of the company shares with the other large holders being various institutions. The CEO Ian Wilson also has a decent holding and the directors seem to be fairly sensibly remunerated.

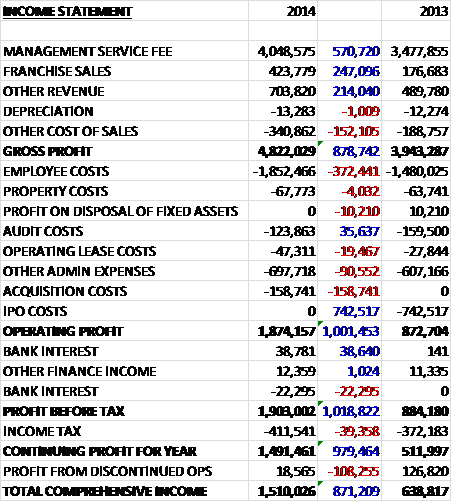

Overall revenues increased year on year with a £571K growth in management service fees (half organic, half from acquisitions), a £247K increase in franchise sales, through the introduction of 14 new franchisees, and a £214K growth in other revenues. Cost of sales also increased to give a gross profit some £879K ahead of last year. We then see a £372K increase in employee costs and a £91K growth in other admin costs reflecting the first full year of being listed, and with regards to non-underlying expenses, the group benefited from the lack of a £743K IPO cost that occurred last year but they did incur £159K of acquisition costs this year. After bank interest, a higher income tax and a profit from discontinued operations that fell by £108K, the profit for the year was 1.5M, an increase of £871K year on year

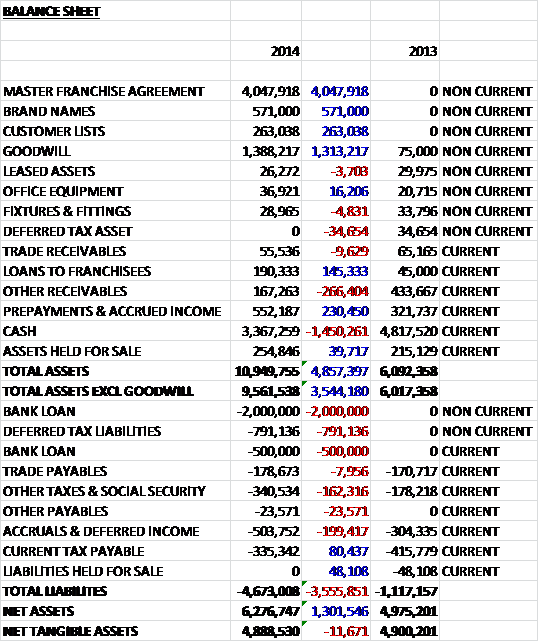

When compared to the end point of last year, total assets increased by £4.9M driven by the £4M master franchise agreement from the acquisition, which is being counted as an intangible asset along with an extra £1.3M increase in goodwill, partially offset by a £1.5M fall in cash levels. Liabilities also increased during the year due to a £2.5M increase in bank loans and a £791K deferred tax liability. The end result is a broadly flat net “tangible” asset level at £4.9M. On this occasion I have counted net tangible assets as being net assets without the goodwill, although it is debatable as to whether the customer list and the master franchise agreement is worth anything. The outstanding operating leases are fairly insignificant at just £61.8K at the end of the year.

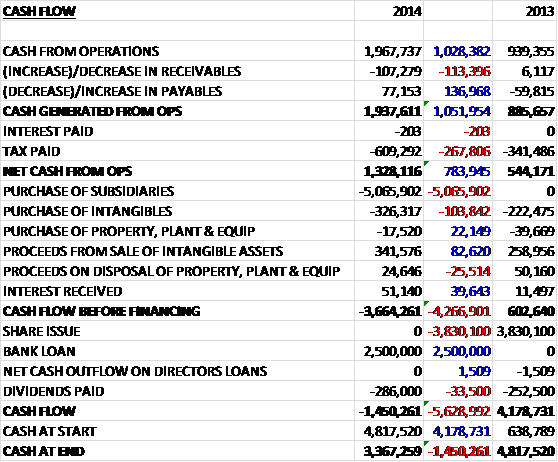

Before movements in working capital, cash profits increased by £1M to £2M. After an increase in both receivables and payables, the cash generated from operations stood at £1.9M and after tax this became £1.3M, an increase of £784K year on year. There was actually a net cash inflow from the purchase/disposal of intangible assets and no real capital expenditure to speak of but the acquisition cost £5.1M which meant that before financing, the cash outflow stood at £3.7M. The group then took out a loan of £2.5M and paid dividends worth £286K to give a cash outflow of £1.5M for the year and a cash level of £3.4M at the year end.

