Cambria Autos has now released its final results for the year ended 2015.

Revenues increased when compared to last year with a £43.2M growth in new car revenue, a £27M increase in used car revenue and a £4.8M growth in after sales revenue. With an increase in cost of sales, the gross profit was some £6.8M higher than last time. Staff costs grew by £3.6M but other operating costs only increased by £313K so that the operating profit was £2.6M higher than in 2014. Consignment and vehicle stocking interest was up and taxation was higher which gave a profit for the year of £6M, a growth of £1.9M year on year.

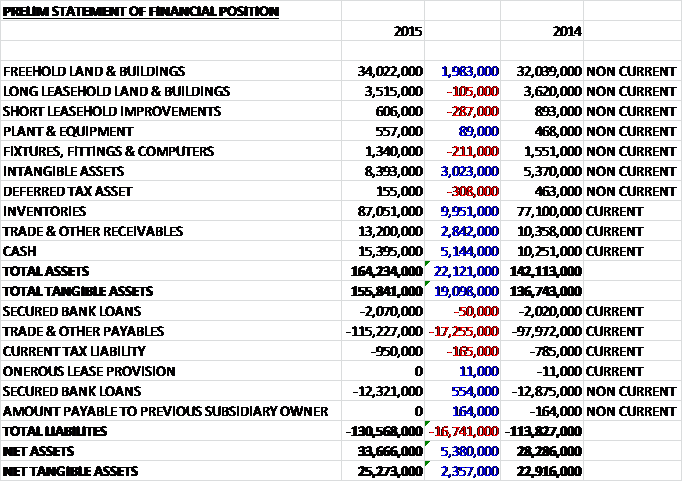

When compared to the end point of last year, total assets increased by £22.1M driven by a £10M growth in inventories, a £5.1M increase in cash, a £3M growth in intangible assets, a £2M increase in freehold land and buildings, and a £2.8M growth in receivables. Total liabilities also increased due to a £17.3M growth in payables. The end result was a net tangible asset level of £25.3M, an increase of £2.4M year on year.

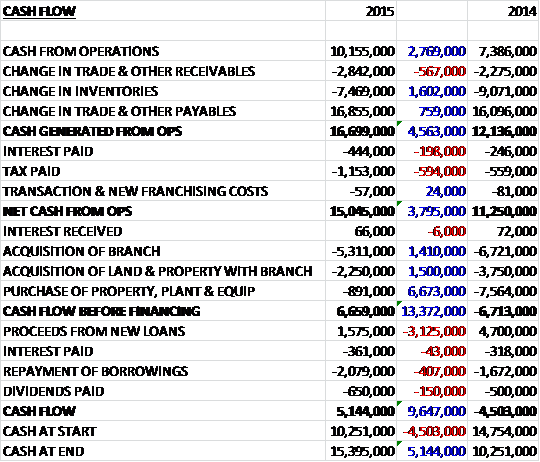

Before movements in working capital, cash profits increased by £2.8M to £10.2M. Due to a large fall in payables, however, which was more than offset by tax and interest, the net cash from operations came in at £15M, a growth of £3.8M year on year. The group then spent £5.3M on new branch acquisitions, £2.3M on land and buildings that came with the acquisitions relating to the Swindon Land Rover acquisition, and £891K on property, plant and equipment to give a cash flow before financing of £6.7M. The group paid back a net £500K of loans and spent £650K on dividends so that the cash flow for the year was £5.1M to give a cash level of £15.4M at the year-end (although obviously this is a bit of a false favourable position given the working capital flows throughout the year).

The gross profit in the new car division was £15.5M, a growth of £3.2M year on year with a 9% increase in new units sold. Excluding the impact of the Barnet and Swindon acquisitions, new sales volumes rose by 1.1% and gross profit was up just £300K. This was delivered in a market that grew 7% but the private registrations element of the market increased by just 4.4%. The industry data indicates that dealer sales are lower than the SMMT registration data which also includes the impact of self-registrations. The group’s sales to private individuals was 9.2% higher and average profit per unit sold was up 12.6% to £1,476. Commercial and fleet vehicles sales by the group increased by 11.6% to 1,090 units and by 0.8% to 605 units respectively and these sales are transacted at lower margins hence the dilutive effect on overall margin.

