Somero has now released its interim results for the year ending 2015.

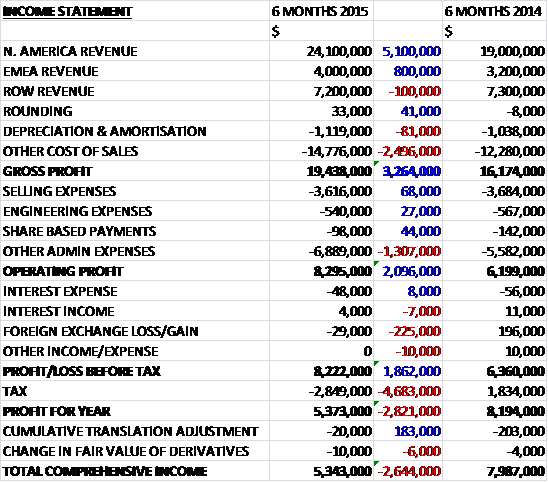

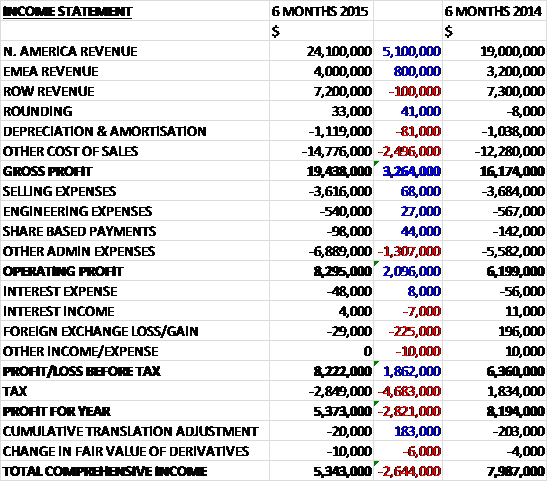

Revenues grew when compared to the first half of 2014 as a $100K fall in ROW revenue was more than offset by a $5.1M increase in North American revenue and an $800K growth in EMEA revenue. Cost of sales also increased to give a gross profit some $3.3M higher. Selling costs were slightly lower than last time but admin costs grew year on year due to increased headcount, higher sales commissions and health insurance expenses, which meant that operating profit was $2.1M ahead year on year. We then see a swing to a foreign exchange loss but the real difference from last year is a $4.7M swing to a tax charge due to last year’s reversal of a non-cash valuation allowance which meant that the profit for the half year was $5.4M, a decline of $2.8M year on year.

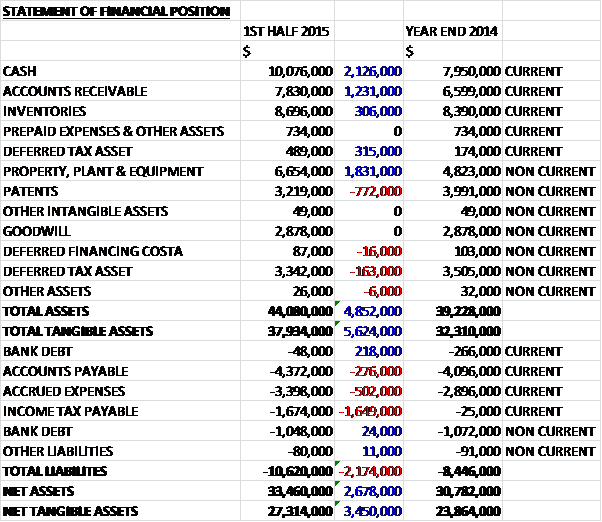

When compared to the end point of last year, total assets increased by $4.9M driven by a $2.1M increase in cash, a $1.8M growth in property, plant and equipment, and a $1.2M increase in accounts receivable, partially offset by a $772K fall in the value of patents. Total liabilities also increased during the year due to a $1.6M increase in income tax payable and a $502K growth in accrued expenses. The end result is a net tangible asset level of $27.3M, an increase of $3.5M over the past six months.

Before movements in working capital, cash profits increased by $789K to $6.5M. We then see an increase in the income tax rebate to give cash from operations of $7.3M, an increase of $1.5M year on year. The group then spent $2.2M on property and equipment, primarily related to investment in the Houghton facility expansion and new Fort Myers HQ, which gave a free cash flow of $5.2M. The bulk of this cash was spent on the dividend plus a few other smaller costs relating to purchases of stock and stock options etc and along with $242K paid back on loans the cash flow for the period was $2.2M to give a cash level of $10.1M at the period-end.

