Spectris has now released its interim results for the year ending 2015.

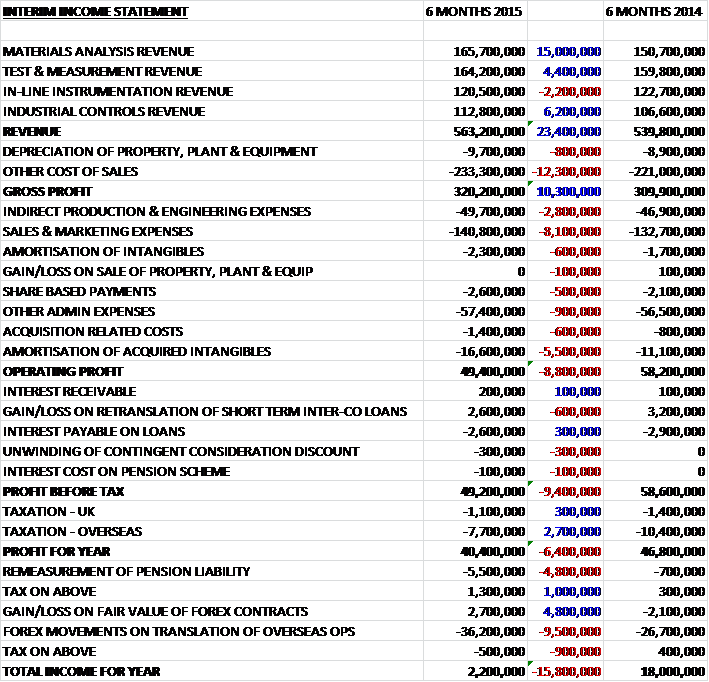

When compared to the first half of last year, revenues increased by £23.4M to £563.2M as a £2M fall in in-line instrument revenue was more than offset by increases in the other divisions, particularly the £15M growth in materials analysis revenue. Cost of sales also increased to give a gross profit some £10.3M ahead of last time. Indirect production and engineering costs also increased, up £2.8M and sales and marketing expenses were up £8.1M. We also see an increase in underlying admin costs along with a £600K growth in acquisition related costs and a £5.5M hike in the amortisation of acquired intangibles to give an operating profit £8.8M lower than in the first half of 2014. Finance costs increased slightly, mainly as a result of a fall in the gain on retranslation of short term inter-company loans but tax fell year on year to give a profit for the year of £40.4M, a decline of £6.4M when compared to last time. Incidentally this profit was almost entirely wiped out by the adverse effects of foreign exchange on the translation of foreign operations. Apparently profits are expected to be weighted towards the second half of the year.

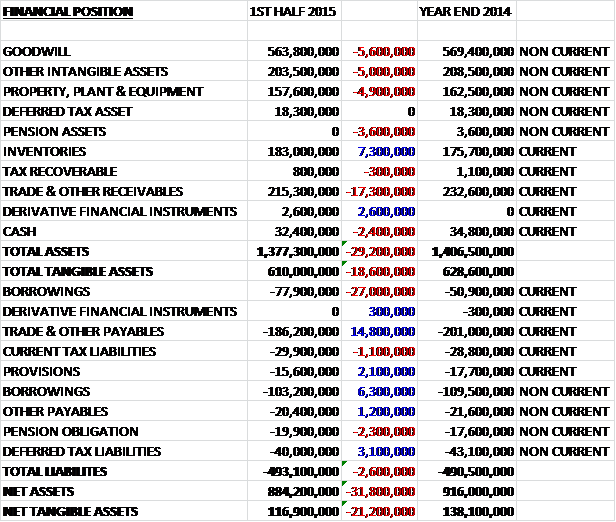

When compared to the end point of last year, total assets fell by £29.2M driven by a £17.3M decline in receivables, a £5.6M fall in goodwill, a £5M decrease in other intangible assets and a £4.9M fall in property, plant and equipment partially offset by a £7.3M increase in inventories. Conversely liabilities increased during the period as a £14.8M fall in payables and a £3.1M decline in the deferred tax liability was more than offset by the £20.7M increase in borrowings to give a net tangible asset level some £21.2M lower at £116.9M. Included in the above is £11.9M of deferred and contingent consideration.

