Spectris is a supplier of productivity-enhancing instrumentation and controls and is made up of four divisions. The Materials Analysis division provides products and services that enable customers to determine structure, composition, quantity and quality of particles and materials when assessing materials before production or during the manufacturing process. The businesses in this division are Malvern Instruments, PANalytical and Particle Measuring Systems and customers tend to be in the metals, minerals and mining, pharmaceutical and fine chemicals, and academic research industries. The Test and Measurement division supplies test, measurement and analysis equipment, software and services for product design optimisation, manufacturing control, microseismic monitoring, and environmental noise monitoring systems. The businesses in this sector are Bruel & Kjaer Sound and Vibration, ESG Solutions and HBM. Customers in this division tend to come from the automotive, aerospace, consumer electronics, energy and environmental noise monitoring industries.

The In-line Instrumentation division provides process analytical measurement, asset monitoring and on-line controls as well as associated consumables and services for both primary processing and the converting industries. The businesses in this division are Bruel & Kjaer Vibro, BTG Group, NDC Technologies and Servomex. Customers in this division tend to be from the process industries, energy and utilities, pulp, paper and tissue, and the converting, web and packaging industries. The Industrial Controls division provides products and solutions that measure, monitor, control, inform, track and trace during the production process. The businesses in this division are Microscan, Omega Engineering and Red Lion Controls. Customers in this division tend to be from the general manufacturing industry.

Spectris has now released its final results for the year ended 2014.

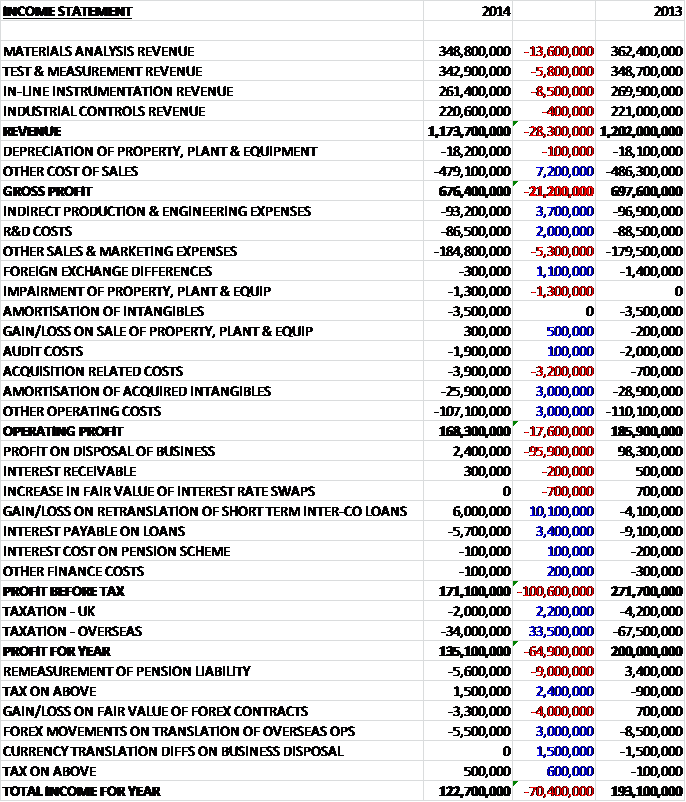

When compared to last year, total revenues fell by £28.3M to £1.173BN with declines in all business areas, particularly materials analysis and in-line instrumentation. Cost of sales also fell, however, to give a gross profit some £21.2M below that of last year. We also fee modest falls in R&D costs and indirect production and engineering expenses but sales and marketing costs increased year on year. There was a £1.1M positive swing in foreign exchange and a £1.3M impairment of fixed assets along with a £3.2M increase in acquisition related costs, which was counteracted somewhat by a £3M fall in the amortisation of acquired intangibles, although these remained substantial at £25.9M. After a decline in other operating costs, group operating profit stood at £168.3M, a decline of £17.6M year on year.

