President Energy has now released its interim results for the year ending 2015.

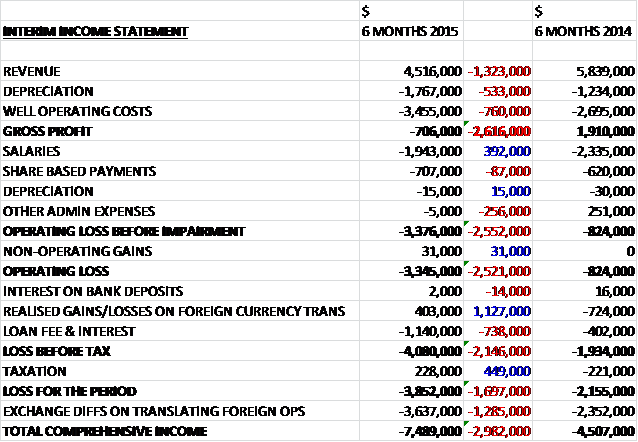

Revenues have fallen by $1.3M when compared to the first half of last year. Both depreciation and well operating costs then increased as the figures reflect a 100% ownership of Puesto Guardian concession so that the gross loss was $706K, a negative swing of $2.6M. Salaries did fall by $392K but share based payments and other admin expenses increased to give an operating loss some $2.6M higher. After a $1.1M positive swing in realised gains and losses on foreign currency transactions was partially offset by a $738K increase in loan fees and interest the loss before tax was some $2.1M higher which became a loss for the period of $3.9M after tax, an increase of $1.7M year on year.

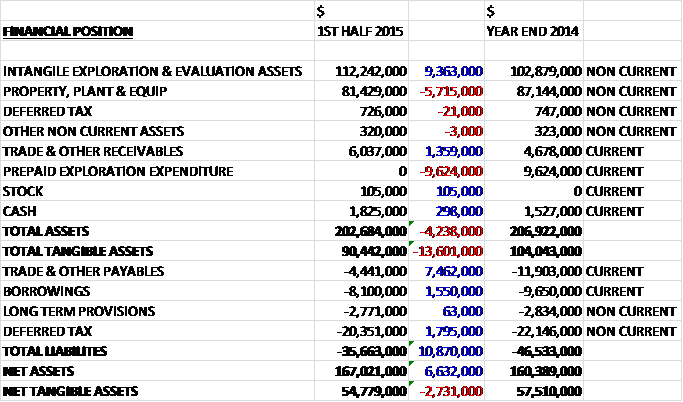

When compared to the end point of last year, total assets fell by $4.2M driven by a $9.6M decline in prepaid exploration expenditure and a $5.7M fall in property, plant and equipment mainly relating to exchange differences, partially offset by a $9.4M increase in exploration and evaluation assets and a $1.4M growth in receivables. Liabilities also fell during the period due to a $7.5K decrease in payables, a $1.8M fall in deferred tax liabilities and a $1.6M decline in borrowings. The end result is a net tangible asset level of $54.8M, a decline of $2.7M year on year.

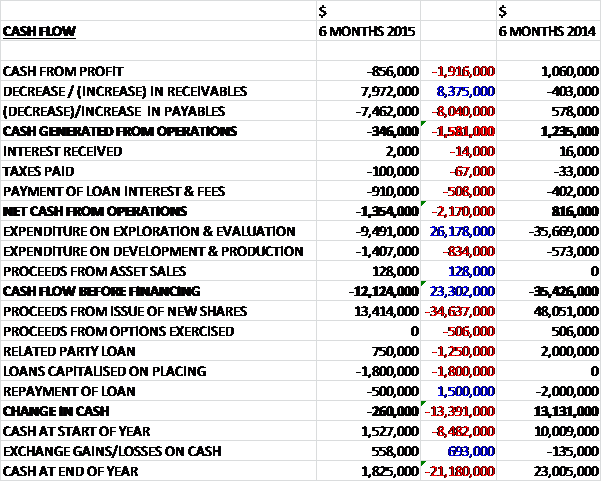

Before movements in working capital, cash losses came in at $856K, a negative swing of $1.9M year on year. After a fall in receivables and payables, along with a $508K increase in loan interest and fees gave net cash from operations was $1.4M, a negative swing of $2.2M. The group then spent $9.5M on exploration and evaluation, along with $1.4M on development and production to give a cash outflow of $12.1M before financing. The group then made $11.6M from the issue of new shares which gave an overall cash outflow of $260K and a cash level of $1.8M at the end of the period – it seems to me that the group are going to have to get another cash injection to carry on like this.