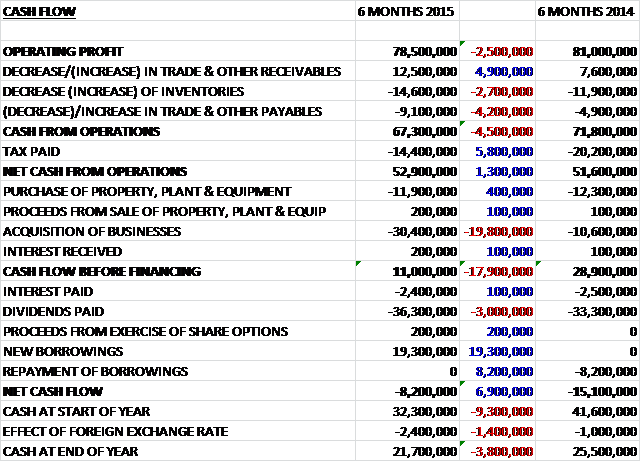

Before movements in working capital, cash profits fell by £2.5M to £78.5M. There was then a net outflow of working capital, driven by a £14.6M increase in inventories and a £9.1M fall in payables but the tax payment was some £5.8M lower than last year to five a net cash from operations of £52.9M, an increase of £1.3M year on year. The group then spent a net £11.7M on capital expenditure and £30.4M on acquisitions which, after an interest payment of £2.4M meant that the free cash flow stood at £8.6M, a fall of £17.8M year on year. This did not cover the £36.3M in dividends so the group took out £19.3M of new borrowings to give a net cash outflow of £8.2M in the first half of the year and a cash level of £21.7M at the period-end.

Regionally sales to North America declined by 2% representing a marked change to the strong performance in this region last year. Sales to China fell by 4% in the first half and, together with a 5% decline in Japan, these countries partially offset a good performance in India and South East Asia to give a 1% increase in sales to the Asia Pacific region. After a strong start to the year, sales growth in Europe moderated as the period progressed resulting in a 4% growth in the first half. Growth in the continent was broad based by industry but was held back by Germany where sales growth was just 1%.

The operating profit at the Materials Analysis division was £14.6M, an increase of £1.4M year on year due to the impact of prior acquisitions. Like for like operating profit fell by 10% as a result of the absence of a one-off R&D related government grant last year. Like for like sales grew by 4%, benefiting from continued good growth from pharmaceutical and fine chemicals and semiconductor customers, particularly in North America. There was a return to growth in the metals, minerals and mining sector, driven principally by the metals and minerals segments with mining demand remaining subdued. Sales to academic research customers declined year on year as fiscal budgets remained constrained in many markets.

Sales to the pharmaceutical sector grew with strong performances in North America, Germany and India helped by growing demand from biopharmaceutical and generic drug manufacturers. The investment in the development of products focused on the life science industry continued to yield results. The group secured a major contract with Novartis for their Viscosizer product which will deliver substantial cost savings to Novartis by enabling more cost effective pre-screening of its therapeutic antibody candidates before they enter clinical trials. Following the acquisition of MicroCal last year, the business has expanded its product range with the launch of the next generation of calorimeters targeted specifically at the life science market.

Within Asia Pacific, sales to Chinese pharmaceutical customers declined as the passing of Good Manufacturing Practice regulations in the country saw the end of a multi-year investment phase by Chinese pharmaceutical companies as they strive to achieve compliance. It is believed, though, that growth prospects remain good in this market over the medium term. Regulatory compliance is now a strong growth driver in India where the generic drug manufacturers are focussed on achieving the standards necessary to export to the US. The particle measuring business won a significant order from Merck for a facility monitoring system together with a multi-year service contract.

After a difficult year last year there was a return to growth in the metals, minerals and mining sectors in all major markets except China, where demand remains subdued in the face of over-capacity in mining and continued postponements and delays to large capital expenditure projects. Generally the growth in this sector is of an after sales nature with customers preferring to repair and support existing equipment rather than replace it. In contrast there is good growth in the cement and building materials markets, particularly in the US, Europe and Mexico.

There has been a major new product launch in the period, the Zetium X-ray spectrometer. This is the first machine in the market that combines several x-ray techniques together in one machine with easy-to-use software. The group have also launched CNA Pentos, a real-time cross-belt elemental analyser targeted at the cement industry and similar applications. Sales to academic research institutes declined, as governments remained fiscally constrained and public funding programmes were either exhausted or awaiting renewal. Notably the strong growth in the UK in recent years has stopped due to uncertainty surrounding the general election in the period.

