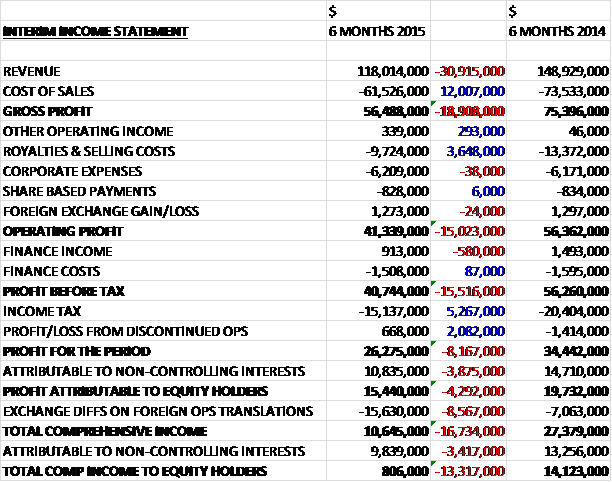

Gem Diamonds has now released its interim results for the year ending 2015.  When compared to the first half of last year, revenues fell by $30.9M(although as it has not yet reached commercial production, all Ghaghoo revenues were capitalised) due to both reduced volumes recovered and lower prices realised, and with cost of sales decreasing by $12M the gross profit saw a decline of $18.9M year on year. Royalty and selling costs fell by $3.6M, mirroring the decline in revenue (most of these costs are royalties paid to the Lesotho government) but finance income fell by $580K to give a profit before tax some $15.5M below that of the first half of last year. After a much smaller tax bill and a positive $2.1M swing to profit for the discontinued operation in Mauritius the profit attributable to the equity holders stood at $15.4M for the half year, a decline of $4.3M year on year.

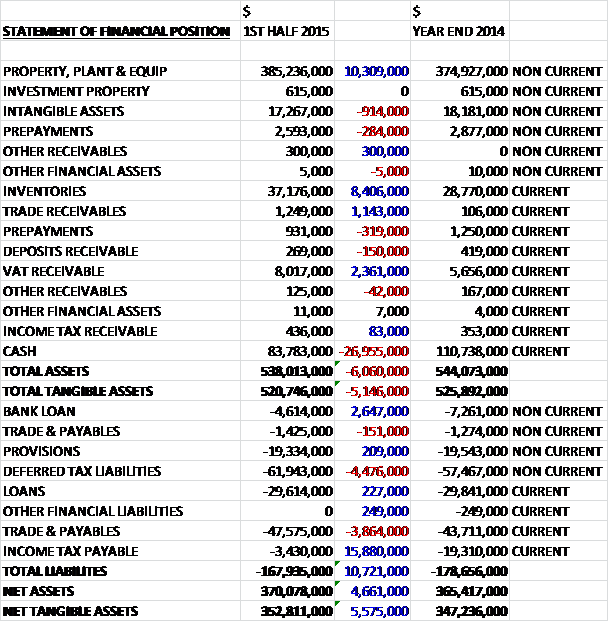

When compared to the first half of last year, revenues fell by $30.9M(although as it has not yet reached commercial production, all Ghaghoo revenues were capitalised) due to both reduced volumes recovered and lower prices realised, and with cost of sales decreasing by $12M the gross profit saw a decline of $18.9M year on year. Royalty and selling costs fell by $3.6M, mirroring the decline in revenue (most of these costs are royalties paid to the Lesotho government) but finance income fell by $580K to give a profit before tax some $15.5M below that of the first half of last year. After a much smaller tax bill and a positive $2.1M swing to profit for the discontinued operation in Mauritius the profit attributable to the equity holders stood at $15.4M for the half year, a decline of $4.3M year on year.  When compared to the end point of last year, total assets fell by $6.1M driven by a $27M crash in cash levels partially offset by a $10.3M increase in property, plant and equipment, an $8.4M increase in inventories, a $2.4M growth in VAT receivable and a $1.1M increase in trade receivables. Liabilities also declined during the period as a $4.5M increase in deferred tax liabilities, and a $3.9M growth in payables was more than offset by a $15.9M fall in income tax payable and a $2.7M decline in bank loans. The end result is a net tangible asset level of $352.8M, an increase of $5.6M year on year.