In Argentina the average net production before workovers was 231bopd compared to 342bopd during the same period of last year. The first phase of workovers of shut-in wells was completed in budget and on time at the end of the period and the current average production is now running at 315bopd with one of the producing wells temporarily in maintenance. The group average a realisation price of $70 per barrel with an additional $3 per barrel increase for new 2015 production which shows that Argentina is a very good prospect in this low oil price environment.

After the period end new concession terms were granted over all producing fields expiring in 2050 and post-period 2P reserves increased by 28% to 18.1MMbls with a net present value 10 before tax and royalties of $329.4M. Analysis of prospective resources shows significant potential in the deep gas prospect within the Puesto Guardian concession and the Matorras license areas. The next phase of workovers is being targeted towards the end of the year with long lead time items now being ordered. Essential maintenance and upgrading of facilities have now been completed.

In Paraguay the group have acquired 603km of 2D seismic which is awaiting final analysis. It is clear from the seismic data that several drillable Paleozoic prospects exist, in line with the company’s expectations and at 2,500 to 3,000 metres depth they are some 1,000 metres shallower than the Lapacho and Jacaranda wells drilled last year. In Australia the PEL82 block is still being retained by the company and remains under review with actions suspended due to the current market conditions.

In Louisiana, production increased by purchasing minority interests in operated assets and carried wells interest coming on stream. The current production of 270bopd represents a 29% increase from the average of 209boepd during the period and 218boepd during the first half of last year. The group also achieved operational cost savings and an extra $140K contribution to facility overheads has been achieved. The realised price for the oil was at WTI price which has fallen considerably over the period, averaging at $52 per barrel compared to $102 in the first half of last year and is now comfortably under the price achieved in Argentina. New well AS5 was drilled and movable hydrocarbons were identified. The well was suspended due to unexpected high pressure, however, with re-entry currently being discussed with a view to be actioned in the medium term.

The group had cash levels of $1.8M at the period end with undrawn loan facilities of $6.9M available.

Overall then, this has clearly been a difficult period for the group. The loss increased, net tangible assets were down and the operating cash outflow grew. Operationally things seem to have been improving through towards the end of the year. In the US, current production has increased but the decline in the realised oil price to $52 has offset this improvement. In Argentina, the fixed $70 per barrel price for oil has sheltered the group somewhat from the oil price declines and production increased here too towards the end of the period due to the workover programme.

In Argentina, the resources have increased and in Paraguay some interesting targets for drilling have emerged. Unfortunately there is currently just $1.8M cash left with some $6.9M in undrawn loans. With the cash burn of $12.1M during the period, further workovers in Argentina planned and a potential drill in Paraguay, it seems likely to me that the group will have to get some more cash from somewhere and whilst I still think this company has some interesting looking assets I don’t think now is the time to buy in.

this is not a joyous chart.

On the 6th October the group announced that it had acquired the 36% interest of the Pirity concession held by Petro Victory which will take President’s holding up to 100%. The acquisition will cost $500K payable by instalments ($200K in completion and three consecutive monthly payments of $100K). In the event of a farm-out taking place and back costs being paid, a sum limited to $2.7M will be payable to PV. Also a net profits interest of 3% of net revenues after deducting royalties and operational expenditure generated from commercial production will be paid to PV.

This looks like a good opportunistic acquisition due to PV’s lack of funds but the fact it is being paid in instalments is a bit odd.

On the 9th October the group announced the results of the Seismic campaign in Paraguay. There is an oil case with gross unrisked recoverable prospective resources of 302MMboe; a gas/condensate with gross unrisked recoverable prospective resources of 559Bcf of gas and 17MMBls of condensate. The overall chance of exploration success is considered by the company to be 22%. The success case is economic even in the current depressed market environment.

Whilst the interpretation of a number of other leads and prospects in Hernandarias continues, the company completed its own estimates of prospective resources in the Boqueron prospect. It is a three way dip structure of up to 60 square km and judged to be juxtaposed against Devonian source rocks. The new seismic supports the correlation of the same Paleozoic section proved in Lapacho in a NW direction through a series of structures culminating in the largest structure at Boqueron. At the Boqueron prospect the Icla, Santa Rosa and Sara reservoirs discovered at Lapacho are judged to correlate to depths of 1600 to 2700 metres. The source rocks are expected to be in the light oil generation window at these depths.