We then see a £10.1M positive swing in the translation of short term inter-company loans and a £3.4M decline in the interest payable on the bank loans but there was the lack of a £98.3M profit on the disposal of the Fusion UV business that occurred last year (although there was a £2.4M income this year related to the release of warranty provisions of the disposed business) which was offset partially by a fall in tax to give a profit for the year of £135.1M, a fall of £64.9M when compared to last year.

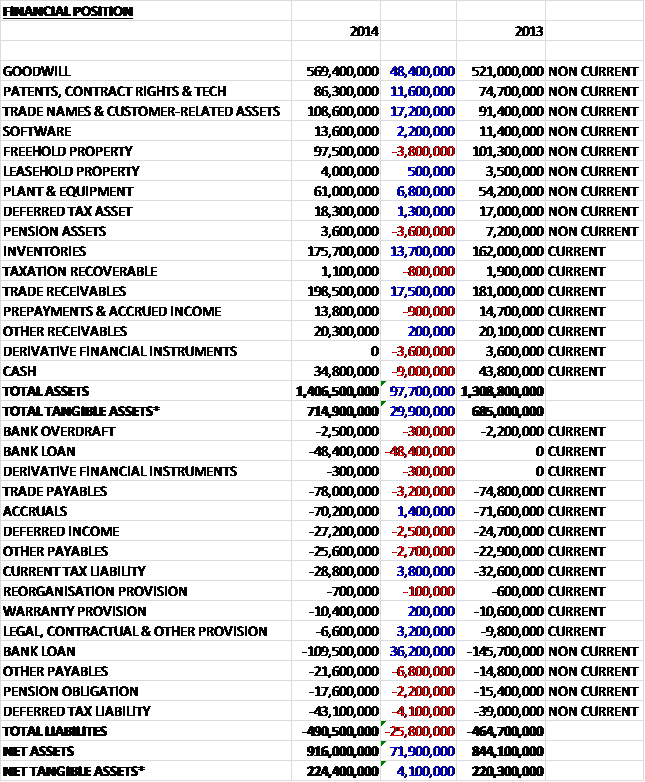

When compared to the end point of last year, total assets increased by £97.7M driven by a £48.4M increase in goodwill, a £17.5M growth in trade receivables, a £17.2M increase in customer-related assets, an £11.6M increase in patents and technology, and a £13.7M growth in inventories, partially offset by a £9M fall in cash. Total liabilities also increased during the year as a £12M increase in bank loans, a £6.8M growth in other payables, a £4.1M increase in deferred tax liabilities, mainly relating to the acquisition, and a £3.2M increase in trade payables was partially offset by a £3.8M fall in current tax liabilities. This gave a net tangible asset level (plus patents and technology) of £224.4M, an increase of £4.1M year on year.

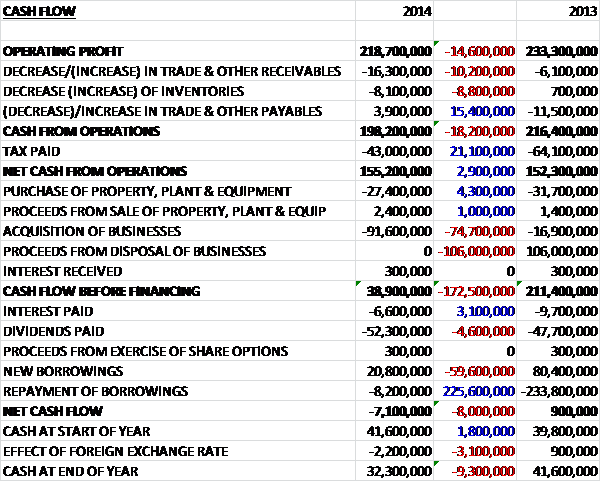

Before movements in working capital, cash profits fell by £14.6M to £218.7M. The group then saw a fairly large outflow of working capital, mainly due to a £16.3M increase in receivables and after a much lower tax bill, the net cash from operations stood at £155.2M, an increase of £2.9M when compared to last year. The group spent a net £25M on fixed assets relating to investments in infrastructure projects in the Netherlands and a new ERP system for Omega Engineering, and some £6.6M on interest (why that is included in financing I do not know…) along with a £91.6M spend on acquisitions and even after all of this, there was a £32.3M increase in cash before financing items. This was not enough to cover the dividend though and after a net £12.6M of new loans the cash outflow for the year was £7.1M and the cash level at the year-end was £32.3M.