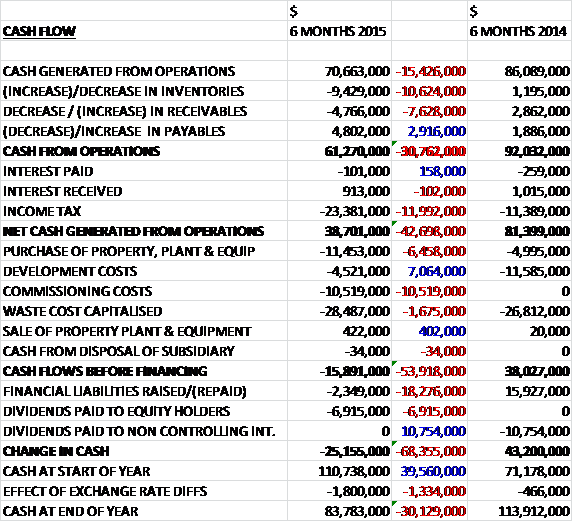

When compared to the end point of last year, total assets fell by $6.1M driven by a $27M crash in cash levels partially offset by a $10.3M increase in property, plant and equipment, an $8.4M increase in inventories, a $2.4M growth in VAT receivable and a $1.1M increase in trade receivables. Liabilities also declined during the period as a $4.5M increase in deferred tax liabilities, and a $3.9M growth in payables was more than offset by a $15.9M fall in income tax payable and a $2.7M decline in bank loans. The end result is a net tangible asset level of $352.8M, an increase of $5.6M year on year.  Before movements in working capital, cash profits fell by $15.4M to $70.7M. Due to a large increase in inventories and receivables, however, the cash from operations fell by $30.8M to $61.3M. The income tax payment fell by $12M which meant that net cash from operations fell by $42.7M to $38.7M. The group then spent $28.5M on deferred stripping costs; $11.4M on fixed tangible assets relating to the coarse recovery plant, the plant 2 phase 1 upgrade and capex at Ghaghoo; $10.5M on commissioning costs at Ghaghoo and $4.5M on development costs. All this meant that there was a $15.9M cash outflow before financing. The group then paid dividends and repaid a small amount of loans to give a cash outflow of $25.2M in the half year and a cash level of $83.8M. During the first half of the year, the rough diamond market experienced continued high inventory levels and liquidity concerns. This, combined with global macroeconomic uncertainties, has continued to place downward pressure on both rough and polished diamond prices. Although demand and prices for Letseng’s high quality diamond production have remained reasonably resilient through the period, the challenging market conditions have had a negative effect on prices achieved for Ghaghoo’s more commercial quality production. In the second half of the year it is expected that prices for Letseng’s diamonds will remain firm while the prices for Ghaghoo’s production should stabilise. During the period the Letseng mine delivered both of its growth projects, the plant 2 phase 1 upgrade and the new coarse recovery plant. The implementation of these two projects will see an increase in tonnes of ore treated and carats recovered in the remainder of the year and beyond. There are now no other major capital projects planned at the mine for the foreseeable future. Operating profits have decreased compared to the corresponding period last year as a result of lower diamond prices achieved due to difficult market conditions and the decreased number of carats recovered and sold due to the shutdown to commission the plant 2 phase 1 upgrade. Royalties and selling costs declined as a direct result of the fall in revenue and other costs declined as a result of the strong US dollar against the Lesotho loti which positively impacted US dollar reported costs during the period. At Letseng, five diamonds recovered in the first half of the year were greater than 100 carats in size, including a 314 carat Type IIa white diamond which was sold into a partnership arrangement in May. In July, a 357 carat Type IIa white diamond was recovered and options for its sale are being considered. The plant 2 phase 1 upgrade was completed on schedule and within the budget of $4.2M with the shutdown for the changeover completed within 19 days. The first phase will deliver an increase in treatment capacity of 250,000 tonnes per annum as well as further reducing diamond damage. Phase 1 will lay the foundation for further improvements in both treatment capacity and diamond damage reduction in subsequent plant development phases at the appropriate time. The shutdown at plant 2 to allow for the upgrade to be completed resulted in 3% lower tonnes treated compared to the first half of last year of 3.1MT, but remained in line with the mine plan guidance for 2015. The construction of the coarse recovery plant was completed on schedule at the end of the period and within the budget of $11.7M. Commissioning has been successful and on the first day of operation, a 52 carat diamond was recovered. The X-Ray sorters installed at the plant will ensure improved recovery of the high value diamonds and personnel x-ray scanners and improved surveillance will result in significant security improvements expected from this project. Electricity at the mine is supplied from South Africa by Eskom. With increased load-shedding events by Eskom, the on-site back up power generators have proved to be a worthwhile investment as they have greatly minimised the impact of power outages on production during the period, without significantly impacting total operating costs. During the period the group released an optimised life of mine plan. The key features are steeper pit slopes made possible by improved blasting practices, increased plant treatment capacity from the plant 2 phase 1 upgrade, smoother