The group is moving forward with planning, strategic considerations and discussions over its Paraguay portfolio now that the recent Pirity acquisition has been completed. Taking into account the current macro environment, the current focus is on investment in production. It is therefore too soon to provide a definitive timetable for drilling of an exploration well at Boqueron. They currently have a 40% interest in the Hernandarias block and are entitled to earn-in to a further 40% on investing into the block within the next four years with an outstanding sum of about $10.4M to be applied towards drilling activity.

On the 4th November the group released a statement covering loan restructuring and a placing to raise $5M. The loan restructuring will result in the amount outstanding under the company’s loan facility being reduced from $11.1M to $7.1M by re-designating up to $4M into an unsecured convertible loan at a lower interest rate of 10% with the ability to convert the loan into shares at a 30% premium to 7.075p with both the revised loan facility and the convertible loan having a maturity date of the end of April 2017. Following the transfer, there will be $2.9M undrawn on the loan.

The proposed subscription is intended to raise up to $5M to be used to support the working capital position of the company and provide more flexibility to achieve the “best value possible for shareholders” with regards to the company’s farm-out process for Argentina and Paraguay while implementing its workover programme in Argentina to increase production. The executive chairman and CEO, Peter Levine, intends to participate in the subscription through the capitalisation of certain amounts due under the loan facility (the company who loaned the money is controlled by him) and in subscribing for new shares for cash. The subscription involves the issue of 45,801,280 new shares at a price of 7.075p per share.

Clearly this is necessary for the group to carry on but there is not that much being raised here and I have to say the fact that Peter Levine’s company is the one loaning the money makes me a bit uncomfortable (although this has been the case for some time of course).

On the 29th October the group announced the appointment of Robert Shepherd as non-executive director. He is former VP for emerging markets oil and gas at ABN Amro, a former non-executive director of Imperial Energy and a former CEO of Azonto Petroleum. He currently already owns a paltry 9,144 shares – no doubt purchased at a much higher price.

On the 14th December the group released an operational update.

Although operations on the two workovers planned for the period are still in progress, the results so far are encouraging. Production during well testing at intermediate steps in the workover and stimulation programs achieved an initial two day rate of 175bopd, substantially in excess of expectations, giving a new daily company production of more than 700boe in Argentina and Louisiana together.

With one of the workover wells, DP10, only currently allocated contingent resources, with continue production the board expect to be able to reclassify some contingent resources to reserves. The workover and stimulation exercises are continuing and both wells will be put back on stream again upon completion of the works in the coming week.

It was also announced that at the end of the year both David Jenkins and David Wake-Walker are retiring as non-executive directors. In the current environment the company will not be taking any immediate steps to replace them, which seems sensible to me.

Overall then, this was actually a very good update. The increase in production at these wells bodes well for the other workovers and the reduction in costs of two board members leaving is a positive too. Unfortunately in the current environment, it is difficult to see how any small oil company is a good investment, particularly as it must be expected that the new government in Argentina may reduce the price they pay for oil in the country given the big disparity between the current price in the country and the current price of oil on the market.

On the 7th January the group released an update covering the Argentine assets. The two workovers at the Dos Puntios Field at Puesto Guardian have now been completed on budget and the results have exceeded management expectations with production of the two previously shut in wells now at an aggregate rate of approximately 120 bopd compared to the initial mid-case projection of 88 bopd. The group is now planning a follow up stimulation programme of five wells to start as soon as possible with further follow on well candidates possible thereafter.

The Government’s policy relating to the price of the local benchmark crude for 2016 has been set at $67.50 per barrel which followed a 30% devaluation of the Peso. The price for crude produced in Salta is still unknown but last year there was a 10% discount on the stand rate which is not great but still above the price of crude in the general market. The new government intends to increase the amount of US dollars that can be paid out of Argentina to repay foreign originated loans with an increase from $50K per month to $2M.

The group is also announcing that Carlos Felices has stepped down from his role as country manager of Argentina having been appointed to the main board of the Argentine National Oil Company but whilst he is no longer an executive of the company, he will continue to provide advice as a part time consultant.

This is mostly positive stuff but unfortunately I think profitability here is some way off and I am not jumping in.

