Vertu has now released its interim results for the year ending 2016.

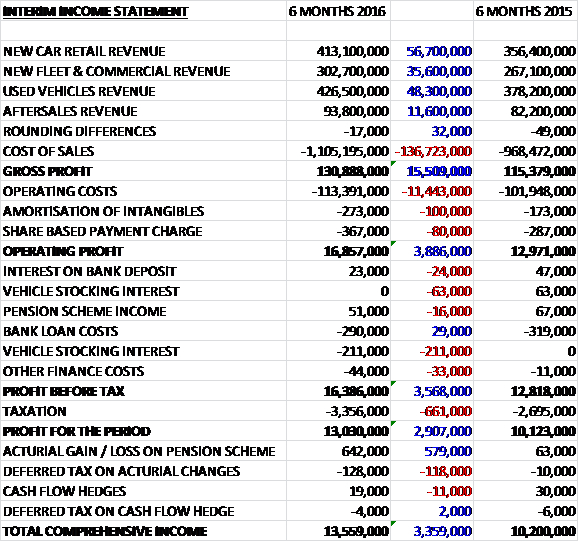

Revenues increased when compared to last year with a £56.7M growth in new car retail sales, a £48.3M increased in used vehicle revenues, a £35.6M growth in new fleet and commercial revenue and an £11.6M increase in aftersales revenue. Cost of sales also increased to give a £15.5M growth in gross profit. Operating costs also grew during the period so that operating profit was some £3.9M above that of last time (with new acquisitions contributing a loss of £384K). We then see a negative swing in vehicle stocking interest and an increase in tax which meant that the profit for the period was £13M, an increase of £2.9M year on year.

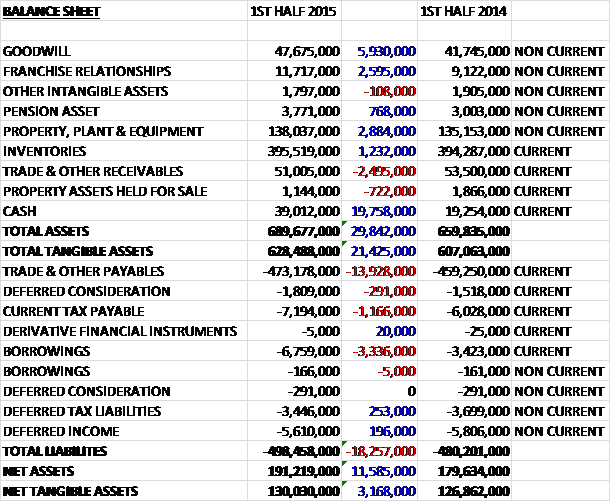

When compared to the end of last year, total assets increased by £29.8M driven by a £19.8M growth in cash, a £5.9M increase in goodwill, a £2.9M growth in property, plant and equipment, a £2.6M increase in franchise relationships and a £1.2M increase in inventories, partially offset by a £2.5M decline in receivables. Liabilities also increased during the period due to a £13.9M growth in payables, a £3.3M increase in borrowings and a £1.2M growth in current taxes payable. The end result was a net tangible asset level of £120M, an increase of £3.2M during the period.

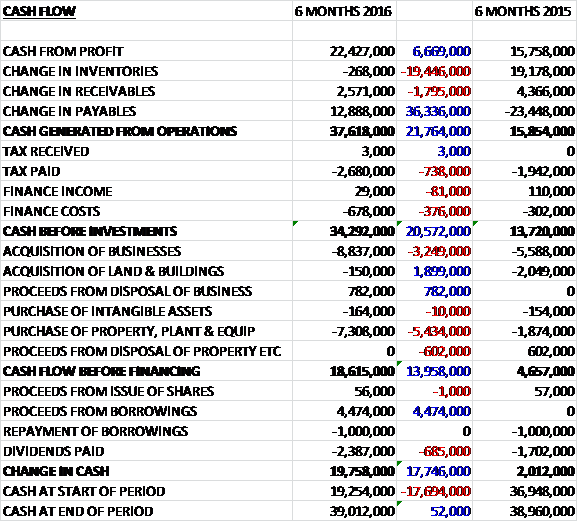

Before movements in working capital, cash profits increased by £6.7M to £22.4M. We then see a large decrease in payables (which seem to be related to lower VAT payments due to fluctuations in new car consignment inventory levels) push the cash generated from operations to £34.3M, an increase of £20.6M year on year. The group then spent £8.8M on acquisitions and £7.3M on property plant and equipment to give a cash flow before financing of £18.6M. We then see a curious increase in borrowings which dwarfed the increase in dividends (presumably the cash level at the period end give a very favourable impression compared to the average cash levels) which meant that there was a cash flow of £19.8M and a cash level of £39M at the end of the half-year.