The adjusted operating profit in the Materials Analysis division was £53.3M, a decline of £10M year on year. This primarily reflected weakness in the metals, minerals and mining industries and first half weakness in the academic research sector, partially offset by sales growth in the pharmaceutical and semiconductor sectors, not helped by costs incurred in relation to new product launches in the life sciences sector. Sales to the pharmaceutical sector increased, driven by growing demand from biopharmaceutical and generic drug manufacturers, particularly in North America, though Asia and Europe both grew too. The group see significant further opportunities in this sector and continue to invest in the area, launching a number of new platforms including the Zetasizer Helix, which can be used to characterise protein size and structure. Additionally, the acquisitions of MicroCal and Affinity Biosensors were completed during the year.

MicroCal is a provider of microcalorimetry instruments for material research with particular applications in biomolecular applications, whilst with Affinity Biosensors the group obtained the Archimedes instrument which accurately measures the density of individual particles, molecules and cells, enhancing the portfolio of solutions across the life science market.

The metals, minerals and mining sector was challenging during the year, notably in China, Australia and Indonesia where there was a significant decline in new commodity related infrastructure investment as customers focussed on improving their returns on existing investments in the face of slowing global commodity demand. In addition, many large projects in China were postponed or subject to delays. The group continued to develop new products and applications for this market, however, launching the upgraded X-Ray Fluorescence benchtop system, the Epsilon 3* and they have been pleased with the initial customer response to the system which is suitable for applications in a wide range of industries such as cement production, mineral analysis and polymer production.

Sales to academic research institutes were broadly flat as the decline experienced in the first half was offset by good growth in the second half with sales to Chinese universities growing strongly in H2, benefiting from environmental projects to improve river water quality and energy storage across the country. There was also good growth from the UK academic sector in the second half of the year. Demand in the semiconductor sector improved as the year progressed, reflecting more favourable market conditions and an increased rate of new product introductions. The acquisition of their distributor in South Korea in the second half of the year also contributed to growth in that sector.

After three successive quarters of sales decline, the segment returned to growth in Q4 and the board expect to see good progress in 2015, boosted by new product launches and the acquisitions made during the year. Continued investment in new products should deliver progress in the pharmaceutical, life science and semiconductor sectors, albeit slower growth is expected in the Chinese pharmaceutical market as compliance with new regulations has now been achieved. The board expect the academic research market to remain subdued given public sector budget constraints and demand from the metals, minerals and mining sector is expected to remain low next year as although there are early signs that demand is stabilising, the timing of any recovery remains uncertain.

The adjusted operating profit in the Test and Measurement division was £52.2M, a fall of £2.6M when compared to last year reflecting investments in the engineering software business and IT infrastructure together with higher personnel costs and adverse foreign exchange movements. There was good growth in the automotive sector, particularly in North America and Japan. Growth is being driven by the investment cycles of the large automotive manufacturers and rising demand from the industry to understand the noise and vibration characteristics of vehicles and engines in order to gain competitive advantages and meet legislative requirements. The industry also continues to invest in hybrid and full electric vehicles, including in China. During the year the group launched important new products targeted at this market such as the MX403B amplifier which measures the high voltages associated with electric car batteries, and the SomatXR data acquisition system which have both been received well so far.

Sales in the aerospace market declined this year following some particularly large projects in 2013 and a second half decline in sales to Russia. The group launched new modules for their data analysis software which enables fatigue testing of new carbon fibre composite materials. They also purchased an optical sensors business during Q4 that will allow HBM to accelerate its growth in optical measurement and monitoring solutions for a wide range of applications including new material development and power systems within the aerospace, automotive and power industries.