Demand in the semiconductor sector continued the progress that began during the second half of last year reflecting more favourable market conditions and new product introductions. Growth was also benefited from the acquisitions made of the distributors for the particle measuring business in South Korea and Taiwan. An important new product released to market in the period was the Ultra DI-20 Liquid Particle Counter which counts and sizes contaminants as small as 20 nanometres.

The board expects this segment to continue to deliver robust sales growth in the second half of the year, notably in the pharmaceutical and semiconductor sectors, boosted by new product launches and the impact of acquisitions. Demand from the mining sector is likely to remain weak but the metals and minerals sector is expected to remain robust. There is expected to be some release of EU funding of research and development budgets in the second half which should lead to improved demand in the academic research sector and cost reduction measures have been taken in order to improve future profitability.

The operating profit at the Test and Measurement division was £18.7M, a decline of £700K when compared to the first half of last year. Sales to the automotive sector declined slightly, mainly due to the lack of large orders from North American customers that were seen last year, which offset continued good growth in Japan and modest growth in Europe. The quality of the in-car infotainment and communications systems continued to be increasingly important to car manufacturers whilst legislation is also driving interest in the group’s full-vehicle simulators that allow more efficient development of noise, vibration and harshness targets with Bentley placing a major order for the simulator during the period.

Sales to the aerospace industry increased despite the economic sanctions on Russia adversely impacting exports of satellite vibration test systems to that end market. There was a strong performance in North America where the group secured a significant order from Lockheed Martin for PULSE software analysers to test sound and vibration in its satellite systems. Whilst there were continued project delays in China there was good growth elsewhere in the Asia Pacific region and following a sizeable order last year, a major South Korean aerospace company placed a further large order during the period for satellite vibration test systems.

Sales to the consumer electronics market were down significantly in the first half of the year, reflecting a strong prior year period when major customers in the segment had particularly large projects in North America and China. There was strong growth in demand for the engineering software solutions in the period with customers increasingly seeking to use software to improve the quality, reliability and durability of their equipment and processes. Since the acquisition of ReliaSoft, the business has secured a number of significant contracts, notably an order worth around €600K from a major oil and gas producer in the Asia Pacific area for software to analyse system and field operational performance and identify opportunities to reduce downtime.

Sales of the environmental noise monitoring services grew in the first half of the year, driven by good growth in Europe. The group has made progress in diversifying away from airports and won a major contract with the Italian government for exhaust monitoring in their vehicle inspection centres. The relationship with AENA, the Spanish airports operator was extended to centralise systems across the six airports already served and to add new systems to further ones. In Australia, the noise monitoring service with the Australian Department of Defence has been expanded to a third military base.

At the end of last year, the group acquired ESG Solutions which was integrated into this division. The weakness in the oil and gas market is causing many producers to delay their investment plans which led to demand for ESG’s products reducing as the period progressed. Nevertheless, the business secured several contract wins against some competitors including a multi-million dollar project in the Marcellus field in the US. Good progress has been made extending ESG’s presence outside North America into China and Australia with the initial establishment of offices in the Middle East and Mexico also taking place.

The board expect the second half of the year to benefit from robust market conditions in the automotive and aerospace sectors, further strong growth in engineering software and the contribution from acquisitions. The microseismic monitoring market is likely to remain challenging through the rest of the year, however, and due to the uncertain nature of the outlook in certain markets, cost reduction measures have been taken in order to improve future profitability.

The operating profit at the In-line Instrumentation division was £13.8M, a fall of £3.5M when compared to the first half of 2014 which reflected adverse currency movements and the ongoing weakness in the graphic paper and coated paperboard markets, particularly in China. This was partially offset by strong growth in both the downstream petrochemicals and wind energy markets.

In the energy and utilities markets, sales were up strongly during the period. This reflected good growth in the downstream petrochemicals market and the wind energy market. In downstream petrochemicals, there was good demand from China where there remains a focus on the control and reduction of emissions, and from SE Asia, although the continued uncertainty in the oil and gas market is leading to fewer large projects being progressed. The group launched a major new product platform for the industrial gases market during the period, a laser gas analyser called MiniLaser. This is more powerful, smaller and lighter than other products on the market. In January, an oxygen variant was released to market aimed at the petrochemicals industry and in the second half they expect to launch an ammonia variant, targeted at the combustion and power markets.

