Empresaria has now released their final results for the year ended 2015.

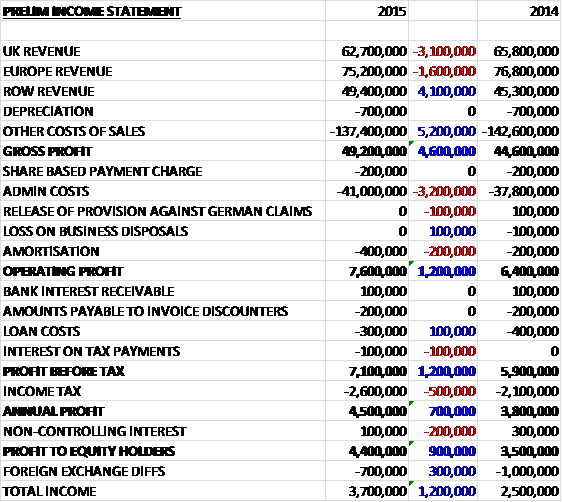

There was a modest fall in revenues when compared to last year due to currency headwinds and the decision to reduce exposure to some low margin business as a £3.1M decline in UK revenue and a £1.6M fall in European revenue was mostly offset by a £4.1M growth in ROW revenue. Cost of sales declined, however, to give a gross profit £4.6M ahead of last year. Admin costs increased by £3.4M, including a £200K growth in amortisation, which meant that the operating profit grew by £1.2M when compared to 2014. Finance costs remained steady but tax increased by £500K which gave a profit for the year of £4.4M, an increase of £900K year on year.

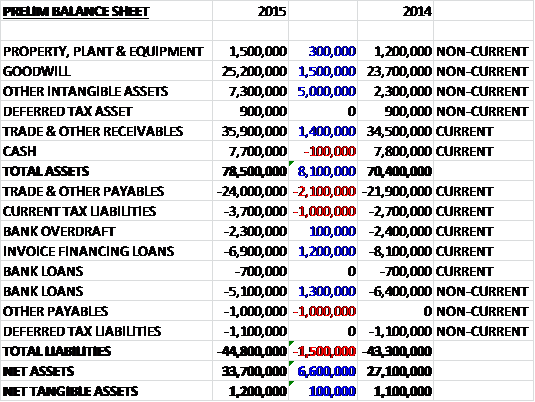

When compared to the end point of last year, total assets increased by £8.1M driven by a £5M growth in intangible assets, a £1.5M increase in goodwill and a £1.4M growth in receivables. Total liabilities also increased during the year as a £2.1M growth in current payables, a £1M growth in non-current “other” payables and a £1M increase in current tax liabilities were partially offset by a £1.3M decline in the bank loans and a £1.2M decrease in invoice financing loans. The end result is a net tangible asset level of just £1.2M, an increase of £100K year on year.

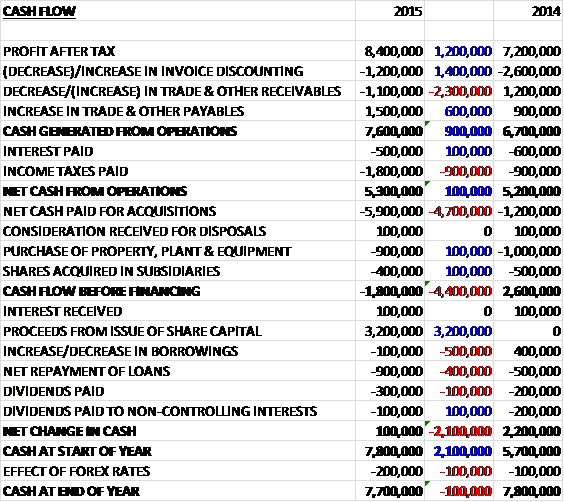

Before movements in working capital, cash profits increased by £1.2M to £8.4M. There was a cash outflow through working capital with an increase in receivables and tax paid was £900K higher than last time to give a net cash from operations of £5.3M, an increase of £100K year on year. The group spent £900K on property, plant and equipment and £400K of shares in the subsidiaries before a £5.9M payment for acquisitions meant that there was a cash outflow of £5.9M before financing. The group then issued new shares which netted them £3.2M which was used to pay back £1M of loans and pay out £400K in dividends so that the cash flow the period was £100K and the cash level at the year-end was £7.7M.

NFI from temporary recruitment was down 1.5% due to a 3.5% reduction in sales, partially offset by improved margins. Permanent sales, including the offshore recruitment business, now account for 45% of NFI. Nearly half of NFI is earned from the technical and industrial division.