waste profile peaking at 36 mtpa, and satellite ore tonnage increasing to 1.65mpta in 2015 to 2019 and 2mpta from 2020 onwards. The focus at the mine going forward will be on optimising the newly commissioned plant 2 to ensure diamond damage is decreased, optimising the new coarse recovery plant to achieve the expected security and recovery benefits, managing the increase in mining fleet to meet the increased annual waste stripping target, optimising the Alluvial Ventures plant to improve throughput and recovery of fine diamonds, and evaluating optimal timing for underground mining. Of the total ore treated at Letseng’s plants, 33% of the material was sourced from the satellite pipe and 67% from the main pipe. The ramp up of satellite pipe ore treated to 1.65MT in 2015 is on track to be achieved. The balance of the ore (500KT) was treated through the Alluvial Ventures contractor plant, 80% of which was sourced from the main pipe and 20% from stockpiles. Certain process improvement modifications were also undertaken during the period at the Alluvial Ventures contractor plant which should see minor improvements in both tonnages treated and grade recovered going forward. Waste mining for the period was 14% higher than in the first half of last year and is on target to achieve 22 to 24MT per annum this year. Additional larger mining equipment is being mobilised to achieve these targets. In all, some 46,961 carats from the mine were sold at an average price of $2,264 per carat compared to last year when 53,799 carats were sold at an average price of $2,747 per carat. During the period, a revision to the number and timing of the mine’s tenders was made. The number of tenders has been reduced from ten to eight during the year. At Ghaghoo, 132,125 tonnes of ore was treated in the first half of the year with 35,283 carats being recovered. This ore was sourced mainly from a trial section on level 0 which is now fully mined out. Mining has now moved to the first production level (level 1) with the May and June average grade recovered increasing to 29.1cpht, above the reserve grade of 27.8cpht. The ramp-up of production continues to progress, albeit slower than anticipated due to difficult localised ground conditions within the orebody. A slot tunnel along the northern contact together with five stoping tunnels have been completed which now allow the production faces to retreat back across the orebody. Development of a further two tunnels west of tunnel 5 has also commenced. As the tonnage of ore from underground increased, the processing plant will continue to ramp up to the name place capacity of 60,000 tonnes per month. Processing optimisation and recovery efficiencies within the plant are ongoing. With the increased tonnage being treated and the plant running more consistently, the mine has started to recover some larger sized diamonds. During the period, 13 diamonds larger than 10 carats each were recovered, including a 35 carat diamond recovered in March and a 48 carat diamond recovered in May (the largest diamond recovered at the mine to date). Also a number of fancy colour diamonds, ranging from blues, pinks, oranges, lilacs and yellows, although predominantly in the smaller sizes, were recovered during the period. Mining production will continue on level 1 for the rest of the year whilst the main decline and the level 1 rim tunnel are progressed in order to access the next production sections. Progress in developing the decline and the rim tunnel has been impeded by the presence of water-bearing fissures. Specialists have been deployed to ensure that the fissures are fully sealed prior to the tunnels advancing and work is progressing slowly in order to avoid any further major ingress of water. The company is planning a feasibility study to determine the appropriate time to expand the mine in order to benefit from economies of scale. The first sale of 10,096 carats of Ghaghoo diamonds was held in February, achieving an average price of $210 per carat for a total value of $2.1M. After the period-end, a second sale of 29,891 carats took place, achieving just $165 per carat for a total value of $4.9M. Although this was below the average price achieved in the first sale, and the mine plan, the production was of lower quality which, together with a declining market for these goods, had a negative effect on the price achieved. The next sale should take place before the end of the year and will include a higher proportion of diamonds from the main body – this will be an important event for the group. Going forward, the focus for the mine will be the ramp up of production to a steady rate of 60,000 tonnes per month, continuing underground development to ensure sustainable production at the planned rates, design and development of long term underground infrastructure to support production, implementation of a water management strategy to deal with the excess water from the mine, management of costs to