Origin Enterprises is a company domiciled and incorporated in Ireland, listed on the AIM and the ESM markets and has now released its final results for the year ended 2015.

The group is an agri-services business with operations in the UK, Ireland, Poland, Ukraine and Romania. This comprises integrated on-farm agronomy services and business to business agri-inputs such as fertilizer, feed ingredients and amenity inputs. These businesses provide solutions that address the efficiency, quality and output requirements of primary food producers. Services include agronomy, crop and variety selection, cultivation systems, nutrition management, soil health and field inspections, logistics, handling, prescription fruit formulation and environmental stewardship.

As far as business to business agri-inputs is concerned, the group provides blended fertilizer in Ireland and the UK and animal feed ingredients in Ireland. In addition, the group is the UK’s leading advisory and inputs provider to the professional sports turf, landscaping and amenity sectors.

The Integrated Agronomy Services business provides specialist agronomy services directly to arable, fruit and vegetable growers in the UK, Poland, Romania and Ukraine. The service encompasses varietal selection, nutrition, crop protection and application techniques necessary to ensure high performing marketable crops.

The group has a number of businesses in Eastern Europe. In the Ukraine, they own the recently acquired Agroscope which is a provider of agronomy services, high spec inputs and advisory support to arable and root crop growers. In Poland they own Dalgety, a farm advisory, crops protection, fertilizer and seed, and crop marketing services provider and have agreed to acquire Kazgod, a provider of agronomy services, inputs, crop market solutions and a manufacturer of micro nutrition applications. In Romania, the group have agreed to acquire Comfert and Redoxim. Comfert is a provider of agronomy services, integrated inputs and crop marketing support to arable and vegetable growers whilst Redoxim is a provider of agronomy services, macro and micro inputs to arable, vegetable and horticulture growers.

Revenues increased when compared to last year due to a €30.2M growth in UK revenue, a €3.2M increase in Irish revenue and a €9.5M growth in ROW revenue, although on a like for like basis revenue fell by €34.6M reflecting a combination of lower crop protection and crop marketing volumes along with lower crop marketing, feed and fertilizer prices. The cost of raw materials grew by €32.3M and other cost of sales were up €3.2M to give a gross profit some €7.3M ahead of last time. Operating leases grew by €1.6M and other distribution expenses were up nearly €10M with depreciation increasing by €920K, forex losses of €1.4M compared to a neutral position last year, and director emoluments up €3.4M due to extra benefits under long-term incentive schemes, offset by a €9.9M decline on other admin expenses. We then see a €1.1M growth in amortisation before an €8.3M increase in rationalisation costs were more than offset by a €22M gain on the disposal of an associate which pushed the operating profit up €11.8M when compared to 2014. Finance income grew, mainly as a result of increased interest receivable on a vendor loan note and income tax was lower to the tune of €1.3M to give a profit for the year of €77.3M, a growth of €13.8M year on year.