The gross profit in the used car business was £20.8M, an increase of £1.8M when compared to last year with the sale of 14,945 units representing a 4.4% growth. Like for like volumes were up 1.3% and gross profit increased by £900K on an organic basis. The group is applying consistent controls to the level of used car stock being held, the pricing and presentation of the inventory and the penetration of finance and insurance products to the sale of used cars. The adoption of this trading style has resulted in the average gross profit on each unit retailed increasing by 5.3% to £1,395 per unit. It has also resulted in the concentration on tight management of inventories and an above industry average return on investment.

The gross profit in the aftersales segment was £25.8M, a growth of £1.9M year on year with service and bodyshop hours increasing by 7.8%. The zero to three year car parc continues to be replenished as new car sales increase year on year and this gives the group confidence of further progress in customer retention and the aftersales business remaining strong.

During the year the group purchased a Land Rover dealership in Wootton Bassett from T.H. White for a total cash consideration of £7.6M which included goodwill of £3M. In the year before the acquisition, it is estimated that the branch made a pre-tax profit of £700K with £207K generated for the group during the period since the start of May when it was acquired. The acquisition represents the group’s second Land Rover dealership and is integrating well, performing in line with expectations so far. During the year this business together with the Barnet Land Rover dealership acquired last year, contributed £1.2M to pre-tax profits.

It is the intention to fully re-develop the Swindon Motor Pak location to provide a new JLR facility in line with the new Arch design concept for JLR facilities. It is anticipated that the development will be completed by summer 2017 and the planning process will start imminently. Once the new development is complete, they will relocate the Land Rover business from the existing property in Wootton Bassett and they will then dispose of the Wootton Basset facility. When the Barnet JLR dealership was acquired in 2014 the group committed to develop the freehold site to provide the Arch concept at that location too. Full planning consent has now been obtained and they are in the process of finalising negotiations with contractors for delivery of the site. It is expected that development will start next year with completion in Q1 2017 calendar year.

The group has refinanced its banking facilities with Lloyds. The existing £14.4M of term loans were refinanced into one £15M that has a five year term and a 15 year capital repayment profile. The cost of the facilities is LIBOR plus a margin which is set each quarter and is dependent on the net debt:EBITDA ratio for the group. It can range from 1.2% where the net debt is less than one times EBITDA, and 2% where the net debt is greater than 2.5 times EBITDA. The group has also arranged two further revolving credit facilities. The first is a five year £15M facility available for the acquisition of businesses and property, the second is a five year property development facility to be used against the Barnet and Swindon properties. The maximum drawdown against this facility is £7M, and it is intended that once the developments are complete, the facility will be converted to a standard amortising term facility.

Since the industry lows experienced in Q4 2011, the UK market has enjoyed 43 consecutive months of year on year growth in new car registrations to September 2015. The situation plateaued in October but the market is expected to reach a record high in 2015 at over 2.6M new car registrations. The group believe that the new car market will remain robust but they do not expect year on year growth in new car registrations to continue when the market reaches its natural mid-cycle level, which is thought to be around now. The UK remains an attractive place for the vehicle manufactures to register and sell cars given the overall recovery of the economy and the exchange rate benefit that the manufacturers receive as sterling remains strong.

As a result of these exchange rate benefits and the ongoing low interest rate environment, vehicle manufacturers continue to deliver strong consumer offers, which represent attractive propositions for the group’s customers to acquire new cars. The level of cars sold on Personal Contract Purchase related products has increased significantly over the past four years. As a result of the increased presentation of the PCP offers, there is a natural change cycle where a customer is more likely to change a car for another new one during the term of the PCP product. A larger portion of cars sold on PCP gives greater control of the customer’s change cycle and creates an opportunity for the company to engage with them.

After the year-end, the growth momentum has continued in the first two months of the year with results substantially ahead of the comparable period this year and tracking ahead of current market expectations, and the board believe they are well placed to continue their growth in the year as a whole. The group are continuing to look for new acquisition targets.

At the current share price the shares trade on a PE ratio of 11.9 which fall to 10.1 on next year’s consensus forecast. After a 25% increase in the total dividend, the shares are now yielding 1% which increases to 1.3% on next year’s forecast. The net cash level currently stands at £1M compared to a net debt position of £4.6M at the end point of last year, although there is a considerable amount of leaseholds outstanding.

