Telecom Plus has now released its interim results for the year ending 2016.

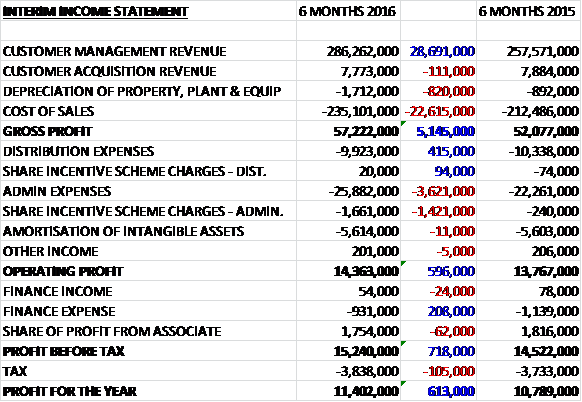

Revenues increased by £28.8M when compared to the first half of last year and after an increase in depreciation and cost of sales, the gross profit grew by £5.1M. Distribution expenses actually fell as a result of a reduction in promotional spend but share based payments grew by £1.5M and other admin expenses were up £3.6M, due to growth in the number of services being provided and higher occupancy costs following the move to the larger HQ, so that operating profit was up £596K. After a decrease in finance expenses, a fall in the profit from the associate and a modestly higher tax cost, the profit for the six month period came in at £11.4M, an increase of £613K year on year.

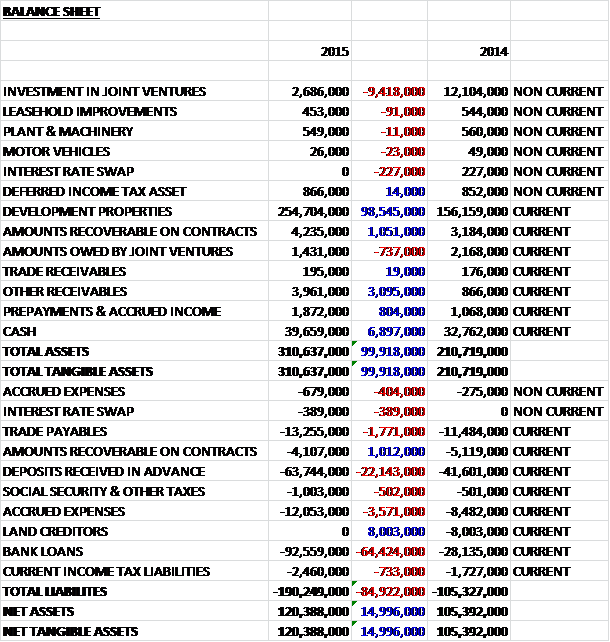

When compared to the end point of last year, total assets fell by £45.4M driven by a £40.1M decline in prepayments and deferred income, an £8.9M decrease in property, plant & equipment, a £5.6M fall in other intangible assets, a £3.9M decline in receivables, and a £3.7M decrease in the value of the investment in the associate, partially offset by a £9.4M growth in the investment property (transferred from PP&E) and a £7M increase in cash. Total liabilities also declined during the period due to a £39.4M fall in accrued expenses and deferred income and a £2.9M decrease in payables. The end result is a net tangible asset level of -£15.7M, a positive movement of £1.3M during the period.

