IQE is the world’s leading manufacturer and supplier of advanced semiconductor wafer products and their finished products are compound semiconductor wafers, also called epiwafers. Their technology is found in smartphones, tablets and various other tech devices and their customers incorporate these wafers into their chips that form the components for a wide range of wireless communications and photonic devices. The group has a 55% market share of the global demand for compound semiconductor wafers in the wireless components sector. The group has also developed advanced materials technology which spans wireless, infrared, photonics, solar, power electronics and CMOS++. The biggest competitor across the compound semiconductor space is a company called VPEC with Landmark, Hitachi and Sumitomo also competing in the space. The products are sold to the chip manufacturers such as Intel and ARM who then supply customers such as Apple and Samsung.

The group has a strategy to mitigate the risk of changing chip manufacturers by establishing strong supply relationships with all major chip companies so that any changes in mobile models do not have a drastic effect in sales.

The group’s core IP is Epitaxy which is a nano-technology that enables the manufacture of epiwafers. Epitaxy is a form of atomic engineering that required high spec cleanrooms and sophisticated production tools. They grow atomically thin films of crystals on a substrate which is a physical and electric template required in order to handle the finished products. It is the combination of layers produced by the group that gives the epiwafer its properties.

The wireless division accounts for just under 80% of total sales and covers electronic devices that communicate wirelessly including mobile phones, mobile networks, WIFI, smart metering, satnav and various other connected devices. The photonics division accounts for about 20% of sales with the market covering applications that either emit or detect light such as emitters and detectors including optical interconnectors, laser projectors, optical storage, cosmetic applications, gesture recognition, and finger navigation; infrared; solar and lighting. The electronics market combines the advanced properties of compound semiconductors with the low cost of silicon with the market separated into power control and advanced materials.

The group is also the clear market leader in advanced gallium antimonide and indium antimonide substrates for use in a range of infrared and heat sensing applications. The sensitivity of current heat sensors enables a monochrome image so that applications such as night vision devices can only see in tones of green and black whereas the new antimonide materials allow greater sensitivity so that different shades and colours can be distinguished, effectively producing full colour night vision images. The group is actively engaged in a number of collaborative programmes with leading industry platers and government agencies in the development and supply of infrared materials based on antimonide materials. The group has now released its final result for the year ended 2014.