Overall then this has been a good year for the group. Profits increased, net assets grew and operating cash flow was up with a decent amount of free cash being generated. The organic new car sales growth seems to be rather lacklustre, though, but this is apparently explained by the official figures including self-registrations. Both used car sales and after sales profits showed good growth too as the strong new car sales of recent years filter through to these markets. As long as Sterling remains strong (one of the few businesses where Sterling strength is a bonus) the UK is likely to be continued to be targeted by car manufacturers but the board now see the market as being mid-cycle so the continued year on year increases are likely to plateau.

It is worth noting that the group will be sinking quite a lot of cash into the JLR refurbishments so I would like to see a prudent acquisition strategy given this and the fact that when the market does turn then car dealerships tend to get hit hard and if CAMB were carrying a lot of debt at that point, they would be in trouble. The dividend yield of 1.3% is nothing to write home about but the forward PE ratio of 10.1 seems to factor in the cyclical nature of the company and the shares still look fairly good value to me – I will continue to hold.

On the 11th January the group announced an acquisition and a disposal. They acquired the Land Rover Franchise in Welwyn Garden City from Jardine Motors for a cash consideration of £10.8M which brings the number of Land Rover franchise under the Grange trading name to three. This acquisition generated £10M of goodwill and is being funded from the newly refinanced banking facilities. It is estimated that the dealership generated a pre-tax profit of £2.5M last year and it is anticipated that it will be earnings enhancing from H2 of this year.

The group disposed of its Grange Jaguar franchise in Exeter to Helston Garages for £1.3M which generated £1.2M in goodwill. The group is also closing its Aston Martin boutique located in the same premises which is apparently in line with the Aston Martin franchise network restructuring strategy and Cambria expect to add another Aston Martin franchise to the portfolio in the short to medium term. The disposed businesses made a profit contribution of £500K to the group last year.

The disposal is in line with the compliance guidelines from JLR which states that both Jaguar and Land Rover brands should be represented by the same dealer in a given franchise territory. The acquisition here certainly looks decent but in my view the disposal seems to have been sold off a bit cheaply. Nonetheless, these transactions seem to have been a net gain for the group.

On the 14th January the group released a trading update. They maintained the momentum achieved over the last year and the trading performance in the first four months of this year has been substantially ahead of 2015 in a backdrop of a record new car market where the market has seen year on year growth in registrations in all but one of the last 46 months, although the rate of growth is slowing. Trading during the period has also been substantially ahead on a like for like basis.

New vehicle unit sales were up 4% but down 1.2% on a like for like basis with gross profit per unit improving. Used vehicle sales performed better with total unit sales up 4.7% and like for like up 2.9% with gross profit per unit improving here too which has significantly enhanced the profit derived from the used car segment of the business. Growth in aftersales has also continued with profitability up 3.1% but flat on a like for like basis.

The Swindon Land Rover business acquired in April has continued to perform in line with expectations. Overall, the board expect the results for the first half of the year to be significantly ahead of last year and in line with recently upgraded (following the acquisition) market expectations. This is all pretty good stuff.

On the 7th March the group released a trading update covering the first five months of the year. They stated that trading was substantially ahead of the same period last year on both a total and like for like basis.

New vehicle unit sales were up 3.8% but down 1.2% on a like for like basis with gross profit per unit improving. Used vehicle sales performed better with unit sales up 4.3% with a 2.3% increase on a like for like basis with gross profit per unit also increasing which enhances the profit derived from the used car segment of the business. Growth in aftersales operations also continued, with profitability up 4.1% with like for like profits flat.

The Swindon Land Rover business that was acquired in April has continued to perform in line with expectations and the new Welwyn Garden City Land Rover dealership, acquired in January, is integrating to plan and will be earnings enhancing in the second half of the year. After the first week of the important March trading period, the new car order book is building well and the board expects the group to deliver another strong trading performance in the month as a whole.

Overall, this seems like an OK update and the group is still growing with increases in gross profit per unit but the increase in sales seems to be coming entirely from acquisitions with like for like sales broadly flat.