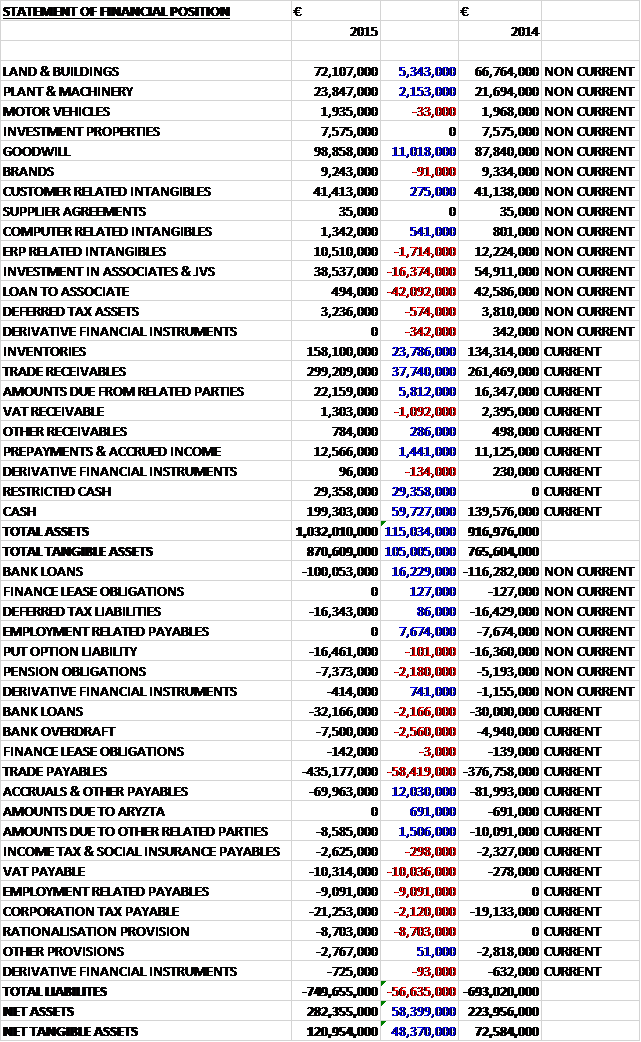

When compared to the end point of last year, total assets increased by €115M, driven by a €59.7M growth in cash, a €37.7M increase in trade receivables, a €29.4M increase in restricted cash relating to money set aside in an escrow account for the acquisition of Redoxim, a €23.8M growth in inventories and an €11M increase in goodwill, entirely due to forex translation differences, partially offset by a €42.1M reduction in a loan to an associate and a €16.4M decline in the investment in associates due to the disposal of Valeo. Total liabilities also increased during the year as a €58.4M growth in trade payables, a €10M increase in VAT payable, and an €8.7M growth in a rationalisation provision was partially offset by a €12M decline in accruals & other payables. The end result was a net tangible asset level of €121M, a growth of €48.4M year on year.

Before movements in working capital and payment into the pension scheme, the cash profits came in at €82.4M, a decline of €1.5M when compared to last year. The extra contributions to the pension scheme fell by €6.6M this year and payables increased by €3.9M but this was not enough to offset a big increase in receivables and a sizeable hike in inventories and after tax more than doubled to €9.4M, the net cash from operations came in at €54.9M, a decline of €20.5M year on year. The group spent €8.7M on property, plant and equipment along with €2.6M in intangible assets but they received a cash income from the disposal of their investment in an associate along with a vendor loan note which together brought it just over €87M and despite €29.4M being funnelled into restricted cash, there was a cash inflow of €104.5M before financing. The group used some €33.8M of this cash to pay off loans and €25M went on dividends to give a cash flow for the year of €45.6M and a cash level at the year-end of €191.8M.

The past year has been a difficult and demanding one for farming and farm incomes. Volatile output markets, high input costs and tightening farm credit can frequently challenge the sustainability and viability of farm enterprises. There is a current bearish crop cycle which coupled with reduced seasonal intensity resulted in lower overall market demand for services and inputs during the year. Against this backdrop the group have achieved a satisfactory result in line with expectations.

The segment result from the agri-service division was £78.9M, a decline of £618K year on year with a €2.6M decline on a like for like basis. As far as integrated on-farm agronomy is concerned, in the UK, Agrii delivered a solid performance against the backdrop of overall lower farm spending. While sales margins were decent, trading conditions limited service revenue and volumes, particularly in Q4. A combination of slower crop development, reflecting reduced seasonal intensity due to lower average temperatures and the backdrop of weaker output markets caused a cautious attitude to investment spend by farmers during the year.

Total winter and spring plantings for the principal arable, root and vegetable crops were some 1.2% behind 2014 levels at approximately 4.34M hectares. A noticeable switch by growers from higher yielding winter plantings to less intensive spring sown crops was evident and largely reflected demand for disease management and grass weed control which resulted in a 2.7% reduction in the winter planted area and a 2.5% increase in the spring planted area.

Good progress was achieved in the further agronomising of Agrii’s seed and nutrition portfolios which contributed to improved sales margins in the period. Key focus areas include an improved mix of value added applications that incorporate nutrient mapping, high spec seed advice and varietal selection, precision applications and variable rate input prescriptions.

In Poland, Dalgety achieved an improved performance, recording higher margins and profits. Increased agronomy revenues reflect the benefit of an early spring season and a favourable cropping profile. Total planted area for the principal cereals and oil seed crops was in line with last year at 8.7M hectares. An increased level of winter cereal sowings was offset by lower spring maize plantings, largely as a result of below average yield performance from spring cropping in 2014.

Lower crop marketing revenues and volumes in the period reflected lacklustre export markets and greater competitive markets. The business recorded good growth in the intensive and technically oriented farm channel with strong progress achieved in the development of integrated and higher specification input and technology offers which was the principal driver of higher margins during the year.