There was a significant decline in the defence and space markets during the year, particularly in the second half of the year when the imposition of economic sanctions on Russia meant the group were unable to export their vibration test systems for communications satellites to that market. In addition, defence budgets have been constrained in most developed markets. There was a continued strong growth in demand for the group’s engineering software solutions, though, as customers increasingly use software to enhance their productivity by converting engineering and process data into information that enables them to improve their products and processes.

Sales to the consumer electronics market were strong throughout the year, benefiting from large projects in North America and China as customers seek to enhance the audio quality on their electronic devices. The group sees opportunities to grow in this market by providing calibration services which should improve the quality of revenues in a sector where sales patterns are lumpy, driven by large customer projects. The group continues to develop their environmental noise monitoring business, launching a service called Noise Sentinel on Demand aimed at construction and industrial markets. This service required no capital outlay and is low-cost to use.

The board expects further progress in the division in 2015, benefiting from the acquisitions and robust market conditions in the automotive, aerospace and consumer electronics sectors. They see increased opportunities for software applications to support innovation in vehicle design and engine technologies with their new solutions such as PULSE reflex targeted at these opportunities. They also expect growing demand for measurement equipment to test new composite materials used in automotive and aircraft frames. The board have highlighted that a repeat of the large projects in the consumer electronics market may not occur this year – this is refreshingly honest I have to say. Near term market conditions in the oil, gas and mining industries are uncertain and the space market is likely to remain subdued whilst economic sanctions against Russia remain. Defence spending will also be constrained by continued pressure on government finances.

Examples of projects in the division during the year include HBMs lean manufacturing programme, ProHBM, which is driving productivity at the Suzhou facility in China. The programme was implemented to improve efficiency as costs increase throughout China. Another initiative involved redesigning the production cell system so that all assembly, quality inspection and final packaging is integrated into a single work station that has resulted in a 50% reduction in the cycle time for each load cell manufactured. Bruel & Kjaer’s new lightweight portable Impedance Meter System measures the acoustic properties of the materials used to help reduce noise from aircraft engines. This helps manufacturers develop quieter aircraft in order to meet increasing environmental noise regulations.

The adjusted operating profit in the In-line Instrumentation division was £48M, a decline of £3.2M when compared to 2013 with sales declining due to foreign currency exchange movements and margins declining due to adverse product mix, primarily in the pulp and paper business. In the energy and utilities market, sales were up significantly during the year with strong demand in China, driven by legislation to reduce emissions, and good growth from the downstream petrochemical markets in North America and the Middle East. The group have launched a new laser gas analyser into this sector which is smaller and lighter than other products in the market. In India, they benefited from the continued expansion of a large petrochemical producer, Reliance Industries, with substantial orders received for the gas analysis products. They also received a major contract from EDP Renewables North America for the supply and retrofit installation of condition monitoring systems on several hundred wind turbines of different brands in the US, together with the adoption of VibroSuite, their monitoring and surveillance software into EDPR’s systems.

During the first half of the year, the decision was taken to merge NDC and Beta LaserMike and the new business, named NDC Technologies, will provide customers with a broader product offering and state of the art technologies. It is expected that the new business will be able to increase sales penetration to a number of markets. Sales to the converting, web and packaging industries showed strong growth, particularly in Asia and Europe, benefiting from new products such as the AccuScan 6012 gauge, the industry’s first four axis diameter and ovality gauge for measuring products up to 12mm.

Sales to the pulp and paper markets declined during the year as market conditions triggered mill closures, curtailments and de-stocking activity while sales of products for tissue applications grew strongly, particularly in North America, which was sufficient to offset lower demand for graphic coated paper in China and Europe. Trading conditions in China were also negatively impacted by project delays and increased price competition. Despite these difficult market conditions, the group are launching new products such as the PROTO UF tungsten carbide coating blade to enhance their market position.

Overall, the board expect progress in this division in 2015. Whilst near-term trading conditions in the coated paper market are likely to remain challenging, they see good opportunities in the tissue industry for consumable products such as creeping blades, as well as for their process control instruments as manufacturers continue to seek to improve their productivity. They see good medium-term growth potential across the energy and utilities sector, albeit the near-term outlook for the energy market is uncertain. There is a strong pipeline of new products to target this sector going forward. In the converting, web and packaging industries, new food safety regulations in the US provide good growth opportunities whilst they also expect to see incremental benefits from the creation of NDC Technologies.

