Empresaria has now released its interim results for the year ending 2015.

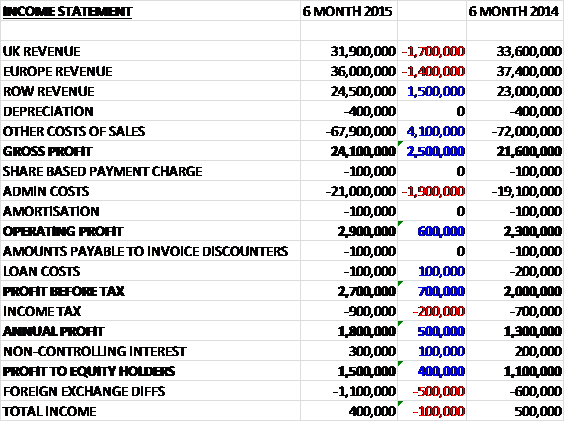

Overall revenues declined year on year as a £1.5M growth in ROW revenue was more than offset by a £1.7M fall in UK revenue and a £1.4M decrease in European revenue. Cost of sales also fell, however, to give a gross profit £2.5M above that of the first half of last year. Admin costs did increase though so that operating profit increased by £600K. Loan costs decreased slightly but this was offset by an increase in tax so that the profit attributable to equity holders came in at £1.5M, an increase of £400K year on year.

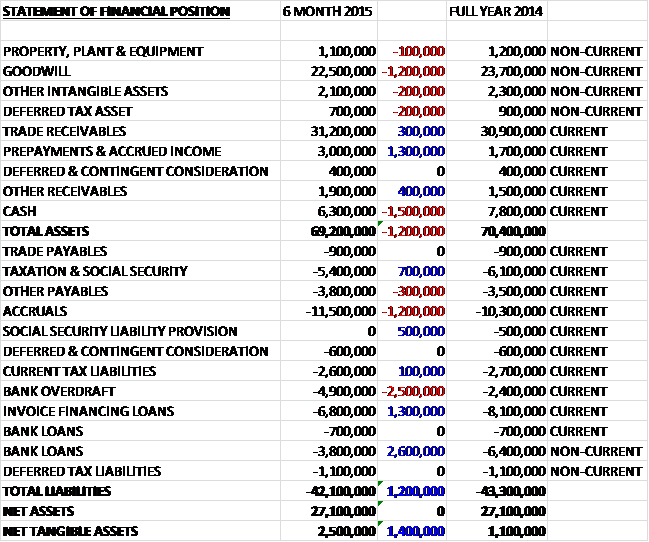

Total assets fell by £1.2M when compared to the end of last year driven by a £1.5M fall in cash and a £1.2M decline in goodwill partially offset by a £1.3M increase in prepayments and accrued income. Liabilities also fell during the period as a £2.6M fall in bank loans and a £1.3M decline in invoice banking loans were partially offset by a £2.5M increase in the overdraft and a £1.2M growth in accruals. The end result is a net tangible asset level of £2.5M, an increase of £1.4M over the past six months.

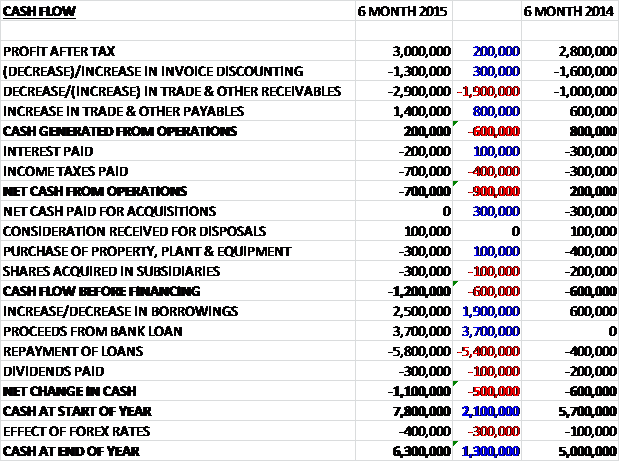

Before movements in working capital, cash profits increased by £200K to £3M. We then see this cash flow collapse, mainly as a result of a large increase in receivables so that after higher taxes are paid, there is a net cash outflow of £700K from operations, compared to a £200K inflow last time. The group then spent £300K on fixed assets and £300K on extra shares in subsidiaries so that the cash outflow before financing was £1.2M. We then see a net £400K increase in borrowings and a token £300K in dividends so that the cash outflow for the period was £1.1M to give a cash level of £6.3M at the end of the half, although the first half is traditionally weaker for cash flows.

