Somero Enterprises designs, assembles and sells patented laser-guided equipment that automates the process of spreading and levelling volumes of concrete for commercial flooring and other horizontal surfaces such as paved car parks. The machines employ laser-guided technology to provide a high level of precision in concrete surface flatness at a higher rate of efficiency than conventional methods. The group has sold to contractors for non-residential construction projects in over 92 countries and the equipment has been specified for use in the construction of warehouses, assembly plants, retail centres and other commercial construction projects that require very flat concrete floors. The products have been used in projects for Costco, Home Depot, B&Q, Daimler Chrysler, various Coca-Cola bottling companies, the US Postal Service, Toys R Us and ProLogis.

Somero Laser Screed equipment holds an incredible 99% market share in the non-residential, horizontal concrete flooring industry. The target customer is the commercial concrete floor contractor of any size. They have assembly operations in Michigan and their HQ is in Florida. Revenues are generated from sales of large line products, sales from new small line products and sales from spare parts, refurbished machines, topping spreaders, mini screeds, 3D profilers, S-15R and accessories. They have now released their final results for the year ended 2014.

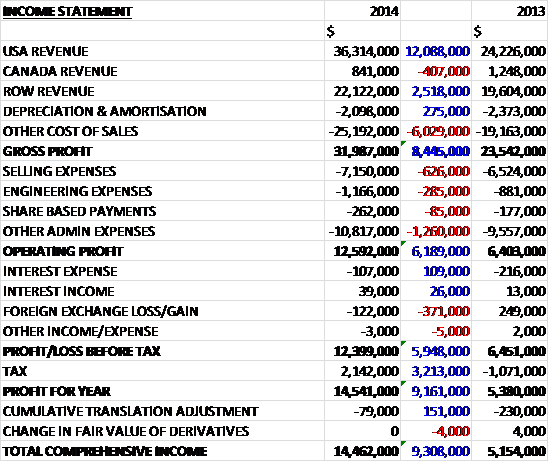

Revenues increased when compared to last year as a $407K fall in Canadian sales was more than offset by a $12.1M increase in US revenues and a $2.5M growth in ROW revenue. Cost of sales also increased despite a lower amortisation charge to give a gross profit some $8.4M ahead. Selling expenses increased by $626K, engineering expenses grew by $285K and admin costs were up $1.3M but operating profit was still $6.2M above that of last year. We then see a bit of a loss from foreign exchange changes which meant that pre-tax profit was $12.4M, an increase of $6M year on year before a $2.1M tax rebate due to a non-cash valuation allowance of $4.1M and $5.9M settlement of restricted stock units and settlement of stock options which are deductible for tax purposes, meant that the profit for the year came in at $14.M, an increase of $9.2M.

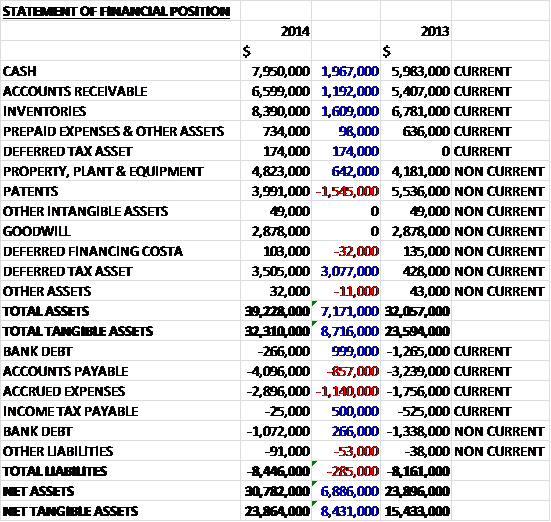

When compared to the end point of last year, total assets increased by $7.2M driven by a $2M increase in cash, a $3.1M growth in deferred tax assets, a $1.6M increase in inventories and a $1.2M growth in accounts receivable, partially offset by a $1.5M fall in the value of patents. Total liabilities also increased as a $1.3M fall in bank debt was more than offset by a $1.1M increase in accrued expenses and an $857K growth in accounts payable. The end result is a net tangible asset level of $23.9M, an increase of $8.4M year on year.

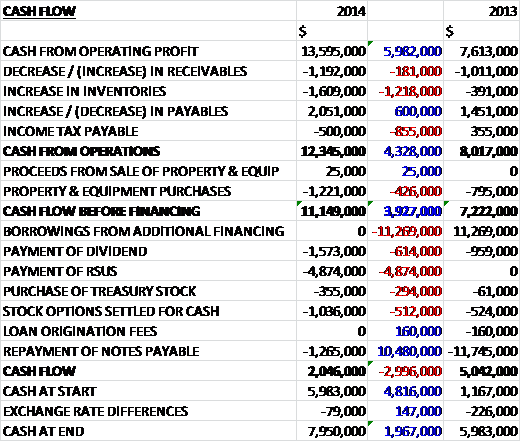

Before movements in working capital, cash profits increased by $6M to $13.6M. We then see an increase in payables more than offset by a growth in inventories and an increase in receivables to give cash from operations of $12.3M, an increase of $4.3M year on year. The group spent just $1.2M on capital expenditure relating to computer hardware and software upgrades, vehicle purchases, ERP upgrades and improvements to the Michigan facility, to give a free cash flow of $11.1M. The bulk of this money was used to pay restricted stock units, of which $554K were still outstanding at the year-end, and we also see $1.6M spent on dividends, $1.3M spent on the repayment of debt and $1M on stock options settled for cash. The end result is a cash flow of $2M and a cash level of $8M at the year-end.