The UK automotive sector has continued to respond positively to the supply push of new vehicles into the market by manufacturers reacting to weaker demand from other global markets and helped by the strong Sterling. This resulted in further growth in UK new vehicle registrations in September, albeit with slowing growth in private new retail registrations with the balance picked up by stronger fleet activity. After three years of growth in new vehicle registrations, the supply of used vehicles has now normalised from the previous period of supply constraint.

The UK economy continues to display positive growth and consumer demand remains buoyant and responsive to finance led offers for new cars which are being made available. The latest SMMT forecast for the total UK new car market for 2015 is £2.6M and the forecast for 2016 is expected to remain flat. The board expect to see a period of stability in the UK car market in the short to medium term.

Like for like new retail sales were up 1.2% against a growth of 1.8% in private registrations for the franchises represented by the group as a whole as the market data includes pre-registered vehicles with levels of dealer self-registration growing. Like for like Motability vehicles sales were up 6%, gaining market share in a market that declined 0.5% during the period. Motability is an important area for the group and represents over 22% of total new car retail sales for them. Motability customers display very high levels of aftersales retention during their three year contract and the group is currently Motability Operations Dealer of the Year. The like for like vehicle gross profit grew by 4.8% in the period as manufacturer targets were achieved at high levels, maximising earnings, which resulted in stable vehicle gross margins of 7.3% as the average selling price per car strengthened from £13,342 to £14,213.

Like for like new car fleet sales fell by 8.5% following a shift in sales mix with reduced supply to lower margin daily rental channels. Gross profit per unit improved, however, resulting in like for like gross profit generation. The fleet business is subject to periodic fluctuations in channel mix as manufacturer strategies and customer requirements change. Like for like commercial new vehicles sales grew by 24.2% against a market that rose 16.4%, reflecting the willingness of both large and small enterprises in the UK to invest in their business. Lower fuel prices have supported this trend, encouraging transport businesses to invest in their vehicle fleets.

Like for like used retail vehicle sales grew by 4.2% against a very strong performance last year as the used car market returned to more normal levels. Like for like margins and gross profit per unit both declined, however, in line with the board’s expectations. The group remains focused on maximising used car return on investment. Rising stock levels from self-registrations and increased used car depreciation have put pressure on returns with the above market average returns for the group falling from 126.3% to 115.2%.

Like for like aftersales revenues increased by 3.7% and gross margins were up from 43.7% to 45.5%. In the high margin service area, like for like revenues grew by 6.2%. Increased sales of service plans have improved customer retention into the service channel, particularly of older used cars. Lower margin fuel sales declined significantly with depressed fuel prices creating a pull on revenues but improving margins.

In non-dealership businesses, Bristol Street Versa, which is a converter of wheelchair accessible vehicles, is now profitable after having undertaken a turnaround plan since its acquisition in 2011. The group currently has 5% of the UK Motability wheelchair accessible vehicle market and supplied 222 vehicles in the period, the bulk of which were procured from the group for conversion. They also supplied 419 vehicles to the Taxi Centre which was acquired in November. Its performance has been in line with expectations and is making an increasing contribution to the group.

In March 2014 the group entered into a business arrangement with Haymarket to jointly operate the What Car Leasing platform. This online portal provides UK automotive retailers with a route to market to customers who wish to purchase new cars via a leasing model. The business generates advertising revenues from the retailers on the website. It continues to be developed and its contribution to the group is increasing, generating over 72,000 enquiries for its subscribers in the period. An expansion of the group’s joint operations with Haymarket is currently being planned.

During the period the group added nine outlets, disposed of one and closed three so that it now operates 119 sales outlets in total. Of the £152.2M increase in revenues, acquisitions in the period accounted for £20.6M of growth and the businesses acquired last year contributed £94.4M which meant that core group revenues increased by 5.2% reflecting increases in vehicle sales and aftersales whilst closed or sold businesses accounted for a decline of £17.3M.

In April the group became the sole franchise partner in Glasgow for Nissan and began to operate from temporary facilities in the North of the city to complement the existing South Glasgow business. In September a significant freehold property was acquired for £3.9M close to the city centre which will be turned into a landmark Nissan dealership in the coming year. The new dealership development will occupy about half of the site acquired with the remainder earmarked for re-sale. In April the group closed its sub-scale Peugeot dealership in Ilkeston and in July they disposed of the Dunfermline Peugeot dealership – there were no significant costs incurred due to these closures. In July they refranchised the former Suzuki outlet in Mansfield to become a Dacia and Renault facility which saw them exit from representing Suzuki. Also, a peripheral aftersales outlet acquired in the Bolton Ford acquisition was sold, realising cash of £700K.