ensure profitability at full production rates, and to commence with a feasibility study with regards to expanding the mine to a higher level of production. Polished sales through the manufacturing division and partnership arrangements contributed $3.3M in additional revenue to the group and $2.6M to underlying EBITDA. In 2012 the group established a small manufacturing facility in Mauritius. At the end of June, this subsidiary was sold. The sale was agreed at a purchase price of $400K to be paid in quarterly instalments of $50K staring at the start of 2016. The subsidiary made an operating loss of $1M during the period and the group made a gain of $1.7M on the sale, mainly due to the recycling of the foreign currency translation reserve and the disposal of $732K-worth of payables. In April, 667,500 nil-cost options were granted to certain key employees under the LTIP. These options vest after a three year period and are exercisable between 2018 and 2025. In addition, 740,000 nil-cost options were granted to the executive directors under the same scheme with the vesting of the options subject to the satisfaction of certain market and non-market performance conditions over a three year period with the same timeframe as above. This is all very nice, nil-cost options! There is no indication of what the performance criteria might be. The group has two main bank loans. The LSL140M bank loan at Letseng Diamonds is a three year unsecured project debt facility signed jointly with Standard Lesotho bank and Nedbank in June 2014 for the funding of the new coarse recovery plant. The loan is repayable in ten quarterly payments which started in March of this year with the final payment due in June 2017. The interest rate on this facility is a mighty 11%! The other one is a $25M bank loan facility at the company. This loan is an unsecured facility which was signed with Nedbank at the start of 2014 for the remaining spend on the Ghaghoo phase 1 development. The loan was extended to October 2015 before it should be refinanced into a six year secured project debt facility expiring in December 2020. The interest rate at this facility is 4.3%. Finally there is a $20M three-year unsecured revolving credit facility with Nedbank which has not been used during the period and an undrawn $20.6M revolving credit facility at Letseng. In all, the group now has cash balances of $83.8M and undrawn facilities of $40.6M. Going forward, the board have approved capital projects of $7.6M and there is a possible dispute approximating $400K and tax claims within the various countries that the group operates approximating $1.4M. In the current depressed diamond market and due to the slower than expected ramp up at Ghaghoo, capital and cash management will be of high priority in the short term. Focus will be on converting the Ghaghoo mine from its commissioning phase into sustaining operational activities and achieving steady state production. At Letseng, the potential added value benefits following the completion of its current projects are expected to materialise and generate positive return on capital invested. Operationally, Letseng is geared to continue to mine a higher percentage of the higher grade, higher value satellite pipe ore. With cost control and operational efficiency the focus for the second half of the year, the company is on track to pay its next dividend in 2016. At the current share price the shares have a dividend yield of 2.3% which is forecasted to increase to 2.5% this year. Overall then, this has been a difficult half year period for the group. Profits are down due to less ore being mined after the planned shut down due to the plant 2 phase 1 upgrade along with a lower price being achieved for the diamonds. Net assets did improve, however, mainly it seems from a reduction in the current tax payable. As far as cash flow is concerned, things were less positive with a $15.9M cash burn before financing – there remains a decent safety net with regards cash though. The prices of the Letseng diamonds did hold up better than the market but still fell from $2,747 last year to $2,264 this year and with less capex at Letseng going forward this mine at least seems like it should generate some cash flow. The problem really lies with the Ghaghoo mine. The more commodity level diamonds mined here have been more affected by the weakness in the market and the price of $165 achieved at the last auction doesn’t look good enough in my view. Management say this is because the quality of diamonds was unusually low but we shouldn’t have to wait long until the next Ghaghoo auction which will be very important. In addition, the operating problems at the mine don’t help either. Progress has been hampered by difficult localised ground conditions and water bearing fissures. In conclusion, I will hold off buying here until there is some more clarity over how much the company can expect to get for its Ghaghoo diamonds in the current market.

