Bioquell has now released its interim results for the year ending 2015.

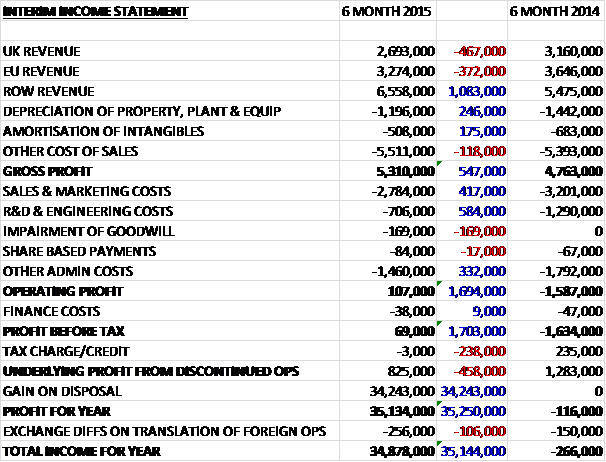

Overall revenues increased modestly when compared to the first half of last year as declines in UK and other European revenue was more than offset by a £1.1M growth in revenue from the rest of the world. Depreciation and amortisation were both down slightly and after a small increase in the other cost of sales the gross profit was £547K above that of last time. Sales and marketing costs reduced, as did R&D costs and despite a £169K goodwill impairment, admin costs also fell along with finance costs before the lack of a tax rebate this time meant that before discontinued operations, the profit for the half year stood at £66K, an improvement of £1.7M year on year. We then see an £825K contribution from the discontinued operation and a £34.2M gain on disposal to give an actual profit for the period of £35.1M.

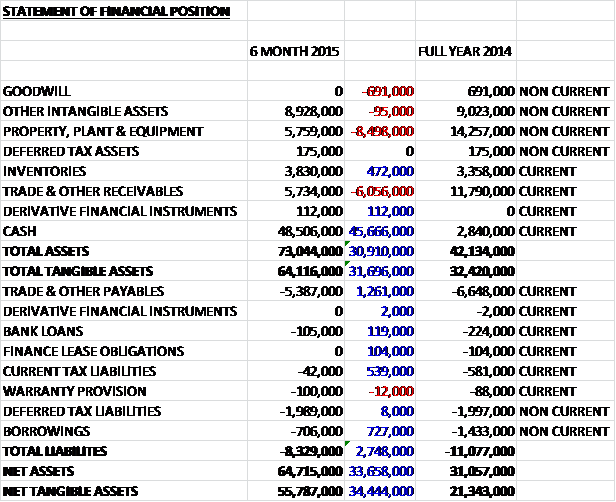

When compared to the end point of last year, total assets increased by £30.9M to £73M driven by a £45.7M increase in cash and a £472K growth in inventories, partially offset by an £8.5M fall in property, plant and equipment, a £6.1M decline in receivables and a £691K fall in goodwill. Total liabilities declined during the year due to a £1.3M fall in payables, a £846K decrease bank loans and a £539K decline in current tax liabilities. The end result is a net tangible asset level of £55.8M, an increase of £34.4M over the past six months.

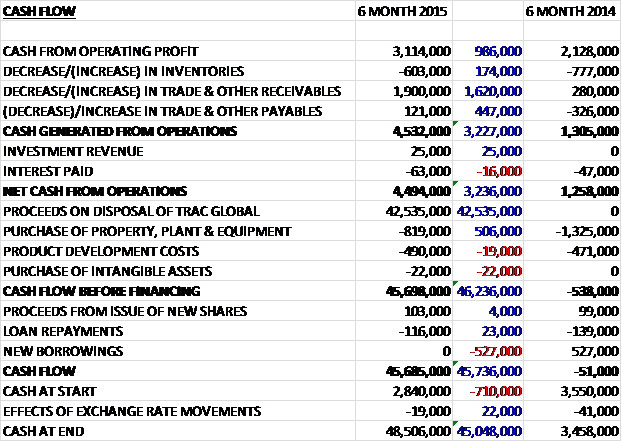

Before movements in working capital, cash profits increased by £986K to £3.1M. A large fall in receivables then drove the net cash from operations up to £4.5M, an increase of £3.2M year on year. The group spent £819K on tangible fixed assets and £490K on product developments to give a decent amount of free cash flow before the £42.5M proceeds from the disposal of Trac Global meant that the cash flow for the year was £45.7M to give a cash level of £48.5M at the period end.

The changes made in the Bio division’s cost base last year means that it is just about profitable now at the operating level. The group are beginning to see the benefits of the new products, services and consumables that have been developed and launched over the past couple of years and the underlying demand in the core life sciences and healthcare markets is increasing.

