IQE has now released its interim results for the year ending 2015.

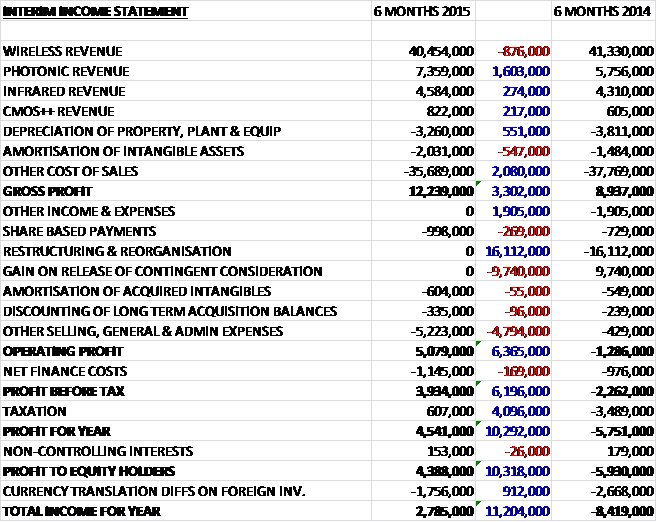

Revenues increased when compared to the first half of last year as an £876K reduction in wireless revenue was more than offset by a £1.6M growth in photonic revenue, a £274K increase in infrared revenue and a £217K growth in CMOS++ revenue. The fall in depreciation was offset by an increase in amortisation but cost of sales declined so that gross profit was some £3.3M ahead of last time. Underlying sales, general and admin costs increased by £4.8M but one-off costs were much lower due to the lack of any restructuring expenses or “other” expenses. After a small increase in finance costs, pre-tax profits increased by £6.2M before a big swing to a tax income due to the tax impact last year of the exceptional release of deferred consideration, meant that the profit for the half year came in at £4.4M, an improvement of £10.3M year on year.

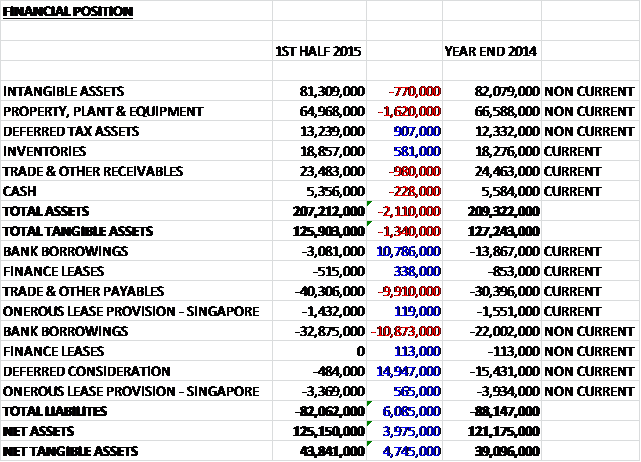

When compared to the end point of last year, total assets fell by £2.1M driven by a £1.6M decline in property, plant and equipment; a £980K fall in receivables and a £770K decline in intangible assets, partially offset by a £907K increase in deferred tax assets and a £581K growth in inventories. Total liabilities also declined during the period as a £14.9M fall in deferred consideration and a £684K decrease in onerous lease provisions was partially offset by a £9.9M increase in payables. The end result was a net tangible asset level of £43.8M, an increase of £4.7M over the past six months.

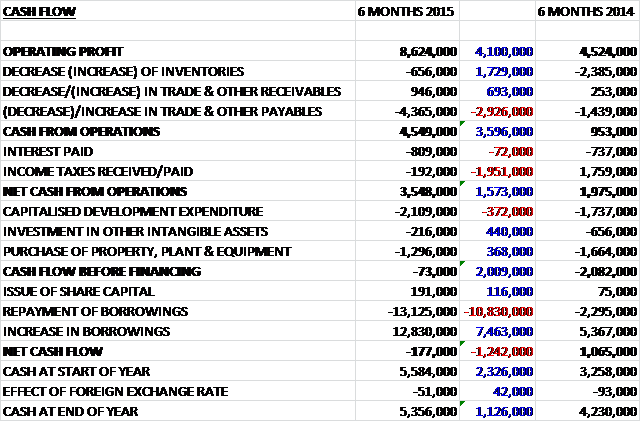

Before movements in working capital, cash profits increased by £4.1M to £8.6M. A large fall in payables, however, along with a swing to a tax expense, meant that net cash from operations was £3.5M, an increase of £1.6M year on year. The group then spent £2.1M on development expenditure, £1.3M on tangible fixed assets and £216K on other intangible assets so that there was no free cash flow, with an outflow of £73K before financing. After a slight net repayment of borrowings, the cash outflow for the period came in at £177K to give a cash level of £5.4M at the period-end.

The adjusted operating profit in the wireless division was £5M, a decline of £541K year on year as some of the sales expected in Q2 fell into Q3 due to temporary production disruption at one customer site – the wireless business as a whole was otherwise stable. The customer forecasts apparently continue to reflect a normal second half weighting of demand and the board remains confident in achieving its full year expectations.

The adjusted operating profit in the photonics division was £1.6M, an increase of £1M when compared to the first half of last year following strong engagement by the group in its customers’ product development programmes over the past few years. The increasing number and quality of customer product development programmes is a positive lead indicator which is providing a high level of confidence over the group outlook for the segment. The business unit is being propelled by the group’s leadership in advance lasers (VCSELs) and has already begun the transition from development and pilot revenues into high volume manufacturing following a number of key contract wins over the past year. The groundwork has been set for significant progress in the business unit for the remainder of this year and into 2016.

