Communisis has now released its interim results for the year ending 2015.

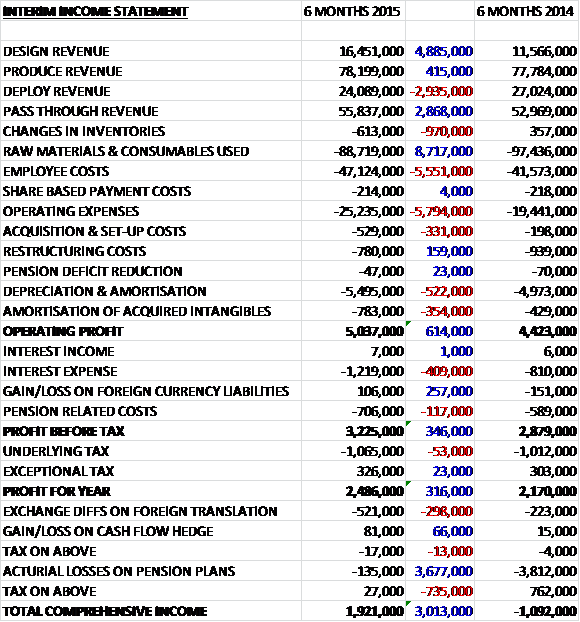

Revenues increased when compared to last year as a £2.9M decline in deploy revenue was more than offset by a £4.9M growth in design revenue reflecting a full six months’ contribution from the agencies acquired last year; a £2.9M growth in pass through revenue and a £415K increase in produce revenue. We then see an £8.7M fall in raw material costs but employee costs were up £5.6M and operating expenses increased by £5.8M, along with an increase in depreciation and amortisation to give an operating profit some £614K ahead of last year. There was a higher interest cost and a slightly higher pension cost which meant that the profit for the half year was £2.5M, an increase of £316K year on year.

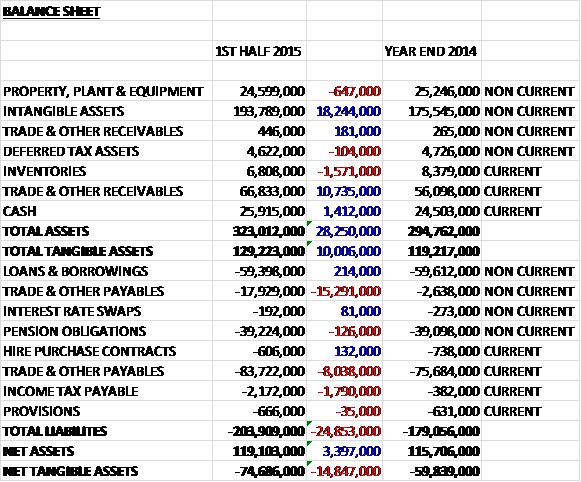

When compare to the end point of last year, total assets increased by £28.3M driven by an £18.2M growth in intangible assets, a £10.7M increase in receivables and a £1.4M growth in cash partially offset by a £1.6M fall in inventories. Total liabilities also increased during the period due to a £23.3M growth in payables and a £1.8M increase in income tax payables. The end result is a net tangible liability level of £74.7M, a detrimental movement of £14.8M over the past six months so the already poor balance sheet is getting worse.

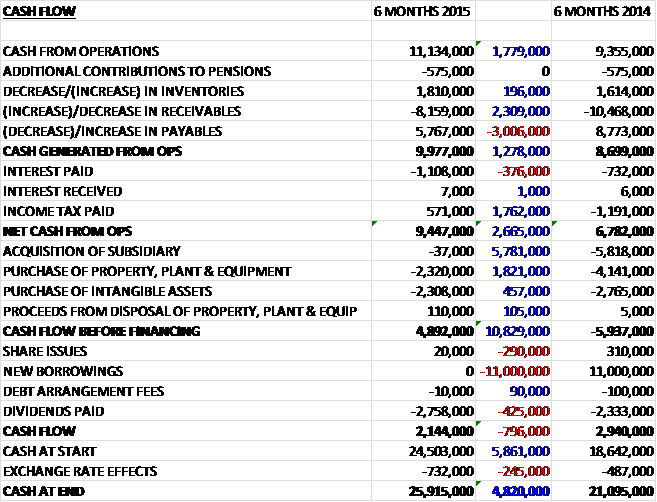

Before movements in working capital, cash profits increased by £1.8M to £11.1M. We then see a bit of a cash outflow from working capital due to an increase in receivables but after a tax receipt as opposed to a cost last time, the net cash from operations was £9.4M, an increase of £2.7M year on year. The group then spent £2.3M on intangible assets and a very similar amount on property, plant and equipment which is apparently a more normal capex level, to give a free cash flow of £4.9M. After the dividends were paid out, the cash flow for the first half of the year was £2.1M to give a cash level of £25.9M at the period-end.

The underlying profit in the design segment was £1.3M, a decline of £52K year on year on revenues that grew due to the contribution from the agencies acquired last year together with a recovery in the data services business following its repositioning in analytics and to appeal to broader market sectors than its historic focus on insurance. The small decline in profit is attributable to some price pressure from larger clients and the effect of a seasonal trading pattern in shopper marketing where profits are weighted to the second half of the year.