Before movements in working capital, cash profits fell by $15.4M to $70.7M. Due to a large increase in inventories and receivables, however, the cash from operations fell by $30.8M to $61.3M. The income tax payment fell by $12M which meant that net cash from operations fell by $42.7M to $38.7M. The group then spent $28.5M on deferred stripping costs; $11.4M on fixed tangible assets relating to the coarse recovery plant, the plant 2 phase 1 upgrade and capex at Ghaghoo; $10.5M on commissioning costs at Ghaghoo and $4.5M on development costs. All this meant that there was a $15.9M cash outflow before financing. The group then paid dividends and repaid a small amount of loans to give a cash outflow of $25.2M in the half year and a cash level of $83.8M. During the first half of the year, the rough diamond market experienced continued high inventory levels and liquidity concerns. This, combined with global macroeconomic uncertainties, has continued to place downward pressure on both rough and polished diamond prices. Although demand and prices for Letseng’s high quality diamond production have remained reasonably resilient through the period, the challenging market conditions have had a negative effect on prices achieved for Ghaghoo’s more commercial quality production. In the second half of the year it is expected that prices for Letseng’s diamonds will remain firm while the prices for Ghaghoo’s production should stabilise. During the period the Letseng mine delivered both of its growth projects, the plant 2 phase 1 upgrade and the new coarse recovery plant. The implementation of these two projects will see an increase in tonnes of ore treated and carats recovered in the remainder of the year and beyond. There are now no other major capital projects planned at the mine for the foreseeable future. Operating profits have decreased compared to the corresponding period last year as a result of lower diamond prices achieved due to difficult market conditions and the decreased number of carats recovered and sold due to the shutdown to commission the plant 2 phase 1 upgrade. Royalties and selling costs declined as a direct result of the fall in revenue and other costs declined as a result of the strong US dollar against the Lesotho loti which positively impacted US dollar reported costs during the period. At Letseng, five diamonds recovered in the first half of the year were greater than 100 carats in size, including a 314 carat Type IIa white diamond which was sold into a partnership arrangement in May. In July, a 357 carat Type IIa white diamond was recovered and options for its sale are being considered. The plant 2 phase 1 upgrade was completed on schedule and within the budget of $4.2M with the shutdown for the changeover completed within 19 days. The first phase will deliver an increase in treatment capacity of 250,000 tonnes per annum as well as further reducing diamond damage. Phase 1 will lay the foundation for further improvements in both treatment capacity and diamond damage reduction in subsequent plant development phases at the appropriate time. The shutdown at plant 2 to allow for the upgrade to be completed resulted in 3% lower tonnes treated compared to the first half of last year of 3.1MT, but remained in line with the mine plan guidance for 2015. The construction of the coarse recovery plant was completed on schedule at the end of the period and within the budget of $11.7M. Commissioning has been successful and on the first day of operation, a 52 carat diamond was recovered. The X-Ray sorters installed at the plant will ensure improved recovery of the high value diamonds and personnel x-ray scanners and improved surveillance will result in significant security improvements expected from this project. Electricity at the mine is supplied from South Africa by Eskom. With increased load-shedding events by Eskom, the on-site back up power generators have proved to be a worthwhile investment as they have greatly minimised the impact of power outages on production during the period, without significantly impacting total operating costs. During the period the group released an optimised life of mine plan. The key features are steeper pit slopes made possible by improved blasting practices, increased plant treatment capacity from the plant 2 phase 1 upgrade, smoother waste profile peaking at 36 mtpa, and satellite ore tonnage increasing to 1.65mpta in 2015 to 2019 and 2mpta from 2020 onwards. The focus at the mine going forward will be on optimising the newly commissioned plant 2 to ensure diamond damage is decreased, optimising the new coarse recovery plant to achieve the expected security and recovery benefits, managing the increase in mining fleet to meet the increased annual waste stripping target, optimising the Alluvial Ventures plant to improve throughput and recovery of fine diamonds, and evaluating optimal timing for underground mining. Of the total ore treated at Letseng’s plants, 33% of the material was sourced from the satellite pipe and 67% from the main pipe. The ramp up of satellite pipe ore treated to 1.65MT in 2015 is on track to be achieved. The balance of the ore (500KT) was treated through the Alluvial Ventures contractor plant, 80% of which was sourced from the main pipe and 20% from stockpiles. Certain process improvement modifications were also undertaken during the period at the Alluvial Ventures contractor plant which should see minor improvements in both tonnages treated and grade recovered going forward. Waste mining for the period was 14% higher than in the first half of last year and is on target to achieve 22 to 24MT per annum this year. Additional larger mining equipment is being mobilised to achieve these targets. In all, some 46,961 carats from the mine were sold at an average price of $2,264 per carat compared to last year when 53,799 carats were sold at an average price of $2,747 per carat. During the period, a revision to the number and timing of the mine’s tenders was made. The number of tenders has been reduced from ten to eight during the year. At Ghaghoo, 132,125 tonnes of ore was treated in the first half of the year with 35,283 carats being recovered. This ore was sourced mainly from a trial section on level 0 which is now fully mined out. Mining has now moved to the first production level (level 1) with the May and June average grade recovered increasing to 29.1cpht, above the reserve grade of 27.8cpht. The ramp-up of production continues to progress, albeit slower than anticipated due to difficult localised ground conditions within the orebody. A slot tunnel along the northern contact together with five stoping tunnels have been completed which now allow the production faces to retreat back across the orebody. Development of a further two tunnels west of tunnel 5 has also commenced. As the tonnage of ore from underground increased, the processing plant will continue to ramp up to the name place capacity of 60,000 tonnes per month. Processing optimisation and recovery efficiencies within the plant are ongoing. With the increased tonnage being treated and the plant running more consistently, the mine