There were a number of acquisitions during the period. In April the group acquired Bury Land Rover in Lancashire from Pendragon for a total consideration of £7M which was settled in cash from existing resources. The group came with no net tangible assets so this consideration was goodwill plus £2.6M allocated to franchise relationships. In May the group acquired Bradford Jaguar from Lancaster PLC for a total consideration of £826K which was settled in cash from existing resources representing goodwill of £750K. In June the group acquired Blacks Autos which operates a Skoda dealership in Darlington. The total consideration amounted to £1.5M settled in cash from existing resources with goodwill of £765K.

The group are engaged in a substantial programme to refurbish and redevelop a number of dealership to latest manufacturer standards. A number of these projects have been completed in the period including the development of a Ford Store in Orpington, completion of Nottingham VW South and a number of Vauxhall refurbishments. The substantial redevelopment and enlargement of the Vauxhall dealership in Waltham Cross has also now been completed. A number of projects are currently ongoing including the development of a Ford Store at Bristol Street, Birmingham and the refurbishment of Mansfield VW.

There were a number of further acquisitions after the period-end. In September the group disposed of a satellite dealership acquired with the Gordons of Bolton acquisition in November 2014. The site in Lancashire realised £1.4M in cash. Also in September the group purchased long leasehold dealership premises in Exeter for a consideration of £2.4M which will be refurbished to allow the future relocation of the existing Hyundai and Renault van operations. They also purchased a freehold property in Glasgow for £3.9M for future development for the Nissan franchise. In October the group acquired SHG Holdings which operated Audi, VW passenger and VW commercial outlets in Hereford. The consideration of £12.8M was satisfied in cash from existing resources and £1.5M is to be deferred for two years to be paid under certain conditions. The group will be investing about £1.5M into the redevelopment of Hereford Audi next year.

In October he group ceased sales operations at two multi-franchised dealerships – Cheltenham Alfa Romeo and Bristol Jeep. Aftersales operations are retained at these locations. In addition, a petrol forecourt operated alongside the Stroud Ford dealership was closed to allow the expansion of used car operations.

While the SMMT data has reported September’s private new vehicle registrations for the franchises represented by the group as being flat, Vertu’s private new vehicle sales were 3.3% below that of September last year. Despite this, new car profitability was a record for the month and along with a solid performance in used vehicles with like for like volume growth of 5.4%, and aftersales, this has established a sound base for the balance for the rest of the year. September profits were ahead of last year with strong turnarounds delivered in a number of businesses acquired in recent years.

After the most recent acquisition, VW franchises now represent about 9%. The manufacturers and retailers are currently working together to ensure that any impacted vehicles are identified and issues resolved. In the near term this is likely to boost aftersales revenues. The group has to date witnessed no significant decline in total vehicle sales volumes or used car valuations above normal seasonal variations in the four VW group brands. After continued strong trading in September with results ahead of last year, the board now anticipate full year results will be ahead of expectations.

At the period end the group had a net cash position of £32.1M compared to £34.4M at the same point of last year. After a 29% increase in the interim dividend, the shares are now yielding 1.6% increasing to 1.8% on the full year forecast.

Overall then, this was a very good six month period for the group. Profits were up, net assets increased and operational cash flow improved to give a decent amount of free cash, although these levels were distorted by large increases in payables. The UK car market is still improving although the rate of growth does seem to be slowing, something that may continue if the supply push comes under threat from improving conditions in the EU. New sales growth seems to be sluggish but Motability is doing well, as is commercial with increased profits per unit. Used car sales were up but profits per unit fell as used car depreciation increased. The all-important aftersales unit did well with increased profits driven by the services business.

The collaboration with Haymarket does sound interesting and the other peripheral businesses seem to be contributing more to the group. After the period end, a net £17.7M has been spent on acquisitions and capex so the cash levels could be coming under threat but despite falling volumes, profits in the important month of September are head of last year which means trading for the full year is expected to be ahead of analyst predictions which is always good to see. The VW scandal doesn’t seem to have hit sales yet but one would expect it will at some point, but this may be mitigated by increased work in the aftersales division. At 1.8% the dividend yield is not much to write home about but I am sorely tempted to buy in here.

This chart is looking rather good too.

On the 1st December the group announced that it had acquired Who’s Ace Holdings, an operator of a well-established online vehicle parts business based in Kent. The business has built a presence in the non-franchised, online automotive parts market and there should be a significant opportunity to apply Who’s Ace’s ability to efficiently manage fitment data and establish the sale of genuine, franchised parts online. Bringing together this data capability with multi-franchise parts supply will provide the opportunity to accelerate growth in the parts sales channel to both retail end users and independent garages.