As mentioned above, NDC Technologies launched the AccuScan 6012 gauge, the industry’s first four axis gauge for measuring products up to 12mm. This features a 25% improvement in flaw detection accuracy compared to a conventional three axis gauge and up to 100% ovality accuracy. Manufacturers of extruded products such as medical tubing and high-performance cable can control product quality more reliably and reduce wastage. Also, Bruel & Kjaer Vibro released a new compact portable monitoring instrument line, the VIBROTEST/VIBROPORT 80 which is more powerful, intelligent and lighter than its predecessor. These handheld vibration measurement tools play an important part in predicting where faults may occur, avoiding damage to machinery and unscheduled downtime.

The adjusted operating profit in the Industrial Controls division was £44.6M, a fall of £800K year on year as a result of the investment in the expansion of Omega Engineering and IP related legal costs (reported sales were flat and LFL sales increased by 5%). Investment in the geographic expansion of Omega is starting to show results with good sales performance during the year, particularly in Asia. The opening of the Japan office in January 2014 completed the initial phase of the Asian expansion programme. Since then, their presence has been strengthened in Europe and Asia through additional investment in digital marketing, development of sales staff and local operational capabilities. In the latter part of the year, the new ERP system was launched across Omega’s global network which will enhance the back office processes and give faster insight into daily orders and sales. During the year the group also increased the number of new product introductions, for example, in late 2014 a new wireless transmitter and Omega app was released that allows customers to use their smartphones and tablets as a data logger for temperature, PH and humidity.

The segment saw particularly strong growth from sales into the supply chain supporting the North American oil and gas sector where the Graphite series of display panels has developed a good position in the fuel distribution market. These displays are robust and provide an interface for operators to communicate and control fuel tank pumping activity to a central server. They are seeing many customers use the product on their tanks as part of their digital oilfield initiative and are expanding the production facilities for this business to increase capacity. A number of new products to strengthen the industrial networking and factory automation offerings were also launched which included the N-Tron Gigabit Power over Ethernet Plus injector, which allows factories and other industrial sites to add new technology without disrupting existing networks.

Sales growth for their track, trace and control products improved as the year progressed. This reflected easier comparator figures in the second half of the year, together with increased activity from their major electronics customers and the launch in mid-2014 of Auto VISION 3.0, the latest machine vision solution that automates tasks such as inspection, gauging and counting, and reads barcodes and optical characters. The board expect to see further growth in this segment in the coming year. The need for customers to improve productivity and efficiency is expected to result in increased demand for factory automation and industrial networking products, particularly in China where there is a drive to improve the return on previous capital investments.

Red Lion Controls added the N-Tron Series Gigabit Power over Ethernet Plus injectors to its portfolio of industrial networking products. These compact injectors are used in space-constrained applications and deliver both power and data over a single Ethernet cable. Gigabit Ethernet is becoming the standard in industrial networking and these products are particularly suitable for video security and other applications requiring high-speed communications. Microscan’s new CloudLink interface enables users to monitor product barcode inspections remotely. It improved productivity by allowing the user to see results immediately on any web-enabled device.

There were a large number of acquisitions during the year. In June, the group acquired La Corporation Scientifique Claisse, a company based in Canada for a total consideration of £10.4M. The purchase extends the group’s capabilities in sample preparation for atomic spectroscopy, including X-Ray analysis and generated goodwill of £3.4M. In July the group acquired MicroCal, a US business, for a total consideration of £28.7M which extends their capabilities in life science analytical solutions and generated goodwill of £14.9M. Also in July the group acquired Affinity Biosensors, a US business, for a total consideration of £9.6M including £700K contingent consideration based on 3% of sales over a threshold amount over the next six years. The Affinity acquisition extends the group’s capabilities in particle measurement within the life science sector and generated goodwill of £4.7M.