The North American market performed well, increasing from $25.5M to $37.2M; the revenues from China grew by 44% to $9.5M; the European market saw a 20% increase to $3.6M and Australia along with SE Asia also saw strong growth. Russia and the Middle East experienced sales declines, however, due to political unrest in those regions. The substantial increase in revenue was driven by two new products, the S-15R and the S-485, the new sales people and increased construction activity. In all, large line sales increased to $22.4M as a result of a 52% increase in volume to 64 units; small line sales decreased to $9.7M due to a slight fall in units to 126 and other revenues increased by $7.1M to $27.2M. There were two customers that accounted for more than 10% of receivables – one of 10% and one of 36%.

All of the Asian markets grew substantially in the year, in particular in China. This growth is driven by increasing their penetration rate in all regions of China and the broader awareness of US floor flatness standards now issued by the China Flooring Association. The Chinese economy is evolving towards more logistics, big box retailing and e-commerce which increase owners’ demands for the speed and flatness provided by the group’s equipment and they invested in an additional $800K to expand the team by five people to 19 employees. The new office is larger than the HQ in Florida and will include the Somero Concrete College and warehousing for over $1M in spare parts and equipment inventory to service the country.

In SE Asia, sales increased from $400K to $700K. The group expect to see strong growth from this region and they will increase their market awareness and penetration as evidenced by the sale of two large line screeds and two 3D profilers for the start-up of a multi-year project in Jakarta which will create a dedicated bus line with concrete pavement in early 2015. Sales in India were very good for the initial phases of penetration into this significant market. Marketing efforts have been stepped up and the group continue to invest in sales and develop revenue opportunities. Europe continues to recover and demonstrated growth year on year. Latin America remained flat due to the Brazilian economy and sales in Russia and the Middle East were slow due to the geo-political changes that occurred during the year.

During the year the group introduced the S-485 Laser Screed. It is designed for easier set-up and operation and requires one less person to operate and only one person is needed to establish a grade or fine tune the programmable height receivers. They have had a good response to the new machine as it was introduced in October and contributed $900K in sales during those three months.

Due to the anticipated growth of the business, the board has concluded that the current global HQ in Fort Myers will not be large enough to accommodate future growth. As a result the company has entered into an agreement to purchase land to build a new global HQ at an expected cost of up to $4M spread over two years. They also plan to expand their Michigan facility at an approximate cost of $1M.

The group have started to devise an education programme specifically for the Chinese market that they are calling the Somero Concrete College. This programme will educate and train the group’s customers to become industry leaders in placing a concrete floor successfully. The group’s current facility in the country will be utilised for the training grounds, regional sales office, customer service call centre and parts warehousing. In addition to the college, they are also launching their Screed Training programme at the facility. This programme is specifically designed for new customers and will educate them in proper operation and maintenance of a newly purchase Somero Laser Screed. This training programme will be similar to the one currently provided in the US. The completion of the college will occur in Q4 2015.

The group’s financial performance is affected by a number of factors, especially the cyclical nature of the non-residential concrete construction industry, as well as the varying economic conditions of the geographic markets they operate in, particularly North America, Western Europe and China. They are particularly affected by construction projects from large North American retailers such as Wal-Mart and Costco where their large laser screed products have been utilised. Their performance is also dependant on the replacement and refurbishment of older products as they reach the end of their expected life cycles. Somero equipment is in a period of demand for replacement and refurbishment as older machines reach the end of their lifecycles.

Strong US sales momentum has carried forward into 2015 as a result of the new product introductions, replacement demands on outdated technology and the ongoing construction growth that the group’s customers are experiencing – this growth trajectory is expected to result in strong sales for 2015. The penetration rate in China is currently only about 1% and the board see the country as a key growth driver. Customers there now have access to financing options made available specifically for Somero equipment which is expected to have a positive impact on sales in the region. Growth is anticipated in Latin America outside of Brazil’s economic slowdown. This was driven by strong Q4 sales in Mexico, attributed to the manufacturing sector, and is continuing into 2015. After a sound start to the new year, the group are confident that this will be a year of solid growth for them

The group has a net cash position of $6.6M compared to $3.4M at the end of last year. After a 150% increase in the total dividend this year, the shares currently yield 2.7% increasing to 2.8% on next year’s consensus forecast.

Overall then this seems like an interesting company and the past year has been a good one. Profits are up, net assets increased and operating cash flow improved to give both a decent free cash flow and a comfortable net cash position. The markets in the US and Europe seem to be improving and China appears to be a big potential growth driver whilst the Middle East, Russia and Brazil are proving to be a drag on results. There are some things to watch out for – this market is very cyclical and although the geographic diversity does mitigate this risk somewhat, the US still makes up the bulk of profits and a slow down here would have drastic consequences. Also, one customer makes up about a third of all receivables which is never a good place to be and there seems to be quite a lot of capex being mooted with the new HQ, Michigan factory and the dubious sounding Concrete College. There is also the lingering doubt about a foreign company listed on AIM. Overall though, the net cash is a nice cushion and the 2.7% dividend yield is pretty good for a fast growing company like this.