Sales of wind turbine monitoring solutions to the renewables sector grew strongly, and the group have now sold over 10,000 condition monitoring units since shipments began 12 years ago. Following on from the contract win last year with EDP Renewables, similar contracts for the supply and retrofit installation of condition monitoring systems on wind turbines has been secured with Capstone Infrastructure in Canada and a major energy company in the US. During the period they also began offering a new “Condition Monitoring Systems as a Service” solution to customers. This is a complete retrofit of CMS for wind turbines without the customers needing to make an upfront capital investment. Instead, they lease CMS equipment from Spectris who then provide services such as fault detection and monitoring, diagnosis and maintenance during the duration of the contract. They also launched the Vibration Interface Module, a system that enables data and signals from any machine protection system to be processed, stored and analysed on a single CMS.

In the pulp and paper markets there were broadly similar trends as experienced during 2014. There was good growth from the tissue segment as more producers move to high performance creping blades and related services, and there was also growth within the pulp segment, reflecting a good reception to the new single point control sensor, as shown by a significant order received in Indonesia. These positive trends continued to be more than offset by weak demand for coating blades in the graphic paper and coated paperboard, markets, however, particularly in China where excess capacity remains. The new Phoenix coating blade technology, which provides better print quality and wear resistance than other products on the market, is gaining traction amongst the group’s customer base.

Sales to the web and converting industries declined overall, primarily reflecting a lack of the large projects and orders in North America and Asia Pacific that benefitted the first half of last year, together with weaker demand across Europe. Demand improved as the period progressed, however, in part reflecting the increase in new product development this year. For example, the group launched the InControl extrusion line controller to strengthen their position in the medical tubing and automotive cable markets, and the InfraLab e-Series meat analyser which provides measurement of fat, moisture, protein and collagen content in meat samples.

Going forward, the board are seeing good opportunities in the tissue industry for their consumable products such as creping blades, as well as for their process control instruments as manufacturers seek to improve their productivity and despite the challenges in the graphic paper and coated paperboard markets, they expect their new products to enable them to deliver some modest growth in sales to the pulp and paper market in H2. Demand from the energy and utilities sector is expected to remain strong, although growth rates are expected to moderate from the strong H1 level given a reduction in large projects in the downstream petrochemical industry. Cost reduction measures have been taken in certain businesses to improve future profitability.

The operating profit at the Industrial Controls division was £20.3M, an increase of just £100K year on year with the positive benefit from foreign exchange movements masking a sales decline, primarily due to a broad based slowdown in North American industrial demand together with the absence of major product development activity by consumer electronics customers.

Investment in the internationalisation of Omega is delivering good results with strong sales growth in Asia, led by Japan, where they have been operating for over a year. Growth was also strong in Mexico and Brazil and the expansion of the European business is progressing to plan. The North American business, in contrast, faced more challenging market conditions with a weak industrial manufacturing environment in the US.

During the year the group launched a new mobile compatible website for North America and established a technical learning section on all websites to enhance Omega’s reputation as a technology leader. There has also been an increase in the rate of new product introductions during the period, both through private label and internal development. In March they launched a major new series of temperature and process controllers which are targeted at customers in the laboratory, in factory automation and chemical industries. The ERP system is now in place throughout the Omega business with the exception of Europe and Mexico where they expect to launch in the second half.

The downturn in the oil and gas market, particularly in North America, led to a decline in sales of the Graphite series of display panels to that market after a strong performance last year. In addition, the industrial Ethernet business experienced fewer large orders from several other industries in the US such as the automotive market. In contrast the industrial cellular products continue to see good demand from the telecoms and utilities industries in North America and Europe. Following a significant order in 2014 from a major US telecoms service provider for cellular modems to enable its smart grid deployment, the group won a large industrial networking order during the period from a major US utility company, also to assist in smart grid deployment.

During the period the group enhanced their series of industrial cellular routers through the addition of SMS text messaging functionality to enable them to provide automatic alerts to operatives. In the UK a major food manufacturer has chosen Graphite display panels to improve data collection and operator productivity with the potential for the order to extend to their other plants outside the UK. The display panels have now also received certification to allow them to be used in hazardous environments in Europe, the Middle East, Africa and Asia, opening up opportunities in the oil and gas and mining industries outside North America for the first time.

After a strong finish to 2014, sales of track, trace and control products declined in the first half of this year, impacted by the industrial slowdown in the US and by reduced demand from a major electronics customer and its supply chain, mostly based in Asia. Demand for products in China remains strong, however, as more Chinese factories seek to increase the amount of automation in order to improve productivity. Progress for this segment as a whole in the second half of the year will be largely determined by the industrial demand environment in the US, albeit a beneficial impact is expected from recent and upcoming new product launches and improved demand from the electronics sector.