The underlying profit in the produce business was £9.6M, a growth of £1.1M when compared to the first half of last year with revenues that also increased due to a number of offsetting factors. Volumes fell faster than expected in chequebooks but more slowly in transactional activities as customers appeared to show some reluctance to migrate from paper to digital formats. These reductions were offset by the benefit of a full six month’s contribution from incoming customer communications services acquired under a contract with Lloyds, and growth in digital distribution, both of which are higher margin services, together with better than expected demand for direct mail which, along with process improvements and cost reductions, drove profits higher. The underling profit in the deploy sector was £5.8M, an increase of just £157K year on year on revenues that were broadly flat due to adverse foreign exchange movements.

During the period the group was awarded a six-year contract with AXA for the provision of incoming and outgoing marketing and operational customer communication services including creative, print, digital and postal distribution and document management services. Under the agreement the group has assumed responsibility for a number of AXA’s existing UK inbound and print centres. The initial transition phase was completed and the contract went live at the end of April. After a competitive tendering process, EE extended its marketing communications contract for two years until March 2017 and a long standing client in the utility sector selected the group for the provision of outgoing transactional communication services for a further five years until October 2020.

Overseas expansion has continued during the period. Three new locations were added in Bucharest, Milan and Warsaw, and activities have been scaled up through the main European hubs with new clients in the drinks, food, pharmaceutical and technology sectors. These market share gains will help to offset a fall in demand from lower margin UK print sourcing clients. The pipeline of opportunities with blue-chip consumer goods groups across Europe is strong, offering good potential for profitable growth.

The group has developed a new digital services platform that provides multi-channel customer messaging services. This allows clients to improve their customers’ experience by delivering communications when, where and how they want to receive them. It was used by Nationwide Building Society to send messages associated with the new ApplePay system.

As usual there were a number of “exceptional” items during the period. Some £780K was incurred in respect of restructuring which included ongoing integration costs relating to the new design agency Psona, and Lloyds activities. There were also £47K of pension deficit reduction costs relating to legal and consultancy expenses. I don’t think any of these are really exceptional – the pension deficit reduction is definitely ongoing and the others just relate to a re-brand and an extension to a contract. A further £500K of exceptional integration charges are expected in the second half of the year.

During the period there was a further acquisition. In January they acquired Life Marketing Consultancy, a research and insight-led shopper marketing agency whose clients are leading consumer goods groups especially in the food, drinks, technology and pharmaceutical sectors. The group acquired the business for an initial consideration of £9.3M satisfied by the issue of a two year, bank guaranteed promissory note of £9.3M, £700K in cash and through the issue of new shares to the value of £4M. As part of the purchase agreement, two contingent consideration mechanisms have been agreed. An amount up to a maximum of £6M will be payable at the end of 2016 subject to the business generating EBITDA of £3M of less due should the business earn between £1.9M and £3M with two thirds payable in cash. An amount up to a maximum of £3.3M will be payable on the achievement of defined synergies over the three years ending 2017, payable in cash with the fair value estimated at £2.5M. The acquisition generated goodwill of £17.2M and contributed a loss of £106K. I have to say that it seems to me the group have overstretched themselves with this one.

With the prospect of ongoing revenue growth, improving profitability and cash generation the board is confident about the group’s prospects for the remainder of the year. At the current share price the shares trade on a forward PE of 9.7 which looks rather cheap on the face of it. After a 9% increase in the interim dividend, the shares currently yield 3.8% increasing to 4% on the full year consensus forecast which is nice to have. At the period-end the net debt stood at £43.4M which seems a bit much to me.

Overall then, this seems to have been a fairly decent update but my previous issues with this company remain. The profit for the period improved, as did the operating cash flow which produced some free cash, although no-where near enough to start paying the debt down to any great degree. The net tangible asset level remained very poor, however, with a large net liability situation which is getting worse. The design business seems to be struggling somewhat due to price pressure from a larger client, the deploy sector is trundling along, not helped by adverse exchange rates and it is left to the produce business to drive growth as the new Lloyds contract and increased demand for direct mail offset the structural decline in chequebooks.

The new AXA contract should start contributing to results soon and I am heartened by the Nationwide contract to send messages related to Apple Pay as this would seem to be the future – I wonder how profitable it was. The Life Marketing acquisition I think is probably a step to far and I would like to see the group take a break from acquisitions and pay back the debt. At a PE ratio of 9.7 and a dividend yield of 4% the shares look good value but the terrible balance sheet and high debt levels mean that this is still too much of a risk for me at present.

This does look like an interesting time for the chart. The recent recovery does seem to put the long term downtrend under threat.

On the 12th November the group released a trading update covering Q3. The group expects to deliver results for 2015 that reflect double digit growth in adjusted operating profit, improved free cash flow and increased adjusted earnings per share when compared to last year, but slightly below expectations due to the performance of the Life business. Life, the new shopper marketing agency acquired in January, is taking longer than expected to contribute its projected earnings, due to some reduction or deferral in spend by existing clients and due to the phasing of some new business opportunities. The pipeline for the business for 2016 is building, however, and some synergies are being realised.

The produce division has continued to take advantage of its market leading position, particularly in the provision of outbound transactional services where the group has signed three important contract renewals during the period and strong new business momentum has been seen in the deploy division where, in recent months, three brand deployment contract wins have been secured with large clients across Europe in the fast moving consumer goods and electronics sectors. Additionally the group’s relationship with Boots has been renewed.

Overall then, this is a bit of a disappointing update and I have decided to reduce the number of companies I am looking at so I’m afraid due to the slow progress and the negative net tangible asset level, this one if for the chop. I will continue to keep it on watch but I will not post any further updates unless something changes.