The UK operating profit was £1M, flat when compared to the first half of last year which reflects in the investment made in staff. UK revenues were down 5% due to a £3.7M decline after the end of the Heathrow T2 project and a £2M impact from the planned reduction in low value work. There was a 37% increase in permanent revenues, half of which arose from the acquisition of Ball and Hoolahan last year with growth across Financial, Technical & Industrial and Domestic services. The temporary margin grew from 13.1% to 14.5% which helped offset the lower revenues from Technical and Industrial so the temporary NFI was only slightly down on the prior year before the contribution from the permanent NFI meant that total NFI increased by 19%.

Market conditions remain positive, in particular in the financial sector. Within technical and industrial, the largest brand is refocussing sales efforts further away from the low value end of the market which is having the effect of reducing productivity in the short term which is expected to continue for the rest of the year.

The operating profit in continental Europe was £1M, an increase of £400K year on year, aided by cost savings and the exit from the loss making GiT business. Revenue decreased by 4% to £36M due to the disposal of the business in the Czech Rep and closure in Slovakia along with adverse currency movements. NFI was also affected by currency movements and fell slightly but the temporary margin increased from 17.8% to 18.4%.

In Germany the logistics services division performed strongly with revenue growth of 24%. Within the temporary division revenue was stable with cost savings helping to improve profit contribution. Market conditions in the country were positive during the period despite the uncertainty around the Greek debt crisis. In the healthcare business, the economic situation in Finland remains difficult. NFI income was down but this was offset by lower costs and the business continues to increase its sales with local candidates as it transitions away from an import model.

The operating profit in the ROW was £900K, an increase of £200K when compared to the first half of 2014. Revenues increased by 7%, primarily from permanent sales which grew by 24% which was helped by the investments made last year in new office openings and the acquisition in Dubai. Together these represented 15% of the growth, with stand-out performances also in Australia (IT, digit & design), Thailand (executive search) and India (offshore recruitment). Against this there was a disappointing result from China and the training business in Indonesia, both of which are reducing costs in line with lower sales.

Temporary sales were up 1%, not helped by adverse currency movements, particularly in Australia and Japan. There was good growth in Chile in temporary sales but this was partially offset by a reduction in the traditional outsourced services. In Japan the retail sector faced candidate shortage issues which negatively impacted revenue and profit. The temporary margin across the region was stable at 13.5%. Costs increased due to the investment in new staff, albeit largely in India where pay rates are lower and where a second centre was opened to accommodate sales growth. This centre was filled quicker than anticipated so they are now looking to open a third centre in the second half of the year, earlier than originally planned. Market conditions in the region are generally favourable, although the economic situation in SE Asia could lead to a slowdown in that region. In the largest markets outside SE Asia (Japan, UAE and India), the board see continued growth prospects.

In June the group increased their interest in the executive search business in Indonesia by 10%, taking it up to 90%, for a cash consideration of £300K. During the period they also closed the GiT operation in Slovakia and sold the operation in the Czech Rep, generating costs of £100K. They do not anticipate any material purchases of minority shares during the rest of the year. The number of management shareholders did not increase during the period but matters are apparently progressing with a number of brand managers that are expected to be finalised before the end of the year. In the second half of the year, it is expected that the deferred consideration of £500K will paid regarding the Ball and Hoolahan acquisition.