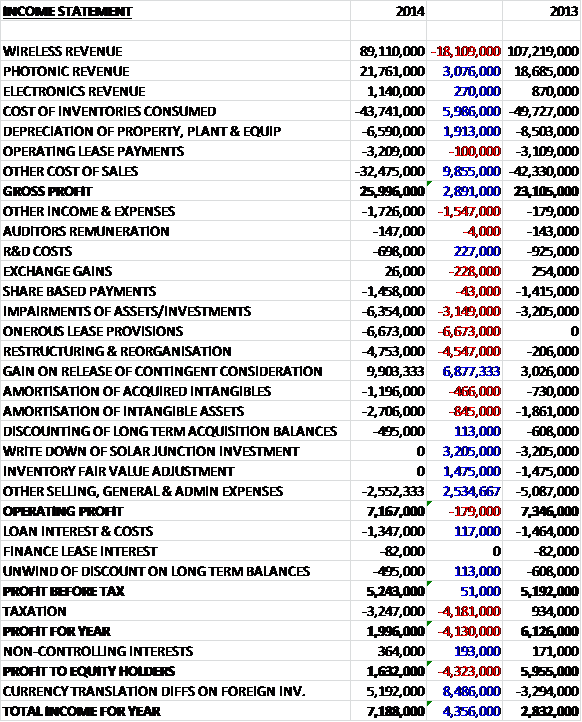

Revenues declined when compared to last year as a £3.1M increase in photonic revenue and a £270K growth in electronics revenue was more than offset by an £18.1M decline in wireless revenue due to the impact of an industry wise inventory correction, foreign exchange and lower underlying growth in demand for wireless wafers. Cost of inventories fell, as did depreciation, but amortisation increased along with operating lease payments. The big fall in other cost of sales, however, meant that gross profit was £2.9M above that of 2013. We then see a £1.5M growth in other expenses and a detrimental movement in exchange gains partially offset by a small fall in R&D costs but there were a number of one-off costs as a £3.1M increase in impairments, a £6.7M onerous lease provision and a £4.5M growth in restructuring expense was offset by a £6.9M increase in the gain on release of the contingent consideration and the lack of the £3.2M write-down of the Solar Junction investment and the £1.5M inventory fair value adjustment. After all that the operating profit fell by just £179K but a smaller loan cost and lower unwinding of the discount on long term balance meant that pre-tax profits increased by £51K. This was entirely dwarfed by the effect of a swing to a tax charge due to a £4.4M deferred tax charge on exceptional items this year, however, and the profit for the year came in at £1.6M, a decline of £4.3M year on year.

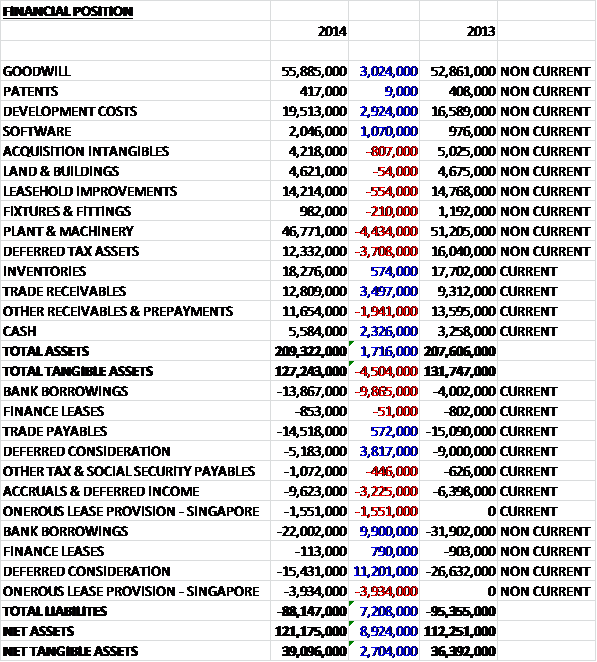

When compared to the end point of last year, total assets increased by £1.7M driven by a £3.5M growth in trade receivables, a £3M increase in goodwill, a £2.9M growth in capitalised development costs, a £2.3M growth in cash and a £1.1M increase in the value of the software partially offset by a £4.4M fall in plant & machinery, a £3.7M decline in deferred tax assets and a £1.9M decrease in other receivables and prepayments. Total liabilities fell during the year as a £15M fall in deferred consideration was partially offset by a £5.5M increase in the onerous lease provision relating to the Singapore facility and a £3.2M fall in accruals and deferred income. The end result is a net tangible asset level of £39.1M, an increase of £2.7M year on year.

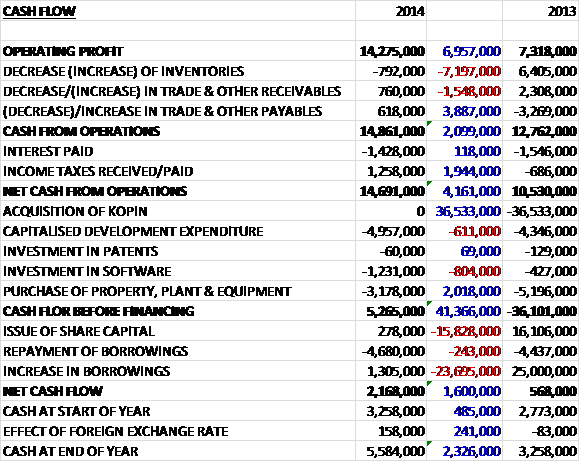

Before movements in working capital, cash profits increased by £7M to £14.3M. There was a slight cash inflow from working capital, but not as much as last year but there was a £1.3M income tax receipt which nearly covered the interest payment to give a net cash from operations of £14.7M, an increase of £4.2M year on year. The group then spent £5M on development expenses, £1.2M on software and £3.2M on fixed tangible assets to give a free cash flow of £5.3M. Most of this was spent on paying back borrowings so that the cash flow for the year was £2.2M to give a cash level of £5.6M at the year-end.