In January the group acquired ReliaSoft, a company based in the USA, for a total consideration of £30.4M, generating goodwill of £18M. The company is a leading provider of reliability engineering software, education, consulting and related services to product manufacturers and maintenance organisations globally. It will be integrated into the Test and Measurement segment. In March, the group acquired Sunway Scientific, a Taiwanese distributor, for a total consideration of £2.2M including £400K contingent consideration which is based on 10% of annual sales over a threshold over the following three years, subject to a total cap of £1.9M. The acquisition generated goodwill of £600K and the business will be integrated into the Materials Analysis segment. The acquisitions contributed £1.2M to operating profits during the period.

Given the weak trading conditions, the group has initiated a number of cost reduction measures, including selective restructuring in certain businesses in order to improve future profitability. These measures resulted in a net cost of £400K in the first half with an additional net cost of £3M expected to be incurred in the second half. The annualised benefits arising from these measures are expected to be around £6M.

During the year Bill Seeger and Ulf Quellmann joined the board as non-executive directors and after nine years of service, John Warren retired as non-executive director.

New product launches and recent acquisitions are expected to benefit performance in the second half of the year and in addition, the group have taken cost reduction measures to improve profitability. Given the challenging near term trading environment and the net effect of the cost reduction measures, full year adjusted operating profit is expected to be around the lower end of market expectations (£200M to £223.4M, so nearer the £200M figure then). This is rather disappointing but I have to say I really like the way this company has stuck their neck out and given a figure – I wish more companies did this.

Net debt at the period end came to £148.7M compared to £107.4M at the same point of last year. After an 8% in the interim dividend, the shares are yielding 2.5%, increasing to 2.6% for the full year consensus estimate.

Overall then this was another mixed half year for the group. Profits fell year on year due in part to the increased amortisation of acquired intangibles but also due to underlying admin costs increasing. Net tangible assets also fell, partly due to increased pension liabilities and increased borrowings and whilst operational cash flow increased, this was entirely due to lower taxes being paid and the underling cash profits fall – although the group is still decently cash generative. Operationally, the materials analysis division improved due to the acquisition but it is still struggling with lower demand from the mining sector. The test and measurement division saw lower profits due to less large orders from the consumer electronics division, the weak coated paperboard and graphic paper market affected the in-line instrumentation division and the industrial controls segment was hit by a slowdown in US industrial demand.

This all adds up to a rather gloomy picture overall. As I said before the company is cash generative and a quality outfit but I don’t think the current share price takes into account the difficult markets the group is facing at the moment.

The downturn might be weakening but this doesn’t look like a good chart to invest in at the moment.

On the 20th November the group released a trading update covering the first four months of the second half. Like for like sales declined by 1% with trading conditions worsening as the period progressed. Acquisitions contributed 2% points of sales growth whilst foreign currency exchange movements adversely impacted growth by 2% which resulted in the 1% fall overall.

Like for like sales grew by 2% in both Europe and Asia Pacific whilst sales to North America declined by 3% and there was a significant decline in sales to the ROW, principally driven by weakness in Russia and Latin America. Materials Analysis and Test and Measurement both continued to deliver sales growth whilst sales declined in both In-line Instrumentation and, more markedly, in Industrial Controls.

The group have completed three bolt-on acquisitions since the half year, for a combined upfront consideration of £11M. In August they purchased Label Vision Systems, a US based leader in surface-based microseismic sensing technology which is provided to the oil and gas along with mining markets. It will integrated into ESG Solutions within the Test and Measurement segment. In November, they acquired Sound Answers Inc, a US based engineering services business that specialises in noise, vibration and harshness design and simulation, primarily for automotive customers. The business will be integrated into Bruel & Kjaer within the Test and Measurement segment. The acquisition pipeline apparently remains encouraging.

Overall, the board currently anticipates that full year adjusted operating profit will be towards the lower end of the range of market expectations which is probably therefore about £180M.

Overall, this is a disappointing update and I am particularly concerned about the comment regarding trading conditions worsening as the period progress so I am not buying these shares at the moment.

On the 25th November it was announced that Chairman John Hughes purchased 2,000 shares at a cost of £34.4K which gives him a total holding of 10,000 shares. A little later it was also announced that director Eoghan O’Lionaird purchased 5,743 shares at a cost of £100K which represents his first share purchase. These buys look like a pretty decent gesture to me.