Moss Bros retails and hires formalwear for men, predominantly in the UK. They operate through Moss Bros branded mainstream stores, promoting a number of own branded sub-brands and third party brands. The group also trades through the premium Savoy Taylors Guild fascia. The other brands comprise Moss London, slim fit styles aimed at a younger audience; Moss 1851, tailored fit suits for business and leisure; Moss Savoy Taylors Guild, the heritage brand with luxury fabrics with a regular fit; and Moss Esq, great value suits for everyday wear with a regular fit.

It has now released its final result for the year ended 2015.

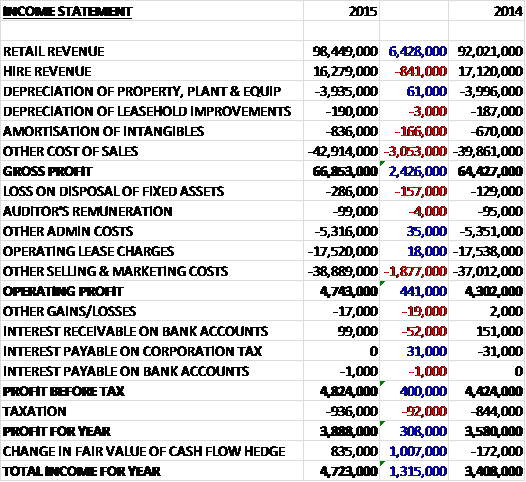

Revenues increased when compared to last year as an £841K decline in hire revenue was more than offset by a £6.4M increase in retail revenues. Cost of sales also increased to give a gross profit £2.4M higher than in 2014. Admin costs were broadly flat but a £1.9M growth in selling and marketing costs meant that operating profit came in £441K ahead of last tome. After less interest received on the bank accounts and a slightly higher tax bill, the profit for the year was £3.9M, a growth of £308K year on year.

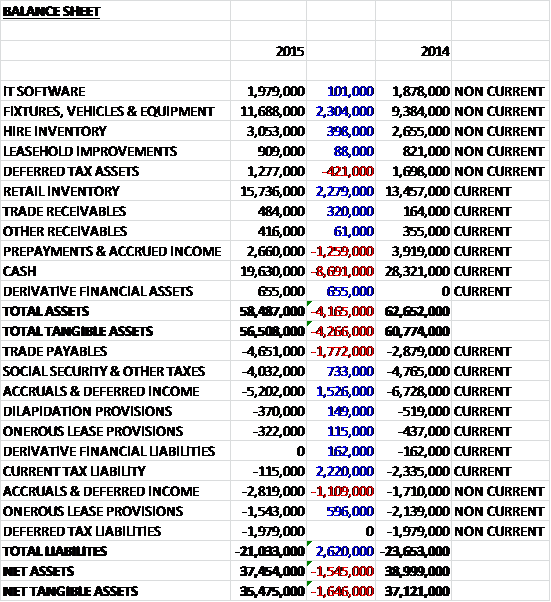

When compared to the end point of last year, total assets fell by £4.3M driven by an £8.7M decline in cash and a £1.3M fall in prepayments and accrued income, partially offset by a £2.3M increase in retail inventory and a £2.3M growth in fixtures, vehicles and equipment. Liabilities also fell during the year as a £2.2M decline in the current tax liability and a £733K decrease in other payables was partially offset by a £1.8M increase in trade payables. The end result is a net tangible asset level of £35.5M, a decline of £1.6M year on year.

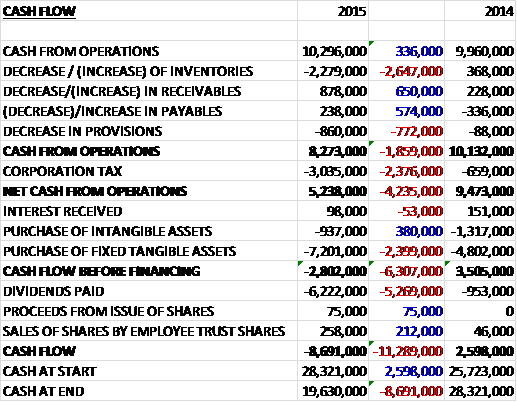

Before movements in working capital, cash profits increased by £336K to £10.3M but a large increase in inventories partly to support the earlier intake of new season’s lines, along with a £2.4M increase in corporation tax meant that the net cash from operations was £5.2M, a decline of £4.2M year on year. The group then spent £7.2M on fixed tangibles relating to the opening of six stores and the refurbishment of 14, and £937K on intangibles (IT) which meant that there was a cash outflow of £2.8M before financing. The group also paid £6.2M in dividends that were clearly not covered by cash flow so that the cash outflow for the year was £8.7M to give a cash level of £19.6M at the year-end.

The retail environment was more competitive during the year with heavy discounting around new events like black Friday. The group continued to develop their brands such as Moss London, Moss 1851 and Moss Esq. There was also investment made in the product offer with a more modern range through the Moss London brand, the development of a strong casualwear range and the launch of hire lounge suits. In addition, the group are taking part in the “Undercover Boss” TV programme which should help promote the brand to a wider audience.