In September the group acquired Sudo Premium Engineering, a South Korean distributor, for a total consideration of £5.9M including a £1.5M contingent consideration which is based on 2.5% of annual sales up to a threshold and 7.5% over this threshold over the next five years. The acquisition came with intangible assets of £5.9M but did not generate any goodwill. In October the group acquired Fibersensing, a company based in Portugal, for a total consideration of £5.1M (plus £1M of acquired debt) including £2.5M of contingent consideration which is based on 50% of sales over a threshold amount over the next three years. This acquisition extends the group’s capabilities in Fiber Bragg Grating measurement and monitoring systems for critical physical assets and generated goodwill of £3.1M.

In December the group acquired Engineering Seismology Group, a company based in Canada, for a total consideration of £44.1M including a £6.9M contingent consideration which is based on 50% of the year on year sales growth over the next three years above certain thresholds. The acquisition generated goodwill of £22.4M and enhances the group’s capabilities in microseismic monitoring equipment and analysis solutions primarily in the oil, gas and mining industries. All of these acquisitions contributed £3.5M to the operating profit throughout the year. This all means that there is some £11.6M of contingent consideration that could potentially be paid going forward but it is unclear whether this has been included under the group’s liabilities.

After the year-end the group acquired ReliaSoft Corp, a company based in the US, for a total consideration of £28M. The business is a provider of reliability engineering software and will be integrated into the Test and Measurement segment. The group is fairly large but seeks to expand further through developing new products, pursuing new growth in new markets and new geographies and pursuing acquisitions.

The group is somewhat susceptible to foreign exchange movements against Sterling with a 10% weakening of the US Dollar reducing pre-tax profits by £5.8M, a 10% weakening of the Euro reducing pre-tax profits by £5.4M and a 10% weakening of the Swiss Franc reducing pre-tax profits by £1.7M. There is less susceptibility to interest rate rises with a 1% increase giving rise to a £200K fall in pre-tax profits. As can be seen, there are also some risks associated with the geographical range the group operates in with the weak Eurozone economies, a slightly softer Chinese economy and economic sanctions imposed on Russia all affecting sales this year.

Assuming a similar macroeconomic environment in 2015, the group expects to deliver progress as they benefit from their new investment in new products and from the recent acquisitions.

At the year-end, net debt stood at £125.6M compared to £104.1M at the end of last year with available undrawn committed borrowing facilities of £316.8M. There is also £40.5M of operating lease payments off the balance sheet but this isn’t particularly high for a company of this size and fell year on year. At the current share price the shares trade on a PE ratio of 17.1, falling to 15.8 on next year’s consensus forecast. After a 9% increase in the total dividend this year, the shares currently yield 2.8% but this falls to 2.6% on next year’s forecast.

Overall then this seems to have been a fairly slow year for the group. Pre-tax profits fell year on year, even when the effect of the loan re-translations (I still don’t really know what that is) and last year’s disposal are removed. Net assets did increase modestly, but that was due to the growth in intangible assets and although net operational cash flow grew year on year (due to much lower tax payments) the underlying cash profit fell. Despite this, the group is still very cash generative and even had free cash left over after the £91M spent on acquisitions – sadly this was not enough to cover the dividends though.

Operationally, all segments experienced declining profit but the overall fall was driven by the Materials Analysis division which struggled in the face of lower demand for commodities and lower academic research. These factors are likely to remain going forward, along with a likely decline in sales to Chinese pharmaceutical companies following the completion of compliance there. In the other divisions, Test and Measurement was impacted by the sanctions on Russia and has warned that the large consumer electronics projects may not be repeated next year and in the In-line Instrumentation division sales were impacted by the falling market for coated paper. The Industrial Controls division was impacted by legal costs and investments in Omega but growth is expected here going forward.

In conclusion, this seems to be a high quality outfit – there are some great in-demand products being sold here and it is generating oodles of cash but there seems to be a bit of a softening in many of the markets and with a forward PE of 15.8 and a dividend yield of 2.8% I am not sure these issues are being fully factored in here.