The operating profit in the UK division was £2.1M, a decline of £100K year on year on revenues that declined by 5% due to the deliberate move away from low value work in the Technical and Industrial sector. The lower paid end of this sector has been heavily impacted by changes in legislation with false self-employment legislation implemented in April 2014 and new travel and subsistence rules in place from April 2016. Their approach to transition away from the generalist market and increase their presence in professional and specialist roles has helped offset the impact of this to a certain extent but there has been a short-term profit impact with a lower contribution from this sector this year.

Excluding this sector, there was revenue growth of 27% with a particularly strong result from the professional services sector, aided by improved conditions in the banking sector and ongoing growth in the HR and secretarial areas. They also saw a full year contribution from Ball and Hoolahan which was acquired at the end of last year as the business was integrated into the Become group. The board have plans to grow the brand’s presence across the network over the next few years. There were also positive performances from their brands in domestic services and retail.

NFI actually increased by 16% to £18.4M but due to the above mentioned move away from the lower margin work there was a reduction in conversion ratio. In addition, they saw increased costs in Q4 from three brands moving office which has caused an increase in rent costs and one-off moving expenses.

The operating profit in the Continental Europe division (mostly Germany) was £3.7M, a growth of £700K when compared to last year. This is due to the Headway business in Germany and Austria where revenue growth is coupled with a more appropriate cost base with the German economy growing this year and business confidence remaining positive into 2016.

The healthcare business in Finland is making good progress with its move away from the import model which is reliant on Estonian staff working in Finland, to a local model. Costs were removed with the closure of a physical presence in Estonia and whilst the group will continue to place Estonian staff, they expect the mix to be in favour of Finnish workers by the end of 2016. The local economic conditions remain weak but the board are pleased with the progress being made.

Due to the weakness of the Euro, currency rates have negatively impacted profits with growth in constant currency being £300K higher. In line with their strategy to exit businesses without strong growth prospects, they finalised the exit of the loss making business in the Czech Republic via a disposal, and in Slovakia which was closed down.

The operating profit in the ROW division was £1.8M, an increase of £600K when compared to 2014 following investments made last year with the new offices all delivering improved contributions. There were mixed performances across the region with the established markets in Japan and Australia performing well along with Thailand, Chile and India.

In India the offshore recruitment services business has seen significant growth with staff numbers at the end of the year up 65% on the prior year. The plan to open a third office in 2016 was brought forward due to high demand, opening in November 2015. This business mainly services clients in the US and UK with a focus on IT and healthcare and the board see good opportunities for continued growth over the coming year.

Market conditions in SE Asia and China have been mixed. In Indonesia they have seen business confidence dented by worsening economic conditions. The executive search business saw slightly lower profit levels and the training business has been restructured to reflect the lower sales level. The majority of this programme has been completed in the year and the management team has been strengthened so the board expect to see a market improvement in performance in 2016.

In Thailand they have seen strong growth and there have been improved performances in the Philippines, Malaysia and Singapore. The group have a small presence in China which has been restructured and rebranded and they see good prospects moving into 2016 with a greater emphasis on Chinese clients rather than multinational companies. In January 2015 the small stand-alone brand in Malaysia was sold to management and they now operate in that market through the Monroe Consulting brand which is making good progress.

On October the group purchased Pharmaceutical Strategies, a US staffing company specialising in the pharmacy benefit management sector of the US healthcare market. The initial consideration is £4.7M with £2.7M of deferred consideration payable in 2016 and a further £500K of contingent consideration for future years, making a total consideration of £7.9M. The acquisition generated goodwill of £2.2M and the business contributed £100K to profits in the two and a bit months following the acquisition and if it had been purchased at the start of the year, it would have delivered £200K to the group’s profit. It is worth noting that due to their high levels of debt, the group had to issue further equity in order to make this acquisition.

The business specialised in providing qualified pharmacists and nurses to the healthcare sector, in particular to the pharmacy benefit management companies. The sector is undergoing high growth rates due to the implementation of the Affordable Care Act and the investment also takes the group into a new geography and provides a base for their other brands if they want to enter the US market (something that shouldn’t be undertaken lightly in my view). In any case, the business is expected to deliver a good uplift in profit in 2016, having integrated well into the group.

Apart from the main acquisition there were a number of other investments and disposals during the year. The group purchased 10% of PT Monroe Consulting in Indonesia for £300K, taking their total interest to 90%; and they purchased 9% of Mansion House in the UK for £100K, taking their total shareholding to 67%. They received £100K in deferred consideration from the disposal of the Bar 2 payroll business in 2013, and the disposals of Metis and January this year and GiT in March. In addition the group made a deferred consideration of £500K for the purchase of 75% of shares in Ball & Hoolahan in September which represented the maximum amount payable under the sale and purchase agreement.