Total consideration is estimated at £2.2M which includes an earn-out over a five year period which would include goodwill of £1M. The initial payment of £1.8M has been settled in cash from the group’s existing resources. Last year the business generated EBITDA of £600K and the board expect the acquisition to be earnings enhancing in its first full year of ownership. This looks like a very nice little acquisition in an interesting new niche to me.

On the 25th January the group announced the acquisition of three Honda dealerships in Nottingham, Derby and Stockton on Tees from Lookers for a total consideration of £2M. This consolidates the group as Honda’s largest retail partner in Europe with 12 car dealerships. The acquisition generated goodwill of just £200K and has been settled in cash from existing resources. Last year the three outlets achieved a break even trading result and the board expects them to be earnings enhancing in their first full year of ownership. This looks to be an excellent deal to me.

On the 1st March the group announced the acquisition of Sigma Holdings and its subsidiary Greenoaks for a total cash consideration of £21.9M, of which £18.4M has been settled immediately with a further £3.5M being deferred for a year. In addition to the purchase, vendor shareholder loans of £9M have been settled in cash on completion by the group. The business operates the Mercedes outlets in Reading, Ascot and Slough with Ascot being an AMG performance centre. This represents the first foray into Mercedes retail. Each of the dealership freeholds is owned by Greenoaks, which is good to hear and the transaction generates goodwill of £13M. Last year the business made a pre-tax profit of £1.2M and the board expects the acquisition to be earnings enhancing in its first full year of ownership.

I have to say that this seems a bit expensive to me and I hope the group are not over-extending themselves.

On the 8th March the group released a pre-close trading update where they state that the trading performance for the year is expected to be ahead of current market expectations.

Vehicle servicing like for like revenues were up 5.6% which helped improve the group’s like for like aftersales gross profits, which increased by 6.7%. This performance was driven by strategies in customer retention into service and vehicle health checks performed on all vehicles vising the group’s service departments. Margins rose in each area of aftersales including service, parts, accident repair and petrol forecourts.

New car retail sales volumes grew by 6.5%, ahead of the UK market growth of 3.6% which meant that market share also grew. Like for like new vehicle gross profit per unit also grew as manufacturer targets were achieved. The group continued to grow their market share of the light commercial van market with like for like sales volumes up by 15.4% on improved margins whilst their fleet car business continued to shift away from supply to lower margin daily rental channels which meant that like for like profit performance improved.

Used car marketing activity has increased which resulted in like for like volume growth of 10.8% in this category. This is significantly ahead of the estimated overall used car market growth and resulted in the group increasing its market share here too. They have increased gross margin on a like for like basis by 5.4%.

At the start of March, Tim Tozer, former chairman of Vauxhall motors, jointed the board and the group also appointed Liz Cope as Chief Marketing Officer with effect from April 2016, representing a new position for the group. She was previously VP Global Marketing for Vax.

The board sees the UK new car market stabilising at current levels and the key drivers of supply push from European manufacturers are likely to stay in place for the medium term. The order book for retail new cars on a like for like basis so far in March was 11.6% ahead of last year and current trading is robust.

The board have identified a number of near term acquisitions comprising both premium and volume dealerships which would add a new manufacturing partner. In order to finance these opportunities, they are considering options to raise further capital for the group including a potential equity issue and a review of its borrowing facilities with a view to introducing property backed, fixed interest long term debt.

Then, just one day later, the group announced a proposed placing to raise £35M at 62.5p per share which represents a discount of 8.8% on the closing price yesterday. The placing shares will represent about 14% of the enlarged share capital and certain directors have indicated an intention to invest £300K as part of the placing.

The placing will enable the group to further expand its portfolio through the acquisition of additional dealerships which the board expects to comprise both existing and new manufacturer partners. Three near term acquisitions have already been identified with a combined consideration of about £26M and will add a new manufacturing partner. The remainder of the proceeds will be used to pursue other acquisition opportunities. The group is also reviewing its borrowing facilities with a view to utilising the security of its substantial freehold property portfolio with a view to mortgaging the properties up to £50M.

So, we have an excellent update followed one day later by a placing. This is very poor form in my view – why not just announce the placing alongside the update? Anyway, I do not really like the way this company is going. It is going to forego its prudent approach and instead embark on a spending spree using placings and more debt. Is this really the right time in the cycle to be going down this route? Sadly these shares are not for me at the moment – what a shame after the excellent progress they made this year.