has started to recover some larger sized diamonds. During the period, 13 diamonds larger than 10 carats each were recovered, including a 35 carat diamond recovered in March and a 48 carat diamond recovered in May (the largest diamond recovered at the mine to date). Also a number of fancy colour diamonds, ranging from blues, pinks, oranges, lilacs and yellows, although predominantly in the smaller sizes, were recovered during the period. Mining production will continue on level 1 for the rest of the year whilst the main decline and the level 1 rim tunnel are progressed in order to access the next production sections. Progress in developing the decline and the rim tunnel has been impeded by the presence of water-bearing fissures. Specialists have been deployed to ensure that the fissures are fully sealed prior to the tunnels advancing and work is progressing slowly in order to avoid any further major ingress of water. The company is planning a feasibility study to determine the appropriate time to expand the mine in order to benefit from economies of scale. The first sale of 10,096 carats of Ghaghoo diamonds was held in February, achieving an average price of $210 per carat for a total value of $2.1M. After the period-end, a second sale of 29,891 carats took place, achieving just $165 per carat for a total value of $4.9M. Although this was below the average price achieved in the first sale, and the mine plan, the production was of lower quality which, together with a declining market for these goods, had a negative effect on the price achieved. The next sale should take place before the end of the year and will include a higher proportion of diamonds from the main body – this will be an important event for the group. Going forward, the focus for the mine will be the ramp up of production to a steady rate of 60,000 tonnes per month, continuing underground development to ensure sustainable production at the planned rates, design and development of long term underground infrastructure to support production, implementation of a water management strategy to deal with the excess water from the mine, management of costs to ensure profitability at full production rates, and to commence with a feasibility study with regards to expanding the mine to a higher level of production. Polished sales through the manufacturing division and partnership arrangements contributed $3.3M in additional revenue to the group and $2.6M to underlying EBITDA. In 2012 the group established a small manufacturing facility in Mauritius. At the end of June, this subsidiary was sold. The sale was agreed at a purchase price of $400K to be paid in quarterly instalments of $50K staring at the start of 2016. The subsidiary made an operating loss of $1M during the period and the group made a gain of $1.7M on the sale, mainly due to the recycling of the foreign currency translation reserve and the disposal of $732K-worth of payables. In April, 667,500 nil-cost options were granted to certain key employees under the LTIP. These options vest after a three year period and are exercisable between 2018 and 2025. In addition, 740,000 nil-cost options were granted to the executive directors under the same scheme with the vesting of the options subject to the satisfaction of certain market and non-market performance conditions over a three year period with the same timeframe as above. This is all very nice, nil-cost options! There is no indication of what the performance criteria might be. The group has two main bank loans. The LSL140M bank loan at Letseng Diamonds is a three year unsecured project debt facility signed jointly with Standard Lesotho bank and Nedbank in June 2014 for the funding of the new coarse recovery plant. The loan is repayable in ten quarterly payments which started in March of this year with the final payment due in June 2017. The interest rate on this facility is a mighty 11%! The other one is a $25M bank loan facility at the company. This loan is an unsecured facility which was signed with Nedbank at the start of 2014 for the remaining spend on the Ghaghoo phase 1 development. The loan was extended to October 2015 before it should be refinanced into a six year secured project debt facility expiring in December 2020. The interest rate at this facility is 4.3%. Finally there is a $20M three-year unsecured revolving credit facility with Nedbank which has not been used during the period and an undrawn $20.6M revolving credit facility at Letseng. In all, the group now has cash balances of $83.8M and undrawn facilities of $40.6M. Going forward, the board have approved capital projects of $7.6M and there is a possible dispute approximating $400K and tax claims within the various countries that the group operates approximating $1.4M. In the current depressed diamond market and due to the slower than expected ramp up at Ghaghoo, capital and cash management will be of high priority in the short term. Focus will be on converting the Ghaghoo mine from its commissioning phase into sustaining operational activities and achieving steady state production. At Letseng, the potential added value benefits following the completion of its current projects are expected to materialise and generate positive return on capital invested. Operationally, Letseng is geared to continue to mine a higher percentage of the higher grade, higher value satellite pipe ore. With cost control and operational efficiency the focus for the second half of the year, the company is on track to pay its next dividend in 2016. At the current share price the shares have a dividend yield of 2.3% which is forecasted to increase to 2.5% this year. Overall then, this has been a difficult half year period for the group. Profits are down due to less ore being mined after the planned shut down due to the plant 2 phase 1 upgrade along with a lower price being achieved for the diamonds. Net assets did improve, however, mainly it seems from a reduction in the current tax payable. As far as cash flow is concerned, things were less positive with a $15.9M cash burn before financing – there remains a decent safety net with regards cash though. The prices of the Letseng diamonds did hold up better than the market but still fell from $2,747 last year to $2,264 this year and with less capex at Letseng going forward this mine at least seems like it should generate some cash flow. The problem really lies with the Ghaghoo mine. The more commodity level diamonds mined here have been more affected by the weakness in the market and the price of $165 achieved at the last auction doesn’t look good enough in my view. Management say this is because the quality of diamonds was unusually low but we shouldn’t have to wait long until the next Ghaghoo auction which will be very important. In addition, the operating problems at the mine don’t help either. Progress has been hampered by difficult localised ground conditions and water bearing fissures. In conclusion, I will hold off buying here until there is some more clarity over how much the company can expect to get for its Ghaghoo diamonds in the current market.  This is not a good looking chart…