The group uses a debt to debtors ratio throughout the report which is not something I have seen before. Anyway, they have achieved their target in this metric so it doesn’t look as though debt reduction is much of a priority going forward which is a little bit of a shame in my view.

The board see exciting opportunities across the group in spite of current global uncertainty and are confident in their ability to deliver profitable growth in 2016, benefiting from the investments made in existing brands and the purchase of Pharmaceutical Strategies.

At the year end, the group had a net debt position of £7.3M compared to £9.8M at the end of last year. At the current share price the shares are trading on a PE ratio of 9.5 which falls to 8.3 on next year’s consensus forecast. After a 43% increase in the final dividend, the shares are now yielding 1.1% which is nothing to get excited about.

Overall then, this has been a year of progress for the group. The profit increased although the net tangible asset level remained flat, as did the operating cash flow due to a higher tax payment and increase in receivables – cash profits did increase and before acquisitions there was a decent level of free cash produced. There was a good performance in mainland Europe despite the weakness of the euro as revenues increased and costs fell in the Germany business which seems to have performed very strongly. There was also a good performance in the ROW business as weakness in Indonesia and China was more than offset by growth in Thailand and India. There was some weakness in the UK, however, as the group moved away from some lower margin business.

The Pharmaceuticals Strategies acquisition seems decent enough but there are some risks involved with this as the US is a tough nut to crack. Also, I prefer businesses that grow using their own cash flow rather than raising equity and diluting shareholders – the net debt is also quite high here so they are probably growing quicker than they should in my view. The dividend is nothing to write home about, as should be the case given the debt and the acquisition policy but the forward PE ratio of 8.3 is looking cheap. This is a tricky one as I am tempted to buy some shares as a bit of a value play. I will have a think!

On the 29th April the group announced that is acquired the remaining 25% interest in Ball and Hoolahan for £250K from Roy Hoolahan as part of a planned succession. Marc Sigrist, who joined B&H as operations director in December will replace Roy as MD. The business generated pre-tax profit of £300K last year.

On the 5th May the group announced that it had made a good start to the year with growth in NFI compared to the same period of 2015. They have seen particularly good trading in Germany, Japan, India and Chile. The US based Pharmaceuticals Strategies is performing well and recent new client wins give the board confidence that it will deliver full year profits in line with their expectations. They do continue to look for further acquisitions which makes me a little nervous but overall the group remains on course to meet market expectations for the full year so steady as she goes then.

On the 1st June the group announced that it had acquired a further 10% of the shares in Monroe Consulting Thailand for a cash consideration of £200K. They now hold a 70% interest in the business which generated a pre-tax profit of £400K last year.

On the 5th July the group announced the acquisition of 82.6% of Rishworth for a total consideration of £7.5M with the rest remaining in the hands of the senior management team. The business is a specialist recruitment group headquartered in New Zealand with a regional office in Sweden, providing pilots and aviation personnel to clients across the globe with a significant presence in Europe, Africa and Asia supplying businesses such as Norwegian, Korean Air and Vietnam Airlines. It is a 100% contract recruitment business with pilot contracts typically lasting between three and five years.

Last year the business made NFI of £4.7M and adjusted EBIT of £1.9M and the board believe the acquisition will be earnings enhancing this year. It is difficult to ascertain how much goodwill will be generated but I think since Rishworth has net liabilities of £451K, this will be nearly £8M. This looks to be a useful acquisition but I feel EMR is looking a bit stretched with regards to debt and the balance sheet so I am not rushing to buy the shares.

On the 21st July the group released a trading update covering the first half of the year. The group is continuing to perform well and is on course to meet market expectations for the full year.

NFI in the first half was up 13% and the group has seen particularly strong trading in Continental Europe, Asia Pacific and the Americas, especially in Germany, Japan, India, Chile and China. The investment in Pharmaceutical Strategies in performing in line with expectations.

In the UK there was a slowdown in May and June as business confidence dropped in the run up to the EU referendum. Following the Brexit result, it has stabilised and sales pipelines are holding up well. Being a globally diversified business they are well positioned to manage the effects of a slowdown in any particular sector or geography. Whilst they are monitoring the short term outlook for the UK, they see strong growth opportunities across the group and will benefit from the effect of current exchange rates as overseas earnings are translated into Sterling.

Whilst there is general uncertainty in the UK markets, this accounts for less than a third of business and overall this is a pretty decent update.