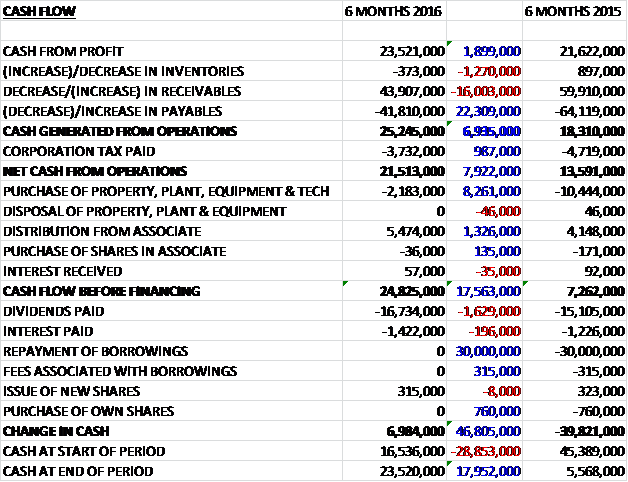

Before movements in working capital, cash profits increased by £1.9M. A large fall in receivables was not quite entirely offset by a large growth in payables and after a lower tax payment, the net cash from operations was £21.5M, an increase of £7.9M year on year. The group did not spend much on capital expenditure, just £2.2M and after the £5.5M distribution from the associate and the interest was paid, the free cash flow was £23.4M, of which £16.7M was spent on dividends to give a cash level of £23.5M at the period-end.

Customer Management profit fell by £85K year on year whilst the losses in Customer Acquisition fell by £681K. Opus continued to make progress in building market share with the number of electricity and gas sites they supply growing to 206,679 and 39,372 respectively which represents a combined increase of 19.7% on the previous year but in spite of this growth, profits are expected to be slightly below last year due to the announcement in the July budget of the removal of the exemption from Climate Change Levy of business customers supplied with European renewable power.

The increase in revenue reflects the growth the group have seen in the size of the customer base over the past year, and seasonally normal weather during the first half of the year compared with an unusually warm spring and summer last year, partially offset by the modest industry-wide reductions to domestic gas prices which took place earlier in the year. The number of customers and services increased by 13,585 and 53,488 respectively which represents quite a slow down when compared to the first half of last year but over half of them applied for at least four services.

There is continuing highly competitive market conditions with both smaller independent energy suppliers and various members of the “big six” continuing to offer heavily discounted short-term fixed price tariffs to attract new customers through price comparison sites and via collective switching initiatives. In the broadband markets, all the major telecoms companies continue to offer free and discounted broadband services for extended periods in order to attract new customers, together with other incentives such as shopping vouchers. These are largely funded by charging more to their existing customers. Telecom Plus no longer offers promotional incentives to new members which, although causes a slow-down in customer acquisition, means that there is lower churn and longer average customer lifetimes and both delinquency levels and bad debt continued to fall.

Around 600-800 new sales partners join a month but these were outweighed by the number of inactive partners who allowed their positions to lapse which resulted in a small reduction in the overall number of registered partners.

The group are looking into expanding into insurance. The current intention is that any such insurance products would form part of the single monthly bill that is already being sent to each customer, and that the group would be acting a broker rather than Principal in relation to these services. Other major areas into which they have considered extending into include TV and water. In relation to the TV market, they have so far been unable to identify a way of entering this space that will earn a satisfactory return for shareholders. In relation to the water supply market, in 2017 there are moves underway to require regional monopoly providers to hive-off their supply business into separate companies. The group will be investigating the feasibility of including the supply of water as an additional core service.

Although wholesale energy prices have fallen considerably over the last two years, little of this reduction has yet been reflected in the standard variable tariffs paid by the vast majority of consumers (and which the group’s purchase price is based on). This is because other suppliers are choosing to re-invest the benefit of these lower commodity costs in creating increasingly attractive short term deals in order to attract new customers.

The CMA enquiry into the energy market published their provisional findings in July, which generated a higher level of responses from interested parties than anticipated. This has delayed the expected publication of their provisional decision on remedies until early 2016, with their final report not now expected until April of that year. They have announced they are considering a number of solutions, including relaxing the current rules that restrict each supplier to just four tariffs, the introduction of a new safeguard tariff, and possible changes to how customers are treated when they reach the end of a fixed term tariff.

In October the group launched “Project Daffodil” where they supply and fit LED light bulbs throughout customer homes free of charge which is expected to reduce their consumption by over 10%. This service will be available to customers who switch all their services to the group. The initial feedback has been encouraging with a significant improvement in the quality of new members joining the business over the past six weeks and has resulted in the proportion of new customers taking all five services increasing from 30% to 45%. It is anticipated that as the sales team become more adept at identifying potential new customers able to take advantage of this benefit, and the number of households who have their free LED light bulbs installed increases, the annualised growth will start to return towards the rates they have historically achieved.