This is not a good looking chart…

On the 14th September the group announced that it had sold an exceptional 357 carat white diamond recovered in July for a total of $19.3M. This really is an impressive achievement and shows that these really large stones are still in high demand. A few more of these and it won’t matter so much about the poor sales of the lower quality Ghaghoo diamonds.

On the 11th November the group released a trading update covering Q3. Prices for the large, high value production from Letseng remained robust during the period, achieving an average of $2,578 per carat compared to $2,374 in the year to date as a whole. The general sentiment in the diamond market remained cautions, and with continuing global macro-economic uncertainty, has placed further downward pressure on both rough and polished diamond prices. Following the HK diamond and jewellery show in September, focus has now turned to the US market.

At Letseng, during the quarter there were 29,460 carats recovered at a grade of 1.68cpht compared to 20,559 carats last quarter. Following the plant 2 phase 1 upgrade, ore processed through the plant is currently achieving the planned head feed tonnage which will increase throughput by 250,000 tonnes on an annualised basis. The two plants treated a total of 1.47M tonnes of ore during the period, of which 55% was sourced from the main pipe and 45% from the satellite pipe. The balance of the ore (290KT) was treated through the Alluvial Ventures contractor plant, of which 70% was sources from the main pipe and 30% from stockpiles.

Following on from the good progress made in the satellite pipe waste stripping, the year to date contribution of ore from the satellite pipe has already reached 1.58M tonnes against the full year target of 1.65M tonnes and is now expected to reach 1.8M tonnes by the end of the year.

Two Letseng tenders were held in the period, achieving an average price of $2,578 per carat compared to an average of $2,374 in the year to date, which seems pretty good. In all, 25,460 carats were sold in the quarter realising a value of $65.6M. There were also 33 carats of diamonds that were extracted for the group’s own manufacturing during the period at a rough value of $1M. Overall, the increased guidance for the year is for 105K to 108K carats to be recovered compared to 102K to 107K previously due to higher amounts of ore being treated. Some thirteen rough diamonds achieved a value of more than $1M including an exceptional quality 357 carat Type IIa white diamond which achieved $19.3M on tender with a total of three diamonds of over 100 carats being sold during the period.

Things at Ghaghoo were not so positive despite an increase in the carats recovered to 31,922 at an increased grade of 29.1cpht. All mined ore is being sourced from tunnels one to five on level 1. Production build up is continuing and development of the next four tunnels is well advanced in order to generate reserves for sustainable production. The water at the rim tunnel has been sealed and development has now progressed through the fissure area.

Plant optimisation continued during the period with the highest year to date monthly treated tonnage of 42,263 achieved in September. As part of this optimisation process, a new 100 tonne surge bin is scheduled for installation in January, and will be positioned ahead of the Autogenous Mill to further enhance the mill’s performance. A second parcel of 29,891 carats of commissioning phase production sold for $4.9M in July representing a price of just $165 per carat which brings the average to date down to $176 per carat.

The group had $86M cash on hand at the period-end with $32.1M drawn down against its available bank facilities resulting in a net cash position of $54M.

Overall then, the performance at Letseng seems to be very robust, with a good operational performance and excellent prices obtained for their output. At Ghaghoo it is a different story. Progress does seem to be being made operationally, with the water fissure issue seemingly dealt with but the prices achieved for the diamonds are poor reflecting the market for the stones in general. The question is, at this share price, is the company worth buying just for Letseng alone?

On the 17th December the group announced the appointment of Michael Lynch-Bell as a non-executive director. Michael spent a 38 year career at Ernst & Young having led its global oil & gas, UK IPO and global oil & gas and mining transaction advisory practices. He is currently a non-executive director Kaz Minerals. This is an interesting appointment, given his experience I wonder if some sort of deal is being lined up?