Life Sciences orders increased by 3% year on year as the new products are gaining traction in the market, in particular the QUBE order book was up 50% to £1M at the end of the period. As expected, life sciences revenues declined by 16%, however, to £8.2M reflecting the phasing of deliveries from the order book as well as the decline in revenues associated with the hydrogen peroxide vapour equipment. Demand for the QUBE product continued to grow from a broad range of customers around the world. Although the product is primarily sold into sterility test and hospital pharmacy applications, it is now beginning to sell into biotech research and low volume biotech manufacturing applications.

The life sciences revenues in the US market increased during the period. The changes made in the US business a year ago are starting to be reflected in the financial results of the business. In contrast the group continues to find the market in China much slower than a few years ago and they are looking at new ways of generating profits in the country. Revenues from the higher margin consumable products continued to grow. The consumables range currently comprises hydrogen peroxide cartridges as well as biological and chemical indicators used to help customers obtain and maintain regulatory approvals.

Revenues from the healthcare business increased 22% to £2.1M. The US showed strong growth and now accounts for about half of worldwide revenues. Factors that are driving this increase include increased awareness following micro-biological contamination linked to the treatment of Ebola patients in US hospitals as well as increasing concerns about hospital acquired infections. The HPV technology was also used to help bring the MERS outbreak in South Korea under control.

The new healthcare product, BQ-50, was launched in May and the order book is beginning to grow. This product incorporates a number of new technologies which make the product easier to use which results in faster eradication of pathogens in hospitals. The product also enables the group to provide lower-cost, more flexible bio-decontamination service offering to hospitals in the US and Europe. Sales of the pod product were slower than expected and a number of changes have been made to the way in which the product is promoted which it is anticipated will help drive growth in healthcare revenues in the second half of the year.

Defence revenues increased from £800K to £2.2M during the period. The group continued to see demand for the specialist filtration equipment from a number of customers around the world, particularly in the Middle East. They have developed a flexible range of modular CBRN products which enable them to produce cost effective solutions to international vehicle and fixed installation manufacturers.

Service related revenues fell by 5% to £5.7M, reflecting a decline in Room Bio-Decontamination Service revenues partly due to a greater number of large emergency RBDS contracts in the first half of last year. The group believe there are a number of new applications for this service arising from biotech applications and they are in the process of increasing their marketing of the service to capture these applications.

In May the group sold TRaC Global, which carried out the group’s testing, regulatory and compliance work. During the period the business contributed £600K to net operating cash flows and had a pre-tax profit of £1M. The disposal brought in £44.5M in cash and there was a gain of £34.2M on disposal so they certainly seem to have got a decent price for the sale but it is disappointing and perhaps a little short sighted in my view to sell your most profitable and growing business. The majority of this cash is intended to be returned to shareholders but this has been deferred pending the outcome of the strategic review.

The increasing demand for the QUBE product is offsetting the decline in older hydrogen peroxide vapour equipment and the group launched their new product, BQ-50, for the healthcare market. Overall the group is on track to meet the board’s expectations for the full year.

There are no interim dividends so the 2.4% dividend yield still applies for the full year. After the receipt of cash from the TRaC sale, the group has a net debt position of £47.7M compared to £1.1M at the end of last year.

Overall then this seems to have been a year of improvement for the underlying bio business. Profits did increase but were still negligible, net assets improved as a result of the gain on the TRaC sale and perhaps most importantly, operating cash flow improved with a decent amount of free cash generated – although this was boosted somewhat by the reduction in receivables. Operationally, the largest division, life sciences, seems to still be struggling somewhat due to a decline in older HPV equipment and subdued Chinese demand but hopefully the growth in QUBE can take up some of the slack. Progress in the other two divisions was good with the BQ50 product likely to improve healthcare revenues going forward. I do think that the TRaC sale is a bit disappointing and the return of cash is dominating proceedings here but I do quite like the company overall.

The share price seems to be going no-where fast at the moment.

On the 14th January the group released a pre-close trading update for 2015. Trading since the half year point has remained broadly consistent with board expectations. Revenues for the year are expected to be flat. Life Sciences revenues grew by 1.8%, reflecting a strong second half but healthcare revenues declined by 2.2% and defence revenues were 13.7% lower at £3.5M. Pre-exceptional profit is expected to be in line with board expectations but an exceptional charge of £200K will be booked this year to reflect headcount reductions in Q4. There will also be an exceptional profit of about £34M associated with the sale of TRaC in March.

In all the company had net cash of £47.5M at the year-end and the strategic review is expected to draw to a conclusion around the end of Q1 2016.