Obviously this initiative will lead to higher customer acquisition costs, these will be partially offset by the higher quality and quantity of new customers signing up. The board remain confident that profit for the current year will be ahead of last year in line with previous guidance.

Clearly one major potential risk to the company is legislative and regulatory risk. Proposed changes such as the new requirements in relation to smart energy meters, social tariffs and changes to the current decommissioning regime could all have a potentially significant impact on the sector, although any additional costs associated with smart metering are not expected to affect the net margins earned by energy companies in the longer term as they are likely to be reflected in higher retail charges. Another topical issue is that of data security risk. A significant breach of cyber security could result in the group facing regulatory fines, loss of commercially sensitive information and damage to its brand. The group continually reviews its approach to cyber security and adopts a multi-layered approach to defence including, high specification firewalls, anti-viral management systems, vulnerability scanning, and third party penetration testing on the group’s IT infrastructure.

During the period the company moved into newly refurbished head offices at Merit House and the former head office building, Southon House, was vacated. Southon House is therefore now held as an investment property and after an independent valuation of the building the value was determined to be £10.2M.

After a 15.8% increase in the interim dividend, at the current share price the shares are yielding 4% which increases to 4.3% on the full year forecast. The net debt fell by £6.8M to £67.2M.

Overall then this was a fairly solid set of results. Profits were up and the net tangible asset position improved despite remaining negative. Operating cash flow also grew and plenty of free cash was generated, although it should be remembered that there is a £21.5M deferred consideration to pay next year. The profits at Opus declined somewhat, however, due to the removal of climate change exemption for businesses supplied with renewable energy. Profits in the core business grew slightly as more favourable weather was experienced but the number of new customers slowed due to the fact that TEP don’t offer discounted introductory deals unlike most of the other energy companies.

The addition of insurance and water could be growth drivers but it doesn’t look as though they will be added in the near future. The CMA enquiry could also be another source of growth for the group depending on its findings, although this now not due until April 2016 and project daffodil sounds really interesting – costs will rise in the short term but this could be a real boost to the number of customers taking all the services offered by the group. Overall profits are still expected to be in line with forecasts and with a 4.3% dividend yield these shares are looking rather interesting to me.

On the 19th April the group released a trading update covering 2016. Notwithstanding the challenges posed by continued falling energy prices, the board are confident of reporting adjusted pre-tax profits of at least £54M, in line with previous guidance. Cash flow remains strong, in line with management expectations and they have taken the opportunity to refinance on more favourable terms.

There has been organic growth of 4.2% in service numbers over the past year taking the number of services supplied to 2,181,704. Whilst this growth was below the level originally anticipated, it has been achieved against a background of a rising gap between standard variable energy tariffs and the cheapest fixed term introductory deals available over the year. This was caused by a number of factors including further deflation in wholesale commodity prices, rising policy costs (including smart meters) and increasingly aggressive collective switching initiatives. Over the last few weeks this gap has narrowed slightly, following recent industry-wide price reductions to standard variable tariffs.

Profit Daffodil, the new benefit announced of supplying and fitting low-energy LED light bulbs free of charge for Double Gold members, is gathering momentum with over 300,000 bulbs already installed. The proportion of new members who have switched all their services to the group is now running at over 50% and if this trend continues, the board expect it to deliver a modest increase in their service growth rate over the course of the coming year.

In line with previous guidance the company intends to pay a total dividend of 46p, an increase of 15% year on year and representing a yield of 5.3%.

Following the CMA’s investigation into the energy industry, they have drawn up draft proposals to remove the current restrictions on discounts, bundling and the number of tariffs each supplier can offer. This will significantly increase the group’s flexibility to offer an attractive choice of packages as they expand their existing range of services in the future. The board were disappointed that they did not propose more radical initiatives to address the widespread practice of offering new customers attractive introductory deals at the expense of the rest of the customer base, however.

The group have a clear strategy to deliver continued high quality growth, albeit at modest levels for as long as the current headwinds continue. Over the course of the new year, the board anticipate that all the key operational and financial metrics for the business will continue to show further progress.