During the period the UK revolving credit facility of up to €10M was repaid, replaced by new facilities in Germany provided directly to the subsidiary there. The new facilities comprise a term loan of €5M and an increase in overdraft facilities of €5M to €8M. It is expected that the UK term loan of £500K will be repaid in the second half of the year to be replaced by a temporary increase in the UK overdraft. In total the group still has undrawn facilities of £8.2M.

The group are experiencing currency headwinds in some of their key markets, in particular Continental Europe, Japan and Chile, which is expected to negatively impact the second half performance. Based on trading in the first half and the opportunity seen in the various markets, the board are confident that results for the full year will be ahead of current market expectations, delivering further growth. Despite the increase in permanent recruitment compared to temporary this year, the focus going forward is still focused on temporary recruitment.

The net debt position at the end of the period was £9.9M compared to £9.8M at the end of last year and £14.2M at the half year point of 2014. The group does not traditionally pay an interim dividend and this was the case this time as well with no dividend announced.

Overall then this was a solid performance from the group. Both profits and net assets increased and despite the fall in operating cash flow, this was only caused by a large increase in receivables and cash profits improved too. Having said that, there was a cash outflow at the operating level which despite the fact it is somewhat seasonal, is not idea. Profits in the UK were flat as the move away from lower margin work seems to be affecting productivity but performance was good in Europe, driven by the previous reduction in costs in Germany; and profits increased in ROW markets despite softness in China as the group performed well in Australia, Thailand and India.

The board now expect performance to be ahead of expectations and the forward PE ratio is a paltry 9.7. There is still a lot of debt here, though, and the dividend yield of 0.8% is not exactly enticing (sensible given the debt levels) so I’m not too sure what to do about this one.

It has to be said that his is a pretty good looking chart.

On the 13th October the group announced the acquisition of various business owned by PS, a specialist recruitment group in the US focussing primarily on pharmacy benefit managers with all of its revenues generated from temporary sales. The aggregate consideration is expected to be about $12.1M. The business generated NFI of $1.9M and EBITDA of $600K last year but the forecast for EBITDA this year is $1.3M and the board expect the acquisition to be earnings enhancing in the first full year of ownership.

There is an initial consideration of about $7.3M, deferred consideration payable in 2016 based on 100% of the financial performance of the business less 60% of the budgeted performance which will be paid on acquisition, first earn-out consideration payable in 2017 based on any increase in the financial performance of the business, and the second earn out consideration payable in 2018 also based on an increase in performance. The consideration is based on a minimum of $9.6M and a maximum of $16M.

The group is expecting to raise £3.3M through a placing and to fund the rest of the acquisition costs with a new debt facility of £4.5M. The placing consists of up to 4,456,285 new shares representing just over 9% of the total share capital at a price of 75p per share. Participation will be limited to certain institutional shareholders and the Chairman.

This seems like a decent acquisition with a first foray into the US market, although it does seem quite expensive. The increase in debt levels is also cause for concern given the high levels of borrowings already present at the group. To be honest this acquisition has put me off a bit and I might wait on the side lines for now.

On the 21st January the group released a trading update covering the year. Full year profitability will be ahead of market expectations despite the impact of adverse currency headwinds. The board expect adjusted pre-tax profit growth of about 23% year on year with NFI about 10% ahead of the prior year. Total net debt is expected to reduce by 26% to £7.3M which includes the term loan to help fund the acquisition of Pharmaceutical Strategies in the US.

During the year they have invested in new staff, launched a second brand in the Middle East and developed the new office openings made in 2014. They have also continued to devolve low margin industrial contracts. There were some notable performances in Australia, Thailand and some UK sectors. They are particularly pleased with the performance in Germany and India during the year with the offshore recruitment business in India significantly increasing profits and opening a third centre ahead of original plans with good possibilities for further growth in the year ahead.

In October they acquired Pharmaceutical Strategies, a healthcare agency operating in the US which has been quickly integrated into the group and should be contributing to profits in 2016. Overall the board see exciting growth opportunities and are confident in their ability to deliver profitable growth.

I like this update, things seem to be going quite well here. The shares have been hit quite badly in recent weeks due to the state of the market but I am tempted to buy in here.