In Ukraine, Agroscope has delivered a resilient performance in its first full year of operations as part of the group. Higher revenues and profits reflect solid progress achieved to date with the business securing favourable sales and customer development through differentiated offers that promote technology intensification. Total plantings for the 2015 production year were approximately 20.5M hectares, some 5% lower than the prior year. From an operational perspective the impact of the current political and economic uncertainty is mostly reflected in pronounced currency weakness and tightening liquidity at farm level. Underlying advice and input spend is lower compared to last year with many farm holdings migrating to cheaper investment options.

The business is adopting a cautious planning approach in light of the current uncertainty. This approach is concentrated on currency and receivables risk management and the establishment of partner programmes to implement jointly developed input financing solutions on farm. The business continued the development of its two crop technology centres in the period which now provide an established knowledge transfer platform within the business. The rollout of precision agronomy and satellite monitoring applications as part of an extended service offer was also further progressed during the year.

As far as Business to Business Agri-Inputs are concerned, the UK and Irish business achieved a solid result reflecting an overall stable volume performance in fertilizer with a marginally lower contribution from feed. Fertilizer achieved volume growth in the UK against lower market demand. This performance was supported by a combination of operational improvements underpinning strong supply chain execution and sales of customised and value added nutrition formulations achieving solid momentum during the year. The favourable volume performance across arable enterprises was partially offset by reduced fertilizer application in the case of livestock enterprises. This is principally driven by lower returns currently generated by UK primary dairy producers.

In Ireland, the abolition of milk quotas supported demand in the second half of the year with farmers focused on maximising grass production to produce higher milk volumes. The routine investment and operational improvement programmes across the group’s fertilizer blending facilities are addressing evolving structural changes in the market with just in time customer ordering systems and the requirement for enhanced technical support becoming more prevalent. The overall capability of their fertilizer offering was further enhanced during the year with the commissioning of expanded blending capacity within the UK.

The amenity business achieved a good result in the year with momentum across the professional and niche agri sectors, offsetting the impact of lower demand within the amenity channel. Performance continues to be positively supported by a combination of ongoing business process alignment, industry leading partnership programmes and focused product development dedicated to the domestic and export home and garden channels.

Feed ingredients performed resiliently in the period against a lower volume result. Reduced feed consumption for the year largely reflected a combination of increased substitute fodder availability and the impact on demand of weaker returns from dairy and beef enterprises due to lower output prices. Pronounced price and currency volatility across raw material markets in the year drove generally weaker buying sentiment and delayed customer purchasing decisions.

The segment result for the associates and joint ventures was £14.1M, a growth of £684K when compared to last year. The bulk of the contribution, and the increase in profit, came from the now-disposed of Valeo Foods which performed in line with expectations in the context of a grocery market that remains highly challenging in both Ireland and the UK. A key success factor was the performance of the business’ brands which continue to consolidate market share and maintain category leading positions. The other joint venture, John Thompson is the largest single site multispecies animal feed mill in the EU and it delivered a satisfactory performance during the year.

During the year the group disposed of its 32% interest in the consumer goods group Valeo Foods to CapVest Partners together with the settlement of the outstanding principle and accumulated interest receivable relating to the group’s vendor loan note which was put in place at the time of formation of the business. A total cash consideration of €86.6M has been received in connection with the transaction comprising €42.5M in respect of the disposal of the 32% shareholding and €44.1M in full settlement of the vendor loan note. In all, a gain of €22M arose on the transaction.

In January 2014 the group completed the acquisition of a controlling interest in Agroscope International based in Ukraine. The business is a provider of agronomy services, high spec inputs and advisory support to arable and root crop growers. The group acquired a 60% interest in the business for a cash consideration and also entered into an arrangement with the minority shareholder under which they have the right to sell the remaining 40% interest to the group based on agreed formula. The group has therefore recognised an option liability of €16.5M. After the end of the year, in September, the group acquired Redoxim and agreed to acquire Comfert in Romania and Kazgod in Poland.

The group acquired Redoxim for a total consideration of €35M, of which €31.5M was paid upon completion and €3.5M is payable on the first anniversary of the acquisition. Underling operating profit in the business last year was €5.6M. The group agreed to acquire Comfert based on an enterprise value of €19.4M and additional deferred consideration will be payable based upon the achievement of specific annual profit targets over a five year period. The transaction is subject to a number of conditions including clearance from the Romanian Competition Council and is expected to complete in October 2015. Last year the business made an underlying operating profit of €3.2M.