Advanced Solar achieved a major milestone with initial sales into field deployments. This is a highly disruptive renewable energy technology. Advances in cell and system efficiency are accelerating the adoption of CPV for utility scale energy generation which is expected to become a $200M market for compound semiconductor materials in the next two to five years. The group are fully prepared for high volume manufacturing and are poised for the ramp as their products complete full end customer qualification and a robust supply chain becomes established. The technical progress made with GaN technologies, is advancing the group towards initial sales into the RF and power markets in the next 12 to 18 months and the group are also at an advanced stage of development with their LED lighting technology with initial product launches expected shortly.

The adjusted operating profit in the infrared division was £655K, a growth of £27K when compared to the first half of 2014 and the group has an estimated 80% market share of indium antimonide and gallium antimonide materials used in high resolution infrared systems. Production is currently concentrated on defence related applications but it is expected to rapidly transition into industrial and commercial use for thermal imaging, safety, security and energy monitoring applications. The adjusted operating loss in the CMOS++ division was £655K, an increase of £215K year on year.

It is worth noting that the group has about £145M of accumulated tax losses which represents a potential reduction in future tax payable of up to £39M.

After the period end, in July, the group entered into a joint venture with Cardiff University to create the Compound Semiconductor Centre, whose aim is to lead the development and commercialisation of compound semiconductor technologies in Europe. The CSC is jointly owned and controlled by IQE and the university with the group contributing equipment with a market value of £12M which was matched by a £12M cash contribution from the university. The group will also license certain IP to the CSC. The creation of the joint venture will create a non-cash exceptional gain of £4.7M due to the difference between the book value and market value of the equipment contributed by IQE and they will also receive revenue of £2M relating to the IP license.

In September the group entered into an exclusive license and option agreement to acquire Translucent’s unique cREO technology. Under the agreement IQE will pay Silex Systems $1.5M within six months in consideration of the license and agreement, which will include the transfer of a range of manufacturing and characterisation equipment from Translucent to IQE and also required the exclusive services of two engineers for a year. The agreement also includes an exclusive option for IQE to acquire cREO technology and IP portfolio for $5M within six months of the exercise of the option, plus a long term royalty agreement of 3% of epi products sold using the cREO technology transferred, or 6% of cREO templates sold using the cREO technology transferred.

At the end of the first half of the year, net debt stood at £31.1M compared to £35.5M at the same point of last year and £31.3M at the end of 2014. There is no dividend at this company but the forward PE stands at a tantalising 9.7.

Overall then, this has been a pretty good six months for the group. The profit is up, net assets increased and the operating cash flow grew year on year. The group did not make any free cash during the half but this does seem to be somewhat seasonal. The profits in the wireless division did decline, however, which is being put down to an issue at a customer site that meant orders for Q2 were pushed into Q3 so hopefully this will be temporary. The increase in the photonics division has made up for the shortfall with some strong growth and the solar products seem to be making progress. The PE of 9.7 looks too cheap to me despite the high debt levels and I am sorely tempted by this share.

The chart looks pretty good to me too.

On the 16th December the group released a trading update. They are on track to achieve year on year growth with H2 revenues expected to be up sequentially over H1. The weakness in the mobile and smartphone markets has impacted wireless wafer sales in Q4 but this has been offset by higher non-wireless revenues, including from photonics and technology licensing. This has given the board confidence that the financial performance for the full year will remains in line with their expectations, which should result in net debt of about £25M by the year-end.

Key wireless customers’ market updates have reflected a mixed performance in H2 2015 and a number of recent company announcements have highlighted broad weakness in the mobile and smartphone segments. Nevertheless, the outlook for 2016 remains positive due to increasing global connectivity and the continuing growth in data traffic. The photonics business has continued to perform strongly, delivering significant double digit revenue growth which is being driven by a wide range of end market drivers, including data centres, optical communications and sensing applications.

InfraRed and CMOS++ have also performed well, in line with expectations and first pilot production revenues were generated from Solar. During the year the group entered into two joint venture arrangements, in Singapore and the UK. These ventures have started positively and the group has licensed additional IP during H2 to enable the acceleration of the joint venture business plans.

This seems to be a pretty decent update, although there is no talk of profits and the wireless end market weakness is cause for concern.

On the 11th January the group announced that it had renegotiated its long-term supply contract with its premier tier 1 customer for the supply of wafer products used in wireless applications. The board estimates that the contract will contribute more than $55M of revenue during 2016. The new supply contract guarantees the group at least 75% of the customer’s demand for epiwafers that are produced using its metal organic chemical vapour deposition platform. It will also see an expansion in terms of additional products from its molecular beam epitaxy platforms.

The contract covers epiwafer products for RF applications including power amplifiers, low noise amplifiers and switches used in smartphones, tablets, PCs, routers, satcoms and some other devices connected to the internet of things.

This is clearly a relief to get this contract extended as it is very important to the group but it is unclear if the margins will be similar to last time and whether the $55M contribution to revenue is better than last time or not. I still find this company interesting but feel the debt levels are still to high for me at the moment.

On the 26th January the group announced that it received a new purchase order agreement for indium phosphide materials to the value of $3.7M from a leading global substrate manufacturer who is an existing long term customer. High Purity InP is the source material for the manufacture of InP wafers used in the production of high-performance photonic components for a range of application in infrared sensing and telecoms with a particular trend towards high definition imaging applications enabled by InP materials.

On the 15th March the group announced that it had issued 5,141,467 shares to Translucent. They have been issued as consideration to satisfy the $1.4M license fee payable for the exclusive license of their Rare Earth Oxide semiconductor technology. The technology apparently offers a unique approach to the manufacture of a wide range of Compound Semiconductor on Silicon products, including gallium nitride on silicon for the power switching and RF technologies markets. All well and good but I am not sure why they are paying them in shares – was this the initial agreement or are they getting short of cash?