Discounting the impairment, the operating profit at the wireless division was £10.1M, an increase of £200K year on year. The wireless communications market has grown rapidly in recent years reflecting the increasing adoption of wireless technology coupled with the need for an increased compound semiconductor content to support greater sophistication of mobile devices. Whilst handset replacement cycles have slowed, innovations such as wearable devices are expected to reignite the desire to upgrade connected devices such as smartphones. Coupled with the potential growth in “internet of things” the overall wireless market is expected to continue to grow. Smartphone shipments are expected to grow from over 1BN units this year to more than 1.5BN in 2017. Growth in the compound semiconductor content in smartphones will be driven by the need for more radio frequency functionality and greater complexity in wireless circuitry but will be partly mitigated by improved efficiencies and a drive towards reduced component footprints.

The operating profit in the photonics division was £3.3M, a vast improvement on the underlying profit of £800K in 2013 with the increase driven by the increasing adoption of VCSEL technology into a wide range of applications from data centres through to industrial processes. It is thought that this ramp is at an early stage and has a long and sustainable future with demand currently outstripping supply in a number of market segments. Feedback from customers apparently indicates further growth in the sector as the need for sensors, energy generation, heating, lighting and other energy efficient products grows. The group have also announced its participation in a €23M programme to establish a Pan European pilot line for the production of VCSEL components.

The Solar business moved into production in early 2015 with the group’s material now being deployed into the field. Although this was later than initially anticipated, the future of this business apparently remains bright as an end market pull should see it ramp up over the next couple of years. The group have also become a key partner in an EU funded programme to develop 4-junction advanced solar cells for space applications.

Conversely the power business has progressed more rapidly than originally expected. A number of major technical milestones and commercial partnerships are positioning the group in a strong position to commercialise this technology with an agreement with M/A-COM Technology Solutions to deliver 200mm GaN on Silicon. The operating loss at the electronics division was £1.2M compared to a loss of just £59K last year.

Currently wired data transmission in the home, the office and data centres is largely undertaken using copper cables. Data traffic is growing at a fast rate, however, due to technologies such as HD imaging, video streaming, big data and cloud computing. This is necessitating a switch from copper wires to optical communication which is a natural evolution that mirrors the transformation that has already taken place in telecoms infrastructure. Optical interconnectors offer significantly higher speed data transfers over much longer distance compared to their copper counterparts, and are much more efficient. Data centres have become major consumers of electrical energy, rivalling traditional heavy industries. A number of contract wins for both production and development contracts were gained during the year.

Compound semiconductor technology that enables optical interconnects include Vertical Cavity Surface Emitting Lasers (VCSEL). They are an advanced laser technology geared to mass production and low costs and the group is the market leader for these products with world record data speeds in excess of 64GB/s already demonstrated.

The group has developed a powerful range of advanced, engineered wafers such as germanium on insulator, germanium on silicon and silicon on sapphire which offer a high performance and low cost solution for next gen microprocessors, ultra-high speed flash memory and MEMS devices such as motion sensors. They have established a good position in these advanced technologies working with some of the biggest names in the industry, which is reflected in a number of joint patents awarded in conjunction with intel for the production of compound semiconductor materials on silicon substrates.

The group made sound technical progress during the year with the launch of the infrared’s industry’s first 150mm indium antimonide wafers, a major milestone in reducing the overall cost of chips to drive increasing adoption. This was followed up with a number of significant contract wins for the division and there has been significant work in developing these materials for consumer sensing applications which will drive much higher volumes of wagers in the future.

The group is somewhat on a number of large customers with one client accounting for 29% of revenues and anther accounting for 24%.