The group also agreed to acquire Kazgod in Poland based on an enterprise value of €22.4M with about €20.3M of the total consideration payable on completion with €2.1M deferred and payable three years following completion. Last year the business recorded EBITDA of €1.2M and tangible integration benefits across Kazgod and Dalgety are targeted are targeted to be achieved over the three year period following completion. The transaction is subject to a number of conditions including clearance from the Office for the Protection of competition and Consumers in Poland and is expected to be completed in December 2015.

There were a number of other non-underlying costs which include rationalisation costs comprising termination payments arising from the restructuring of agri-services in the UK. The transaction costs relate to expenses arising on the acquisition of Redoxim and Comfert, along with Kazgod.

During the year the group recorded pension costs comprising of a settlement gain of €1.3M arising on the closure of two of their Irish-based defined benefit schemes, and costs of €500K in relation to the merger of the UK based defined benefit schemes. Other costs in the year relate to the movement in fair value of the put option liability in respect of the Agroscope acquisition. The exceptional costs arising in associates and joint ventures relate to the group’s share of redundancy, acquisition and financing costs arising in Valeo.

The group’s currency is the Euro but in addition to sales in Euro countries, the group sells a considerable amount into the UK as well as smaller operations in Poland and Ukraine. In addition they purchase from suppliers denominated in US dollars which exposes the group to currency differences. A 10% strengthening of the US dollar against the Euro would reduce profits by €241K while a 10% weakening of Sterling against the Euro would reduce profits by €23K. There is also some susceptibility to interest rate rises with a 50 basis point increase giving rise to a cash outflow of €336K for the year.

It is worth noting that an incredible 90% of earnings are made in the second half of the year so the interim results are nearly meaningless for this company. Also the group is now exposed to political risk overseas, particularly with the precarious situation in Ukraine. The group’s largest shareholder is ARYZTA AG, a Swiss-based food business who have 29% of the total share capital. At the start of the year ARYZTA was the controlling shareholder with 68% of the share capital and placed 49M shares over the course of 2015. Some of the directors of Origin are also investors in ARYZTA.

The group operates a number of defined benefit pension schemes and defined contribution schemes. All of the defined benefit schemes are closed to new members and the total deficit in the schemes currently stands at €7.4M. During last year, following discussions with the trustees, the company ceased its liability to contribute to two of its Irish based defined benefit schemes and a payment of €6.5M was made in full and final settlement of their obligation and resulted in a termination gain of €1.3M in the prior year. Although the deficit is not really that material to a company of this size, it is worth bearing in mind that the present value of scheme obligations is €107M. Overall though, I don’t think there is anything to be concerned about regarding these schemes.

Going forward, primary output markets continue to remain under sustained pressure with near term visibility on new price direction unlikely before mid-2016. This weaker backdrop is impacting farm sentiment and a lower demand profile for services and inputs is anticipated for 2016.

At the current share price the shares trade on a PE ratio of 15.6 which reduces to 13.2 on next year’s consensus forecast. At the end of the year the shares have a net cash of €88.8M compared to a net debt position of €11.9M at the end of last year although the year-end represents a low point in the group’s debt and the low point in the working capital cycle of the group, and average net debt amounted to €186M during the year. After a 5% increase in the dividend, the shares currently yield 3.1% which is expected to remain the same next year.

On the 27th November the group released an update covering trading in Q1 2016 where they report a slower start to the year for the seasonally quiet quarter. This performance is attributed to a delay in new season activity on farm during August and September as weather interruption slowed the 2015 harvest resulting in the later timing of service and input application in respect of the winter crop planting programmes.

New season activity levels on farm were robust in the latter part of the period with strong winter crop planting progress achieved during October and the total sown area for the principal winter crops is broadly in line with last year across the majority of markets. The generally weaker output price backdrop and the associated cash flow pressure on farm are expected to result in more concentrated purchasing patterns by primary producers. Accordingly, farmer decision making on crop investment spend will likely occur closer to the main application and usage period in the second half of the year – so, poor visibility of earnings then.

In Agri-Services, revenue in the quarter was €300.4M, a decline of 5.5%. This figure was flattered by favourable exchange rates, however, and the underlying decrease was 9% driven by lower fertilizer and crop protection volumes. The division performed satisfactorily in the UK against the backdrop of slower new season activity levels on farm. A weather interrupted harvest largely contributed to delayed in-field operations which limited early season agronomy revenue development in the period. Favourable weather towards the end of the quarter, however, supported good in-field conditions which resulted in significant catch up crop drilling activity.