Large line sales increased to $15.4M as a result of an increase in volume from 30 units to 44 units; mid line sales decreased to $2.3M due to a decrease in volume from 18 units to 12 units; small line sales increased to $6.3M due to a slight increase in volume to 76 units; remanufacturing sales increased to $3.7M despite a decrease in units from 26 to 23 units due to higher average prices; and 3D profiler sales increased to $2M due to an increase in units sold from 17 to 21.

US sales momentum carried forward into the current year as a result of the new product introductions such as the S-485, replacement demands on outdated technology, ongoing construction growth and project backlogs the group’s customers are experiencing. This growth trajectory is expected to result in strong sales for the year. A particularly strong performance in the Middle East, with revenues above expectations and increasing by $1.7M to $1.9M, has positioned EMEA for growth compared to the first half of last year which offset a sluggish performance in Russia and India. In addition the board are encouraged by improved activity in Europe with revenues up 36% to $1.9M.

The markets in SE Asia experienced solid growth during the period, increasing revenues by $600K to $1M but China started the year slowly, resulting in trading falling compared to the same period of last year. The group continues to progress in developing brand awareness, providing education and training on the value of high performance flat concrete floors, and finalising third party equipment financing options through the Bank of China. The low penetration rate in the country, combined with greater acceptance of flatness standards and customer willingness to use the group’s products suggests that the group has opportunity for growth going forward. In addition, the board is expecting the planned launch of the Concrete College in Shanghai in Q4 will play a key role in supporting growth in the region.

Growth is also anticipated in Latin America outside Brazil (so not the region as a whole then), driven by increased activity in Mexico attributed to the manufacturing sector. Positive signs of improvement have also been seen in other countries in the region.

In the second half of the year the group expect to launch the S-10A. This machine is designed to benefit contractors with smaller to mid-sized slabs and ranging from the beginner to those ready to move to a higher level boom-out Laser Screed Machine.

Ground has been broken for the 20,000 square foot expansion in Houghton, Michigan with an expected capital cost of $1.3M and targeted completion in Q4 2015. Land has also been purchased and the design completed for the new 14,000 square foot facility in Fort Myers, Florida with an expected capital cost of $4.8M and targeted completion in Q2 2016 – it is notable that the costs for both of these projects have increased having initially been expected to be $1M and $4M respectively.

The board are encouraged by trading early in the second half of the year and are confident that the group will deliver a strong performance in line with market expectations.

After a 27% increase in the interim dividend, the shares are currently yielding 2.9% but for some reason this is expected to fall to 2.8% once the full year dividend is announced. The future PE ratio is 10.9 which seems fairly reasonable. The net cash position at the period-end was $9M compared to $6.6M at the end point of last year.

Overall then this seems to have been another good update from the group. Profits did fall but this was entirely due to last year’s reversal of non-cash valuation tax allowance and operating profits were up. Net assets increased and operating cash flow was also up, with a good amount of free cash generated once again. Operationally, the group is still dependent on the US market and luckily this is going well. Other areas that experienced growth were the Middle East, Europe and Mexico with the BRIC nations the ones where the group is struggling with China being the most important market that is showing cause for concern. It is notable that the capital investment projects seem to be more expensive than initially thought so it will be worth looking for some cost over-runs on these. Despite this though, the shares look cheap with a PE ratio of 10.9, a dividend yield of 2.8% and plenty of net cash.

There does seem to be some recent weakness on the chart but perhaps there is a long-term support nearby.

On the 10th November the group announced that Chairman Lawrence Horsch sold 5,000 shares at a value of £6.6K. He still owns 147,000 shares so this looks to be just a small sale and not really much to worry about.

On the 7th January the group released a trading update covering the full year of 2015. In the second half of the year the group has performed strongly, particularly in Q4, with monthly sales at an all-time high in December. As a result they now expect to report revenue ahead of current market expectations. Furthermore, as a result of an improved gross margin performance, they now expect to report EBITDA materially ahead of current market expectations.

Demand in the second half of the year remained robust across the core product range with North America and Europe contributing significantly to sales growth while performance in China was healthy and remained stable. The particularly strong finish to the year in Europe and full year performance in the Middle East notably exceeded board expectations.

The year-end demand for the company’s products in North America was predominantly driven by technology upgrades and fleet additions, highlighting lengthy project backlogs for customers that extend will into 2016. On a product basis, while large line machine sales continue to represent the majority of volume, small line revenues, including the S-485 introduced at the end of 2014, were key contributors to growth.

The board is confident that it will deliver another year of growth in 2016 and that the high level of activity in December will continue into the year, providing a solid start to trading.

This is a nice looking update with both revenues and margins increasing. This remains a highly cyclical business but trading seems to be going well at the moment and I have taken an initial position here. Note that these shares are counted as being US equities so I had to fill out a form to allow me to trade them.