The gross profit at the retail business was £53.3M, an increase of £3.4M year on year. The group have continued to implement operational improvements across the business and the programme of refitting stores, together with the successful launch of the new sub-brand line up, positively impacted like for like sales, which were up 7.1%. The promotional activity around Black Friday generated significant customer interest across stores and online and affected the pattern of sales and margin across key trading weeks, although there was some downward pressure on gross margins which ended the year 0.1% below the previous year.

During the year, six new stores were opened and nine were closed. The board are considering further new store opportunities over the next year and they now have 130 stores. The average lease length across the portfolio is now 53 months and they are targeting improved lease terms on renewal, of a ten year term, with a tenant only break clause after five years. The underpinning of hire and demand for e-commerce click and collect points, together with advantageous lease deals means there is an opportunity to expand the number of stores with good returns.

The gross profit at the hire business was £13.5M, a decline of £1M when compared to last year. Overall like for like sales fell by 3.6% in the year due to a decline in wedding hire items. Evening Wear, Royal Ascot and school proms showed good levels of growth. The group carried out a review of their product offer and customer experience. As a result they have invested in new hire stock, introducing their lounge suite offer with two new styles, introducing new styling in the morning suite offer, and adding to the branded ranges. A number of initiatives around stock management and customer comms have been launched and management is confident that the product availability will be improved for the new season.

E-commerce sales performed very strongly with the rate of sales growth at just under 59% and online sales now represent 7.8% of the total. Site traffic, conversion and retention rates are all on improving trends with returns rates currently at 23%, which sounds rather high. The mobile and tablet enabled website grew strongly and now comprises 35% of total e-commerce sales. Expansion into international markets is underway is underway with dedicated sites for Ireland, Sweden, Denmark, Netherlands and Australia and further territories are planned for next year. E-commerce has also proved to be an efficient way of clearing end of lines stock with faster sell through rates.

The early clearance of residual stock has enabled new season’s stock to be introduced in stores earlier, improving the customer offer and enabling greater scope for tactical promotions. The increase in direct sourcing from the Far East has increased exposure to foreign currency risk, though, which is being mitigated through hedges.

The hire website continued to gain traction and the group believe the recently added group hire functionality should support future growth. Results are apparently encouraging and there is evidence of wedding hire customers starting off online before going into stores to complete the transaction. A number of improvements are planned this year to improve conversion rates.

The store refit programme is now entering its fourth year and 58 stores are now trading with the new look format. Refitted stores achieve a three year payback criteria and the board are accelerating the refit programme with 27 stores planned for refit next year. This will impact on cash reserves but this is expected to be recouped quickly due to short payback period. Capital expenditure for the next year is expected to be about £14M (compared to £7.2M last year) which includes £7.5M for the refits and £2.5M hire stock.

During the year the group upgraded their stock control and distribution centre systems and plans are in place to upgrade their point of sale systems. The upgrade is largely cost neutral with lower annual maintenance costs offsetting higher depreciation charges. This upgrade will involve capex of £400K next year with additional costs of £200K being incurred during the implementation period. As well as introducing latest technology, the upgrade will also improve business efficiency and the customer experience.

Initiatives to provide a fully multi-channel offer to all customers offering a number of ways to shop have been implemented. The project to create a single customer database, including full customer transaction history, is nearing completion and offers significant CRM opportunities for the business. Once completed it will enable customers to shop for retail and hire seamlessly across a range of channels. Social media is also being used to gain traction for the brand across a number of platforms.

The group has contracted capital commitments of £3M and net operating leases of £85.5M, although of course they are spread over many years.

Group like for like sales in the first seven weeks of the new year are up 7.5% and early season wedding bookings for 2015 are showing an improvement on the prior year, although it is too early to say if this upturn will be sustainable.

At the current share price the shares trade on a PE ratio of 25.5 which falls to 23.3 on net year’s consensus forecast which looks rather expensive. On the other hand the shares do yield 5.4% after a 5% increase in the total dividend which seems pretty good.

Overall then this was a decent period for the group. Profits increased but net tangible assets did fall slightly. Operating cash flow also fell but this was due to a build in inventory and underlying cash profits increased year on year. It is notable that there was no free cash flow, however. The retail business is progressing well despite the effect events such as Black Friday have on margins as the new sub-brands and store refits increased profits. The hire business fared less well with declining profits due to a poor wedding season. The geographic expansion that comes with e-commerce looks interesting.

The increase in capex surrounding the store refits will likely reduce cash even further in the new year but the three year payback seems like a good investment. The new year has started well with sales up 7.5% on a like for like basis and the hire business improving due to a good start to the wedding season. The shares are certainly not cheap but the yield is pretty juicy if sustainable. In my opinion this looks like a quality outfit but the shares may be priced to reflect this.