On the 3rd February the group released a trading update covering Q4. The diamond market remained weak during the period as it had done for much of 2015. The slowdown in Chinese retail demand, liquidity constraints and high polished inventory levels, particularly in the manufacturing sector, together with a strong US dollar contributed to a cautious approach being adopted by both the manufacturing and retail sectors. The prices achieved for the large, high value rough production from Letseng remained comparatively firm during the period, achieving an average of $2,117 per carat but the same cannot be said for the more commodity sized diamonds from Ghaghoo.

Initial data from the 2015 holiday season retail sales in the US has been positive and the general sentiment in the diamond market going into 2016 has improved. The reduction in the supply of rough diamonds from the major producers, together with the reduction of prices seen in 2015 and concerted consumer marketing efforts have helped to improve sentiment. The group’s first Letseng tender of 2016 currently underway in Antwerp has been well attended and sentiment is upbeat.

At Letseng there was 1,810,935 tonnes of ore treated that recovered 29,100 carats at a grade of 1.61cpht which is a 3% increase on the tonnes of ore treated by a 1% fall in the carats recovered due to a 4% fall in the average grade when compared to Q3. The plants 1 and 2 treated 1.53M tonnes of ore, of which 79% was sourced from the man pipe and 21% from the satellite pipe. The balance of the ore was treated through the Alluvial Ventures Plant. The higher production levels achieved are as a result of the plant 2 phase 1 upgrade which was implemented at the beginning of the year.

During the quarter a total of 30,357 carats were sold, an increase of 19% quarter on quarter but the price achieved declined by 18% to $2,117 per carat which meant that the total value sold fell by 2% at $64.3M. A total of two tenders were held during the period. The mine has managed to maintain its costs within expected targets and are in line with the full year guidance. Going forward, next year the mine is expected to treat 6.8M to 7M tonnes of ore, with the satellite pipe contributing 1.65MT. A total of 107K to 110K carats are expected to be sold and stay in business capital is expected to be between $8M and $10M.

At Ghaghoo, 85,046 tonnes of ore was treated in Q4 which recovered 24,294 carats at a grade of 28.6cpht. This compared unfavourably with Q3 when 109,751 tonnes were treated and 31,923 carats were recovered at a grade of 29.1. The majority of ore treated during the period was sourced from tunnels one to five on level one. During the period 503 metres of tunnelling was completed with development well advanced in the next series of tunnels on level one. Following the sealing off of the water fissure on level one, the planned intersection on the decline to level two has also been sealed.

As part of the treatment plant optimisation, a 100 tonne per hour surge bin, positioned ahead of the Autogenous Mill to enhance the Mill’s performance was commissioned in January. Post commissioning, the plant achieved its targeted treatment rate of 2,000 tonnes per day, confirming the plant’s ability to run its nameplate capacity of 60,000 tonnes per month.

A parcel of 49,120 carats was sold for $7.4M in December at just $150 per carat which brings the average to date down to $162 per carat. Based on the prices achieved in this sale and the currently depressed state of the rough diamond market for Ghaghoo’s production, various options have been reviewed with the aim of minimising operating losses during the year. It is considered prudent to downsize current production to achieve a modified target of about 300,000 tonnes for 2016.

Underground mining conditions experienced during the development phase of Ghaghoo have continued to be difficult. At the end of November, caving at the end of tunnels two and three propagated through to the surface. Although this was anticipated as the volume of ore extracted underground increased, it occurred some six months earlier than expected. Actions required to create a buffer zone to limit sand dilution were put in place and underground mining was then resumed. It has now become apparent that the area subject to dilution risk is greater than originally advised and the buffer zone has been increased following reassessment which will result in the deferment of extraction of about 300,000 tonnes of ore.

Reverting back to the original phase 1 production levels of 60,000 tonnes per month, or expanding beyond that production level will be largely dependent upon an improvement in the diamond pricing environment and options are being assessed to expand the operation in order to achieve acceptable financial returns as and when the diamond price improves.

The group ended the year with $85.7M cash on hand and a net cash position of $55.3M with the dividend payment for 2015 remaining on track.

Overall then this is a bit of a mixed update. The prices at Letseng, although down a bit are fairly robust and the operational performance at the mine seems good. Things are not the same at Ghaghoo, however, with the mine beset by operational difficulties and the smaller diamonds being sold there are not getting good prices. There does seem to be an improvement in sentiment in the diamond market, however, so it is possible prices may pick up. Until then, I will not be rushing to buy the shares.