Winter plantings are well advanced with current estimates for the total winter sown area at 3.05M hectares compared with 3.09M in 2014. In the case of winter wheat there is an estimated 2.5% increase in sown area to 1.9M hectares which mostly offset a 12% reduction in the winter oil seed rape area to 572K hectares. The sown areas for the remaining winter crops are about the same as last year. Crops are well established and in good condition with growing conditions to date providing for a more normalised level of seasonal growing intensity than last year.

Harvest yields are above average and providing support to cost recovery for primary producers. The group’s service and input portfolios continue to perform resiliently in highly challenging and competitive trading conditions through targeted and customised agronomy programmes promoting high output management and flexible crop production systems.

In Poland, higher agronomy revenues underpinned an improved result in the period which more than offset the impact of lower crop marketing volumes and margins. Dalgety’s service and input portfolios maintained decent momentum in the period with higher specification seed varieties in particular performing strongly. Crop marketing continued to be adversely impacted by highly competitive trading conditions, principally in export markets.

Harvest yields to date are below average and reflect the impact of unseasonal high temperatures over the summer period on maize cropping in particular. There was good progress in respect of winter sowings in the period with final plantings for the principal winter crops estimated at 5.6M hectares compared with 5.8M in 2014 but combined winter and spring plantings are expected to be broadly equivalent to last year. The acquisition of Kazgod was completed in November.

The group’s Ukraine operation recorded higher early season agronomy revenues underpinning an improved Q1 performance. Market conditions continue to be adversely impacted by the current political uncertainty, however, which is reflected in currency weakness and tightening liquidity on farm. The business remains well positioned, though, and has made good progress in securing advance customer commitments in respect of the main application season in the second half of the year.

Sustained drought conditions over the summer period have reduced 2015 harvest yields and significantly impacted the level of winter plantings. Farm management programmes are now focused on increased spring sowings and underlying crop investment spend for the 2016 production year is expected to be lower with the combined total for winter and spring plantings forecast to be equivalent to last year at 20.5M hectares.

In Romania the acquisition of Redoxim was completed in September and the business has achieved a satisfactory performance in the period as integration systems and process planning was started. The acquisition of Comfert has been cleared by the Romanian competition council and is expected to complete in Q2.

Business to business Agri inputs recorded lower revenues in the quarter due to slower fertilizer volume development which was partially offset by the benefit of higher feed volumes. Fertilizer consumption in Ireland was in line with the same period of last year with primary dairy producers investing in nutrition programmes prior to the end of the grass growing season. Fertilizer deliveries in the UK were lower, however, in part relating to an element of seasonal timing due to the later harvest. More importantly, the reduction reflects delayed customer purchasing decisions until closer to the main application period in the second half pending greater visibility on pricing and crop development. Overall the group is anticipating lower market volumes for the year as a whole.

Feed ingredients achieved higher volumes in the period with customers taking advantage of favourable pricing opportunities and the amenity business which provides advice and input solutions to the sports turf, landscaping and amenity sectors, performed satisfactorily in the period, underpinned by solid development momentum across the professional and nice agri sectors. The joint venture, John Thompson, delivered a satisfactory performance during the quarter.

Going forward, the weaker market backdrop for primary producers and the associated pressures on farm incomes makes for a challenging backdrop for service and input demand in 2016. The board anticipate an increased level of seasonality in H2, reflecting more concentrated purchasing patterns by primary producers. The current autumn cropping profile provides a strong foundation for the seasonally more important second half, however. At this stage in the year, the board expects to achieve full year adjusted EPS of between 51c and 53c.

Overall then, this has been a mixed year for the group. Profits were up, but this was due to the gain on the disposal of the associate and excluding this, profits fell due to higher rationalisation costs. Net assets did increase but operating cash flows were down, not helped by a large increase in receivables. The group remained comfortably cash generative, however. Looking at the performance in Q1, there was a slower start to the year due to a delay in new season activity which is weather related and led to lower sales of fertilizer and crop protection products. The performance was better in Poland and Ukraine, however, although continued economic problems in the latter must be considered.

Going forward, the board see a challenging 2016 ahead which is characterised by lower earnings visibility as a result of falling output prices. With a forward PE of 13.2 and yield of 3.1%, the shares are not that expensive but look priced about right given the difficulties the industry is currently facing.