On the 22nd January the group released a Paraguay update. Following on from the results of the recent drilling campaign, it is now estimated that the Pirity and Hernandarias concessions together hold about 2.55Tcf and 425MMbbls of prospective resources net to the group in six identified main structures. In addition, the data shows more than 23 leads in Cretaceous and Palaeozoic plays in those concessions.

In the 100% owned Pirity concession, the ministry of public works has granted a year suspension for the time to complete the relevant work programme with an option to extend the suspension for a further six months subject to prevailing circumstances. The outstanding commitment under the contractual work programme is to drill one more exploration well before September 2017.

In the 40% owned Hernandarias concession, the group has relinquished a part of the concession in the northern part of the area but they have re-applied for a prospection permit for this area which is now known as the Don Quixote block and is pending approval subject only to obtaining an environmental license. The cost to earn in the further 40% of the concession has now reduced to $10M from the original figure of $17M and the work remaining commitment in the concession is one well to be drilled before October 2019.

The group has been granted a prospection permit over an area called Pilcomayo which is located between the Pirity and Hernandarias blocks and the prospectivity of this relatively small area is consifered promising. At Dermattei, after consideration of the work programme terms, the group has decided to terminate their farm-in agreement with Crescent and has therefore transferred operatorship to them, although they retain a 10% interest in the concession.

On the 2nd March the group announced that Chairman Peter Levine purchased 4M shares at a value of £200K to give him a total of 121,834,586 shares. This is a decent purchase but whether it is an attempt to halt the decline in the share price or he genuinely sees value in the shares is impossible to ascertain.

On the 7th March the group released an update. Current trading in Argentina and Louisiana continues in mine with management expectations with both trading profitably at current oil and gas prices. Louisiana remains a profitable contributor to the group whilst Argentina benefits from realisation prices of about $58 per barrel which, combined with a strongly depreciated peso, assists in keeping margins robust and acts as a cushion against domestic inflation levels. As it is now possible to transfer dollars out of the country, the operation is expected to become a net cash contributor to the group in H2.

The next set of workovers are due to commence by the end of March with purchase orders signed for an initial four well programme. The programme will be funded out of cash generated by the Argentine operation without the need to draw on the group’s facilities.

The company continues to plan a multi-well drilling programme in Argentina to materially increase production with a view to start drilling in H2 2016. Planning has now progressed to negotiations with contractors. With the improving investment environment in Argentina, it is anticipated that the funding of the drilling programme will be sourced out of existing and new bank facilities so on that basis, the board do not believe it will be necessary to raise additional equity.

The company continues to trade within its facilities with adequate headroom. Emphasis remains on rationalising core central admin costs and concentrating spend in countries where the group operates. Therefore, the company’s London-based full time finance director, Ben Wilkinson, has agreed to step down with immediate effect with his current responsibilities being shared between the existing group financial controller and an interim part-time CFO to be appointed as soon as possible. The company also intends to appoint a second non-executive director within the next three months.

It is good to hear that both regions will be profitable, even at this oil price, and given the low share price I think the group should do all they can to prevent the need for a placing to pay for the drilling campaign. I have mixed feelings about the finance director leaving. It will be good to save on his salary but it does feel a bit like a step backwards. The current environment in Argentina is now a lot less hostile and I feel this might be worth a punt so I have made a small purchase which I will probably live to regret!

On the 29th March the group released an update. The four well workover programme has started. They are on currently producing wells with three at Puesto Guardian and one at Dos Puntitas. Present trading in Argentina is operationally profitable, with planning and negotiations continuing in respect of the proposed H2 drilling programme which is expected to comprise an initial six wells.

They also announced the appointment of Jorge Dario Bongiovanni as a non-executive director. He is an Argentinian citizen and has worked for Repsol and Petrobras in South America. He now works for the IFC as a consultant.

On the 12th April the group gave an update on the Argentina operations. The four well workover programme has been completed at a cost of less than $400K, funded from the operating cash flow. This amount is less than a third of the cost of December’s workover programme due to rig-less working with a pumping unit. The programme increased production by about 150bopd and total production from the Puesto Guardian concession is now 500bopd. As part of field operations, a rolling programme of producing well workovers will now be started to mitigate the normal field declines with the cost of these to be paid out of cash flow.

The cost of these workovers looks very good and the increase looks useful too. I was for some reason expecting a bit more but these workovers look to have been successful in my view.