At the end of the year the group had 155 Martin & Co offices offering an estate agency service alogn with 88 Xperience estate agency offices. The estate agency business achieved a 138% year on year increase in management service fees with the number of sales increasing from 597 last year to 1,355 this year, and the directors believe that there is a significant potential for further development of this income stream, although the roll-out is now almost complete. The franchisees acquired 845 properties to the total being let in a number of small scale acquisitions and the acquisition added about 10,000 properties to the portfolio which grew to 42,177 at the year-end.

The board reckon that the burden of increasing government regulation in the sector means private landlords are more often turning to agents for professional advice but a more important factor is the rise of the internet property portals such as Rightmove which do not allow private landlord advertisers. The rental market itself is also forecast to increase considerably with estimates of a 7.4% annual growth in rents up to 2017. The management also believe that the pension reforms recently enacted will release pension funds that will be invested into buy-to-let properties and with net migration running consistently at 300,000 per annum and restrictions on mortgage lending affecting the young, it is the cash-rich older generation who can afford the 25% deposits on buy-to-let properties and there will be no shortage of tenants to occupy them.

During the year the group acquired Xperience Franchising and Whitegates Estate Agency for a net cash consideration of £5.1M, The group paid £4.1M for Xperience which included goodwill of £913K and a master franchise agreement worth £3.4M. The acquisition of Whitegates cost the group £991K in cash and came with £401K of goodwill and a master franchise agreement worth £653K. Since the date of the acquisition, Xperience contributed £100K in profit and Whitegates contributed £50K and had the acquisitions taken place at the start of the year, group profits would be some £900K higher so despite this being a lot of money for a company of Martin & Co’s size, this seems good value to me. It does seem as though, the deal took longer than it should have done to complete which apparently distracted the group from other opportunities.

The group has decided to discontinue the activity of owning and managing its own offices and this year an office in Worthing was sold, representing the last owned office with several offices sold the previous year. The group has deferred the income for some of these sales and the cash inflows this year were £365K and £252K of deferred consideration existed at the year-end.

During the year the group acquired its first portfolio of 374 managed lettings properties in Saltaire for £300K but portfolios that meet the group’s criteria have been difficult to find due to the sales price or issues with the quality of the portfolio. After the year-end these properties in Saltaire have been subsequently purchased by the franchisee that was managing them for £256K which resulted in a profit over its net book value of £1K (these are the assets held for sale on the balance sheet above). It is apparently still the group’s intention to acquire portfolios of managed properties going forward despite this sale but this element of the acquisition strategy will play a minor role for the foreseeable future.

At the current share price the shares trade on a PE ratio of 22.1 which seems rather expensive but falls to a more reasonable 15.5 on next year’s consensus forecast. The shares are currently trading on a dividend yield of 2.7% which is useful to have and is forecasted to increase to 3.2% next year. It is worth noting that there is still £300K of deferred consideration receivable at the year-end following the sale of the Worthing office and there is still £2.5M of unutilised loans available to the group for development and expansion of operations.

On the 7th May the group released an AGM statement and told the market that current trading is in line with expectations. The acquisition of the Xperience offices is producing the expected uplift in revenue and all of the franchisor functions for the five brands have now been successfully consolidated into one HQ with the associated restructuring costs being absorbed.

On the 13th May the group announced that it had appointed Phil Crooks as non-executive director who is currently a partner in forensic and investigations services at Grant Thornton.

Overall then, the results in the company’s first full year of listing seem pretty good. Profit increased, along with operational cash flow. There was next to no capital expenditure, instead the group seems to be expanding through acquisition and the cash from operations did not come close to covering the cost of that over the year. The balance sheet looks a little thin, depending on how the franchise master agreement is valued and the net assets remained fairly flat year on year. Current trading is in line with expectations and the new acquisition along with the estate agency work should drive an increase in profits. The forward PE of 15.5 is decent enough, as is the forward dividend yield of 3.2%. It should be noted that this company is a franchise seller really as opposed to a lettings agent or estate agent but it potentially looks quite interesting to me.

The shares have recovered from their low point at the start of the year and are now above the IPO price – this chart looks fairly decent to me.