During the period the group was engaged in restructuring its global operations which has resulted in certain cash costs and provisions for asset impairments and future lease costs. No further restructuring costs are expected in 2015. The cash costs incurred were £4.8M which related to redundancy costs, requalification costs and the duplication of overheads to support the transition of customers between production facilities.

The asset and lease provisions primarily related to the group setting aside the Singapore facility and certain equipment for use by a new joint venture with WIN Semiconductors and Nangyang Technological University called the Compound Semiconductor Development Centre of which the group has a 50% stake. It has been established to accelerate the development of compound semiconductor technology to provide an effective incubator for bringing new innovations to market. The group will be providing facilities, equipment and IP on favourable terms to the joint venture which have caused the asset impairments. In return the group will be the production partner for the high volume manufacturing that emerges. The asset impairments related to equipment (£4.9M), inventories (£1.4M) and the provision of onerous leases (£6.7M).

An acquisition was made in 2012 where the consideration is being settled through agreed contractual price discounts. Subsequent to the measurement period, any adjustments to the recorded fair value of the contingent consideration are taken through the income statement within other income. The revenues of products sold which are subject to this discount are recognised at full market value. On settlement of the transaction, the discount is applied to reduce the deferred consideration balance.

The group also generated a non-cash profit of £9.9M arising from a reduction in the estimated remaining deferred consideration, settled via trade discount, in respect of a previous acquisition. Of the total deferred consideration of £15.4M outstanding, some £10.7M is expected to be settled through the agreed price discounts over the next two years. The investment in Solar Junction was fully provided for last year and in 2013 prior to the disposal of the minority interest to Solar Junction Corporation.

As with anything in this fast moving space there is always the risk that this new technology will be superseded by something else or may not be able to make the impact in new applications that is expected. There has apparently been some commentary about the threat that silicon will replace compound semiconductor technology in mobile communication. The board believes that this sis contrary to both the underlying technology trends and the fundamental properties of these respective materials. Indeed, it is widely expected that the next disruptive technology in the semiconductor industry will be the combination of compound semiconductor and silicon technologies which will enable “System on Chip” integration.

The group is somewhat susceptible to interest rate rises with a 50 basis point increase pushing up the interest costs by about £170K per annum. Most of the group’s sales take place in the US so there is also a susceptibility to exchange rate changes with a 1c movement in the US dollar to Sterling exchange rate impacting earnings by about £200K.

As can be seen, a large onerous lease provision has been recognised during the year. The provision assumes that the lease will be onerous for the next four and a half years. Subsequent to this period, the group expect to be able to sublet the premises or negotiate to exit the lease, the full term of which is seven years with the lease running to 2021.

The current year has started in line with expectations, and the outlook for the full year remains positive. At the current share price the shares trade on a PE ratio of 11.5 which seems rather decent value but there are no dividends paid by this company. At the end of the year the group had a net debt position of £31.3M compared to£34.4M at the end of last year.

Overall then, this is an interesting company with a 55% market share for their products that go into the wireless market. Profits fell during the year but this was due to a large deferred tax charge and pre-tax profits were flat with underlying profits increasing during the year. Net assets increased as the deferred consideration was settled via a trade discount and the balance sheet looks fairly good actually. Operating cash flows also improved with the group actually making some free cash.

Profits at the wireless division, which makes up about 80% of the business, increased modestly as handset replacement cycles slowed. The photonic division was the growth driver as an increasing adoption of VCSEL technology drove profits higher. The electronics division is still fairly loss making, however, with losses widening during the year. The solar product looks like it has the potential to be disruptive, although progress is slower than expected here and the power division is progressing quickly.

There are clearly some risks here. The fact that the group delivers into a small number of chip makers means that there is key client risk despite the diversification and there is always the chance that another technology will come along to disrupt the market. In addition, the group is susceptible to interest rate rises and any weakness in the dollar with the latter admittedly looking unlikely for the time being. There is no dividend yield here but cash does seem to be being generated and at a PE ratio of 11.5, this company does look rather interesting to me despite the large debt pile.